Resources

About Us

Battery Energy Storage (BESS) Market for Data Centers by Battery Technology (Lithium-Ion, Lead-Acid, Flow Batteries, Sodium-Ion, Others), Application (UPS & Backup Power, Peak Shaving, Renewable Integration, Grid Services, AI Load Management), Data Center Type, Capacity, and Geography — Global Opportunity Analysis & Industry Forecast (2026–2036)

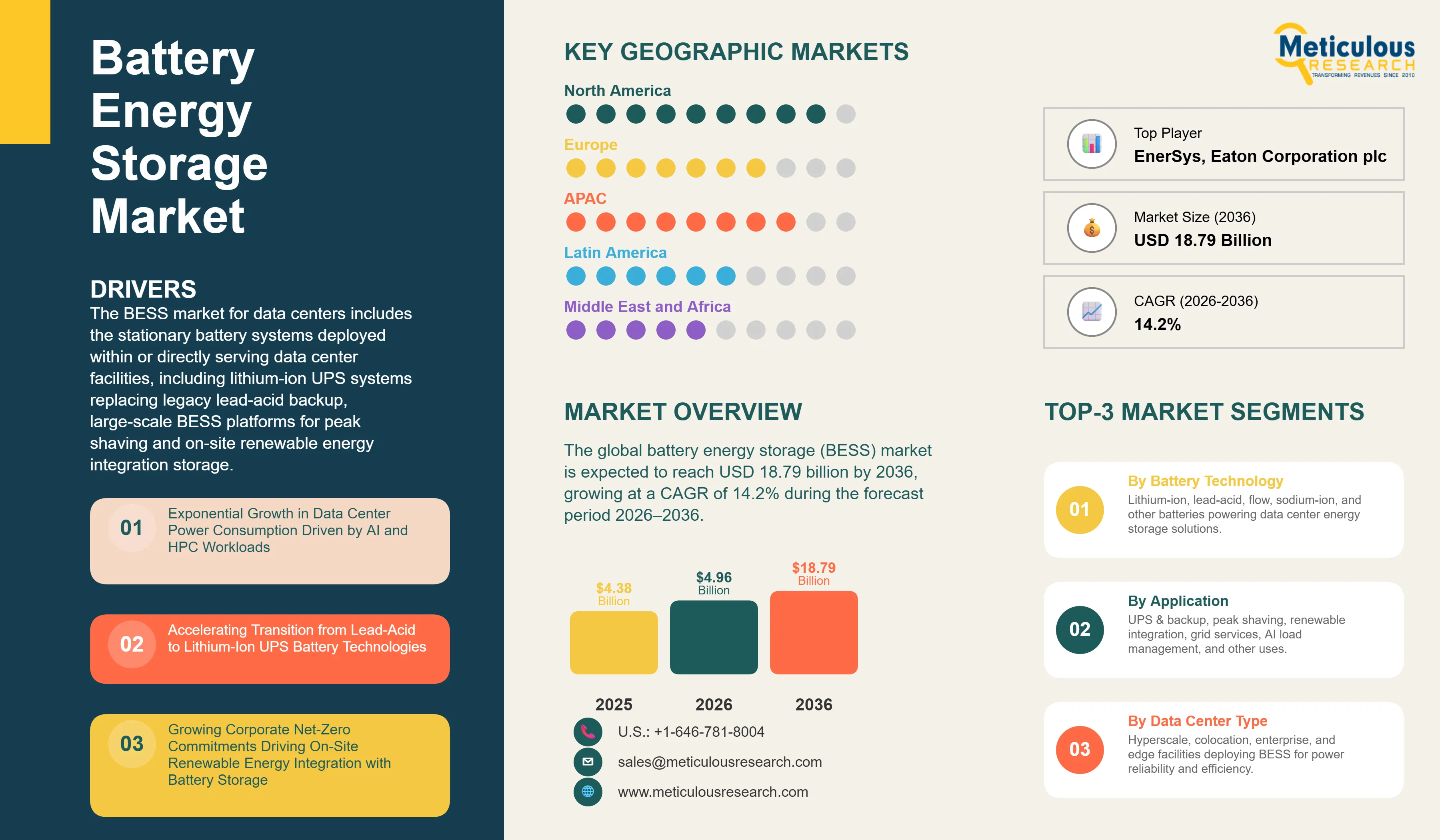

Report ID: MRSE - 1041858 Pages: 287 Apr-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global battery energy storage (BESS) market for data centers was valued at USD 4.38 billion in 2025. This market is expected to reach USD 18.79 billion by 2036 from an estimated USD 4.96 billion in 2026, growing at a CAGR of 14.2% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global BESS market for data centers includes the stationary battery systems deployed within or directly serving data center facilities, including lithium-ion UPS systems replacing legacy lead-acid backup, large-scale BESS platforms for peak shaving and demand response, on-site renewable energy integration storage, grid services and frequency regulation assets, and emerging purpose-built AI data center energy buffer systems across hyperscale, colocation, enterprise, and edge data center deployments worldwide.

The growth of this market is primarily driven by the increase in data center power consumption generated by AI and high-performance computing workloads accelerating the adoption of advanced BESS solutions for backup power, peak shaving, and renewable energy integration; the growing transition from legacy lead-acid UPS batteries to lithium-ion and next-generation battery technologies offering superior energy density, cycle life, and footprint efficiency; and the growing corporate sustainability commitments of hyperscale operators driving the integration of on-site renewable energy with battery storage to achieve net-zero carbon goals.

However, the high upfront capital cost of advanced BESS deployments, safety concerns associated with large-scale lithium-ion installations in occupied data center facilities, and the complexity of integrating BESS with existing power infrastructure and utility interconnection frameworks restrain the growth of this market.

The emergence of purpose-built AI data center energy storage solutions designed to manage the highly variable and instantaneous power demand spikes characteristic of GPU cluster workloads, the rising adoption of BESS-as-a-Service subscription models that remove upfront capital expenditure barriers, and the growing deployment of long-duration flow batteries for extended backup and renewable firming in hyperscale campuses offer significant market growth opportunities for stakeholders operating in this market.

Furthermore, the increasing regulatory transition away from diesel backup generators toward battery-based alternatives, driven by air quality regulations and sustainability mandates, is a major trend shaping this market.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 18.79 Billion |

|

Market Size in 2026 |

USD 4.96 Billion |

|

Market Size in 2025 |

USD 4.38 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 14.2% |

|

Dominating Battery Technology |

Lithium-Ion |

|

Fastest Growing Battery Technology |

Flow Batteries |

|

Dominating Application |

UPS & Backup Power |

|

Fastest Growing Application |

AI Load Management |

|

Dominating Data Center Type |

Hyperscale |

|

Fastest Growing Data Center Type |

Edge Data Centers |

|

Dominating Capacity |

1 MW–10 MW |

|

Fastest Growing Capacity |

Above 10 MW |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

AI Data Center Energy Buffer Storage Entering Commercial Deployment

The emergence of AI data center (AIDC)-specific energy buffer storage, distinct from conventional UPS systems, is a key trend driving the data center battery energy storage market. Unlike traditional UPS solutions, which function as passive backup systems activated only during grid outages, AIDC energy storage is designed as an active, integrated component of data center power architecture. These systems combine battery storage with intelligent energy management software, enabling bidirectional grid interaction and multi-hour discharge capabilities aligned with the dynamic power profiles of AI workloads.

AIDC energy storage systems actively manage real-time power delivery to high-density GPU clusters by mitigating sub-second load fluctuations. When thousands of GPUs ramp up simultaneously, these systems absorb sudden power spikes, and during ramp-down phases, they release stored energy to smooth demand curves and reduce peak electricity charges. This capability is becoming increasingly critical as AI workloads introduce unprecedented variability and intensity in power consumption patterns within hyperscale environments.

Early commercial deployments indicate this transition toward integrated energy storage architectures. Companies such as Microsoft Corporation and Equinix, Inc. are deploying large-scale battery energy storage systems alongside AI data center campuses to enhance energy efficiency, grid interaction, and operational resilience. This approach is expected to evolve into a standard design paradigm for hyperscale AI data centers by the latter part of the decade, particularly as power constraints and energy cost optimization become central to AI infrastructure planning.

Lithium Iron Phosphate Chemistry Displacing NMC as the Dominant Data Center Battery

Lithium iron phosphate (LFP) chemistry is rapidly displacing nickel manganese cobalt (NMC) as the preferred lithium‑ion chemistry for data center BESS applications, driven by LFP’s superior thermal stability, which significantly reduces fire risk in occupied data center facilities, its longer cycle life exceeding 3,000–4,000 charge‑discharge cycles compared to 1,500–2,500 cycles for NMC, and its dramatic cost decline to around USD 60–65/kWh for LFP‑based systems in Chinese project tenders in 2025.

Leading data center BESS integrators, such as Fluence Energy and Schneider Electric, have transitioned their primary stationary and data‑center BESS product lines toward LFP chemistry, and hyperscalers such as Microsoft are increasingly specifying LFP for new deployments based on lifecycle‑cost and safety considerations.

BESS-as-a-Service Models Expanding Addressable Market Beyond Hyperscale

The emergence of BESS‑as‑a‑Service (BESSaaS), in which battery storage system providers finance, install, own, and operate BESS within data center facilities under long‑term energy‑service‑type agreements, is expanding the commercial viability of data center battery storage beyond the large hyperscale operators who have historically dominated BESS procurement.

Under BESSaaS models, colocation and enterprise data center operators receive the operational benefits of battery storage—backup power, diesel‑generator reduction, peak shaving, and renewable‑firming—without the upfront capital expenditure or operational management burden, paying a monthly fee based on delivered energy services rather than on system purchase price.

This financing model is particularly relevant for mid‑market colocation and edge data center operators who require BESS for sustainability compliance and resilience but lack the scale and capital budgets of hyperscale customers, thereby enabling broader adoption of advanced energy‑storage solutions across the data‑center ecosystem.

Based on battery technology, the global battery energy storage market for data centers is segmented into lithium-ion (LFP, NMC, NCA), lead-acid (VRLA, advanced lead-acid), flow batteries (vanadium redox flow, zinc-bromine, others), sodium-ion batteries, and other technologies.

In 2026, the lithium-ion segment is expected to account for the largest share of around 55–60% of the global battery energy storage market for data centers. The large share of this segment is attributed to its superior combination of energy density, cycle life, round-trip efficiency, and declining system cost that has made it the preferred replacement technology for both UPS backup and advanced BESS applications across all data center types globally.

LFP chemistry is gaining significant traction in data center applications due to its thermal stability, long cycle life exceeding 4,000 cycles, and declining cell costs that reached approximately USD 63/kWh in project tenders in China in 2025.

However, the flow batteries segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the growing requirement for long-duration energy storage in hyperscale data center campuses seeking multi-hour backup capability, the suitability of flow batteries for renewable firming applications where several hours of discharge duration are required, and the modular scalability of flow battery architectures that enables capacity to be expanded independently of power rating.

Based on application, the global battery energy storage market for data centers is segmented into UPS and backup power, peak shaving and demand response, renewable energy integration, grid services and frequency regulation, AI‑related load‑management use cases, and other applications.

In 2026, the UPS and backup power segment is expected to account for around 40–45% of the global battery energy storage market for data centers, making it the largest application segment. This large share reflects the foundational requirement for reliable backup power in every operational data center, from the smallest enterprise server room to the largest hyperscale campus, and the active replacement cycle as operators retire legacy lead‑acid UPS batteries and upgrade to lithium‑ion systems. Tier 3 and Tier 4 data centers, which collectively represent the majority of commercial data‑center floor space, have contractual uptime commitments of 99.982% and above that make UPS‑battery investment non‑discretionary.

However, the AI‑related load‑management segment is expected to grow at the highest CAGR during the forecast period. The high growth of this segment is driven by the emergence of AI‑data‑center‑specific energy‑buffer storage designed to manage the instantaneous and highly variable power‑demand spikes characteristic of GPU‑cluster workloads, a requirement that cannot be fully met by conventional UPS or passive BESS systems. This is creating a new application category with premium system‑pricing potential and high growth rates through 2036.

Based on data center type, the global battery energy storage market for data centers is segmented into hyperscale, colocation, enterprise, and edge data centers.

In 2026, the hyperscale segment is expected to account for the largest share of the global battery energy storage market for data centers. This is primarily attributed to the very large scale of BESS procurement by the world’s leading cloud providers, who are building AI‑optimized hyperscale campuses with integrated renewable‑energy targets that require large‑scale battery storage for firming, backup power, and managing the instantaneous power‑demand spikes of GPU‑cluster workloads.

However, the edge data centers segment is poised to grow at the highest CAGR from 2026 to 2036. The high growth of this segment is driven by the proliferation of distributed edge data centers in locations with unreliable grid infrastructure, where BESS is essential for both backup power and power‑quality management, and by the growing adoption of renewable energy at edge sites, where battery storage is required to firm intermittent generation and improve system reliability.

Based on capacity, the global battery energy storage market for data centers is segmented into below 1 MW, 1 MW–10 MW, and above 10 MW.

In 2026, the 1 MW–10 MW capacity segment is expected to account for the largest share of the global battery energy storage market for data centers. This capacity range corresponds to BESS deployments at mid‑size hyperscale facilities, large colocation data centers, and enterprise data centers, which together represent the largest proportion of operational data‑center floor space globally, and includes both UPS‑replacement systems and initial‑scale BESS for peak shaving and renewable integration.

However, the above‑10 MW segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the scale‑up of BESS deployments at gigawatt‑class AI data center campuses, where hyperscale operators are deploying 20–100 MW battery storage systems for comprehensive renewable‑firming, AI‑load management, and grid‑services applications—deployments that individually represent tens to hundreds of millions of dollars of battery‑system procurement.

Based on geography, the global battery energy storage market for data centers is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global battery energy storage market for data centers. North America’s significant market share is attributed to the highest global concentration of hyperscale and AI‑optimized data center deployments, which generate the largest BESS procurement volumes, strong government policy support through mechanisms such as investment tax credits for standalone battery storage that improve project economics, and the most developed BESS system integration ecosystem, including leading providers such as Fluence Energy, Eaton, Schneider Electric, and Vertiv with established data‑center customer relationships.

However, the Asia Pacific BESS market for data centers is expected to grow at the highest CAGR from 2026 to 2036. The rapid growth in this region is driven by the rapid expansion of AI data center capacity across China, which has invested billions of dollars in new data‑center capacity in the early 2020s and is rapidly adding server‑rack‑scale infrastructure, the emergence of China as one of the world’s most active BESS markets, where AI‑data‑center‑optimized energy‑storage solutions are entering commercialization, and the rapid expansion of data‑center infrastructure across India, Japan, Singapore, and Southeast Asia, which increasingly require both conventional UPS‑replacement systems and advanced BESS for renewable integration and AI‑load management.

Projections indicate that by 2030 global shipments of lithium‑ion batteries for AI‑data‑center‑oriented BESS could exceed 300 GWh, with China expected to contribute a dominant share of this volume.

The global battery energy storage market for data centers is moderately fragmented, with competition focused on battery chemistry performance, system integration capability, safety certification for occupied facility deployments, total cost of ownership, and the ability to address both conventional UPS‑replacement applications and emerging AI‑specific energy‑storage requirements.

Battery cell manufacturers, such as CATL, BYD, LG Energy Solution, Samsung SDI, and HiTHIUM, compete on cell chemistry, cost, cycle life, and manufacturing scale.

System integrators, such as Fluence Energy, Schneider Electric, Vertiv, Eaton, and ABB, compete on software‑based energy‑management platforms, grid‑interconnection capability, and data‑center‑specific deployment expertise.

Meanwhile, UPS manufacturers, such as Delta Electronics, Eaton, and Schneider Electric, are expanding from traditional UPS offerings into full‑featured BESS platforms that combine backup power, peak‑shaving, and renewable‑firming capabilities.

The report offers a competitive analysis based on an extensive assessment of product portfolios, geographic presence, and key growth strategies adopted by the leading players over the last few years. Some of the key players operating in the global battery energy storage market for data centers are Tesla, Inc. (U.S.), LG Energy Solution, Ltd. (South Korea), Samsung SDI Co., Ltd. (South Korea), Contemporary Amperex Technology Co., Ltd. (CATL, China), BYD Company Ltd. (China), Fluence Energy, Inc. (U.S.), Schneider Electric SE (France), Vertiv Holdings Co. (U.S.), Eaton Corporation plc (Ireland), ABB Ltd. (Switzerland), Delta Electronics, Inc. (Taiwan), Hitachi Energy Ltd. (Switzerland), Panasonic Energy Co., Ltd. (Japan), EnerSys (U.S.), and HiTHIUM Energy Storage Technology Co., Ltd. (China) among others.

The global battery energy storage market for data centers is expected to reach USD 18.79 billion by 2036 from an estimated USD 4.96 billion in 2026, at a CAGR of 14.2% during the forecast period 2026–2036.

In 2026, the lithium-ion segment is expected to hold the largest share of the global battery energy storage market for data centers.

The flow batteries segment is expected to register the highest CAGR during the forecast period 2026–2036.

In 2026, the UPS and backup power segment is expected to hold the largest share of the global battery energy storage market for data centers.

The AI load management segment is expected to register the highest CAGR during the forecast period 2026–2036.

The growth of this market is primarily driven by the exponential increase in data center power consumption from AI workloads, the growing transition from lead-acid to lithium-ion UPS technologies, and the growing integration of on-site renewable energy requiring battery storage for firming and backup.

Key players are Tesla, Inc. (U.S.), LG Energy Solution, Ltd. (South Korea), Samsung SDI Co., Ltd. (South Korea), Contemporary Amperex Technology Co., Ltd. — CATL (China), BYD Company Ltd. (China), Fluence Energy, Inc. (U.S.), Schneider Electric SE (France), Vertiv Holdings Co. (U.S.), Eaton Corporation plc (Ireland), ABB Ltd. (Switzerland), Delta Electronics, Inc. (Taiwan), Hitachi Energy Ltd. (Switzerland), Panasonic Energy Co., Ltd. (Japan), EnerSys (U.S.), and HiTHIUM Energy Storage Technology Co., Ltd. (China).

Asia Pacific is expected to register the highest growth rate in the global battery energy storage market for data centers during the forecast period 2026–2036.

Published Date: Jan-2024

Published Date: Jun-2026

Published Date: Jan-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates