Resources

About Us

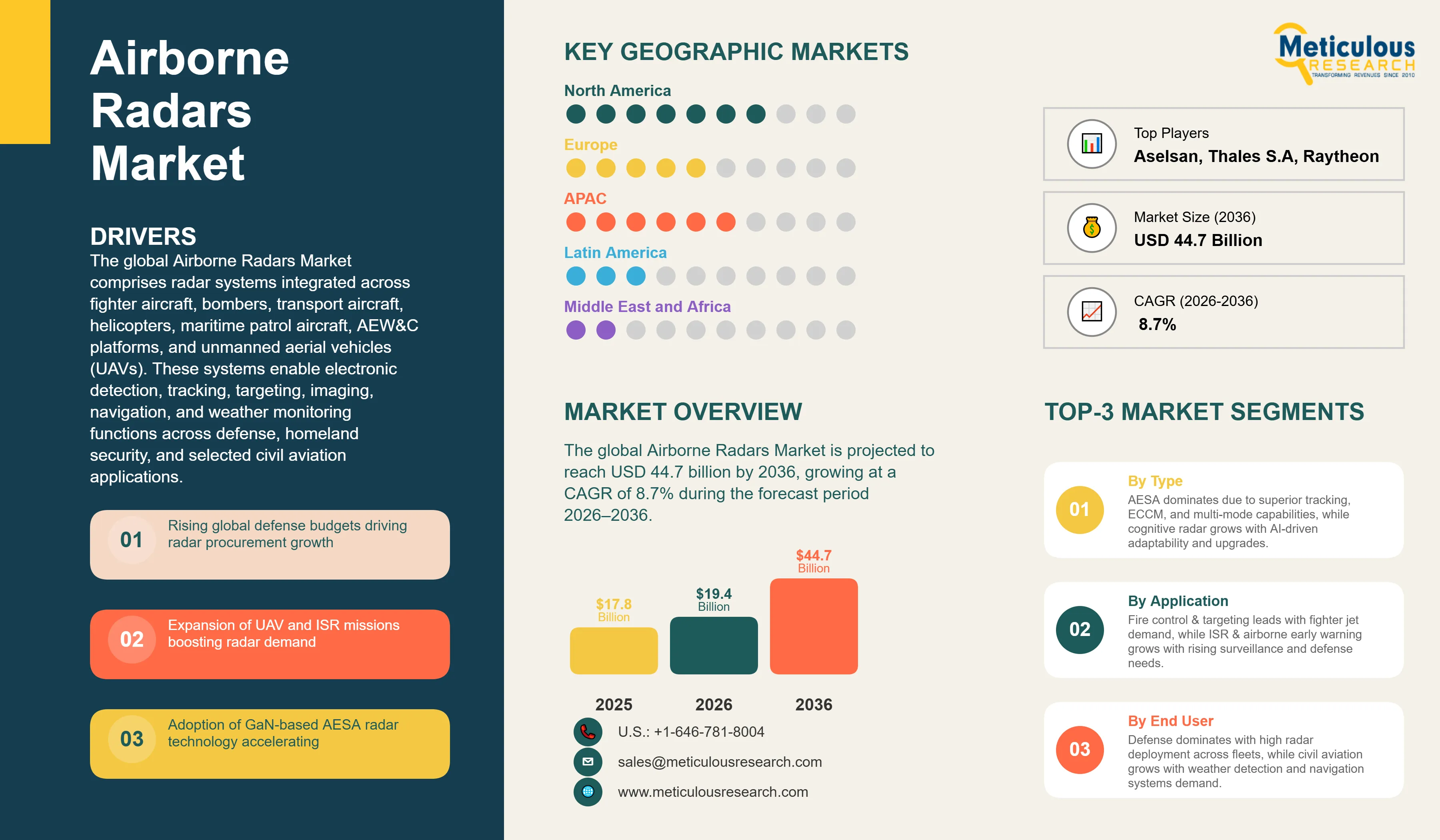

The global Airborne Radars Market was valued at USD 17.8 billion in 2025. The market is projected to reach USD 44.7 billion by 2036 from an estimated USD 19.4 billion in 2026, growing at a CAGR of 8.7% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global Airborne Radars Market comprises radar systems integrated across fighter aircraft, bombers, transport aircraft, helicopters, maritime patrol aircraft, AEW&C platforms, and unmanned aerial vehicles (UAVs). These systems enable electronic detection, tracking, targeting, imaging, navigation, and weather monitoring functions across defense, homeland security, and selected civil aviation applications.

The market continues to benefit from rising geopolitical tensions and accelerated military modernization programs worldwide. The ongoing Russia–Ukraine conflict, elevated Indo-Pacific security risks, and persistent instability across parts of the Middle East have led to sustained increases in defense spending and procurement activity. NATO’s long-standing defense spending benchmark of at least 2% of GDP has further supported investments in airborne surveillance and combat aviation upgrades.

A major demand driver remains the F-35 Lightning II program, which continues to represent the world’s largest single airborne radar production ecosystem. The aircraft is equipped with Northrop Grumman’s AN/APG-81 AESA radar, while the next-generation AN/APG-85 radar is scheduled for Lot 17 aircraft and beyond, entering production from 2025 onward. This transition is expected to create significant upgrade-driven revenue opportunities across advanced fire-control radar systems.

North America continues to benefit from large-scale retrofit demand. A key example is the U.S. Air Force F-16 radar modernization program, which includes deployment of the AN/APG-83 SABR AESA radar across hundreds of aircraft. The cumulative contract value for this program has reached approximately USD 1.6 billion, underscoring strong long-term demand for legacy fleet upgrades.

One of the most important technology transitions in the market is the shift from gallium arsenide (GaAs) to gallium nitride (GaN)-based transmit/receive modules. GaN technology enables higher power density, improved thermal performance, longer detection range, and stronger resistance to electronic countermeasures, while also supporting smaller and lighter radar apertures. This is increasingly important for UAVs, light combat aircraft, and collaborative combat aircraft platforms.

A notable example is Raytheon’s PhantomStrike GaN-based AESA radar, designed as a lightweight, air-cooled radar for UAVs and light combat aircraft. Poland’s selection of this radar for its 36 FA-50PL aircraft further validates the growing commercial potential of compact GaN-based airborne radar systems.

Despite strong growth prospects, the market faces some restraints. High development and procurement costs continue to limit adoption among smaller defense forces and cost-sensitive emerging markets. Advanced AESA radars involve significant capital expenditure not only at procurement but also across integration, maintenance, and lifecycle support.

Supply chain risks also remain an important challenge. Export controls on gallium and limited GaN foundry capacity continue to create lead-time uncertainty and component cost pressure for radar OEMs and defense integrators. In addition, cybersecurity risks are emerging as a critical challenge as airborne radars become increasingly integrated with network-centric warfare and digital battlespace management systems.

|

Parameters |

Details |

|---|---|

|

Market Size by 2036 |

USD 44.7 Billion |

|

Market Size in 2026 |

USD 19.4 Billion |

|

Market Size in 2025 |

USD 17.8 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 8.7% |

|

Dominating Technology |

Active Electronically Scanned Array (AESA) |

|

Fastest Growing Technology |

Software-Defined / Cognitive Radar |

|

Dominating Frequency Band |

X-Band |

|

Fastest Growing Frequency Band |

Ka/Ku-Band |

|

Dominating Platform |

Fixed-wing Military Aircraft (Fighter Jets) |

|

Fastest Growing Platform |

Unmanned Aerial Vehicles (UAVs/UCAVs) |

|

Dominating Application |

Fire Control & Targeting |

|

Fastest Growing Application |

ISR & Airborne Early Warning |

|

Dominating End User |

Defense / Military |

|

Fastest Growing End User |

Civil Aviation (Weather & Terrain Avoidance) |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

GaN-Based AESA Technology Reaching Tipping-Point Adoption Across Fighter and UAV Platforms

One of the key trends in the global Airborne Radars Market is the rapid adoption of gallium nitride (GaN)-based AESA radar technology across new and upgrade programs. This transition shows a clear shift from legacy gallium arsenide (GaAs)-based systems toward higher-performance semiconductor architectures. The scale of deployment across multiple countries indicates that GaN is approaching a technology inflection point in airborne radar systems.

GaN offers measurable performance advantages over GaAs. It enables significantly higher power density and improved thermal efficiency, allowing radars to operate at higher output power with reduced cooling requirements. These advantages translate into longer detection ranges, stronger electronic counter-countermeasure (ECCM) performance, and improved reliability, while also enabling smaller and lighter radar apertures suitable for UAV and light combat platforms.

In the U.S., Raytheon completed the first flight test of its PhantomStrike GaN-based AESA radar on May 6, 2025. The radar is designed as a compact, air-cooled system weighing ~68 kg (150 lbs), significantly lighter than traditional fighter-class AESA radars. This positions it for deployment across UAVs, light combat aircraft, and collaborative combat aircraft platforms.

The U.S. Air Force continues to allocate funding toward advanced radar upgrades. The FY2026 budget includes approximately USD 90 million for F-22 Raptor modernization, including radar and sensor enhancements. This reflects continued investment in high-performance airborne sensing capabilities.

At the platform level, the F-35 program remains the largest airborne radar production ecosystem globally. More than 3,000 AN/APG-81 AESA radars are expected across the planned F-35 fleet, with production extending into the 2030s. The transition to the AN/APG-85 radar from Lot 17 (production beginning 2025) represents a major upgrade cycle within this installed base.

North America is also witnessing large-scale retrofit demand. The U.S. Air Force F-16 radar modernization program covers over 600 aircraft, including active-duty and Air National Guard fleets. The program’s cumulative contract value has reached approximately USD 1.6 billion, highlighting the scale of AESA upgrade demand.

Raytheon is further expanding GaN deployment through its PhantomStrike radar. Poland has selected the system for 36 FA-50PL aircraft, marking one of the first operational deployments of a compact GaN AESA radar in light combat aircraft.

Asia-Pacific is emerging as a major growth center for GaN radar adoption. India’s DRDO is advancing the Virupaksha AESA radar for Su-30MKI upgrades, building on indigenous AESA development programs. South Korea’s Hanwha Systems has initiated production of an indigenous AESA radar for the KF-21 Boramae fighter in 2025, marking a key milestone in domestic radar capability development.

At the system level, GaN-based AESA radars are increasingly being designed for multi-role functionality, including fire control, ISR, electronic warfare support, and high-resolution SAR imaging. Their ability to support simultaneous multi-mode operations is becoming critical for next-generation air combat and network-centric warfare environments.

The simultaneous deployment of GaN radar programs across the U.S., Europe, and Asia-Pacific confirms a clear industry-wide transition. GaN is no longer limited to niche or high-end applications. It is rapidly becoming the baseline technology for new airborne AESA radar systems, with implications for both performance benchmarks and lifecycle cost structures over the next decade.

Sixth-Generation Combat Air Programs and UAV Loyal Wingman Driving Long-term Radar System Requirements

The simultaneous development of sixth-generation combat air programs and unmanned collaborative combat aircraft is emerging as a long-term demand driver for next-generation airborne radar systems. These programs are expected to drive radar innovation and procurement cycles well into the 2030s and beyond, supported by multi-decade defense investments and platform development timelines.

Two major multinational sixth-generation programs are currently at the center of this transition. The Global Combat Air Programme (GCAP), led by the UK, Japan, and Italy, and the Future Combat Air System (FCAS), led by France, Germany, and Spain, are both progressing through advanced development phases. Both programs place sensor fusion and advanced radar systems at the core of their operational architecture.

GCAP formally established its joint government–industry structure in 2025, with BAE Systems, Leonardo, and Japan Aircraft Industrial Enhancement Co. (JAIEC) forming a joint venture with equal 33.3% ownership stakes. The program aims to deliver a sixth-generation combat aircraft by 2035, supported by a fully integrated system-of-systems architecture including unmanned platforms.

The program is expected to involve over USD 40 billion in cumulative development spending through 2035, with total lifecycle investments likely exceeding USD 60 billion as partner nations scale production and system integration. This level of investment indicates the critical role of radar systems in enabling sensor fusion, distributed sensing, and multi-domain combat operations.

Japan’s participation is strategically aligned with regional security dynamics, mainly in response to evolving threats in the Indo-Pacific. The program includes co-development of next-generation radar sensors, reinforcing the importance of radar as a core mission system within sixth-generation platforms.

The Future Combat Air System (FCAS) program similarly emphasizes distributed sensing and network-centric warfare. Airbus-led Remote Carrier unmanned systems are designed to operate alongside manned fighter aircraft, requiring compact, high-performance radar systems capable of operating within constrained size, weight, and power (SWaP) environments.

In parallel, the U.S. is advancing its Collaborative Combat Aircraft (CCA) program, which is expected to procure more than 1,000 autonomous aircraft over time to operate alongside platforms such as the F-35 and Next Generation Air Dominance (NGAD) fighter. These systems will rely heavily on onboard and networked sensors, including lightweight AESA radar systems, for autonomous mission execution.

This shift is creating a new product segment within the Airborne Radars Market. There is growing demand for compact, cost-optimized GaN-based AESA radars designed specifically for UAVs and loyal wingman platforms. These radars must meet strict SWaP constraints while still delivering multi-mode functionality, including target detection, tracking, SAR imaging, and electronic warfare support. Raytheon’s PhantomStrike radar is a key example of this emerging category. The system weighs approximately 68 kg (150 lbs) and is designed as an air-cooled AESA radar, eliminating the need for complex liquid cooling systems. This significantly reduces integration complexity and lifecycle costs, making it suitable for large-scale deployment across collaborative combat aircraft fleets.

The combination of sixth-generation combat air programs and unmanned systems is reshaping radar requirements. Future airborne radar systems will need to support distributed sensing, AI-enabled data processing, multi-platform interoperability, and autonomous decision support. As a result, radar is evolving from a standalone sensor into a core node within a networked combat ecosystem.

This transformation is expected to drive strong demand for advanced airborne radar systems over the next decade, with increasing emphasis on scalability, software-defined architectures, and integration across manned-unmanned teaming environments.

By Technology: In 2026, AESA to Dominate the Global Airborne Radars Market

Based on technology, the market is segmented into AESA, PESA, MSA, and software-defined and cognitive radar systems.

In 2026, AESA is expected to account for the largest share of the global Airborne Radars Market. The segment is projected to maintain its dominance due to its status as the standard technology for new airborne radar programs, particularly in military aviation.

AESA radars offer key advantages over MSA and PESA systems. These include simultaneous multi-mode operation, electronic beam steering, low probability of intercept (LPI), and high reliability due to distributed T/R modules. These capabilities support applications across fire control, ISR, SAR imaging, and electronic warfare.

At the program level, the F-35 AN/APG-81 radar remains the largest AESA production program, with over 3,000 units expected. Retrofit demand is also strong, with the APG-83 SABR deployed across more than 600 U.S. Air Force F-16 aircraft, with cumulative contracts of ~USD 1.6 billion. AESA adoption is also expanding across UAVs and next-generation platforms.

However, software-defined and cognitive radar systems are expected to register the highest CAGR during the forecast period. These systems enable software-based upgrades, AI-driven adaptability, and real-time spectrum management, making them critical for future electronic warfare environments.

Frequency Band Insights

By Frequency Band: In 2026, X-Band to Account for the Largest Share

Based on frequency band, the market is segmented into X-Band, Ku/Ka-Band, L/S-Band, C-Band, W-Band, and multi-band systems.

In 2026, X-Band is expected to account for the largest share of the global Airborne Radars Market. The segment benefits from an optimal balance of detection range, angular resolution, target discrimination, and compact antenna size, making it the preferred band for fighter aircraft fire-control and multi-role radar systems.

X-Band radars account for approximately 45–50% share of the overall airborne fire-control radar deployments, reflecting their widespread use across combat aircraft. Leading systems such as the AN/APG-81 (F-35), APG-83 SABR (F-16), APG-82(V)1 (F-15E), and PhantomStrike AESA radar all operate in the X-Band frequency range, reinforcing its dominance across both new production and retrofit programs.

However, Ku/Ka-Band is projected to register the highest CAGR during the forecast period. These higher-frequency bands (Ku: ~12–18 GHz; Ka: ~27–40 GHz) enable significantly higher-resolution SAR/ISAR imaging, making them increasingly suitable for UAV-mounted radars, maritime surveillance, and precision terrain mapping. The rapid expansion of UAV-based ISR missions is driving demand for compact, high-resolution Ku/Ka-Band radars, mainly in applications where SWaP constraints and imaging accuracy are critical.

By Platform: In 2026, Fighter Aircraft to Hold the Largest Share

Based on platform, the market is segmented into fighter aircraft, helicopters, maritime patrol aircraft, AEW&C aircraft, transport & special mission aircraft, UAVs/UCAVs, and commercial aircraft.

In 2026, fighter aircraft are expected to account for the largest share of the global Airborne Radars Market. This is driven by strong procurement of fifth-generation platforms and large-scale AESA radar upgrades across legacy fleets. The F-35 program remains the primary driver, with Lockheed Martin targeting ~156 aircraft annually, with peak deliveries in the range of 175–190 aircraft per year. The program includes 17 partner and FMS customer nations, supporting a sustained global radar production pipeline through the 2030s. In parallel, a large installed base of fourth-generation fighters, such as F-16, F-15, F/A-18, Eurofighter Typhoon, Dassault Rafale, Saab Gripen, MiG-29, and Su-27 variants, is undergoing AESA radar upgrades, further reinforcing segment dominance.

However, UAVs and UCAVs are projected to register the highest CAGR from 2026 to 2036. The growth of this market is driven by increasing deployment of radar-equipped unmanned systems across ISR, maritime surveillance, counter-drone, and collaborative combat missions. Program-level investments highlight this trend. The MQ-4C Triton program includes ~USD 376.4 million in FY2026 funding, while the MQ-25 Stingray program is supported by ~USD 305.5 million in FY2026 funding. These investments reflect the growing scale of radar-enabled UAV procurement.

The increasing integration of SAR, maritime surveillance, and targeting radars on MALE and HALE UAV platforms is expected to further drive demand, mainly in applications requiring persistent surveillance and autonomous mission capability.

By Application: In 2026, Fire Control & Targeting to Hold the Largest Share

Based on application, the market is segmented into fire control & targeting, ISR & airborne early warning, weather detection, terrain following & SAR/ISAR mapping, ASW, maritime surveillance, and navigation.

In 2026, fire control & targeting is expected to account for the largest share of the global Airborne Radars Market. The large share of this segment is driven by high procurement volumes across global fighter aircraft fleets and the premium value of fire control radar systems. The segment benefits from both new production and retrofit demand. Ongoing manufacturing of fifth-generation aircraft, mainly the F-35, and large-scale AESA upgrades across fourth-generation fleets continue to drive demand.

Fire control radars command the highest per-unit pricing in the market due to their complexity, weapon system integration, and stringent qualification requirements. For example, a U.S. Air Force contract for 31 APG-83 AESA radars was valued at ~USD 88.24 million, highlighting the strong unit economics of this segment.

However, the Airborne Radars Market for the ISR and airborne early warning application segment is projected to grow at the fastest CAGR from 2026 to 2036, driven by increasing investments in persistent surveillance, maritime domain awareness, and network-centric battle management systems. High-value programs continue to support this segment. Platforms such as the Boeing E-7A Wedgetail and Saab GlobalEye are witnessing growing international adoption. In addition, modernization initiatives to replace aging AWACS fleets are creating long-term procurement opportunities.

The expansion of ISR missions is also visible in UAV deployments. NATO’s RQ-4D Phoenix deployment in Finland in 2025 highlights the increasing use of radar-equipped HALE UAVs for persistent surveillance across contested regions.

Based on geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

In 2026, North America is expected to account for the largest share of the global Airborne Radars Market, at approximately 35% of global revenue. The region’s dominance is driven by the scale and technological sophistication of U.S. defense procurement programs.

The U.S. Department of Defense operates the world’s most extensive airborne radar portfolio. Key programs include the F-35 AN/APG-81 production (with over 3,000 units expected) and the transition to the AN/APG-85 from Lot 17 (2025 onward). Retrofit demand is also significant, with the F-16 APG-83 upgrade covering over 600 aircraft, with cumulative contracts of ~USD 1.6 billion. Additional programs include the F-15E/EX APG-82 radar, ongoing F-22 radar upgrades, and the B-21 Raider, which is expected to incorporate advanced AESA radar systems.

The U.S. Navy further strengthens regional demand through programs such as the F/A-18E/F APG-79, supported by a ~USD 603 million radar support contract (2025), along with the E-2D Advanced Hawkeye, P-8A Poseidon, and MQ-4C Triton surveillance radar systems. Canada contributes through F-35A procurement and continued modernization of legacy fleets.

Europe holds the second-largest share, driven by widespread AESA radar upgrades across NATO air forces. Key programs include the Eurofighter Typhoon Captor-E AESA radar, developed by the Euroradar consortium, the Rafale F4 upgrade with the RBE2-AA AESA radar, and continued Gripen E/F production with advanced AESA radar systems. In addition, the Global Combat Air Programme is driving long-term investment in next-generation radar technologies across the UK and Italy industrial base.

The Asia Pacific Airborne Radars Market is poised to grow at the fastest CAGR during the forecast period, driven by large-scale modernization programs across multiple defense markets. South Korea’s KF-21 Boramae program and FA-50 radar upgrades represent parallel indigenous and export-driven AESA deployments. Japan’s FY2025 defense budget of ~JPY 7.95 trillion (USD ~50+ billion), combined with GCAP participation and maritime surveillance investments, further drives the strong demand in the region.

India’s Su-30MKI upgrade program, covering ~300 aircraft, alongside Tejas MkI/MkII radar programs, represents one of the largest modernization efforts in the region. China continues to expand indigenous AESA radar deployment across platforms such as J-20, J-16, and J-10C, while Taiwan’s F-16V upgrade program with APG-83 AESA radar reflects continued investment driven by regional security dynamics.

Overall, the Asia Pacific Airborne Radars Market is expected to grow at the fastest CAGR through 2036, driven by rising defense budgets, indigenous radar development, and strong fighter and UAV procurement.

The global Airborne Radars Market is highly concentrated, dominated by a few defense electronics prime contractors with the technological expertise, manufacturing scale, and long-standing defense procurement relationships required to develop and produce advanced radar systems. The competitive landscape is focused around the U.S. and Western European defense majors, supported by Israeli and Asia-Pacific players with growing indigenous AESA radar capabilities. High entry barriers, long development cycles, and dependence on government contracts continue to shape competition, with increasing focus on GaN-based AESA systems, software-defined radar architectures, and network-centric integration.

Key players operating in the global Airborne Radars Market are Northrop Grumman Corporation, RTX Corporation / Raytheon, Lockheed Martin Corporation, Leonardo S.p.A., Thales S.A., Saab AB, BAE Systems plc, Hensoldt AG, Israel Aerospace Industries / Elta Systems, Elbit Systems Ltd., L3Harris Technologies, Inc., Mitsubishi Electric Corporation, Hanwha Systems, Aselsan A.Ş., Indra Sistemas S.A., Toshiba Corporation, China Electronics Technology Group Corporation, Aviation Industry Corporation of China, and Defence Research and Development Organisation, among others.

This report provides market size estimates and forecasts for each segment and sub-segment at the global, regional, and country levels. The report further offers an in-depth analysis of the latest industry trends, market dynamics, technological advancements, regulatory developments, and key strategic initiatives across each sub-segment for the forecast period 2026–2036.

For the purpose of this study, the global Airborne Radars Market has been segmented based on technology, frequency band, range, platform, application, end user, and geography.

|

Segment |

Sub-Segments |

|---|---|

|

By Technology |

Active Electronically Scanned Array (AESA), Passive Electronically Scanned Array (PESA), Mechanically Scanned Array (MSA), Software-Defined / Cognitive Radar |

|

By Frequency Band |

X-Band, Ku/Ka-Band, L/S-Band, C-Band, W-Band, Multi-Band |

|

By Range |

Short Range (< 50 km), Medium Range (50–200 km), Long Range (> 200 km) |

|

By Platform |

Fighter Aircraft, Helicopters, Maritime Patrol Aircraft, AEW&C Aircraft, Transport & Special Mission Aircraft, UAVs / UCAVs, Commercial Aircraft |

|

By Application |

Fire Control & Targeting, ISR & Airborne Early Warning, Weather Detection & Avoidance, Terrain Following & Ground Mapping (SAR/ISAR), Anti-Submarine Warfare (ASW), Maritime Surveillance, Navigation |

|

By End User |

Defense / Military, Civil Aviation, Homeland Security & Law Enforcement |

|

By Geography |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

By Technology (Revenue, USD Billion, 2026–2036)

By Frequency Band (Revenue, USD Billion, 2026–2036)

By Range (Revenue, USD Billion, 2026–2036)

By Platform (Revenue, USD Billion, 2026–2036)

By Application (Revenue, USD Billion, 2026–2036)

By End User (Revenue, USD Billion, 2026–2036)

By Geography (Revenue, USD Billion, 2026–2036)

The global Airborne Radars Market is expected to reach USD 44.7 billion by 2036 from an estimated USD 19.4 billion in 2026, at a CAGR of 8.7% during the forecast period 2026–2036.

In 2026, AESA (Active Electronically Scanned Array) is expected to hold the largest market share, driven by its multi-mode multi-function capability, electronic beam agility, LPI characteristics, high reliability, and established production across all major fighter aircraft programs globally.

Software-defined and cognitive radar is expected to register the highest CAGR during the forecast period 2026–2036, driven by defense agencies’ shift toward open-architecture, software-reprogrammable systems enabling rapid capability insertion and AI-enabled adaptive signal processing in contested electromagnetic environments.

In 2026, X-Band is expected to hold the largest market share, driven by its optimal combination of range, resolution, and compact aperture dimensions for fighter aircraft and helicopter radar applications.

In 2026, fighter aircraft is expected to hold the largest market share, driven by the dominant revenue contribution of F-35 APG-81/85 production, the F-16 APG-83 upgrade program, F-15EX APG-82 production, and numerous international fighter AESA modernization programs.

In 2026, fire control and targeting is expected to hold the largest market share of the global Airborne Radars Market, reflecting the high per-unit value and procurement volume of fighter aircraft fire control radar systems globally.

The growth of this market is primarily driven by escalating geopolitical tensions and consequent global defense budget increases accelerating procurement of new airborne platforms and radar upgrades; the F-35 production program and successor AN/APG-85 development representing the world’s largest AESA production pipeline; the broad adoption of GaN semiconductor technology enabling more capable, lighter, and cost-competitive airborne AESA systems (including Raytheon’s PhantomStrike first flight test in May 2025); the development of GCAP, FCAS, and collaborative combat aircraft programs driving next-generation radar requirements; and the rapid expansion of UAV-mounted radar applications for ISR, maritime surveillance, and autonomous targeting.

Key players in the global Airborne Radars Market include Northrop Grumman Corporation (U.S.), RTX Corporation / Raytheon (U.S.), Lockheed Martin Corporation (U.S.), Leonardo S.p.A. (Italy), Thales S.A. (France), Saab AB (Sweden), BAE Systems plc (UK), Hensoldt AG (Germany), Israel Aerospace Industries / Elta Systems (Israel), Elbit Systems Ltd. (Israel), L3Harris Technologies, Inc. (U.S.), Mitsubishi Electric Corporation (Japan), Aselsan A.?. (Turkey), and Indra Sistemas S.A. (Spain).

Asia Pacific is expected to register the highest growth rate in the global Airborne Radars Market during the forecast period 2026–2036, driven by South Korea’s indigenous KF-21 AESA production and FA-50PL radar modernization, Japan’s GCAP commitment and maritime patrol investment, India’s Super Sukhoi Virupaaksha GaN AESA upgrade program covering 300 aircraft, and Australia’s maritime surveillance and ISR radar investments.

1. INTRODUCTION

1.1. Market Definition & Scope

1.2. Market Ecosystem

1.3. Currency & Pricing Assumptions

1.4. Key Stakeholders

2. RESEARCH METHODOLOGY

2.1. Research Process

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research / Interviews with Key Opinion Leaders from the Industry

2.3. Market Assessment

2.3.1. Market Size Estimation

2.3.1.1. Bottom-up Approach

2.3.1.2. Top-down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

2.4. Limitations of the Study

3. EXECUTIVE SUMMARY

3.1. Overview

3.2. Market by Technology

3.3. Market by Frequency Band

3.4. Market by Range

3.5. Market by Platform

3.6. Market by Application

3.7. Market by End User

3.8. Market by Geography

3.9. Competitive Landscape Snapshot

3.10. Key Strategic Insights

3.11. Analyst Recommendations

4. MARKET INSIGHTS

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Escalating Geopolitical Tensions and Global Defense Budget Increases

4.2.1.2. F-35 Production Program and AN/APG-85 Next-Generation Radar Development

4.2.1.3. Transition to GaN Semiconductor Technology in AESA T/R Modules

4.2.1.4. Increasing Demand for ISR and Airborne Early Warning Capabilities

4.2.1.5. Rapid Expansion of UAV and Collaborative Combat Aircraft Programs

4.2.2. Restraints

4.2.2.1. High Development and Per-Unit Procurement Costs of AESA Systems

4.2.2.2. Export Controls on Gallium and Limited GaN Foundry Capacity

4.2.2.3. Cybersecurity Threats in Networked Airborne Radar Systems

4.2.2.4. SWaP Constraints for UAV-Mounted Radar Integration

4.2.3. Opportunities

4.2.3.1. GCAP and FCAS Sixth-Generation Radar System Development Contracts

4.2.3.2. Cost-Competitive Compact GaN AESA Radars for Light Combat and UAV Platforms

4.2.3.3. AEW&C Platform Modernization and E-3 Sentry Replacement Programs

4.2.3.4. Indo-Pacific Maritime Patrol and ASW Radar Fleet Expansion

4.2.4. Challenges

4.2.4.1. Qualified Workforce and Supply Chain Capacity for GaN Component Production

4.2.4.2. Spectrum Management and Frequency Allocation in Contested Environments

4.2.4.3. Integration Complexity for Multi-Function RF Aperture Systems

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of Substitutes

4.3.4. Threat of New Entrants

4.3.5. Degree of Competition

4.4. Regulatory Landscape & Export Control Standards

4.4.1. U.S. — ITAR, EAR, DoD Procurement Frameworks

4.4.2. Europe — EU Export Controls, NATO Interoperability Standards

4.4.3. Asia Pacific — Japan, South Korea, India Defense Procurement Frameworks

4.4.4. Other Key Regulatory Jurisdictions

4.5. Value Chain Analysis

4.6. Impact of Macroeconomic Factors

5. AIRBORNE RADARS MARKET, BY TECHNOLOGY

5.1. Overview

5.2. Active Electronically Scanned Array (AESA)

5.3. Passive Electronically Scanned Array (PESA)

5.4. Mechanically Scanned Array (MSA)

5.5. Software-Defined / Cognitive Radar

6. AIRBORNE RADARS MARKET, BY FREQUENCY BAND

6.1. Overview

6.2. X-Band

6.3. Ku/Ka-Band

6.4. L/S-Band

6.5. C-Band

6.6. W-Band

6.7. Multi-Band

7. AIRBORNE RADARS MARKET, BY RANGE

7.1. Overview

7.2. Short Range (< 50 km)

7.3. Medium Range (50–200 km)

7.4. Long Range (> 200 km)

8. AIRBORNE RADARS MARKET, BY PLATFORM

8.1. Overview

8.2. Fighter Aircraft

8.3. Helicopters

8.4. Maritime Patrol Aircraft

8.5. AEW&C Aircraft

8.6. Transport & Special Mission Aircraft

8.7. UAVs / UCAVs

8.8. Commercial Aircraft

9. AIRBORNE RADARS MARKET, BY APPLICATION

9.1. Overview

9.2. Fire Control & Targeting

9.3. ISR & Airborne Early Warning

9.4. Weather Detection & Avoidance

9.5. Terrain Following & Ground Mapping (SAR/ISAR)

9.6. Anti-Submarine Warfare (ASW)

9.7. Maritime Surveillance

9.8. Navigation

10. AIRBORNE RADARS MARKET, BY END USER

10.1. Overview

10.2. Defense / Military

10.3. Civil Aviation

10.4. Homeland Security & Law Enforcement

11. AIRBORNE RADARS MARKET, BY GEOGRAPHY

11.1. Overview

11.2. North America

11.2.1. U.S.

11.2.2. Canada

11.3. Europe

11.3.1. U.K.

11.3.2. Germany

11.3.3. France

11.3.4. Italy

11.3.5. Sweden

11.3.6. Spain

11.3.7. Rest of Europe

11.4. Asia Pacific

11.4.1. Japan

11.4.2. China

11.4.3. South Korea

11.4.4. India

11.4.5. Australia

11.4.6. Rest of Asia Pacific

11.5. Latin America

11.5.1. Brazil

11.5.2. Mexico

11.5.3. Rest of Latin America

11.6. Middle East & Africa

11.6.1. Israel

11.6.2. Saudi Arabia

11.6.3. UAE

11.6.4. Rest of Middle East & Africa

12. COMPETITIVE LANDSCAPE

12.1. Overview

12.2. Key Growth Strategies

12.2.1. Market Differentiators

12.2.2. Synergy Analysis: Major Deals and Strategic Alliances

12.3. Competitive Dashboard

12.3.1. Industry Leaders

12.3.2. Market Differentiators

12.3.3. Vanguards

12.3.4. Emerging Companies

12.4. Competitive Benchmarking

12.5. Market Share / Ranking Analysis (2025)

13. COMPANY PROFILES

Business Overview, Financial Overview, Product Portfolio, Strategic Developments, and SWOT Analysis

13.1. Northrop Grumman Corporation (U.S.)

13.2. RTX Corporation / Raytheon (U.S.)

13.3. Lockheed Martin Corporation (U.S.)

13.4. Leonardo S.p.A. (Italy)

13.5. Thales S.A. (France)

13.6. Saab AB (Sweden)

13.7. BAE Systems plc (U.K.)

13.8. Hensoldt AG (Germany)

13.9. Israel Aerospace Industries / Elta Systems (Israel)

13.10. Elbit Systems Ltd. (Israel)

13.11. L3Harris Technologies, Inc. (U.S.)

13.12. Mitsubishi Electric Corporation (Japan)

13.13. Toshiba Corporation (Japan)

13.14. Hanwha Systems (South Korea)

13.15. Aselsan A.Ş. (Turkey)

13.16. Indra Sistemas S.A. (Spain)

13.17. Aviation Industry Corporation of China (China)

13.18. China Electronics Technology Group Corporation (China)

13.19. Others

14. APPENDIX

14.1. Questionnaire

14.2. Customization Options

14.3. Abbreviations

14.4. List of Data Sources

Published Date: Apr-2026

Published Date: Sep-2025

Subscribe to get the latest industry updates