Resources

About Us

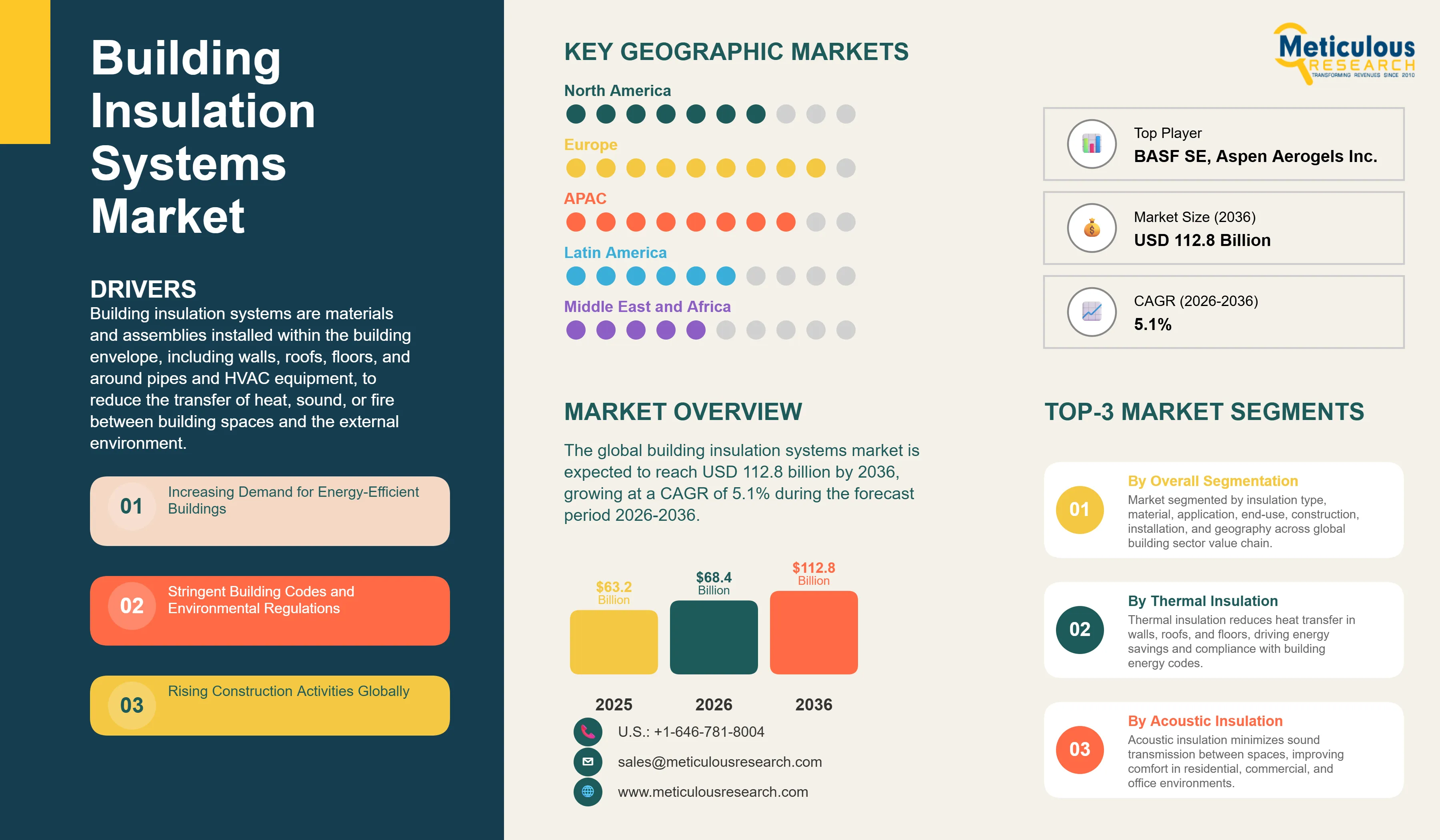

Building Insulation Systems Market Size, Share & Trends Analysis by Insulation Type, Material Type, Application, and End-Use Sector - Global Opportunity Analysis & Industry Forecast (2026-2036)

Report ID: MRSE - 1041945 Pages: 270 Apr-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global building insulation systems market was valued at USD 63.2 billion in 2025. This market is expected to reach USD 112.8 billion by 2036 from an estimated USD 68.4 billion in 2026, growing at a CAGR of 5.1% during the forecast period 2026-2036. Buildings account for approximately 36% of global final energy consumption and nearly 40% of energy-related carbon dioxide emissions, according to the International Energy Agency, making building insulation one of the most commercially impactful segments of the broader energy transition.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Building insulation systems are materials and assemblies installed within the building envelope, including walls, roofs, floors, and around pipes and HVAC equipment, to reduce the transfer of heat, sound, or fire between building spaces and the external environment. Effective thermal insulation keeps buildings warm in winter and cool in summer, cutting heating and cooling energy demand by 30 to 50% compared with uninsulated structures, according to the European Insulation Manufacturers Association. Beyond energy savings, insulation improves occupant comfort, reduces condensation and moisture damage, and provides fire containment and acoustic privacy. Given that a poorly insulated home can lose up to 35% of its heat through the roof and 25% through walls, quality insulation installation is one of the highest-return energy efficiency investments available.

The market is growing because governments globally are tightening building energy performance standards at an accelerating pace. The European Union's Energy Performance of Buildings Directive now requires all new buildings to be nearly zero energy buildings, directly mandating higher insulation standards across the 27-member bloc. In the U.S., the Department of Energy's adoption of ASHRAE 90.1-2022 energy efficiency standards in federal buildings is driving specification upgrades across the commercial sector. The U.S. Inflation Reduction Act of 2022 allocated over USD 4 billion in tax rebates for home energy efficiency improvements including insulation, creating direct consumer demand. China's 14th Five-Year Plan sets explicit energy intensity reduction targets for buildings that require substantial insulation upgrades across its enormous new construction pipeline. These regulatory and financial incentives are creating a sustained, policy-backed demand environment across all major markets simultaneously.

Two major opportunities are shaping the market's next phase. The retrofitting of Europe's 220 million existing buildings, over 75% of which are considered energy inefficient by EU standards, represents what the European Commission has called the largest investment opportunity in the building sector in decades. The EU's Renovation Wave strategy targets doubling the energy renovation rate from 1% to at least 2% annually by 2030. Simultaneously, aerogel-based insulation materials, which offer thermal performance up to ten times better than conventional mineral wool at the same thickness, are transitioning from aerospace and industrial niche applications to broader building use. Aspen Aerogels reported aerogel building product revenues growing over 40% year-on-year in recent results, signaling the commercial momentum building in this premium segment.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 112.8 Billion |

|

Market Size in 2026 |

USD 68.4 Billion |

|

Market Size in 2025 |

USD 63.2 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 5.1% |

|

Dominating Insulation Type |

Thermal Insulation |

|

Fastest Growing Insulation Type |

Fire-Resistant Insulation |

|

Dominating Material Type |

Mineral Wool |

|

Fastest Growing Material Type |

Advanced Materials (Aerogels, VIPs) |

|

Dominating Application |

Walls |

|

Fastest Growing Application |

HVAC and Pipes |

|

Dominating End-Use Sector |

Residential Buildings |

|

Fastest Growing End-Use Sector |

Commercial Buildings |

|

Dominating Construction Type |

New Construction |

|

Fastest Growing Construction Type |

Renovation and Retrofit |

|

Dominating Installation Type |

Post-Installed Systems |

|

Fastest Growing Installation Type |

Pre-Installed Systems |

|

Dominating Geography |

Europe |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

EU Renovation Wave and Nearly Zero-Energy Building Standards Reshaping European Demand

Europe is the world's most policy-intensive building insulation market, with the revised Energy Performance of Buildings Directive establishing mandatory net-zero building standards for new construction by 2028 for public buildings and 2030 for all new buildings. This directly requires higher insulation performance specifications than current practice in most European countries. Germany's Building Energy Act, France's RE2020 regulation, and the UK's Future Homes Standard are each requiring new homes to meet increasingly stringent thermal performance targets that can only be achieved with high-performance wall, roof, and floor insulation systems.

The retrofit market is equally significant. The EU's Renovation Wave initiative, backed by over EUR 150 billion in funding from the EU Recovery and Resilience Facility, targets 35 million building renovations by 2030. Deep energy retrofits that improve a building's energy class by two or more levels generate intensive insulation procurement: a typical deep retrofit of a 1970s apartment block may require the installation of 100 to 200 millimeters of external wall insulation across the entire building facade, representing substantial material volumes and installation labor. Companies like Rockwool, Saint-Gobain, and Kingspan are all investing in expanded European manufacturing capacity in direct response to this policy-driven demand pipeline.

Bio-Based and Sustainable Insulation Materials Gaining Commercial Traction

Growing consumer awareness of the embodied carbon of building materials and the regulatory push for Environmental Product Declarations across Europe is creating commercial momentum for bio-based insulation materials including wood fiber, hemp, cellulose, and sheep's wool as alternatives to petroleum-derived plastic foam products. Wood fiber insulation boards from companies including Steico and Pavatex are gaining market share in European passive house and low-energy building projects where architects specify materials based on whole-lifecycle carbon performance rather than installed cost alone. Cellulose insulation, produced from recycled paper, requires roughly 10 times less energy to manufacture than glass wool and has a near-zero carbon footprint, making it an increasingly popular choice for green building projects.

Kingspan Group's Net Zero Now commitment and its investment in manufacturing insulation products with net-zero embodied carbon by 2030 is a high-profile industry example of how leading manufacturers are repositioning their product portfolios in response to the embodied carbon agenda. BASF's development of partially bio-based polyurethane formulations and Saint-Gobain's sustainability roadmap both reflect the same commercial recognition that the construction sector's decarbonization agenda extends beyond operational energy use to include the carbon embodied in the building materials themselves. This trend is expected to grow the market share of natural and bio-based insulation from a niche to a meaningful commercial segment through the forecast period.

Extreme Heat and Climate Resilience Driving New Insulation Investment in Warm Climates

While building insulation has historically been associated primarily with keeping buildings warm in cold climates, the accelerating frequency and intensity of heat waves globally is creating substantial new demand for insulation in warm and temperate climate regions where buildings have traditionally been lightly insulated. Southern European countries including Spain, Italy, and Greece experienced record-breaking summer temperatures exceeding 45 degrees Celsius in recent years, with the European Environment Agency estimating that heat-related deaths exceeded 60,000 across Europe in the summer of 2022 alone. Poor insulation in southern European buildings, which are generally built to keep out winter cold rather than summer heat, is a major contributor to uncomfortable and dangerous indoor temperatures during heat events.

This climate reality is driving new policy attention to summer thermal comfort in building codes and is creating demand for insulation solutions specifically valued for their ability to reduce solar heat gain and moderate indoor temperature swings, including high-density wood fiber insulation that offers superior thermal mass alongside thermal resistance. In rapidly urbanizing Southeast Asian and Middle Eastern markets, where air conditioning accounts for a very large share of peak electricity demand and where cooling costs are a major household expense, improved building insulation is increasingly recognized as a cost-effective way to reduce energy bills, improve comfort, and reduce the strain on electrical grids during peak demand periods.

Increasing Demand for Energy-Efficient Buildings

Buildings consume approximately 36% of global final energy, with heating and cooling accounting for roughly half of that consumption according to IEA data. The direct link between insulation quality and energy consumption means that every improvement in building insulation standards translates directly into measurable energy savings and carbon emission reductions. A home insulated to current best-practice standards can reduce heating energy demand by 50 to 80% compared with a typical building constructed before 2000. For homeowners, this translates into significant energy bill reductions: the U.S. Department of Energy estimates that a well-insulated and air-sealed home can save 15% or more on heating and cooling costs. As energy prices remain elevated globally and as household energy affordability becomes a political priority, the financial case for insulation investment is stronger than it has been in decades, driving both new installation and retrofit demand across all building types.

Stringent Building Codes and Environmental Regulations

Building energy codes are becoming progressively more stringent in every major construction market globally, and compliance with these codes requires increasingly high levels of insulation performance. The EU's Energy Performance of Buildings Directive mandates that all new buildings must be nearly zero energy buildings, and the revised directive published in 2024 tightens these requirements further. In the U.S., the International Energy Conservation Code is updated every three years with increasingly demanding insulation requirements, and over 90% of U.S. states have adopted versions of this code. California's Title 24 building energy standards are among the world's most demanding, requiring very high levels of wall, roof, and foundation insulation in new construction. Australia's National Construction Code 7-Star energy rating requirement for new homes, introduced in 2023, has significantly increased insulation specification in a market where thin wall insulation was previously common. Each regulatory tightening in these markets creates a direct procurement demand for better-performing insulation products.

Development of Advanced Insulation Materials (Aerogels, Vacuum Panels)

Aerogel insulation, originally developed for NASA space applications, is the world's best thermally insulating solid material, with thermal conductivity values as low as 0.015 W/mK compared with 0.030 to 0.040 W/mK for conventional mineral wool. This exceptional performance means that an aerogel blanket just 10 millimeters thick can provide the same insulation as 30 to 40 millimeters of glass wool, making it transformative for retrofit applications where space is limited, for insulating structural thermal bridges, and for thin-profile external insulation on heritage buildings where adding significant thickness to facades is architecturally undesirable. Aspen Aerogels, the leading commercial aerogel manufacturer, has been expanding its building and construction product range and reported a year-on-year revenue increase exceeding 40% in its latest reported results, demonstrating the strong commercial momentum building in this premium segment. Vacuum Insulated Panels offer similarly exceptional performance at thermal conductivities below 0.008 W/mK and are gaining adoption in refrigeration and specialist building applications where ultra-thin insulation is required.

Retrofitting and Renovation of Existing Buildings

The global building stock of over 150 billion square meters includes hundreds of millions of buildings constructed before modern energy codes that are poorly insulated by current standards. Retrofitting these buildings with modern insulation represents one of the largest and most immediately cost-effective climate mitigation opportunities available. In Europe, where over 75% of the existing building stock is estimated to be energy inefficient, the EU's Renovation Wave initiative targets a doubling of the renovation rate, supported by over EUR 150 billion of EU funds and national tax incentives. Germany's Federal Funding for Efficient Buildings program provides grants covering up to 20% of the cost of energy renovation including insulation, generating significant consumer demand. The UK's Great British Insulation Scheme and the ECO4 obligation are directing billions of pounds toward insulation upgrades in fuel-poor households. These programs are creating a large, government-funded retrofit market that will sustain insulation demand regardless of the economic cycle for at least the coming decade.

By Insulation Type: In 2026, Thermal Insulation to Dominate

Based on insulation type, the global building insulation systems market is segmented into thermal insulation, acoustic insulation, and fire-resistant insulation. In 2026, the thermal insulation segment is expected to account for the largest share of the global building insulation systems market. Reducing heat transfer is the primary function of building insulation in the vast majority of applications globally, and thermal insulation products represent the largest procurement category by volume and value. The direct link between thermal insulation quality and building energy consumption, combined with rising energy costs and tightening building energy codes, ensures that thermal insulation remains the dominant application driver across all markets and building types.

However, the fire-resistant insulation segment is projected to register the highest CAGR during the forecast period. Following high-profile fire incidents in multi-story residential buildings, including the Grenfell Tower fire in London in 2017 that claimed 72 lives and led to a comprehensive review of building cladding and insulation fire performance requirements across the UK and internationally, fire safety has become a primary specification criterion for insulation materials in multi-family residential and commercial buildings. The resulting regulatory changes mandating non-combustible or limited-combustibility insulation in buildings above certain heights have created strong and sustained demand growth for mineral wool and other fire-resistant insulation products.

By Material Type: In 2026, Mineral Wool to Hold the Largest Share

Based on material type, the global building insulation systems market is segmented into mineral wool, plastic foams, natural and bio-based materials, advanced materials (aerogels and vacuum insulated panels), and other materials. In 2026, the mineral wool segment is expected to account for the largest share of the global building insulation systems market. Glass wool and stone wool collectively represent the most widely used building insulation material globally, valued for their combination of thermal performance, fire resistance, acoustic absorption, and competitive cost. Rockwool International, which produces stone wool insulation under its Rockwool and Roxul brands, serves customers in over 40 countries and reported revenues of approximately EUR 3.8 billion in 2023, making it the world's largest dedicated insulation manufacturer and illustrating the commercial scale of the mineral wool market.

However, the advanced materials segment, particularly aerogels and vacuum insulated panels, is projected to register the highest CAGR during the forecast period. As aerogel production costs fall with manufacturing scale-up and as the premium performance of these materials becomes better understood among architects and contractors, adoption in building applications is accelerating. The retrofit market in particular is creating strong commercial pull for ultra-thin high-performance insulation that can improve building thermal performance without consuming valuable interior floor space.

By Application: In 2026, Walls to Hold the Largest Share

Based on application, the global building insulation systems market is segmented into walls, roofs and ceilings, floors, HVAC and pipes, windows and doors (insulated systems), and other applications. In 2026, the walls segment is expected to account for the largest share of the global building insulation systems market. Wall insulation covers by far the largest surface area in most building types and represents the single most impactful insulation application by both heat loss reduction potential and total material volume. External wall insulation systems, where insulation boards are fixed to the outside of the existing wall and covered with a render or cladding finish, have become the dominant retrofit insulation solution in Europe, with the European market for these systems growing strongly driven by renovation programs.

However, the HVAC and pipes segment is projected to register the highest CAGR during the forecast period. The rapid growth of district energy networks, the expansion of industrial and commercial HVAC infrastructure, and growing awareness of heat loss and condensation risks in uninsulated pipework are driving above-average growth in pipe and duct insulation. Armacell, the world's leading flexible foam insulation manufacturer, has specifically highlighted HVAC and technical insulation as its fastest-growing product category, with the segment benefiting from both new installation demand and significant retrofit activity in energy system optimization programs.

By End-Use Sector: In 2026, Residential Buildings to Hold the Largest Share

Based on end-use sector, the global building insulation systems market is segmented into residential buildings, commercial buildings, and industrial buildings. In 2026, the residential buildings segment is expected to account for the largest share of the global building insulation systems market. Housing construction and renovation represent the largest single source of insulation demand globally by volume, driven by the very large number of housing units built and renovated each year, the strong government support for residential energy efficiency improvements in most major markets, and the high political priority attached to household energy affordability. In the U.S. alone, residential buildings account for 21% of total energy consumption, and improving home insulation is among the most cost-effective interventions available for reducing energy bills and carbon emissions.

However, the commercial buildings segment is projected to register the highest CAGR during the forecast period. New commercial construction is growing rapidly, particularly in data centers where the thermal management requirements are extreme, in logistics and warehousing where large floor areas require significant insulation to meet energy codes, and in healthcare and laboratory facilities where precise temperature control requires high-performance building envelopes. The commercial sector's larger average building size means that individual project insulation procurement values are significantly higher than in residential construction, driving strong revenue growth.

Building Insulation Systems Market by Region: Europe Leading by Share, Asia-Pacific by Growth

Based on geography, the global building insulation systems market is segmented into Europe, North America, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, Europe is expected to account for the largest share of the global building insulation systems market. Europe leads because it has the most stringent building energy performance regulations of any region, the most mature and policy-driven renovation market, and the highest per-square-meter insulation performance requirements in new construction. Germany is the largest European market, driven by its very large new construction and renovation volumes and its Federal Funding for Efficient Buildings program that disbursed over EUR 13 billion in energy efficiency grants in 2022 alone. France's RE2020 regulation, which came into force for new residential buildings in January 2022, introduces carbon lifecycle requirements in addition to energy performance standards that are already driving specification shifts in insulation materials. The UK's revised building regulations and ambitious national retrofit programs are creating sustained demand across Britain's housing stock of over 28 million homes, approximately 19 million of which are estimated to have energy ratings of D or below according to the UK Department for Energy Security and Net Zero. Scandinavia, particularly Sweden and Norway, maintains among the world's highest insulation performance standards and is an important market for premium insulation products and innovative installation systems.

However, the Asia-Pacific building insulation systems market is expected to grow at the fastest CAGR during the forecast period. China is both the world's largest construction market by volume, with annual new building completions exceeding 2 billion square meters at the peak of the construction cycle, and a country that has recently established ambitious building energy efficiency policies including the requirement for green building certification for all new urban buildings by 2025. India is experiencing one of the fastest rates of urbanization in the world, with over 500 million people expected to live in cities by 2050 according to United Nations projections, driving an enormous new construction pipeline. India's construction sector is also increasingly adopting energy efficiency requirements, with the Energy Conservation Building Code being strengthened and extended to residential buildings. Rapidly growing economies in Southeast Asia including Vietnam, Indonesia, and Thailand are constructing enormous volumes of residential and commercial buildings, and awareness of the energy savings and comfort benefits of insulation is growing alongside rising energy costs. Japan's very high construction quality standards and commitment to zero-energy housing by 2030 make it an important market for premium insulation products.

North America is a large and technically sophisticated insulation market, with the U.S. supported by the Inflation Reduction Act's USD 4.3 billion in home energy efficiency rebates and tax credits that directly subsidize insulation upgrades. The U.S. Department of Energy's weatherization assistance program, which provides free insulation and energy efficiency improvements to low-income households, supported over 100,000 homes annually and represents consistent baseline demand. Canada's greener homes program has also provided significant grants for insulation upgrades. Latin America and the Middle East and Africa are earlier-stage markets where growing energy costs, rising urbanization, and the construction of new commercial and residential buildings are creating growing insulation demand, with the Gulf states' massive new urban development programs including NEOM in Saudi Arabia representing a significant procurement opportunity for specialized insulation systems.

The building insulation market is served by a combination of large diversified building materials companies with broad insulation portfolios, specialist insulation manufacturers focused on specific material types or applications, and emerging companies developing advanced insulation technologies. Market competition is based on thermal performance per unit thickness, fire resistance classification, acoustic performance, sustainability credentials and embodied carbon, installed cost competitiveness, and the strength of technical support and specification services for architects and contractors.

Saint-Gobain is the world's largest building materials company with one of the broadest insulation portfolios, covering glass wool through its Isover brand, gypsum-based systems, and advanced glazing. Owens Corning is the world's largest glass fiber manufacturer and a leading U.S. insulation supplier, reporting insulation segment revenues of approximately USD 2.2 billion in recent results. Kingspan Group is the world's leading manufacturer of high-performance insulation boards and insulated panels, with particular strength in polyisocyanurate and phenolic foam insulation for commercial and industrial applications. Rockwool International is the world's leading stone wool manufacturer, with a strong position in fire-resistant insulation for multi-story buildings and an explicit sustainability strategy targeting climate-positive operations. BASF produces polyurethane and melamine foam insulation materials widely used in building and industrial applications. Knauf Insulation is a major European glass wool and stone wool producer with growing global reach. Aspen Aerogels is the leading commercial aerogel insulation manufacturer and is the primary supplier of aerogel blankets for building applications.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, geographic presence, sustainability credentials, and recent strategic developments. Some of the key players operating in the global building insulation systems market include Saint-Gobain S.A. (France), Owens Corning (U.S.), Kingspan Group plc (Ireland), Rockwool International A/S (Denmark), BASF SE (Germany), Knauf Insulation (Germany), Johns Manville/Berkshire Hathaway (U.S.), Covestro AG (Germany), Huntsman Corporation (U.S.), GAF Materials Corporation (U.S.), Recticel Group (Belgium), Armacell International S.A. (Luxembourg), Fletcher Building Limited (New Zealand), Aspen Aerogels Inc. (U.S.), and Paroc Group/Owens Corning (Finland), among others.

The global building insulation systems market is expected to reach USD 112.8 billion by 2036 from an estimated USD 68.4 billion in 2026, at a CAGR of 5.1% during the forecast period 2026-2036. The market is underpinned by the fact that buildings account for approximately 36% of global energy consumption, making insulation improvement one of the most cost-effective and widely accessible energy efficiency interventions available globally.

In 2026, the mineral wool segment is expected to hold the largest share of the global building insulation systems market. Rockwool International alone, as the world's largest dedicated insulation manufacturer with revenues of approximately EUR 3.8 billion, illustrates the commercial scale of the mineral wool category, which is valued for combining thermal performance, fire resistance, and acoustic properties at competitive cost.

The advanced materials segment, particularly aerogels and vacuum insulated panels, is expected to register the highest CAGR during the forecast period 2026-2036.

In 2026, the walls segment is expected to hold the largest share of the global building insulation systems market, reflecting walls covering the largest surface area in most building types and representing the single most impactful insulation application. Poorly insulated walls can account for up to 25% of a building's total heat loss, making wall insulation the highest-priority specification for building energy performance compliance.

The EU's Renovation Wave initiative, backed by over EUR 150 billion in EU recovery funding, targets the renovation of 35 million buildings by 2030. Germany's Federal Funding for Efficient Buildings program disbursed over EUR 13 billion in 2022 alone. The U.S. Inflation Reduction Act provides USD 4.3 billion in home energy efficiency rebates including insulation. These programs collectively represent the most significant government-backed insulation demand stimulus in history.

The market is primarily driven by progressively tightening building energy codes in all major markets, including the EU's requirement for nearly zero-energy buildings and the U.S. Inflation Reduction Act's insulation incentives, combined with the very large government-funded renovation and retrofit programs that are creating sustained demand for insulation upgrades across the existing building stock. The IEA's estimate that buildings account for 36% of global final energy consumption makes insulation one of the most policy-prioritized product categories in the energy transition.

Key players are Saint-Gobain S.A. (France), Owens Corning (U.S.), Kingspan Group plc (Ireland), Rockwool International A/S (Denmark), BASF SE (Germany), Knauf Insulation (Germany), Johns Manville/Berkshire Hathaway (U.S.), Covestro AG (Germany), Huntsman Corporation (U.S.), GAF Materials Corporation (U.S.), Recticel Group (Belgium), Armacell International S.A. (Luxembourg), Fletcher Building Limited (New Zealand), Aspen Aerogels Inc. (U.S.), and Paroc Group/Owens Corning (Finland), among others.

Asia-Pacific is expected to register the highest growth rate in the global building insulation systems market during the forecast period 2026-2036. China's requirement for green building certification for all new urban buildings by 2025, India's expected addition of 500 million urban residents by 2050 requiring enormous new construction volumes, and the rapidly growing construction sectors of Vietnam, Indonesia, and Thailand collectively make Asia-Pacific the most dynamic growth region in the global insulation market.

Published Date: Feb-2026

Published Date: Jun-2023

Published Date: Feb-2026

Published Date: Oct-2025

Published Date: Feb-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates