Resources

About Us

Space Logistics Market Size, Share & Trends Analysis by Service Type (Launch Logistics, In-Orbit Transportation), Orbit Type, Application, End User, and Vehicle Type - Global Opportunity Analysis & Industry Forecast (2026-2036)

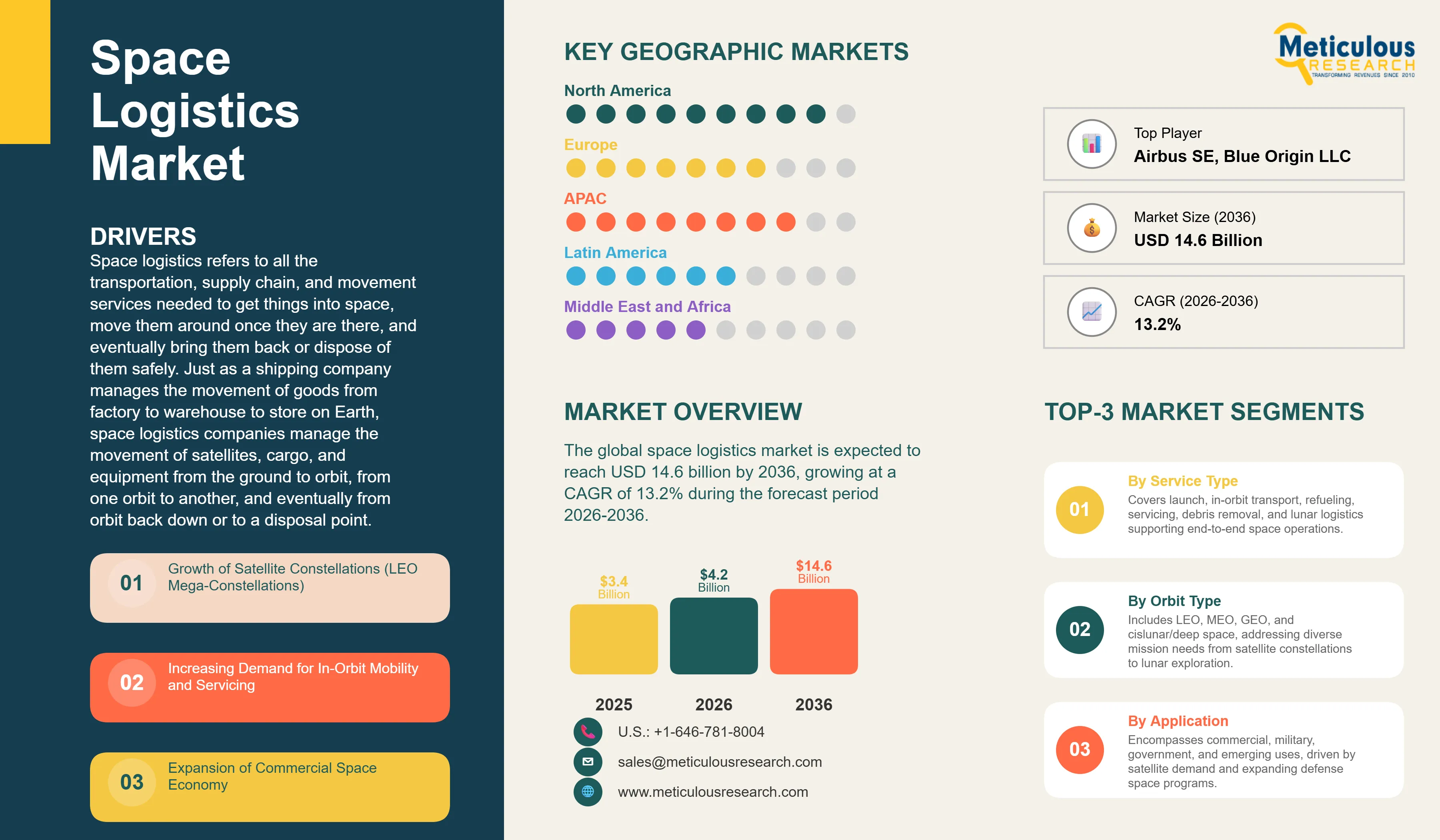

Report ID: MRAD - 1041916 Pages: 289 Apr-2026 Formats*: PDF Category: Aerospace and Defense Delivery: 24 to 72 Hours Download Free Sample ReportThe global space logistics market was valued at USD 3.4 billion in 2025. This market is expected to reach USD 14.6 billion by 2036 from an estimated USD 4.2 billion in 2026, growing at a CAGR of 13.2% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Space logistics refers to all the transportation, supply chain, and movement services needed to get things into space, move them around once they are there, and eventually bring them back or dispose of them safely. Just as a shipping company manages the movement of goods from factory to warehouse to store on Earth, space logistics companies manage the movement of satellites, cargo, and equipment from the ground to orbit, from one orbit to another, and eventually from orbit back down or to a disposal point. The market includes conventional launch services that carry payloads from Earth to orbit, orbital transfer vehicles and space tugs that move satellites to their final destinations after launch, refueling services that extend satellite operational lives, and the logistics of resupplying space stations and eventually supporting permanent infrastructure on the Moon and beyond.

The market is growing rapidly because the volume and complexity of space activity is growing much faster than the simple launch-and-forget model of the early space industry can support. A decade ago, most satellites were large, expensive, and designed to operate entirely independently once placed in orbit. Today, thousands of small and medium satellites are being deployed in large constellations that need deployment services, orbital optimization support, and eventually end-of-life management. The rapid cost reduction of launch services, led by SpaceX's reusable Falcon 9 and Falcon Heavy rockets and followed by Rocket Lab, Blue Origin, and others, has lowered the barrier to orbit and significantly increased the number of organizations that can afford to send hardware to space, creating a much larger customer base for space logistics services than existed previously.

Two major opportunities are shaping the next phase of market growth. Space tugs and orbital transfer vehicles that can collect satellites released to a standard orbit by a rideshare launch and deliver them to their specific operational destinations are filling a gap in the current space supply chain where satellites launched as rideshares often cannot reach their ideal operating orbit under their own power. Companies including D-Orbit, Momentus, Exolaunch, and Rocket Lab's Photon platform are all offering these last-mile delivery services for small satellites, and this segment is growing very rapidly. Looking further ahead, the development of permanent infrastructure in cislunar space and on the Moon through NASA's Artemis program and its commercial partners is creating an entirely new logistics market category centered on moving cargo between Earth orbit and the Moon, which will require new vehicles, refueling infrastructure, and logistics management services that do not yet exist at commercial scale.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 14.6 Billion |

|

Market Size in 2026 |

USD 4.2 Billion |

|

Market Size in 2025 |

USD 3.4 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 13.2% |

|

Dominating Service Type |

Launch Logistics Services |

|

Fastest Growing Service Type |

Space Infrastructure Logistics (Lunar) |

|

Dominating Orbit Type |

Low Earth Orbit (LEO) |

|

Fastest Growing Orbit Type |

Cislunar and Deep Space |

|

Dominating Application |

Commercial Applications |

|

Fastest Growing Application |

Military & Defense Applications |

|

Dominating End User |

Commercial Satellite Operators |

|

Fastest Growing End User |

Private Space Companies |

|

Dominating Vehicle Type |

Launch Vehicles |

|

Fastest Growing Vehicle Type |

Orbital Transfer Vehicles (OTVs) |

|

Dominating Operation Type |

Semi-Autonomous Operations |

|

Fastest Growing Operation Type |

Autonomous Operations |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Reusable Rockets Transforming the Economics of Space Logistics

The single most important trend reshaping the entire space logistics market is the commercial success of reusable launch vehicles, led by SpaceX's Falcon 9, which has demonstrated that recovering and relaunching rocket boosters can reduce the cost of reaching orbit dramatically compared with expendable rockets that are discarded after each use. SpaceX has now reflown individual Falcon 9 boosters more than 20 times, and the cost reduction compared with a new booster on every mission is very significant. This lower launch cost has already caused a fundamental shift in how satellite operators, governments, and emerging space businesses think about what is economically viable in space. Applications that were once too expensive to consider, including large satellite constellations with thousands of individual satellites, are now commercially practical because the cost of getting each satellite to orbit has fallen enough to make the business model work.

The reusable rocket trend is also driving competition across the launch industry. Rocket Lab's Neutron vehicle, Blue Origin's New Glenn, and several other reusable rockets in development are all targeting the same cost reduction model, which will further reduce launch prices and open up additional demand for space logistics services as more customers find that access to space fits within their budgets. The growing list of launch providers is also creating a more competitive and resilient space logistics supply chain, reducing the dependence on any single rocket for critical payloads that characterized the launch market for many years.

Last-Mile Satellite Delivery Emerging as a Major Commercial Service Category

One of the fastest-growing service categories in space logistics is what the industry calls last-mile delivery for satellites, which refers to the service of taking a satellite from the standard orbit where a rideshare launcher drops it off and delivering it to its specific operational destination. When many small satellites share a single rocket to reduce individual launch costs, the rocket typically delivers all of them to the same orbit, which may not be exactly right for each satellite's intended application. The satellite then needs to use its own propulsion to travel to its correct altitude and inclination, which consumes fuel that could otherwise extend its operational life and requires the satellite to carry a larger and more expensive propulsion system.

Space tug and orbital transfer vehicle services solve this problem by taking groups of satellites from the shared launch orbit and delivering each one to its precise destination, allowing the satellites themselves to be simpler and cheaper while still reaching their intended positions. D-Orbit has flown multiple commercial missions delivering satellites to their final orbits using its ION satellite carrier vehicle. Momentus is developing a microwave electrothermal thruster-powered transfer vehicle for similar missions. Rocket Lab's Photon kick stage has delivered NASA and commercial payloads to orbits ranging from low earth to cislunar space. This service category is growing rapidly as the rideshare launch market grows and the number of small satellite operators seeking affordable precision delivery services increases.

NASA Artemis and Commercial Lunar Programs Creating a New Logistics Frontier

The development of permanent human presence on and around the Moon through NASA's Artemis program and the associated Commercial Lunar Payload Services program is creating an entirely new and large space logistics market that will need to be served by commercial providers over the coming decade and beyond. NASA's CLPS program has already contracted multiple commercial lunar landing missions to deliver scientific payloads to the lunar surface, with companies including Intuitive Machines, Astrobotic, and Firefly Aerospace selected as providers. These initial missions represent the beginning of what NASA and space industry analysts project will grow into a substantial ongoing logistics market as lunar exploration transitions from one-off missions to regular cargo delivery supporting increasingly permanent infrastructure.

The logistics requirements for supporting a permanent lunar outpost are substantially more complex and higher-volume than the one-off delivery missions of the early Artemis era. Lunar Gateway, NASA's planned space station in lunar orbit that will serve as a staging point for lunar surface missions, will require regular resupply of crew provisions, equipment, and propellant from Earth. The eventual development of a permanent crewed lunar base will require the delivery of construction materials, life support equipment, scientific instruments, and regular consumable resupply on a scale that will need dedicated commercial logistics services. Sierra Space, Blue Origin, SpaceX's Starship, and several other commercial space companies are positioning themselves to provide these lunar logistics services, representing a significant and growing market opportunity over the forecast period.

Growth of Satellite Constellations (LEO Mega-Constellations)

The deployment of large satellite constellations in low earth orbit by SpaceX Starlink, Amazon Kuiper, OneWeb, and a growing number of other operators is the primary driver of the space logistics market, as each constellation represents hundreds to thousands of individual satellites that need to be launched, placed in the correct orbits, maintained in operation, and eventually replaced or decommissioned as they reach the end of their service lives. SpaceX has already launched over 6,000 Starlink satellites and has regulatory approval for up to 42,000, and Amazon's Kuiper constellation targets 3,236 satellites. Deploying, managing, and eventually disposing of these very large satellite populations requires a sophisticated and scalable logistics infrastructure, including rideshare launch coordination, orbital transfer services to optimize constellation geometry, satellite replacement logistics, and debris disposal services for retired satellites. The scale of the logistics requirement created by LEO mega-constellations alone is sufficient to sustain rapid market growth through the forecast period.

Rising Investments in Deep Space Exploration

NASA's Artemis program, SpaceX's Starship deep space ambitions, Blue Origin's cislunar transportation plans, and the national space programs of China, India, Japan, and the European Union are all investing heavily in the capability to conduct missions beyond low earth orbit, including to the Moon, Mars, and eventually beyond. These deep space ambitions require substantial investment in the logistics infrastructure needed to support them, including propellant depots in high earth orbit or at the lunar gateway that would allow deep space missions to refuel before proceeding beyond Earth's gravitational influence, cargo vehicles capable of the long-duration burns needed for cislunar and translunar trajectories, and the ground-based logistics management systems needed to plan and coordinate complex multi-leg space missions. The commercial contracts already awarded under NASA's CLPS program, the significant private investment in lunar transportation companies, and the growing number of national space agency budgets directed toward deep space exploration collectively represent a large and growing demand source for space logistics services that will expand substantially through the forecast period.

Development of Space Tugs and Orbital Transfer Vehicles (OTVs)

Orbital transfer vehicles and space tugs that can move satellites, cargo, and eventually crew between different orbital destinations represent the single largest new commercial service opportunity in the space logistics market over the forecast period. Currently, most satellites are delivered to a single orbit by their launch vehicle and must use their own propulsion to travel to their final operational position, which is inefficient and limits how precisely and how cost-effectively satellites can be positioned. A commercial OTV service that picks up satellites from a standard rideshare delivery orbit and delivers them precisely to their individual operational destinations would allow satellite operators to buy simpler and cheaper satellites while still achieving precise orbital positioning, and would enable much more flexible and responsive satellite constellation management than is possible with current approaches. Multiple companies including D-Orbit, Momentus, Exolaunch, and Rocket Lab are already offering early versions of this service, and the market is expected to grow significantly as more satellite operators recognize the value of precision orbital delivery and as the capability and reliability of OTV services improves.

Growth in Space Stations and Lunar Logistics

The development of commercial space stations and the logistics requirements of NASA's Artemis lunar program are creating a large and growing market for cargo delivery, supply chain management, and transportation services beyond low earth orbit. The International Space Station currently receives regular cargo deliveries from SpaceX's Dragon and Northrop Grumman's Cygnus spacecraft under NASA contracts, and the commercial space station programs of Axiom Space, Blue Origin, and Sierra Space that are planned to replace the ISS will need similar ongoing cargo logistics services. The lunar logistics market is even larger in its long-term potential, as NASA's Commercial Lunar Payload Services program, the lunar gateway station, and eventually a permanent lunar surface presence will require regular and substantial cargo delivery services from commercial providers. For space logistics companies, securing early contracts in the lunar logistics market while it is still developing offers the opportunity to establish customer relationships and operational experience that will be very valuable as the market grows into one of the largest commercial space service categories of the 2030s.

By Service Type: In 2026, Launch Logistics Services to Dominate

Based on service type, the global space logistics market is segmented into launch logistics services, in-orbit transportation services, refueling services, in-orbit servicing and maintenance, active debris removal, and space infrastructure logistics. In 2026, the launch logistics services segment is expected to account for the largest share of the global space logistics market. Launch logistics encompasses the full range of services surrounding a rocket launch, including payload integration and preparation, launch scheduling and coordination, rideshare management for multiple payloads on a single rocket, and launch campaign management. The large number of commercial satellite launches driven by LEO constellation deployment programs makes this the highest-volume and highest-revenue service category in the current market. SpaceX's Falcon 9 and Falcon Heavy, Rocket Lab's Electron, and the growing fleet of other commercial launch vehicles are all driving this market.

However, the space infrastructure logistics segment, encompassing space station resupply, lunar logistics, and deep space cargo delivery, is projected to register the highest CAGR during the forecast period. The combination of ongoing ISS resupply missions, the transition to commercial space station resupply contracts as the ISS era ends, and the rapidly developing lunar logistics market driven by NASA's Artemis program and commercial lunar activities will make this the fastest-growing service category as new destinations and more permanent space infrastructure create sustained logistics demand beyond low earth orbit.

By Orbit Type: In 2026, LEO to Hold the Largest Share

Based on orbit type, the global space logistics market is segmented into low earth orbit, medium earth orbit, geostationary orbit, and cislunar and deep space. In 2026, the LEO segment is expected to account for the largest share of the global space logistics market. Low earth orbit is where the vast majority of new satellite deployments are concentrated, driven by the mega-constellation programs of SpaceX, Amazon, OneWeb, and others. The combination of very high launch volumes to LEO and the growing need for in-orbit transportation, orbital optimization, and debris management services in the increasingly crowded LEO environment makes this the current dominant revenue category for space logistics providers.

However, the cislunar and deep space segment is projected to register the highest CAGR during the forecast period. The development of lunar exploration infrastructure under NASA's Artemis program and the associated commercial lunar services market is creating a new and growing logistics demand category that did not generate significant commercial revenue before 2020. As lunar missions become more frequent and lunar infrastructure becomes more permanent, the logistics market in cislunar space is expected to grow from a very small base to a significant commercial market segment over the forecast period.

By Application: In 2026, Commercial Applications to Hold the Largest Share

Based on application, the global space logistics market is segmented into commercial applications, military and defense applications, government and civil applications, and emerging applications. In 2026, the commercial applications segment is expected to account for the largest share of the global space logistics market. Commercial satellite constellation deployment, broadband service delivery, and earth observation missions collectively represent the largest volume of space logistics activity globally, driven by the extraordinary scale of LEO constellation deployment programs and the growing commercial earth observation market. Commercial satellite operators are the largest and most active buyers of launch logistics and orbital transfer services, and this commercial demand base underpins the market's current revenue leadership in the commercial applications segment.

However, the military and defense applications segment is projected to register the highest CAGR during the forecast period. The U.S. Space Force's growing investment in commercial launch services, satellite repositioning, and space domain awareness programs, combined with allied military space programs in Europe, Japan, and Australia, is creating rapidly growing government defense demand for space logistics services. The increasing strategic importance of space assets to military operations and the recognition that resilient space architecture requires the ability to rapidly deploy, reposition, and if necessary replace satellites are driving defense organizations to invest more heavily in the commercial space logistics capabilities that support these requirements.

By End User: In 2026, Commercial Satellite Operators to Hold the Largest Share

Based on end user, the global space logistics market is segmented into commercial satellite operators, defense organizations, space agencies, and private space companies. In 2026, the commercial satellite operators segment is expected to account for the largest share of the global space logistics market. Commercial satellite operators, including the large constellation operators such as SpaceX Starlink and Amazon Kuiper as well as established GEO satellite fleet operators such as Intelsat, SES, and Eutelsat, represent the largest category of paying customers for space logistics services. The enormous scale of LEO constellation deployment programs means that commercial satellite operators generate the majority of launch logistics demand globally, and as these constellations mature and require ongoing management, refueling, and debris disposal services, their demand for in-orbit logistics services will grow substantially.

However, the private space companies segment is projected to register the highest CAGR during the forecast period. The rapid emergence of a new generation of commercial space companies pursuing activities including commercial space stations, lunar exploration, in-orbit manufacturing, and space tourism is creating a fast-growing new customer category for space logistics services that is very different from traditional satellite operators. These new space economy companies need transportation, supply chain management, and logistics support for activities that are significantly more complex and varied than conventional satellite deployment, representing a high-growth and high-value segment for space logistics providers with the technical capability to serve diverse customer needs.

By Vehicle Type: In 2026, Launch Vehicles to Hold the Largest Share

Based on vehicle type, the global space logistics market is segmented into launch vehicles, orbital transfer vehicles, space tugs, refueling vehicles, and servicing spacecraft. In 2026, the launch vehicles segment is expected to account for the largest share of the global space logistics market. Launch vehicles, from SpaceX's Falcon 9 to Rocket Lab's Electron and the growing fleet of emerging rocket providers, generate the largest revenue within the space logistics market by value, as each launch mission represents a significant commercial transaction covering rocket, integration, and associated services. The high and growing demand for commercial launches driven by LEO constellation deployment ensures that launch vehicles remain the dominant revenue category.

However, the orbital transfer vehicles segment is projected to register the highest CAGR during the forecast period. OTVs are one of the newest commercially available space logistics vehicle categories, with D-Orbit, Momentus, and Rocket Lab's Photon among the first commercial providers. As the market for in-orbit satellite delivery, constellation management, and eventually cislunar transportation grows, OTVs will be among the fastest-growing hardware categories in the space logistics market, transitioning from early commercial demonstrations to high-volume operational services.

By Operation Type: In 2026, Semi-Autonomous Operations to Hold the Largest Share

Based on operation type, the global space logistics market is segmented into autonomous operations, semi-autonomous operations, and teleoperated systems. In 2026, the semi-autonomous operations segment is expected to account for the largest share of the global space logistics market. Most current space logistics vehicles operate in a semi-autonomous mode where routine navigation and orbital maneuvers are handled automatically by onboard computers while ground controllers monitor the mission and intervene for critical decisions such as rendezvous approaches, docking, and anomaly resolution. This balance of automation and human oversight is appropriate for the current stage of the technology and the regulatory environment, where human oversight of operations near other space assets is expected by regulatory bodies and satellite operators alike.

However, the autonomous operations segment is projected to register the highest CAGR during the forecast period. As the volume of space logistics missions grows and the operational experience with autonomous space vehicle operations increases, full autonomy will become both technically feasible and commercially necessary. Ground control of every maneuver by every vehicle in a large fleet of space tugs or OTVs would require enormous staffing and create latency issues that reduce operational efficiency. Fully autonomous operations, validated through demonstrated reliability in semi-autonomous missions, will be essential for scaling commercial space logistics to the volumes that the growing space economy will require.

Space Logistics Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global space logistics market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global space logistics market. The United States dominates this market through a combination of the world's most active commercial launch industry anchored by SpaceX's extraordinary launch rate of over 90 missions per year, a large and diverse group of emerging space logistics companies including D-Orbit, Momentus, Orbit Fab, Firefly Aerospace, and Sierra Space, and the very large NASA and U.S. Space Force procurement programs that provide both direct revenue and technology development funding that stimulates commercial market growth. SpaceX alone accounts for a very significant share of global launch activity by both number of missions and total mass delivered to orbit, making the U.S. the unambiguous leader in the global space logistics market. Rocket Lab's New Zealand launch facility and U.S. headquarters, Blue Origin's New Glenn and lunar logistics programs, and the growing commercial space station ambitions of Axiom Space and Sierra Space collectively make North America the world's most active and commercially advanced space logistics market. Canada's contributions through its robotics expertise and space agency partnerships add further depth to the North American market.

However, the Asia-Pacific space logistics market is expected to grow at the fastest CAGR during the forecast period. China has become a major space power with a large and growing commercial launch industry including Long March rocket variants and the emerging commercial launch vehicles of companies including LandSpace, iSpace, and Galactic Energy, alongside China's own satellite constellation programs and its ambitious national plans for a permanent lunar presence. India's space sector is undergoing a significant transformation as private commercial space companies enter the launch and logistics market following ISRO's commercial arm NewSpace India Limited demonstrating the commercial potential of the Indian launch industry. Japan's H3 rocket program, South Korea's Nuri rocket, and Australia's growing commercial space sector are all contributing to the Asia-Pacific market's growth. The region's large satellite operator market, particularly in Japan, South Korea, and the growing Southeast Asian satellite communications sector, provides strong demand for space logistics services alongside the expanding supply-side capabilities of regional launch and space service providers.

Europe is a significant space logistics market anchored by the Ariane launch family and the European Space Agency's substantial budget for launch services, space exploration, and commercial space development. ESA's commercial contracts for lunar payload delivery, debris removal demonstrations, and orbital transfer services represent important demand for commercial space logistics providers. Airbus Defence and Space, Thales Alenia Space, and Avio provide significant space logistics capabilities including the Ariane 6 rocket, upper stages, and satellite integration services. Luxembourg's SES and other European satellite operators are among the most active commercial customers for launch and in-orbit logistics services, and the European space investor community has backed several important space logistics startups including ClearSpace and others that are developing services for the European and global market.

The space logistics market spans companies from SpaceX, which is simultaneously the world's dominant launch provider and a major satellite constellation operator, through specialized orbital transfer and in-orbit services companies, to the established aerospace primes that provide satellite integration, cargo vehicle, and space station logistics services. Competition is based on launch cost and reliability, in-orbit services capability, vehicle reusability and resulting economics, customer relationships, regulatory standing to operate in proximity to other satellites, and the ability to serve the full range of a customer's space logistics needs.

SpaceX dominates the global launch logistics market through the Falcon 9 and Falcon Heavy reusable rockets, which have set new standards for cost, reliability, and launch cadence, and is developing the fully reusable Starship system targeting even lower costs for large payloads and cislunar missions. Rocket Lab has established itself as the leading provider of small satellite launch services through the Electron rocket and is developing the larger Neutron rocket and has demonstrated cislunar delivery capability through its Photon upper stage. Northrop Grumman provides cargo resupply to the International Space Station through its Cygnus spacecraft, a proven and contracted space logistics service. D-Orbit has flown multiple commercial in-orbit delivery missions using its ION satellite carrier, becoming one of the earliest companies to operate a commercial orbital transfer vehicle service. Momentus is developing the Vigoride orbital transfer vehicle for in-space transportation. Firefly Aerospace offers small to medium launch services and has been contracted for a CLPS lunar delivery mission.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' service portfolios, mission track records, customer relationships, geographic presence, and recent strategic developments. Some of the key players operating in the global space logistics market include SpaceX (U.S.), Rocket Lab USA Inc. (U.S./New Zealand), Northrop Grumman Corporation (U.S.), Airbus SE (Netherlands), Astroscale Holdings Inc. (Japan/UK), Maxar Technologies Inc. (U.S.), Thales Alenia Space (France/Italy), Orbit Fab Inc. (U.S.), D-Orbit S.p.A. (Italy), Momentus Inc. (U.S.), Redwire Corporation (U.S.), Firefly Aerospace Inc. (U.S.), Blue Origin LLC (U.S.), Sierra Space Corporation (U.S.), and Relativity Space Inc. (U.S.), among others.

The global space logistics market is expected to reach USD 14.6 billion by 2036 from an estimated USD 4.2 billion in 2026, at a CAGR of 13.2% during the forecast period 2026-2036.

In 2026, the launch logistics services segment is expected to hold the largest share of the global space logistics market, driven by the very high volume of commercial satellite launches for LEO mega-constellation deployment programs and the large revenue per mission associated with commercial launch services.

The space infrastructure logistics segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the rapidly developing lunar logistics market through NASA's Artemis program, growing commercial lunar missions, and the transition to commercial space station resupply services as the ISS era ends.

In 2026, the LEO segment is expected to hold the largest share of the global space logistics market, reflecting the concentration of new satellite deployment activity in low earth orbit driven by broadband constellation programs and earth observation missions.

In 2026, the commercial applications segment is expected to hold the largest share of the global space logistics market, driven by commercial satellite constellation deployment and fleet management representing the largest volume of space logistics activity globally.

The market is primarily driven by the rapid expansion of LEO satellite mega-constellations creating very large launch logistics and in-orbit transportation demand, and by the development of NASA's Artemis lunar program and the associated commercial lunar services market opening a new and growing logistics frontier beyond low earth orbit that will require dedicated commercial logistics services.

Key players are SpaceX (U.S.), Rocket Lab USA Inc. (U.S./New Zealand), Northrop Grumman Corporation (U.S.), Airbus SE (Netherlands), Astroscale Holdings Inc. (Japan/UK), Maxar Technologies Inc. (U.S.), Thales Alenia Space (France/Italy), Orbit Fab Inc. (U.S.), D-Orbit S.p.A. (Italy), Momentus Inc. (U.S.), Redwire Corporation (U.S.), Firefly Aerospace Inc. (U.S.), Blue Origin LLC (U.S.), Sierra Space Corporation (U.S.), and Relativity Space Inc. (U.S.), among others.

Asia-Pacific is expected to register the highest growth rate in the global space logistics market during the forecast period 2026-2036, driven by China's rapidly expanding commercial launch industry and satellite programs, India's commercialization of its space sector, and the growing space ambitions of Japan, South Korea, and Australia.

Published Date: Apr-2026

Published Date: Jul-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates