Resources

About Us

Drone Detection Radar Systems Market Size, Share and Trends Analysis by Radar Type, Frequency Band, Application, End User, and Integration Type — Global Opportunity Analysis and Industry Forecast (2026 to 2036)

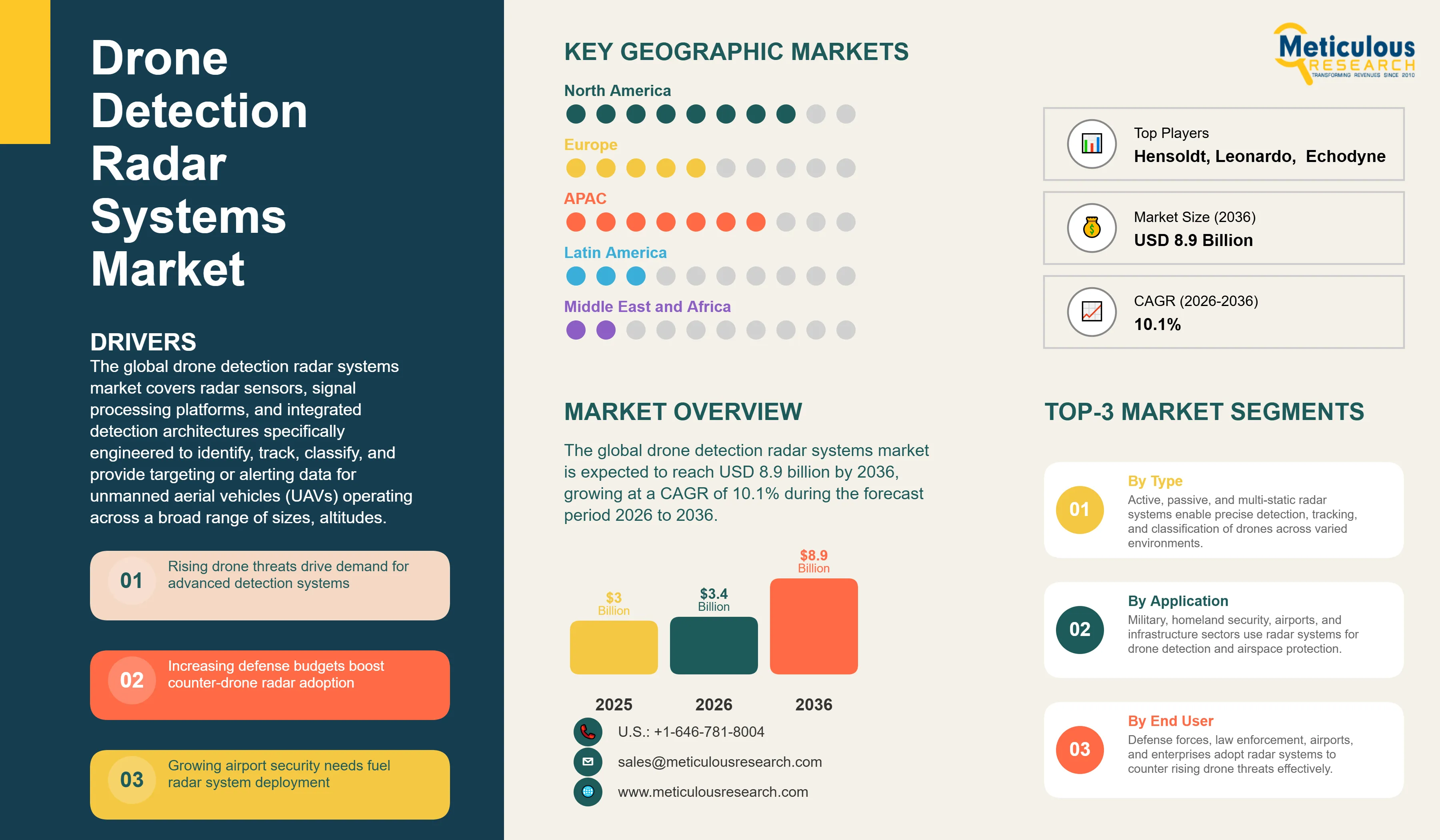

Report ID: MRAD - 1041908 Pages: 265 Apr-2026 Formats*: PDF Category: Aerospace and Defense Delivery: 24 to 72 Hours Download Free Sample ReportThe global drone detection radar systems market was valued at USD 3.0 billion in 2025. This market is expected to reach USD 8.9 billion by 2036 from an estimated USD 3.4 billion in 2026, growing at a CAGR of 10.1% during the forecast period 2026 to 2036.

