Resources

About Us

Data Center Cabling Market Size, Share & Trends Analysis by Cable Type (Fiber Optic, Copper, Active Optical Cables), Component (Cables, Connectors & Patch Panels, Cable Management, Software & Services), Data Speed, Data Center Type, End Use, and Geography — Global Opportunity Analysis & Industry Forecast (2026–2036)

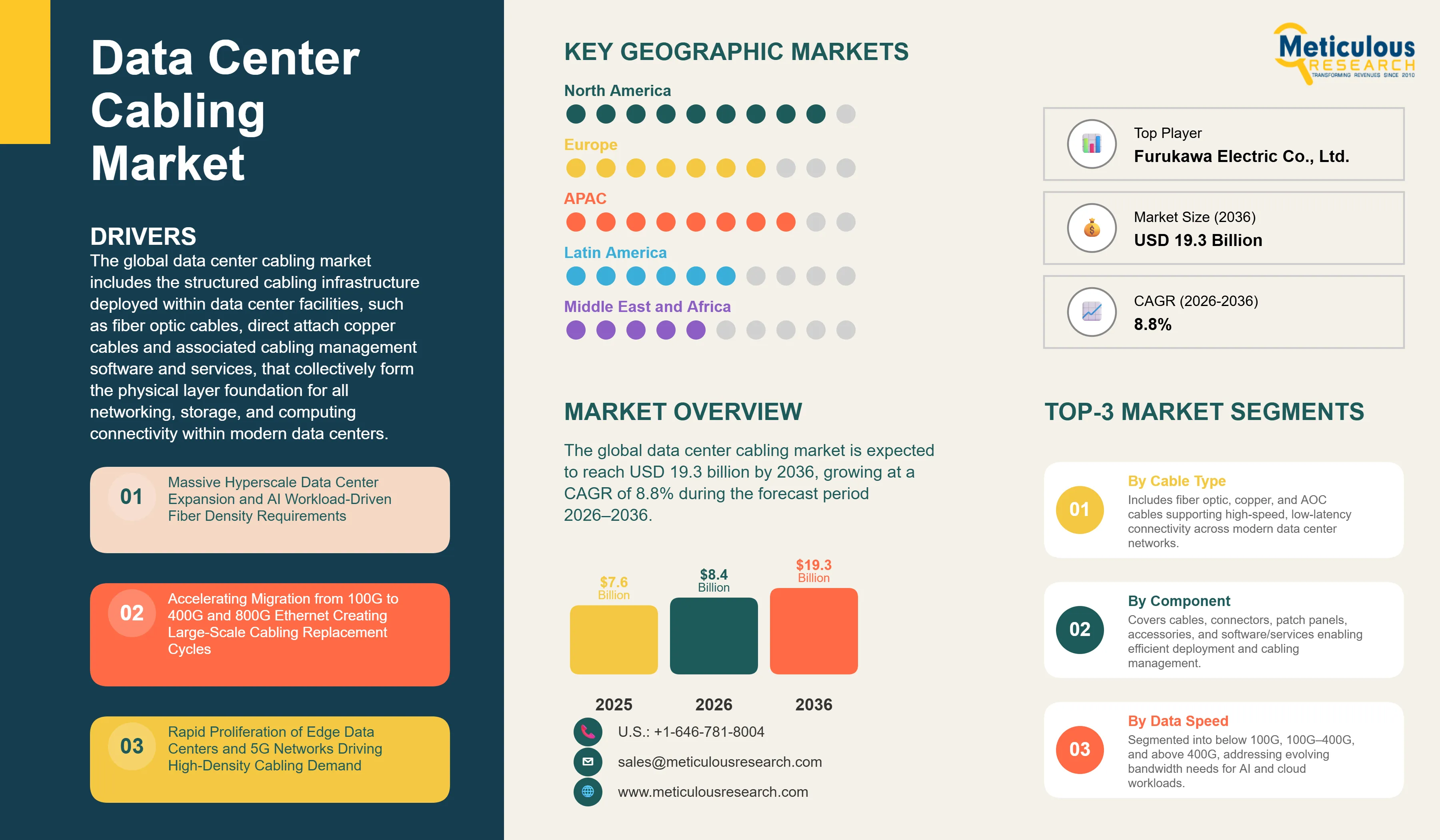

Report ID: MRSE - 1041859 Pages: 285 Apr-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global data center cabling market was valued at USD 7.6 billion in 2025. This market is expected to reach USD 19.3 billion by 2036 from an estimated USD 8.4 billion in 2026, growing at a CAGR of 8.8% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global data center cabling market includes the structured cabling infrastructure deployed within data center facilities, such as fiber optic cables, copper data cables, active optical cables, direct attach copper cables, connectors, patch panels, cable trays and management accessories, and associated cabling management software and services, that collectively form the physical layer foundation for all networking, storage, and computing connectivity within modern data centers. These products are deployed across hyperscale, colocation, enterprise, and edge data center environments to support server-to-switch connectivity, spine-leaf switching architectures, storage area networks, cross-connects, and intra-campus backbone cabling.

The growth of the global data center cabling market is primarily driven by the rapid expansion of hyperscale data center capacity worldwide. Large-scale campuses require extensive deployment of high-performance fiber optic cabling, often spanning thousands of kilometers per site.

In addition, the ongoing transition from 100G to 400G and 800G Ethernet architectures is creating a significant structured cabling replacement cycle across existing facilities. The increasing adoption of AI and high-performance computing workloads is further driving demand, as these environments require substantially higher fiber interconnect density per rack compared to traditional CPU-based configurations.

However, the market faces certain constraints. Raw material price volatility, mainly in copper, has increased cable costs significantly in recent years, impacting overall infrastructure budgets. In parallel, compatibility challenges associated with upgrading legacy cabling systems to support 400G and higher-speed architectures can complicate migration efforts and increase deployment complexity.

Despite these challenges, several growth opportunities are emerging. The adoption of pre-terminated, factory-assembled cabling solutions is increasing, as these systems reduce on-site installation time and improve performance consistency.

Additionally, intelligent cabling management platforms with AI-enabled monitoring and predictive maintenance capabilities are gaining traction. The growing use of high-density MPO/MTP trunk systems in AI-driven data center environments is also supporting higher bandwidth requirements and improved space utilization.

A key trend shaping the market is the development of ultra-high fiber count cables. Innovations such as Corning Incorporated advanced fiber solutions, which significantly increase fiber density within the same cable footprint, are helping reduce pathway congestion in high-density AI data halls and enabling more efficient scaling of next-generation data center infrastructure.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 19.3 Billion |

|

Market Size in 2026 |

USD 8.4 Billion |

|

Market Size in 2025 |

USD 7.6 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 8.4% |

|

Dominating Cable Type |

Fiber Optic Cables |

|

Fastest Growing Cable Type |

Active Optical Cables (AOC) |

|

Dominating Component |

Cables |

|

Fastest Growing Component |

Software & Services |

|

Dominating Data Speed |

100G–400G |

|

Fastest Growing Data Speed |

Above 400G (800G, 1.6T and Beyond) |

|

Dominating Data Center Type |

Hyperscale |

|

Fastest Growing Data Center Type |

Edge & Micro Data Centers |

|

Dominating End Use |

IT & Telecom |

|

Fastest Growing End Use |

Healthcare |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Ultra-High-Fiber-Count Cable Architectures Addressing AI Campus Density

The emergence of ultra-high fiber count cable architectures, delivering 288, 432, and up to 864 fibers within compact outer diameters previously occupied by 144-fiber cables, is directly addressing pathway and space constraints in AI-driven data center environments.

Solutions from Corning Incorporated, Prysmian Group, and OFS are increasingly deployed in backbone infrastructure to support 400G and 800G spine-leaf architectures without exceeding cable pathway capacity.

This transition is driving a product refresh cycle across trunk cabling layers in both new and existing hyperscale facilities. As a result, revenue growth within the cables segment is outpacing simple port count expansion, reflecting the premium pricing and higher value associated with high-density fiber solutions.

Pre-Terminated Factory Assemblies Becoming Standard for Hyperscale Deployments

The adoption of pre-terminated, factory-assembled fiber optic trunk assemblies is becoming the dominant deployment approach in hyperscale data centers. In these systems, MPO/MTP multi-fiber connectors are factory-polished, tested, and integrated with high-count fiber cables prior to shipment. This approach enables faster deployment, improved performance consistency, and reduced reliance on on-site labor compared to traditional field-terminated cabling.

Factory-assembled solutions typically deliver superior optical insertion loss performance and significantly reduce installation time, often lowering on-site labor requirements by 40–60%. They also minimize the risks of contamination and damage associated with field polishing in active data hall environments, improving overall network reliability and deployment quality.

Leading vendors such as Corning Incorporated, CommScope Holding Company, Inc., Panduit Corp., and Belden Inc. are reporting increasing contributions from pre-terminated assembly solutions in hyperscale deployments. This trend is expected to accelerate further as AI-driven data center buildouts require shorter deployment timelines and higher installation precision.

By Cable Type: In 2026, the Fiber Optic Cables Segment to Dominate the Global Data Center Cabling Market

Based on cable type, the global data center cabling market is segmented into fiber optic cables (single-mode fiber, multi-mode fiber), copper cables (Cat 6A, Cat 7/7A, Cat 8, DAC), and active optical cables (AOC).

In 2026, the fiber optic cables segment is expected to account for the largest share of around 55–60% of the global data center cabling market. The large share of this segment is attributed to the dominance of fiber optic technology for all medium- and long-distance connections within hyperscale and colocation data centers, the mandatory use of single-mode fiber for 400G and above data rates across spine-leaf switching fabrics, and the growing adoption of multi-mode OM4 and OM5 fiber for short-reach GPU-to-switch connections.

Within the fiber optic segment, single-mode fiber is gaining share relative to multi-mode as 400G deployments expand, since single-mode supports longer reach distances that better accommodate the larger footprints of AI campuses.

However, the active optical cables (AOC) segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the growing adoption of integrated AOC solutions that combine optical transceivers and fiber in a single, pre-terminated assembly optimized for GPU-to-switch connectivity in AI training clusters, where they eliminate the separate transceiver and patch cord procurement steps and provide assured optical performance at 400G and 800G data rates within the constrained cable management environments of high-density AI racks.

By Component: In 2026, the Cables Segment to Account for the Largest Share

Based on component, the global data center cabling market is segmented into cables, connectors and patch panels, cable management and accessories, and software and services.

In 2026, the cables segment is expected to account for the largest share of the global data center cabling market, indicating the dominant revenue contribution of fiber optic trunk cables, copper backbone cables, and pre-terminated assembly products that represent the highest per-unit value within the cabling infrastructure procurement bill. Cable procurement is driven directly by new data center construction and the 400G migration replacement cycle, both of which are operating at peak intensity through the forecast period.

However, the software and services segment is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing adoption of intelligent infrastructure management platforms that automate physical layer documentation and enable AI-driven analytics for cabling system optimization.

In addition, the expanding demand for structured cabling installation and commissioning services is supporting segment growth. Large-scale AI data center campuses require specialized expertise to manage the complexity and scale of cabling deployment, leading to increased reliance on experienced service providers.

By Data Speed: In 2026, the 100G–400G Segment to Hold the Largest Share

Based on data speed, the global data center cabling market is segmented into below 100G, 100G–400G, and above 400G (800G, 1.6T and beyond).

In 2026, the 100G–400G segment is expected to account for the largest share of the global data center cabling market. This indicates the current phase of the hyperscale networking upgrade cycle, where most new deployments are being built or upgraded to 400G Ethernet, while 800G deployments are still in the early scaling stage.

The transition from 100G to 400G is driving both greenfield procurement for new 400G-native infrastructure and replacement demand as existing 100G systems are upgraded to support increasing AI-driven traffic volumes.

However, the above 400G segment is projected to register the highest CAGR during the forecast period. This growth is driven by the growing adoption of 800G Ethernet in hyperscale spine networks and AI GPU cluster interconnects from 2026 onward.

In addition, the emergence of 1.6T transceivers and cabling solutions targeting next-generation GPU architectures is expected to further increase demand for ultra-high-bandwidth infrastructure from 2027 to 2028.

By Data Center Type: In 2026, the Hyperscale Segment to Hold the Largest Share

Based on data center type, the global data center cabling market is segmented into hyperscale, colocation, enterprise, and edge and micro data centers.

In 2026, the hyperscale segment is expected to account for the largest share of the global data center cabling market. This dominance is driven by the substantial cabling requirements of hyperscale AI campus developments, where each gigawatt-scale facility requires extensive deployment of fiber trunk cabling, large volumes of patch cords, and significant quantities of connectors and cable management infrastructure.

However, the edge and micro data centers segment is projected to register the highest CAGR during the forecast period, driven by the proliferation of distributed edge computing locations for 5G, autonomous vehicle support, and industrial AI applications that each require structured cabling infrastructure sized for their specific compute and networking density requirements.

By End Use: In 2026, the IT & Telecom Segment to Hold the Largest Share

Based on end use, the global data center cabling market is segmented into IT and telecom, BFSI, government and defense, healthcare, retail and e-commerce, energy and utilities, and other end uses.

In 2026, the IT and telecom segment is expected to account for the largest share of the global data center cabling market. This dominance reflects the leading role of cloud service providers, telecommunications carriers, and IT infrastructure companies as the primary procurers of data center cabling globally. The segment includes hyperscale operators such as Amazon Web Services, Microsoft Corporation, and Alphabet Inc., along with colocation providers and telecom operators deploying carrier-grade cabling for 5G core network infrastructure.

However, the healthcare segment is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing deployment of AI-enabled diagnostic systems, clinical decision support tools, and genomics analysis applications, which require high-bandwidth, low-latency on-premises infrastructure. As a result, healthcare organizations are investing in advanced structured cabling systems to support data-intensive workloads while ensuring compliance with clinical data sovereignty and security requirements.

Based on geography, the global data center cabling market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global data center cabling market. This dominant position is supported by the highest global concentration of hyperscale AI data center deployments, the most active 400G and 800G Ethernet upgrade cycle, and the strong presence of leading cabling manufacturers, such as Corning, Panduit, Belden, and Amphenol/CommScope with established hyperscale supply chain relationships.

However, Asia Pacific is expected to register the highest growth rate during the forecast period. China leads the growth of data center cabling market in this region, driven by large-scale investments in hyperscale data centers, AI campus construction, and cloud infrastructure expansion. India follows, with data center capacity expected to grow from 1.8 gigawatts in 2026 to 4.5 gigawatts by 2030, requiring massive greenfield cabling procurement for new AI-ready facilities in Mumbai, Chennai, Hyderabad, and emerging Tier 2 city markets. Japan, Singapore, and South Korea are also contributing to the high growth of the APAC region through sustained data center investment programs anchored to national AI infrastructure strategies.

The global data center cabling market is moderately concentrated, with competition focused on optical performance specifications, product breadth across fiber‑optic and copper categories, pre‑terminated assembly manufacturing capability, supply‑chain scale for large‑volume hyperscale deployments, and the ability to integrate intelligent infrastructure‑management software into physical cabling products.

Corning is a leading global provider of data center fiber‑optic cables, with strong market presence driven by its OpticalCon and Contour Flow product families and its deep supply‑chain relationships with hyperscale operators.

CommScope (including its Vistance Networks brand), Panduit, and Belden compete across the full cabling product spectrum, offering both fiber and copper solutions, and hold strong positions in enterprise and colocation data center markets.

Nexans and Prysmian compete primarily in the European and several emerging‑market segments, focusing on structured‑cabling and high‑performance copper‑ and fiber‑cable solutions.

The report offers a competitive analysis based on an extensive assessment of the leading players’ product portfolios, geographic presence, and key growth strategies adopted in the last few years. Some of the key players operating in the global data center cabling market are Corning Incorporated (U.S.), CommScope Holding Company, Inc. / Vistance Networks (U.S.), Panduit Corp. (U.S.), Belden Inc. (U.S.), Nexans SA (France), Prysmian S.p.A. (Italy), Schneider Electric SE (France), Legrand SA (France), Siemon Company (U.S.), TE Connectivity Ltd. (Switzerland), Amphenol Corporation (U.S.), Leviton Manufacturing Co., Inc. (U.S.), Furukawa Electric Co., Ltd. (Japan), Sterlite Technologies Limited (India), and Hengtong Group Co., Ltd. (China).

The global data center cabling market is expected to reach USD 19.3 billion by 2036 from an estimated USD 8.4 billion in 2026, at a CAGR of 8.8% during the forecast period 2026–2036.

In 2026, the fiber optic cables segment is expected to hold the largest share of the global data center cabling market.

The active optical cables (AOC) segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by growing adoption for 400G and 800G interconnects within AI GPU clusters.

In 2026, the 100G–400G segment is expected to hold the largest share of the global data center cabling market.

In 2026, the IT and telecom segment is expected to hold the largest share of the global data center cabling market.

The growth of this market is driven by the massive global expansion of hyperscale data center capacity, the accelerating migration from 100G to 400G and 800G Ethernet creating large-scale cabling replacement cycles, and the surging adoption of AI workloads requiring four to five times more fiber interconnects per rack.

Key players are Corning Incorporated (U.S.), CommScope Holding Company, Inc. / Vistance Networks (U.S.), Panduit Corp. (U.S.), Belden Inc. (U.S.), Nexans SA (France), Prysmian S.p.A. (Italy), Schneider Electric SE (France), Legrand SA (France), Siemon Company (U.S.), TE Connectivity Ltd. (Switzerland), Amphenol Corporation (U.S.), Leviton Manufacturing Co., Inc. (U.S.), Furukawa Electric Co., Ltd. (Japan), Sterlite Technologies Limited (India), and Hengtong Group Co., Ltd. (China).

Asia Pacific is expected to register the highest growth rate in the global data center cabling market during the forecast period 2026–2036.

Published Date: Jun-2026

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Feb-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates