Resources

About Us

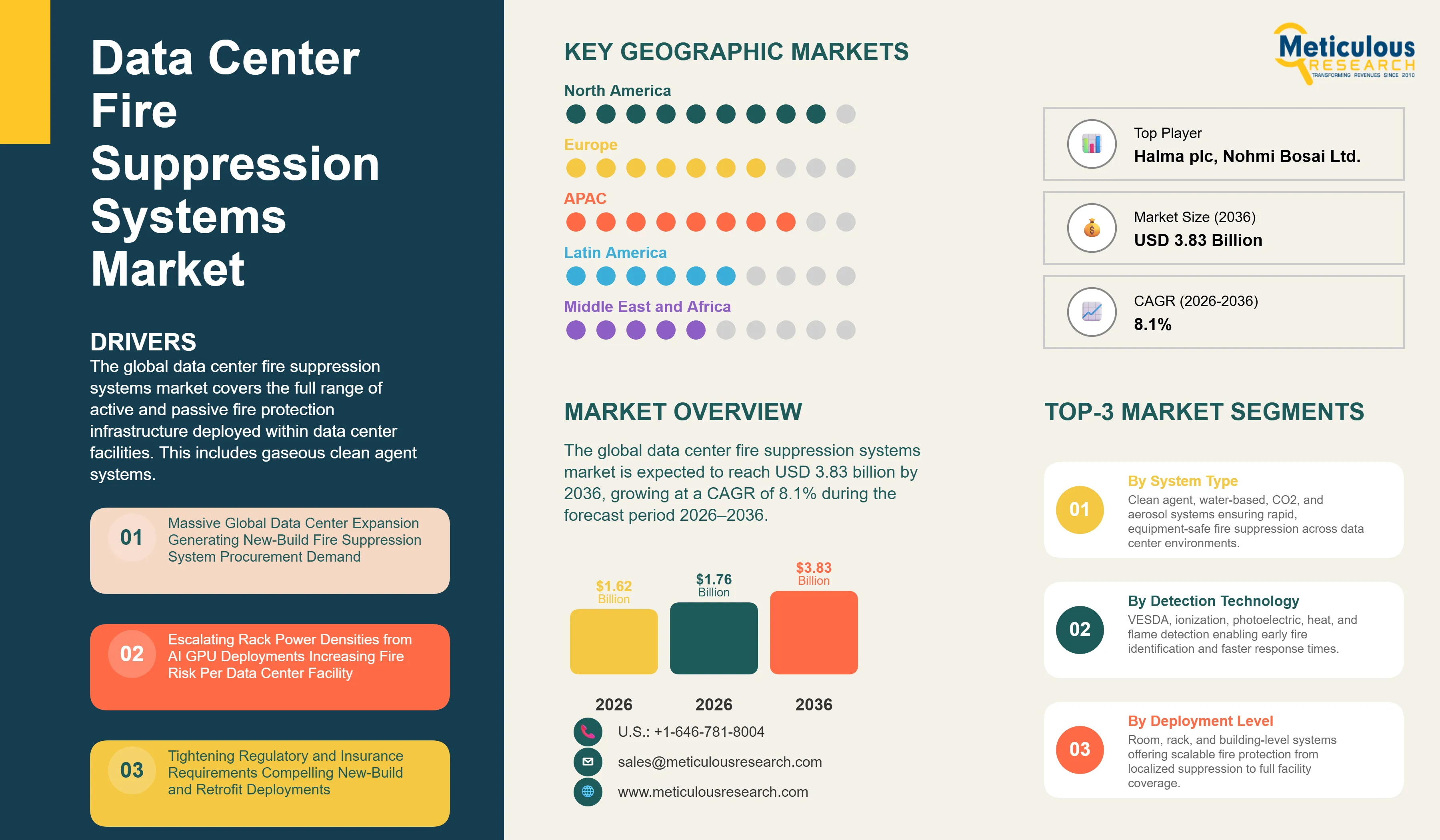

The global data center fire suppression systems market was valued at USD 1.62 billion in 2025. This market is expected to reach USD 3.83 billion by 2036 from an estimated USD 1.76 billion in 2026, growing at a CAGR of 8.1% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global data center fire suppression systems market covers the full range of active and passive fire protection infrastructure deployed within data center facilities. This includes gaseous clean agent systems, water-based sprinkler and mist systems, CO2 and aerosol-based solutions, as well as associated detection technologies, control panels, alarm systems, and monitoring services. Collectively, these systems are designed to protect critical data center assets from fire-related operational, financial, and reputational risks.

Fire suppression systems are mandatory under established safety standards such as NFPA 75, NFPA 76, EN 15004, and applicable local building codes across major data center markets. As a result, fire protection infrastructure represents a non-discretionary investment for data center operators, forming an essential component of all new facility construction and periodic upgrade cycles.

The growth of the global data center fire suppression systems market is primarily driven by the rapid expansion of hyperscale and colocation data center capacity worldwide. This expansion is generating significant new-build demand for advanced fire suppression systems across all facility types.

In addition, the increasing deployment of high-density AI and GPU server configurations is elevating thermal loads and electrical fault risks, necessitating more robust and responsive fire protection solutions. Tightening global fire safety regulations and insurance requirements are further compelling operators to upgrade both new and existing facilities with compliant suppression systems.

However, the market faces certain constraints. Clean agent fire suppression systems involve high installation and recharge costs, mainly in large hyperscale environments that require substantial volumes of pressurized agents.

Moreover, increasing regulatory restrictions on high global warming potential fluorinated agents, such as HFC-227ea under the EU F-Gas framework, are limiting the use of certain legacy suppression technologies and increasing compliance complexity.

Despite these challenges, several growth opportunities are emerging. The adoption of AI-enabled very early smoke detection systems and IoT-based fire safety monitoring solutions is enabling predictive risk analytics and faster incident response.

Additionally, hybrid fire suppression approaches, combining gaseous agents with water mist systems, are gaining traction, mainly for managing lithium-ion battery-related fire risks in data center environments. The expansion of edge and micro data centers is also driving demand for compact, modular fire suppression solutions tailored to space-constrained deployments.

A key trend shaping the market is the integration of fire suppression monitoring with data center infrastructure management (DCIM) platforms. This integration enables unified visibility, centralized control, and improved operational efficiency, supporting more proactive and data-driven fire safety management across modern data center environments.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 3.83 Billion |

|

Market Size in 2026 |

USD 1.76 Billion |

|

Market Size in 2025 |

USD 1.62 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 8.1% |

|

Dominating System Type |

Clean Agent Systems |

|

Fastest Growing System Type |

Water Mist Systems |

|

Dominating Detection Technology |

VESDA/Aspirating Smoke Detection |

|

Dominating Deployment Level |

Room/Hall Level |

|

Fastest Growing Deployment Level |

Rack/Cabinet Level |

|

Dominating Data Center Type |

Hyperscale |

|

Fastest Growing Data Center Type |

Edge & Micro Data Centers |

|

Dominating End Use |

IT & Telecom |

|

Fastest Growing End Use |

Healthcare |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

AI-Driven VESDA Integration with DCIM Platforms for Predictive Fire Risk Management

The integration of very early smoke detection apparatus (VESDA) with data center infrastructure management (DCIM) platforms is transforming fire protection from a reactive emergency response function into a continuous, predictive risk management capability. By correlating smoke particle data with server operations, airflow dynamics, and thermal sensor inputs, these systems enable real-time fire risk analytics and earlier detection of potential incidents.

Solutions from Honeywell International Inc. and Siemens AG now offer API-level integration with major DCIM platforms, allowing operators to monitor fire risk alongside key performance metrics such as power usage effectiveness, cooling efficiency, and server utilization within a unified operational framework.

This integration is driving a sustained upgrade cycle, as legacy standalone fire detection systems are increasingly replaced with DCIM-integrated architectures. The trend is especially evident in hyperscale and AI-optimized data centers, where early warning capabilities and system-wide operational visibility are critical for maintaining uptime and managing high-density compute environments.

Lithium-Ion Battery Thermal Runaway Creating New Hybrid Suppression System Requirements

The rapid deployment of large-scale lithium-ion battery energy storage systems within and adjacent to data center facilities is creating new fire suppression requirements that conventional gaseous clean agent systems and traditional water-based sprinkler systems cannot fully address on their own. As battery energy storage becomes integral to data center power architectures, fire protection strategies are evolving to accommodate the unique risks associated with lithium-ion technologies.

Lithium-ion thermal runaway involves self-sustaining exothermic reactions that cannot be effectively suppressed through oxygen displacement, the primary mechanism of gaseous clean agent systems. Instead, these events require continuous cooling to reduce cell temperatures below the propagation threshold, making water-based suppression methods essential for effective mitigation.

As a result, an emerging best-practice approach is the adoption of hybrid fire suppression architectures. These systems combine water mist or direct water application for battery cooling and heat dissipation with gaseous clean agent systems deployed in surrounding areas to protect IT equipment. This hybrid model is driving simultaneous growth in both water-based and clean agent fire suppression segments within data center environments.

Rack-Level Micro-Suppression Systems for High-Density AI GPU Configurations

The adoption of in-rack micro suppression systems, incorporating miniaturized clean agent or inert gas dispensers integrated directly within server rack enclosures, is increasing as data center operators deploy high-density AI GPU configurations. In such environments, conventional room-level suppression systems can lead to disproportionate operational disruption when responding to localized fire incidents.

Rack-level suppression systems detect smoke or heat within individual enclosures and release a precisely metered quantity of suppression agent to extinguish the fire at its source. This targeted response avoids triggering full room-level discharge, thereby preserving operational continuity in adjacent racks and minimizing downtime.

This category is emerging as a fast-growing deployment-level segment within the fire suppression market. It represents a new procurement layer that complements existing room-level systems, rather than replacing them, especially in high-density and AI-optimized data center environments.

By System Type: In 2026, the Clean Agent Systems Segment to Dominate the Global Data Center Fire Suppression Systems Market

Based on system type, the global data center fire suppression systems market is segmented into clean agent systems (FM-200/HFC-227ea, Novec 1230/FK-5-1-12, inert gas systems), water-based systems (pre-action sprinklers, water mist), CO2 systems, and aerosol-based systems.

In 2026, the clean agent systems segment is expected to account for around 55–60% of the global data center fire suppression systems market, making it the largest technology segment. The large share of this segment is attributed to the universal preference of data center operators for electrically non‑conductive, residue‑free gaseous suppression agents, particularly Novec 1230, FM‑200, and inert‑gas blends, that can extinguish fires within approximately 10 seconds without damaging sensitive IT equipment, without creating secondary water damage, and without interrupting operations in adjacent zones. Clean agent systems are widely treated as the de‑facto standard specification in hyperscale and colocation data center fire‑protection programs globally.

However, the water mist systems segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the growing adoption of high‑pressure water mist as a sustainable, environmentally compliant suppression alternative, using approximately 90% less water than traditional sprinklers while still ensuring minimal operational disruption, and the emerging application of water‑mist hybrid systems for lithium‑ion battery thermal‑runaway suppression in data center BESS deployments.

By Detection Technology: In 2026, the VESDA/Aspirating Smoke Detection Segment to Hold the Largest Share

Based on detection technology, the global data center fire suppression systems market is segmented into VESDA/aspirating smoke detection, ionization smoke detection, photoelectric smoke detection, heat detection, and flame detection.

In 2026, the VESDA/aspirating smoke detection segment is expected to account for the largest share of the global data center fire suppression systems market. The large market share of this segment is attributed to the universal specification of VESDA and equivalent aspirating smoke detection systems by hyperscale and Tier 3+ colocation operators who require the earliest possible warning of developing fire conditions in high-value, continuously operational IT environments.

By Deployment Level: In 2026, the Room/Hall Level Segment to Hold the Largest Share

Based on deployment level, the global data center fire suppression systems market is segmented into room/hall level, rack/cabinet level, and building level.

In 2026, the room/hall level segment is expected to account for the largest share of the global data center fire suppression systems market, highlighting the foundational role of data hall-level gaseous clean agent flooding systems as the primary suppression technology across all data center types. Room/hall level suppression indicates the highest per-installation procurement value and is the mandatory baseline specification for all new data center construction across all major regulatory jurisdictions.

However, the rack/cabinet level segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the growing adoption of in-rack micro-suppression systems for high-density AI GPU server configurations that require localized suppression capability to avoid the operational disruption of full data hall agent discharge for a contained rack-level fire event.

By Data Center Type: In 2026, the Hyperscale Segment to Account for the Largest Share

Based on data center type, the global data center fire suppression systems market is segmented into hyperscale, colocation, enterprise, and edge and micro data centers.

In 2026, the hyperscale segment is expected to account for the largest share of the global data center fire suppression systems market. This dominance is driven by the scale of fire suppression procurement at hyperscale AI campuses, where each 100+ MW facility requires coverage across multiple data halls, UPS and BESS rooms, and extensive support infrastructure. These deployments generate significant system-level spending per campus, making hyperscale operators and cloud providers the largest and most technically demanding buyers of fire suppression solutions.

However, the edge and micro data centers segment is projected to register the highest CAGR during the forecast period. This growth is driven by the proliferation of distributed edge locations supporting 5G networks, industrial AI, and autonomous systems. These deployments require compact, self-contained fire suppression solutions suited to space-constrained and remotely operated environments, where conventional room-level systems are often impractical.

By End Use: In 2026, the IT & Telecom Segment to Hold the Largest Share

Based on end use, the global data center fire suppression systems market is segmented into IT and telecom, BFSI, government and defense, healthcare, energy and utilities, retail and e-commerce, and other end uses.

In 2026, the IT and telecom segment is expected to account for the largest share of the global data center fire suppression systems market. This segment includes hyperscale cloud providers, telecommunications carriers, colocation operators, and IT infrastructure companies, collectively representing the largest buyers of fire suppression systems. These organizations deploy advanced detection and suppression technologies to safeguard high-value IT assets and ensure compliance with strict service level agreements.

However, the healthcare segment is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing adoption of AI-enabled clinical applications that require dedicated on-premises data center infrastructure. In addition, stringent fire safety regulations in healthcare facilities are driving the adoption of high-specification fire suppression systems that exceed standard commercial data center requirements

Based on geography, the global data center fire suppression systems market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global data center fire suppression systems market. This dominant position is attributed to the highest global density of hyperscale data center deployments, which generate the largest fire‑suppression procurement volumes; a highly stringent regulatory framework under NFPA 75 and NFPA 76; and a mature ecosystem of fire‑suppression manufacturers and specialist data center fire‑protection integrators.

However, Asia Pacific is expected to register the fastest growth rate during the forecast period. China leads the regional growth, with the highest CAGR projected from 2026 to 2036, driven by large‑scale investments in hyperscale and AI‑optimized data centers and the tightening of Chinese fire‑safety standards for critical IT infrastructure. India follows, with data center capacity expected to grow substantially over the coming years, each megawatt of power‑densified capacity requiring compliant fire‑suppression systems for data halls, UPS rooms, and support spaces.

Japan, Singapore, and South Korea are also contributing to regional growth through sustained data center investment anchored to national digital‑infrastructure strategies and increasingly stringent fire‑safety compliance requirements.

The global data center fire suppression systems market is moderately consolidated, with competition focused on suppression‑agent performance and regulatory‑compliance credentials, detection‑technology sensitivity, system‑integration capability with DCIM and building‑management systems, geographic installation and service‑network coverage, and the ability to design and certify fire‑suppression systems for complex, multi‑zone hyperscale data center environments.

Honeywell International is a leading global provider through its Notifier, Gamewell‑FCI, and Gent detection and suppression platforms, catering to a broad range of hyperscale and large‑scale data center customers.

Johnson Controls competes through its Ansul, Tyco, and Simplex brands, with strong positions in colocation and enterprise data center fire‑protection markets.

Siemens AG offers its Sinteso and Cerberus fire‑safety platforms, with particularly strong positioning in the European data center segment.

The report offers a competitive analysis based on an extensive assessment of the leading players’ product portfolios, geographic presence, and key growth strategies adopted in the last few years. Some of the key players operating in the global data center fire suppression systems market are Honeywell International Inc. (U.S.), Johnson Controls International plc (Ireland), Siemens AG (Germany), Carrier Global Corporation (U.S.), Eaton Corporation plc (Ireland), Fike Corporation (U.S.), Robert Bosch GmbH (Germany), Minimax Viking Group (Germany), ORR Protection Systems (U.S.), Halma plc (U.K.), Hochiki Corporation (Japan), Nohmi Bosai Ltd. (Japan), Kidde Fire Systems (U.S.), SEM‑SAFE (Denmark), and Securiton AG (Switzerland).

The global data center fire suppression systems market is expected to reach USD 3.83 billion by 2036 from an estimated USD 1.76 billion in 2026, at a CAGR of 8.1% during the forecast period 2026–2036.

In 2026, the clean agent systems segment is expected to hold the largest share of the global data center fire suppression systems market.

The water mist systems segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by adoption as an environmentally compliant alternative and effective lithium-ion battery thermal runaway suppression solution.

In 2026, the room/hall level segment is expected to hold the largest share of the global data center fire suppression systems market.

In 2026, the IT and telecom segment is expected to hold the largest share of the global data center fire suppression systems market.

The growth of this market is driven by the massive global expansion of data center capacity generating new-build fire suppression demand, the escalating rack power densities from AI GPU deployments increasing fire risk per facility, and tightening regulatory and insurance requirements.

Key players are Honeywell International Inc. (U.S.), Johnson Controls International plc (Ireland), Siemens AG (Germany), Carrier Global Corporation (U.S.), Eaton Corporation plc (Ireland), Fike Corporation (U.S.), Robert Bosch GmbH (Germany), Minimax Viking Group (Germany), ORR Protection Systems (U.S.), Halma plc (U.K.), Hochiki Corporation (Japan), Nohmi Bosai Ltd. (Japan), Kidde Fire Systems (U.S.), SEM-SAFE (Denmark), and Securiton AG (Switzerland).

Asia Pacific is expected to register the highest growth rate in the global data center fire suppression systems market during the forecast period 2026–2036.

1.Introduction

1.1. Market Definition and Scope

1.2. Currency & Limitations

1.3. Key Stakeholders

2.Research Methodology

2.1. Research Approach

2.2. Data Collection Methods

2.3. Market Estimation and Forecast Methodology

2.4. Assumptions and Limitations

3.Executive Summary

3.1. Market Overview

3.2. Market Analysis by System Type

3.3. Market Analysis by Detection Technology

3.4. Market Analysis by Deployment Level

3.5. Market Analysis by Data Center Type

3.6. Market Analysis by End Use

3.7. Market Analysis by Geography

4.Market Dynamics

4.1. Overview

4.2. Drivers

4.2.1. Massive Global Data Center Expansion Generating New-Build Fire Suppression System Procurement Demand

4.2.2. Escalating Rack Power Densities from AI GPU Deployments Increasing Fire Risk Per Data Center Facility

4.2.3. Tightening Regulatory and Insurance Requirements Compelling New-Build and Retrofit Deployments

4.2.4. Integration of Large-Scale Lithium-Ion BESS Creating New Thermal Runaway Fire Suppression Requirements

4.3. Restraints

4.3.1. High Installation and Agent Recharge Costs of Clean Agent Suppression Systems in Large Hyperscale Data Halls

4.3.2. Regulatory Restrictions on High-GWP Fluorinated Agents Including HFC-227ea Under EU F-Gas Regulation

4.4. Opportunities

4.4.1. Retrofit Market in Aging Data Center Facilities Requiring Compliant Upgrades of Legacy Suppression Systems

4.4.2. Lithium-Ion Battery Thermal Runaway Suppression Driving Demand for Hybrid Suppression Architectures

4.4.3. Compact Modular Fire Suppression Solutions for Rapidly Proliferating Edge and Micro Data Centers

4.5. Challenges

4.5.1. Complexity of Designing Multi-Zone Suppression Systems for Large Hyperscale Data Halls

4.5.2. PFAS-Related Regulatory Uncertainty Affecting Some Fluorinated Clean Agent Formulations

4.6. Porter’s Five Forces Analysis

5.Data Center Fire Suppression Systems Market, by System Type

5.1. Overview

5.2. Clean Agent Systems

5.2.1. FM-200 / HFC-227ea Systems

5.2.2. Novec 1230 / FK-5-1-12 Systems

5.2.3. Inert Gas Systems (IG-55 Argonite, IG-541 Inergen, IG-100 Nitrogen)

5.3. Water-Based Systems

5.3.1. Pre-Action Sprinkler Systems

5.3.2. High-Pressure Water Mist Systems

5.4. CO2 Systems

5.5. Aerosol-Based Systems

6.Data Center Fire Suppression Systems Market, by Detection Technology

6.1. Overview

6.2. VESDA / Aspirating Smoke Detection (ASD)

6.3. Ionization Smoke Detection

6.4. Photoelectric Smoke Detection

6.5. Heat Detection

6.6. Flame Detection

7.Data Center Fire Suppression Systems Market, by Deployment Level

7.1. Overview

7.2. Room / Hall Level

7.3. Rack / Cabinet Level

7.4. Building Level

8.Data Center Fire Suppression Systems Market, by Data Center Type

8.1. Overview

8.2. Hyperscale Data Centers

8.3. Colocation Data Centers

8.4. Enterprise Data Centers

8.5. Edge & Micro Data Centers

9.Data Center Fire Suppression Systems Market, by End Use

9.1. Overview

9.2. IT & Telecom

9.3. BFSI

9.4. Government & Defense

9.5. Healthcare

9.6. Energy & Utilities

9.7. Retail & E-Commerce

9.8. Other End Uses

10.Data Center Fire Suppression Systems Market, by Geography

10.1. Overview

10.2. North America

10.2.1. U.S.

10.2.2. Canada

10.3. Europe

10.3.1. Germany

10.3.2. U.K.

10.3.3. France

10.3.4. Italy

10.3.5. Spain

10.3.6. Ireland

10.3.7. Netherlands

10.3.8. Rest of Europe

10.4. Asia Pacific

10.4.1. China

10.4.2. Japan

10.4.3. India

10.4.4. Singapore

10.4.5. South Korea

10.4.6. Australia

10.4.7. Rest of Asia Pacific

10.5. Latin America

10.5.1. Brazil

10.5.2. Mexico

10.5.3. Rest of Latin America

10.6. Middle East and Africa

10.6.1. UAE

10.6.2. Saudi Arabia

10.6.3. South Africa

10.6.4. Rest of MEA

11.Competitive Landscape

11.1 Overview

11.2 Key Growth Strategies

11.3 Competitive Benchmarking

11.4 Competitive Dashboard

11.4.1 Industry Leaders

11.4.2 Market Differentiators

11.4.3 Vanguards

11.4.4 Emerging Companies

11.5 Market Share Analysis (2025)

12.Company Profiles

12.1. Honeywell International Inc.

12.2. Johnson Controls International plc

12.3. Siemens AG

12.4. Carrier Global Corporation

12.5. Eaton Corporation plc

12.6. Fike Corporation

12.7. Robert Bosch GmbH

12.8. Minimax Viking Group

12.9. ORR Protection Systems

12.10. Halma plc

12.11. Hochiki Corporation

12.12. Nohmi Bosai Ltd.

12.13. Kidde Fire Systems

12.14. SEM-SAFE

12.15. Securiton AG

12.16. Others

13.Appendix

13.1. Questionnaire

13.2. Available Customization Options

13.3. Related Reports

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Feb-2026

Subscribe to get the latest industry updates