The global drone detection radar systems market covers radar sensors, signal processing platforms, and integrated detection architectures specifically engineered to identify, track, classify, and provide targeting or alerting data for unmanned aerial vehicles (UAVs) operating across a broad range of sizes, altitudes, and operational profiles. The market spans active radar technologies including active electronically scanned array (AESA), pulse-Doppler, and frequency-modulated continuous-wave (FMCW) radar systems; passive radar architectures exploiting ambient radio frequency emissions; and multi-static radar configurations deploying spatially separated transmitters and receivers to achieve detection geometries optimized for small, low-radar-cross-section (RCS) drone targets. These systems serve defense forces, law enforcement agencies, airport authorities, commercial enterprises, and government agencies across applications spanning military and defense operations, homeland security, critical infrastructure protection, aviation security, public event security, and industrial facility protection.

The growth of the global drone detection radar systems market is primarily driven by the rapidly escalating threat environment created by the proliferation of commercially available drone technology capable of delivering surveillance, electronic warfare, explosive payload, and cyberattack capabilities to non-state actors, criminal organizations, and adversarial military forces at unprecedented accessibility and low cost. The armed drone threat has transitioned from an asymmetric capability available only to well-resourced state military forces into a mainstream tactical tool employed by a broad spectrum of conflict actors, as demonstrated by the extensive and innovative use of commercial quadcopter drones modified for grenade and munitions delivery in the Ukraine conflict, the complex swarm drone attacks on Saudi Aramco's Abqaiq and Khurais oil processing facilities, and the documented use of drones for surveillance and smuggling at correctional facilities, military installations, and international borders globally. This threat environment is generating urgent and sustained procurement investment by defense establishments, homeland security agencies, and critical infrastructure operators in radar detection systems capable of providing the earliest possible detection and cueing of drone threats to enable protective countermeasure response.

Two transformative opportunities are defining the market's long-term trajectory. The integration of artificial intelligence signal processing algorithms into drone detection radar systems is enabling a new generation of detection capability that can distinguish drone radar signatures from bird and other airspace clutter with dramatically improved discrimination accuracy, classify detected drones by type and payload probability based on micro-Doppler blade rotation signatures and flight behavior analysis, and manage simultaneous multi-target tracking scenarios across complex urban and cluttered airspace environments that challenge conventional radar signal processing. Simultaneously, the expansion of civil airspace integration of commercial drone operations under UTM frameworks being developed by aviation regulators globally is creating a large new procurement market for drone detection radar at airports, heliports, urban air mobility corridors, and dense commercial drone delivery operating zones where airspace surveillance is required to ensure safe and compliant drone traffic management.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 8.9 Billion |

|

Market Size in 2026 |

USD 3.4 Billion |

|

Market Size in 2025 |

USD 3.0 Billion |

|

Revenue Growth Rate (2026 to 2036) |

CAGR of 10.1% |

|

Dominating Radar Type |

Active Radar Systems |

|

Fastest Growing Radar Type |

Multi-Static Radar Systems |

|

Dominating Frequency Band |

X-Band |

|

Fastest Growing Frequency Band |

Ku/Ka-Band |

|

Dominating Detection Range |

Medium Range (5 to 20 km) |

|

Fastest Growing Detection Range |

Long Range (above 20 km) |

|

Dominating Platform |

Fixed/Stationary Systems |

|

Fastest Growing Platform |

Mobile/Vehicle-Mounted Systems |

|

Dominating Application |

Military and Defense |

|

Fastest Growing Application |

Critical Infrastructure Protection |

|

Dominating End User |

Defense Forces |

|

Fastest Growing End User |

Airport Authorities |

|

Dominating Integration Type |

Multi-Sensor Integrated Systems |

|

Fastest Growing Integration Type |

Command and Control Integrated Systems |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Integration of AI-Powered Signal Processing and Multi-Sensor Fusion

The integration of artificial intelligence and machine learning algorithms into drone detection radar signal processing represents the most consequential technology advancement currently reshaping the capability and commercial differentiation of drone detection radar systems, enabling detection performance across challenging clutter environments, small target sizes, and complex multi-drone scenarios that conventional Doppler processing and threshold-based detection algorithms cannot reliably achieve. The fundamental detection challenge of drone radar is the similarity of small commercial drone radar cross-section signatures to those of birds and other airspace clutter objects, combined with the low radar cross-section of nano-drone and micro-drone targets that may present effective radar areas below 0.01 square meters, placing them below the detection threshold of radar systems designed for conventional aircraft detection. AI-based signal processing approaches including convolutional neural networks trained on extensive drone radar signature datasets and recurrent neural network architectures capable of analyzing temporal signature evolution are achieving drone versus bird discrimination accuracy rates exceeding 95% in operationally relevant clutter environments, a fundamental performance advance that is driving procurement preference for AI-enabled radar platforms.

Multi-sensor fusion architectures that combine radar primary detection with radio frequency (RF) signal detection of drone control links, electro-optical and infrared camera cueing for visual identification, and acoustic sensor arrays for short-range near-ground detection are delivering layered detection capability that significantly exceeds what any single sensor modality can achieve independently. Radar provides all-weather, day-night, long-range primary detection; RF detection identifies drone communication protocols and control signal sources enabling drone operator geolocation; EO/IR cameras provide visual identification and classification confirmation; and acoustic sensors provide last-resort detection for drones operating in RF-silent modes or at very low altitudes where radar coverage degrades. Leading suppliers including Thales, Hensoldt, and SRC are architecting their drone detection solutions as fusion management platforms that seamlessly integrate data from multiple sensor types into a unified threat picture, and this multi-sensor integration capability is emerging as the primary competitive differentiator in sophisticated defense and critical infrastructure procurement programs.

Growing Adoption of AESA Radar Technology for Drone Detection

The adoption of active electronically scanned array radar technology for drone detection applications is accelerating as the cost of AESA systems continues to decline through semiconductor technology advances and volume production scale, making AESA capabilities accessible for drone detection applications that previously could only justify conventional mechanically scanned or fixed-beam radar architectures. AESA radar systems offer fundamentally superior drone detection performance relative to mechanically scanned alternatives through their ability to simultaneously perform multiple radar functions including wide-area surveillance scanning, precision tracking of multiple detected drone targets, and high-range-resolution imaging for target classification, all within the same hardware platform without the physical limitations and mechanical reliability constraints of rotating antenna systems. The electronic beam steering capability of AESA radar enables sub-millisecond beam repositioning for agile tracking of fast-maneuvering drone swarms and the rapid revisit rates necessary to maintain track continuity on small, agile drone targets that can accelerate, decelerate, and change direction more rapidly than conventional aircraft.

Miniaturization advances in gallium nitride (GaN) and gallium arsenide (GaAs) semiconductor components that constitute the transmit/receive modules of AESA arrays are enabling compact, low-power AESA radar systems suitable for vehicle-mounted, portable, and fixed small-footprint counter-drone applications. Echodyne Corp.'s metamaterials-based AESA radar platforms represent a notable example of AESA miniaturization applied specifically to counter-drone detection, achieving impressive detection ranges in compact form factors compatible with mobile platform integration. Raytheon Technologies and Northrop Grumman are applying their extensive AESA development heritage from advanced military radar programs to purpose-built drone detection AESA variants that deliver military-grade detection performance in configurations optimized for the power, size, and cost requirements of counter-drone deployment scenarios.

Expansion of Portable and Mobile Drone Detection Systems

The growing demand for deployable drone detection radar capability that can be rapidly transported, set up, and operated by small teams without specialized technical infrastructure is driving significant product development investment in portable and mobile drone detection radar platforms that extend detection capability beyond fixed-site installations to forward military operating bases, temporary security perimeters for high-value events and public gatherings, expeditionary combat operations, and rapidly evolving border security scenarios. Portable drone detection radar systems are being developed to operate within backpack-transportable form factors weighing under 15 kilograms, with battery-powered operation durations of several hours, rapid deployment times under ten minutes, and wireless communication integration for mesh networking of multiple portable sensors into distributed detection networks that provide overlapping coverage without the infrastructure requirements of fixed-site radar installations.

Vehicle-mounted mobile drone detection radar systems represent a rapidly growing platform category serving military convoy protection, mobile command post security, and law enforcement rapid response applications where a dedicated drone detection radar system must be transported and operated from standard military or law enforcement vehicles without requiring vehicle modification or specialized mounting infrastructure. Companies including Blighter Surveillance Systems and Hensoldt are developing compact radar systems specifically designed for integration into the confined mounting points and power supply constraints of standard military tactical vehicles, enabling organic counter-drone awareness for mobile ground force elements that are increasingly vulnerable to commercially available drone surveillance and attack capabilities in contemporary conflict environments.

Rising Threat of Unauthorized and Malicious Drones

The rapidly escalating global threat posed by unauthorized and maliciously operated drone platforms constitutes the most urgent and immediate structural driver of the drone detection radar systems market, as drone incidents across military, governmental, and civilian contexts have grown in frequency, sophistication, and consequence at a pace that has overtaken the protective deployment of drone detection systems at the majority of vulnerable sites globally. Documented drone incidents demonstrate the breadth and severity of the threat landscape: the January 2024 Tower 22 base attack in Jordan that killed three U.S. service members utilized one-way attack drones that evaded existing base protection systems; Houthi forces have deployed sophisticated drone and anti-ship missile combinations that have disrupted global shipping through the Red Sea; and criminal organizations in multiple countries are systematically using drones to conduct aerial surveillance of law enforcement operations, deliver contraband into correctional facilities, and coordinate organized criminal activities with real-time aerial intelligence unavailable by any other means. This documented threat environment is creating urgent procurement imperatives for drone detection capabilities across the defense, homeland security, and critical infrastructure sectors that are driving accelerated investment in radar-based detection as the foundational sensor technology for drone awareness.

Increasing Defense and Homeland Security Spending

The sustained global expansion of defense budgets and homeland security spending in response to the evolving drone threat is generating large and growing procurement programs for counter-unmanned aerial systems (C-UAS) capabilities in which drone detection radar systems constitute the essential detection layer. NATO member states' commitment to defense spending targets of 2% of gross domestic product or above, combined with the urgent C-UAS capability requirements demonstrated by conflicts in Ukraine and the Middle East, are generating synchronized and substantial drone detection procurement programs across multiple Allied nations simultaneously. The United States Department of Defense's Joint Counter-Small Unmanned Aircraft Systems Office (JCO) has identified counter-drone capability as one of the highest operational priority gaps requiring urgent investment, and its multi-billion-dollar C-UAS program portfolio includes detection radar systems deployed across Army, Navy, Air Force, and Marine Corps installations and forward operating bases globally. The U.S. Department of Homeland Security's parallel counter-drone investment programs targeting the protection of the aviation system, federal facilities, and national special security events from drone threats represent a substantial second domestic procurement channel for drone detection radar systems separate from military procurement.

Integration with AI and Multi-Sensor Fusion Systems

The commercial opportunity created by developing and delivering AI-enhanced, multi-sensor integrated drone detection solutions that dramatically outperform single-sensor radar-only systems represents the highest-value market differentiation opportunity in the drone detection radar systems market over the forecast period. Defense and critical infrastructure customers are increasingly specifying multi-sensor integration as a mandatory system requirement rather than an optional enhancement in their drone detection procurement programs, recognizing that the complex, cluttered operational environments of military bases, airports, and urban infrastructure sites require the complementary detection capabilities of radar, RF, EO/IR, and acoustic sensors working in a fused detection architecture to achieve the detection reliability and false alarm rates acceptable for operational deployment. Equipment suppliers that can offer pre-integrated, tested, and operationally validated multi-sensor fusion platforms with AI-powered threat assessment and decision support are capturing premium contract values and preferred supplier positions relative to competitors offering point radar solutions that require customer integration of the multi-sensor detection architecture.

Increasing Adoption in Smart Cities and Airports

The expanding adoption of drone detection radar systems in smart city infrastructure and airport airspace management represents a large and rapidly growing civil market opportunity that complements the established defense and homeland security market in scale and growth rate. International airports face a documented and growing drone incursion threat that has resulted in major flight disruption events at London Gatwick, Dubai International, Newark Liberty, and numerous other airports globally, creating both regulatory requirements and operational imperatives for airport authorities to deploy detection radar providing continuous surveillance of the airspace within several kilometers of the runway environment. The International Civil Aviation Organization's ongoing development of UTM standards for drone traffic management is establishing the regulatory framework that will mandate airspace monitoring infrastructure deployment at airports globally, with drone detection radar serving as the primary surveillance sensor for airspace awareness in the complex, traffic-dense environments surrounding major aviation hubs. Smart city programs in Singapore, the UAE, and European municipalities are evaluating and piloting drone detection radar as a component of integrated urban airspace management systems designed to enable safe commercial drone delivery and urban air mobility operations while providing security monitoring of unauthorized drone activity in populated urban areas.

By Radar Type: In 2026, Active Radar Systems to Dominate

Based on radar type, the global drone detection radar systems market is segmented into active radar systems (AESA, pulse-Doppler, FMCW), passive radar systems, multi-static radar systems, and other radar types. In 2026, the active radar systems segment is expected to account for the largest share of the global drone detection radar systems market. Active radar systems dominate the market because they provide the all-weather, day-night, long-range detection performance and reliable standalone operation capability that defense and security customers require as the foundational detection sensor in their counter-drone architectures. AESA radar systems offer the highest performance in terms of simultaneous multi-target tracking, beam agility, and electronic protection against jamming. Pulse-Doppler radar systems provide excellent velocity discrimination that enables moving drone detection against stationary ground clutter, while FMCW radar systems offer cost-effective short to medium range detection in compact form factors suitable for portable and vehicle-mounted applications. The well-established procurement track records, extensive field deployment experience, and broad supplier ecosystem of active radar technologies support their continued dominant position across defense, homeland security, and airport procurement programs.

However, the multi-static radar systems segment is projected to register the highest CAGR during the forecast period. Multi-static radar configurations deploy spatially separated transmitter and receiver nodes to illuminate drone targets from multiple geometric angles simultaneously, overcoming the radar cross-section nulls that cause monostatic radars to temporarily lose tracking continuity on targets maneuvering to present minimal RCS aspect. This geometric diversity advantage is particularly valuable for detecting small drone targets and drone swarms executing evasive maneuvers, and the growing sophistication of adversarial drone operators in exploiting monostatic radar limitations is driving interest in multi-static architectures among defense procurement agencies evaluating next-generation counter-drone detection capabilities.

By Frequency Band: In 2026, X-Band to Hold the Largest Share

Based on frequency band, the global drone detection radar systems market is segmented into L-Band, S-Band, C-Band, X-Band, and Ku/Ka-Band. In 2026, the X-Band segment is expected to account for the largest share of the global drone detection radar systems market. X-Band radar (8 to 12 GHz) represents the optimal frequency band for drone detection applications, offering the combination of sufficient wavelength for atmospheric transmission under most weather conditions, antenna aperture sizes compatible with man-portable and vehicle-mounted system form factors, and range resolution capable of resolving the micro-Doppler signatures of drone rotor and propeller blade rotation that are the primary radar signature discriminator for drone identification and classification. The wide deployment of X-Band marine and weather radar technology has established a mature supplier ecosystem for X-Band components and antenna systems that enables cost-effective drone detection radar development relative to higher-frequency bands. Leading drone detection radar suppliers including Blighter Surveillance Systems, Hensoldt, and SRC have developed their primary drone detection radar product lines in the X-Band, and the large installed base of X-Band drone detection systems in military and security deployments globally establishes this frequency band's market leadership.

However, the Ku/Ka-Band segment is projected to register the highest CAGR during the forecast period. The higher frequencies of Ku-Band (12 to 18 GHz) and Ka-Band (26.5 to 40 GHz) radar provide superior micro-Doppler resolution for rotor blade signature analysis, enabling more detailed drone classification and even identification of specific drone models based on characteristic blade rotation patterns. The finer range resolution achievable at millimeter-wave Ka-Band frequencies enables imaging-quality target characterization at short ranges that is valuable for high-confidence drone identification in urban and facility protection scenarios. Miniaturized solid-state Ku and Ka-Band radar modules enabled by advanced semiconductor manufacturing are making these higher-frequency radar approaches increasingly cost-competitive for drone detection applications, driving growing adoption particularly in short-range portable and automated point-defense applications.

By Detection Range: In 2026, Medium Range (5 to 20 km) to Hold the Largest Share

Based on detection range, the global drone detection radar systems market is segmented into short range (below 5 km), medium range (5 to 20 km), and long range (above 20 km). In 2026, the medium range (5 to 20 km) segment is expected to account for the largest share of the global drone detection radar systems market. Medium-range drone detection radar systems represent the optimal capability tier for the largest proportion of current deployment scenarios, providing detection range adequate for airbase and military installation perimeter protection, airport airspace surveillance, critical infrastructure facility protection, and urban security monitoring while remaining within cost and form factor parameters compatible with broad procurement and deployment. A detection range of 5 to 20 kilometers provides approximately 2 to 8 minutes of warning time against drones approaching at 15 to 20 meters per second cruise speed, which is sufficient for trained security teams to implement defensive protocols and activate countermeasure systems in the majority of threat scenarios. The market-leading drone detection radar systems from suppliers including Blighter, Echodyne, and Thales in this detection range category have accumulated extensive field deployment references that support their continued procurement dominance.

However, the long range (above 20 km) segment is projected to register the highest CAGR during the forecast period. Growing awareness of the range capabilities of military-grade and high-endurance commercial drones capable of flying missions at altitudes and ranges beyond the coverage of conventional medium-range detection systems is driving defense procurement agencies to specify long-range drone detection capabilities for the protection of high-value fixed installations, air defense command and control nodes, and strategic infrastructure that adversaries would prioritize for drone reconnaissance and attack. Extended detection range also provides the additional response time required for kinetic and non-kinetic defeat systems including laser weapons, directed energy, and interceptor drone systems to engage drone threats before they reach protected airspace or delivery range of their payload.

By Platform: In 2026, Fixed/Stationary Systems to Hold the Largest Share

Based on platform, the global drone detection radar systems market is segmented into fixed/stationary systems, mobile/vehicle-mounted systems, portable systems, and airborne systems. In 2026, the fixed/stationary systems segment is expected to account for the largest share of the global drone detection radar systems market. Fixed drone detection radar installations at military bases, airports, nuclear power plants, government facilities, and critical infrastructure sites represent the largest by-value deployment category, as permanent fixed-site installations can accommodate the larger antenna apertures, higher power outputs, and infrastructure-connected processing systems that deliver the highest detection performance and most comprehensive coverage geometry for protecting fixed high-value assets. The permanence of fixed installations supports the integration of drone detection radar into broader security system architectures including perimeter intrusion detection, access control, video surveillance, and command and control center operations in ways that mobile and portable systems cannot replicate. Airport drone detection radar installations mandated by aviation regulators across Europe, North America, and Asia-Pacific represent a large and growing fixed-site procurement category that is driving sustained fixed system market revenue.

However, the mobile/vehicle-mounted systems segment is projected to register the highest CAGR during the forecast period. The operational requirement to provide organic counter-drone awareness to mobile military ground forces, convoy protection units, and rapidly redeploying security elements is generating strong and growing demand for vehicle-integrated drone detection radar that can operate while in transit and be rapidly deployed at new operating positions without infrastructure requirements. The Ukraine conflict has demonstrated with particular clarity the vulnerability of military ground forces to commercially available drone surveillance and one-way attack capabilities, and this demonstrated operational reality is driving urgent procurement of vehicle-integrated drone detection radar systems by NATO members and other defense establishments seeking to equip their maneuver forces with protective counter-drone awareness across the full range of operational scenarios.

By Application: In 2026, Military and Defense to Hold the Largest Share

Based on application, the global drone detection radar systems market is segmented into military and defense, homeland security, critical infrastructure protection, airports and aviation security, public events and urban security, and industrial facilities. In 2026, the military and defense segment is expected to account for the largest share of the global drone detection radar systems market. Military and defense procurement constitutes the dominant application segment, driven by the urgent operational priority that drone detection has achieved across all major military establishments following the demonstrated effectiveness of drone systems in contemporary conflicts. The scale of military procurement programs for drone detection radar substantially exceeds civil and commercial procurement by both unit count and system value, as military-specification systems deployed in operational conflict environments command premium pricing reflecting their advanced electronic protection, environmental ruggedization, and integration requirements. The United States military's comprehensive C-UAS program portfolio spanning all service branches, NATO allies' coordinated drone detection capability development programs, and the major defense modernization investments of countries including India, South Korea, Japan, and Australia collectively constitute a procurement base that established the military segment's dominant market position.

However, the critical infrastructure protection segment is projected to register the highest CAGR during the forecast period. The documented vulnerability of power generation facilities, oil and gas processing infrastructure, water treatment systems, telecommunications towers, and data centers to drone-borne surveillance, physical disruption, and cyberattack through proximity-enabled wireless access is driving rapidly growing investment in drone detection radar by critical infrastructure operators, government infrastructure protection agencies, and energy sector security organizations. The 2019 Abqaiq attack on Saudi Aramco's oil processing infrastructure, which temporarily disrupted approximately 5% of global oil supply, demonstrated the catastrophic economic impact of successful drone attacks on critical infrastructure and accelerated protective investment globally.

By End User: In 2026, Defense Forces to Hold the Largest Share

Based on end user, the global drone detection radar systems market is segmented into defense forces, law enforcement agencies, airport authorities, commercial enterprises, and government agencies. In 2026, the defense forces segment is expected to account for the largest share of the global drone detection radar systems market. Military and defense forces globally represent the largest procurement channel for drone detection radar systems by aggregate spending, as national defense establishments are investing in multi-system, multi-site drone detection radar deployments at military installations, forward operating bases, and operational theaters of a scale and value that exceeds any other end-user segment. Defense procurement programs for drone detection radar are characterized by long contract durations, large per-contract values including system procurement, installation, training, and multi-year maintenance and upgrade provisions, and stringent technical performance and security requirements that support premium pricing for systems meeting military specifications. The JCO's procurement of Raytheon Technologies' KuRFS radar systems, Northrop Grumman's Forward Area Air Defense Command and Control integration contracts, and European NATO member states' national C-UAS procurement programs represent the scale and value of defense procurement driving segment leadership.

However, the airport authorities segment is projected to register the highest CAGR during the forecast period. Regulatory requirements for drone detection systems at airports are being progressively implemented across major aviation markets, with the UK Civil Aviation Authority, European Union Aviation Safety Agency, and Federal Aviation Administration developing drone detection standards and requirements that will create mandatory procurement obligations for airport operators globally. The documented history of drone incursions causing flight suspensions at major international airports, including the December 2018 Gatwick Airport closure that disrupted over 1,000 flights and affected approximately 140,000 passengers, has created both the regulatory impetus for mandatory drone detection requirements and the airport operator motivation to invest proactively in detection systems that avoid the severe operational and reputational costs of unmanaged drone incursion events.

By Integration Type: In 2026, Multi-Sensor Integrated Systems to Hold the Largest Share

Based on integration type, the global drone detection radar systems market is segmented into standalone radar systems, multi-sensor integrated systems, and command and control integrated systems. In 2026, the multi-sensor integrated systems segment is expected to account for the largest share of the global drone detection radar systems market. Multi-sensor integrated systems that combine radar with RF, EO/IR, and acoustic sensor data in a fused detection and tracking architecture are the preferred procurement choice for the majority of sophisticated defense, security, and infrastructure protection customers, reflecting the widely recognized principle that no single sensor technology achieves the combination of detection range, all-weather operation, target classification accuracy, and false alarm performance required for reliable operational deployment. The market leadership of multi-sensor systems reflects the maturation of the drone detection market beyond its early phase where standalone radar was the primary available solution into a more sophisticated procurement environment where buyers specify integrated multi-sensor performance requirements and evaluate competing systems on the basis of their fusion architecture capability, data management platform, and operational software interface.

However, the command and control integrated systems segment is projected to register the highest CAGR during the forecast period. The integration of drone detection sensor data into broader command and control (C2) architectures that manage the complete counter-drone response cycle from detection through classification, threat assessment, engagement decision support, and countermeasure activation represents the most sophisticated and highest-value integration tier in the drone detection market. Defense procurement programs are increasingly specifying C2-integrated drone detection as a requirement, recognizing that detection data that cannot be rapidly and reliably communicated to decision-makers and defeat system operators provides incomplete operational value. The development of open architecture C2 integration standards for counter-drone systems by the U.S. DoD's JCO and NATO's C-UAS working groups is enabling more efficient C2 integration of detection systems from multiple suppliers and driving the adoption of C2-integrated architectures across both military and civil security applications.

Drone Detection Radar Systems Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global drone detection radar systems market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global drone detection radar systems market. North America's dominant market position reflects the United States' position as both the world's largest defense spender and the most advanced developer and deployer of counter-drone detection technologies. The U.S. Department of Defense's C-UAS priority investment programs, administered through the Joint Counter-Small Unmanned Aircraft Systems Office, encompass radar detection system procurement for hundreds of military installations across the continental United States and overseas deployments in Europe, the Pacific, and the Middle East. The U.S. homeland security procurement ecosystem for drone detection spans airport security, border protection, federal facility protection, and national special security events, adding substantial civil procurement volume to the dominant military program base. Canada's defense investment in drone detection capability under the NORAD modernization program, which is allocating over USD 4.9 billion to Arctic surveillance and detection infrastructure upgrades that include drone detection radar capability, represents a significant regional procurement addition to U.S. market leadership.

However, the Asia-Pacific drone detection radar systems market is expected to grow at the fastest CAGR during the forecast period. Asia-Pacific's rapid growth reflects the convergence of multiple demand drivers operating simultaneously across the region's largest defense markets. India's defense modernization investment, supported by the government's push for indigenous defense manufacturing under the 'Make in India' program and the substantial procurement budget of the Indian Army and Air Force for counter-drone capabilities along the Line of Actual Control with China and the Line of Control with Pakistan, is generating large and sustained procurement demand for drone detection radar systems. China's investment in counter-drone detection for its military and border security forces, while opaque in procurement detail, represents a major demand element within the Asia-Pacific market. South Korea's urgent operational requirement for counter-drone detection along the Demilitarized Zone, driven by documented North Korean balloon and drone incursions into South Korean airspace, is funding accelerated procurement of advanced detection systems. Japan's Self Defense Forces' investment in drone detection capability under the country's historic defense spending increase toward 2% of GDP is establishing a new and substantial procurement program in the region's third-largest defense market.

Europe represents the third-largest regional drone detection radar market and is experiencing rapid growth driven by the operational urgency demonstrated by the Russia-Ukraine conflict and its implications for NATO member state counter-drone capability requirements. The extensively documented operational effectiveness of drone systems in the Ukraine conflict, including both Russian and Ukrainian use of commercial and military drones for reconnaissance, fire correction, and precision attack missions, has created an urgent capability gap awareness among NATO members that is driving accelerated counter-drone procurement investment. Germany's Bundeswehr, the UK's Ministry of Defence, France's Armee de Terre, and Poland's rapidly expanding defense forces are all executing or planning drone detection radar procurement programs that collectively represent multi-billion-euro regional market demand. European defense industry participants including Hensoldt, Thales, Saab, and Leonardo are competing actively for this domestic procurement while also pursuing export opportunities across NATO partner and global security market customers.

The global drone detection radar systems market is moderately concentrated, with established defense electronics and radar system manufacturers including Raytheon Technologies, Thales, Saab, Northrop Grumman, and L3Harris Technologies leveraging their advanced radar development capabilities and defense procurement relationships to compete alongside focused counter-drone specialists including Blighter Surveillance Systems, Hensoldt, SRC, DeTect, and Echodyne Corp. that have built dedicated drone detection product lines and operational deployment track records. Competition is focused on detection performance against small and low-RCS drone targets, false alarm rate in operationally realistic clutter environments, multi-sensor integration architecture, C2 system interoperability, geographic coverage pattern optimization, and the breadth and quality of deployment-level support services including installation, operator training, and system maintenance.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' radar technology portfolios, customer deployment bases, geographic market presence, and key strategic developments. Some of the key players operating in the global drone detection radar systems market include Raytheon Technologies Corporation (U.S.), Thales Group (France), Saab AB (Sweden), Hensoldt AG (Germany), Blighter Surveillance Systems Ltd. (U.K.), Lockheed Martin Corporation (U.S.), Leonardo S.p.A. (Italy), Rheinmetall AG (Germany), Israel Aerospace Industries (Israel), Elbit Systems Ltd. (Israel), Northrop Grumman Corporation (U.S.), L3Harris Technologies, Inc. (U.S.), SRC, Inc. (U.S.), DeTect, Inc. (U.S.), and Echodyne Corp. (U.S.), among others.

The global drone detection radar systems market is expected to reach USD 8.9 billion by 2036 from an estimated USD 3.4 billion in 2026, at a CAGR of 10.1% during the forecast period 2026 to 2036.

In 2026, the active radar systems segment is expected to hold the largest share of the global drone detection radar systems market, driven by the all-weather, day-night, standalone detection performance, extensive field deployment track record, and broad supplier ecosystem that active radar technologies including AESA, pulse-Doppler, and FMCW systems provide across defense, homeland security, and civil airspace monitoring procurement programs.

The multi-static radar systems segment is expected to register the highest CAGR during the forecast period 2026 to 2036, driven by growing defense procurement interest in multi-static geometric diversity as a solution to the radar cross-section null limitation of monostatic radar systems when detecting small, maneuvering drone targets and swarm formations executing evasive flight profiles.

In 2026, the X-Band segment is expected to hold the largest share of the global drone detection radar systems market, reflecting X-Band radar's combination of favorable drone detection performance characteristics including micro-Doppler rotor signature resolution, all-weather transmission, and compact antenna form factor alongside a mature and cost-competitive supplier ecosystem that has established X-Band as the primary frequency band for purpose-designed drone detection radar products.

In 2026, the military and defense segment is expected to hold the largest share of the global drone detection radar systems market, driven by the urgent operational priority status of counter-drone detection capability across military establishments globally and the large-scale procurement programs of U.S. DoD, NATO member states, and major Asia-Pacific defense forces investing in drone detection radar at military installations and operational deployment configurations.

The growth of this market is primarily driven by the rapidly escalating threat environment created by the proliferation of commercially available drones capable of delivering surveillance, payload, and attack capabilities to a broad spectrum of malicious actors; increasing defense and homeland security spending on counter-drone capabilities in response to documented drone incidents at military, governmental, and infrastructure sites globally; the expanding regulatory requirement for drone detection at airports and in civil airspace management infrastructure; and the integration of AI signal processing and multi-sensor fusion that is dramatically expanding drone detection system performance and commercial addressability.

Key players are Raytheon Technologies Corporation (U.S.), Thales Group (France), Saab AB (Sweden), Hensoldt AG (Germany), Blighter Surveillance Systems Ltd. (U.K.), Lockheed Martin Corporation (U.S.), Leonardo S.p.A. (Italy), Rheinmetall AG (Germany), Israel Aerospace Industries (Israel), Elbit Systems Ltd. (Israel), Northrop Grumman Corporation (U.S.), L3Harris Technologies, Inc. (U.S.), SRC, Inc. (U.S.), DeTect, Inc. (U.S.), and Echodyne Corp. (U.S.), among others.

Asia-Pacific is expected to register the highest growth rate in the global drone detection radar systems market during the forecast period 2026 to 2036, driven by India's large-scale border security and defense modernization procurement, South Korea's urgent operational counter-drone requirements along the Demilitarized Zone, Japan's historic defense spending increase creating new drone detection procurement programs, and the rapid expansion of commercial drone airspace integration across Asia-Pacific economies requiring civil airspace surveillance infrastructure.

Published Date: Apr-2026

Published Date: Oct-2024

Published Date: Apr-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates