Resources

About Us

Advanced Avionics Systems Market Size, Share & Trends Analysis by System Type, Platform, Fit Type, Architecture Type (Federated, IMA), Application, End User, and Technology - Global Opportunity Analysis & Industry Forecast (2026-2036)

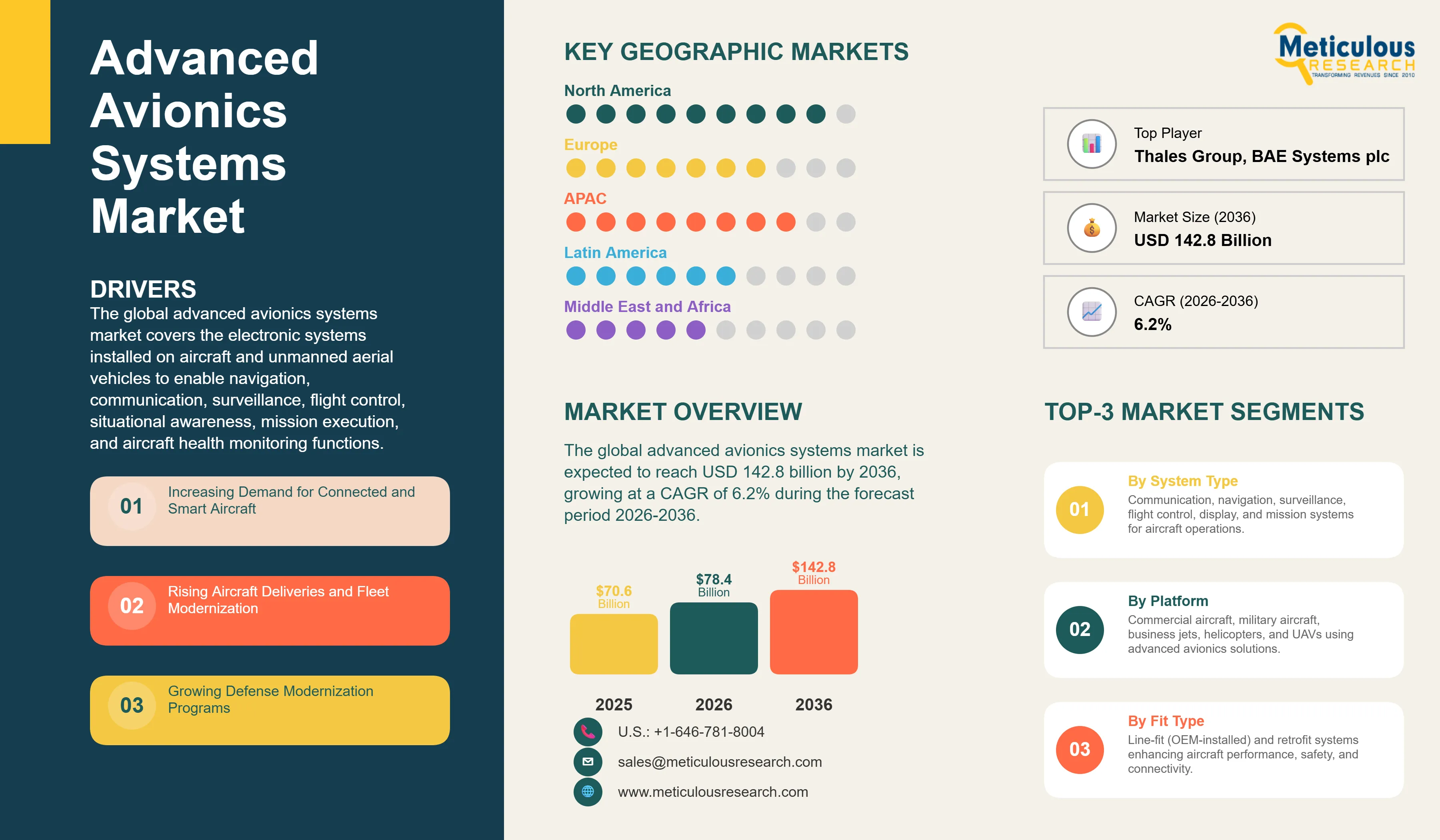

Report ID: MRAD - 1041912 Pages: 295 Apr-2026 Formats*: PDF Category: Aerospace and Defense Delivery: 24 to 72 Hours Download Free Sample ReportThe global advanced avionics systems market was valued at USD 70.6 billion in 2025. This market is expected to reach USD 142.8 billion by 2036 from an estimated USD 78.4 billion in 2026, growing at a CAGR of 6.2% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global advanced avionics systems market covers the electronic systems installed on aircraft and unmanned aerial vehicles to enable navigation, communication, surveillance, flight control, situational awareness, mission execution, and aircraft health monitoring functions. This encompasses communication systems including SATCOM, VHF and HF radio, and digital data link platforms; navigation systems including GPS and GNSS receivers, inertial navigation systems, and flight management computers; surveillance systems including weather radar, ADS-B transponders, and TCAS collision avoidance; flight control systems including fly-by-wire and autopilot platforms; cockpit display systems including primary flight displays, multi-function displays, and head-up displays; and the mission and tactical systems, health monitoring platforms, and integrated modular avionics architectures that form the digital backbone of modern aircraft across commercial, military, business aviation, and unmanned system applications.

The growth of the global advanced avionics systems market is primarily driven by the strong recovery and expansion of commercial aircraft deliveries following the COVID-19 pandemic disruption, with Boeing and Airbus collectively delivering over 1,200 commercial aircraft annually at peak rates and carrying large order backlogs that translate into sustained avionics line-fit procurement demand extending well through the forecast period. The aviation industry's progressive digital transformation toward connected aircraft architectures that enable real-time data exchange between the aircraft and ground operations, maintenance, and air traffic management systems is driving avionics investment in SATCOM broadband connectivity, electronic flight bag integration, ADS-B systems, and the data link infrastructure that enables performance-based navigation and digital air traffic management operations.

Two significant opportunities are shaping the market's long-term trajectory. The rapid growth of the unmanned aerial vehicle market across both commercial and military applications is creating a large and fast-growing new avionics procurement channel that requires purpose-designed avionics platforms optimized for the size, weight, power, and cost constraints of unmanned systems while providing the navigation, communication, and sense-and-avoid capabilities required for safe urban and beyond-visual-line-of-sight operations. The very large global installed base of aging aircraft requiring avionics retrofits to comply with ADS-B mandate implementation programs, Performance-Based Navigation requirements, and the NextGen and SESAR air traffic management modernization programs represents a large and addressable near-term aftermarket revenue opportunity for avionics suppliers with FAA and EASA-certified retrofit product lines.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 142.8 Billion |

|

Market Size in 2026 |

USD 78.4 Billion |

|

Market Size in 2025 |

USD 70.6 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 6.2% |

|

Dominating System Type |

Communication Systems |

|

Fastest Growing System Type |

Health Monitoring Systems |

|

Dominating Platform |

Commercial Aircraft |

|

Fastest Growing Platform |

Unmanned Aerial Vehicles (UAVs) |

|

Dominating Fit Type |

Line-Fit (OEM Installation) |

|

Fastest Growing Fit Type |

Retrofit/Aftermarket |

|

Dominating Architecture Type |

Integrated Modular Avionics (IMA) |

|

Fastest Growing Architecture Type |

Software-Defined Avionics |

|

Dominating Application |

Flight Operations and Navigation |

|

Fastest Growing Application |

Aircraft Health Monitoring |

|

Dominating End User |

Commercial Aviation Operators |

|

Fastest Growing End User |

UAV Operators |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Connected Aircraft and Real-Time Data Integration Transforming Avionics

The progressive transformation of commercial and business aircraft from isolated airborne systems to network-connected nodes in integrated aviation data ecosystems is driving significant avionics investment across SATCOM broadband communication, electronic flight bag and connected cockpit applications, aircraft health management data streaming, and the cybersecurity infrastructure required to protect connected aircraft systems from the vulnerabilities that internet connectivity introduces. The connected aircraft concept, which enables airlines to receive real-time aircraft health and performance data from sensors across the airframe and engines during flight, communicate updated weather, routing, and operational information to flight crews through digital datalink, and manage cabin connectivity services for passengers, is generating substantial avionics system procurement for SATCOM high-speed data terminals, avionics networking gateways, and aircraft data management platforms at both line-fit and retrofit customer demand levels.

The major commercial aircraft SATCOM market expansion, driven by airlines' adoption of Ku-band and Ka-band satellite broadband for both passenger connectivity and operational data applications, is generating large avionics procurement programs at both Boeing and Airbus new aircraft delivery programs and through retrofit installation at existing aircraft operators. Panasonic Avionics, Thales InFlyt Experience, Collins Aerospace's Satellite Communications division, and Inmarsat's aviation network service represent the primary commercial beneficiaries of this trend. The emerging integration of ground-based 5G aircraft connectivity for gate and terminal area high-bandwidth data exchange represents an additional avionics connectivity investment driver that will supplement SATCOM services for high-data-volume aircraft health management and operational data transfer applications as 5G aeronautical coverage expands at major airports.

Autonomous and AI-Augmented Avionics Advancing Toward Commercial Deployment

The progressive advancement of autonomous flight system technology and AI-augmented avionics capabilities from research and early development programs toward initial commercial and military deployment is creating a significant market opportunity within the advanced avionics segment for suppliers with demonstrated autonomous flight and AI-based decision support capabilities validated to aviation certification standards. AI-based flight management system enhancements that optimize routing and fuel consumption through real-time weather data integration, provide intelligent alerting and anomaly detection capabilities based on aircraft sensor data pattern analysis, and support crew decision-making in degraded visibility and unusual flight situation scenarios are being incorporated into next-generation flight management system products by Honeywell, Collins Aerospace, and Thales.

The autonomous aviation market, encompassing both fully autonomous unmanned aircraft and single-pilot operations technology for commercial aviation that reduces crew requirements on short-haul routes, represents a multi-year avionics development and certification investment program that is generating growing R&D spending across the avionics industry. The FAA's development of certification standards for autonomous flight systems under its Aviation Rulemaking Committee programs, EASA's autonomous and remotely piloted aircraft regulatory development, and the substantial venture and strategic capital being invested in autonomous aviation startups including Xwing, Reliable Robotics, and Merlin Labs are collectively advancing the certification and commercial timeline for autonomous and single-pilot commercial aviation operations that will require new avionics architectures and capability certifications from established avionics suppliers.

Defense Avionics Modernization Driving High-Value Upgrade Cycles

The large-scale military aircraft avionics modernization programs being executed across NATO, the Indo-Pacific, and the Middle East are generating very large avionics upgrade and replacement procurement programs as Cold War-era cockpit and mission systems are replaced with modern digital architectures, glass cockpit displays, advanced mission computers, and integrated modular avionics platforms that support the multi-domain operations and network-centric warfare requirements of contemporary military aviation. The U.S. Air Force's F-15EX Eagle II procurement including advanced APG-82 AESA radar and digital flight deck, the F-16 Active Electronically Scanned Array radar upgrade program for the large global F-16 fleet, the E-2D Advanced Hawkeye's ADS-18 radar, and the Multiple Integrated Laser Engagement System upgrade programs collectively represent multi-billion-dollar avionics procurement programs within the U.S. defense aviation market alone.

European NATO member state defense budget increases following Russia's 2022 invasion of Ukraine are accelerating military aircraft avionics modernization programs that had been deferred during the post-Cold War defense drawdown. The Eurofighter Typhoon Quadriga and Tranche 4 avionics upgrade programs, the French Rafale F4 standard avionics enhancement, the Swedish Gripen E/F's advanced sensor and communications suite, and the Polish and Romanian F-35A deliveries requiring avionics integration and support infrastructure represent the primary European military avionics procurement programs through the forecast period. In Asia-Pacific, Japan's F-35 and F-15J upgrade programs, South Korea's KF-21 Boramae domestic fighter development, India's Tejas Mk2 and AMCA programs, and Australia's F-35 fleet expansion are collectively generating large Asian military avionics procurement demand.

Increasing Demand for Connected and Smart Aircraft

The aviation industry's broad adoption of connected aircraft architectures that leverage satellite and terrestrial broadband communications to integrate aircraft with ground-based airline operations centers, maintenance facilities, and air traffic management systems in real time is the primary demand driver generating avionics system investment growth across both commercial line-fit and retrofit market segments. Airlines are increasingly requiring SATCOM broadband data connectivity on their aircraft fleets to enable predictive maintenance programs that use real-time aircraft sensor data streamed during flight to detect engine, system, and structural anomalies before they cause in-service failures, reducing unplanned maintenance events and improving aircraft dispatch reliability. The FAA and EASA mandates for ADS-B Out equipage that were fully implemented by 2020 in the U.S. and 2023 in Europe required avionics upgrades on thousands of commercial and general aviation aircraft, and the follow-on SESAR and NextGen programs are generating further avionics investment requirements for Performance-Based Navigation, datalink weather and routing services, and digital ATIS subscription terminals that collectively represent a sustained avionics modernization investment cycle.

Rising Aircraft Deliveries and Fleet Modernization

The strong recovery and expansion of commercial aircraft production following the COVID-19 pandemic's severe disruption to the aviation industry is generating sustained and growing line-fit avionics procurement demand as Airbus and Boeing execute their large order backlogs extending into the early 2030s at production rates that are approaching and targeting historic peaks. Airbus's A320neo Family and A350 program deliveries, Boeing's 737 MAX return to service and delivery acceleration, and the emerging widebody deliveries of Airbus A330neo and Boeing 787 and 777X programs collectively generate very large annual avionics system procurement from Honeywell, Collins Aerospace, Thales, Garmin, and Safran as launch suppliers for these platforms. The simultaneous retirement of older Boeing 747, 737 Classic, and Airbus A320ceo and A330ceo aircraft creates both demand for new aircraft avionics through replacement aircraft orders and retrofit avionics demand as operators invest in extending the service life of retained older aircraft through avionics modernization programs that improve operational capability and compliance with mandate requirements.

Growth in Electric and Autonomous Aircraft

The commercial development of electric aircraft, eVTOL urban air mobility platforms, and advancing autonomous flight systems is creating a new and significant avionics market opportunity for suppliers capable of developing the novel avionics architectures and certifications required by electric and autonomous aircraft that differ fundamentally from conventional aircraft avionics in their power system management requirements, autonomous flight control software, sense-and-avoid system needs, and the human-machine interface requirements of single-pilot or no-pilot operations concepts. The eVTOL market, with Joby Aviation, Archer Aviation, Vertical Aerospace, and multiple other developers advancing toward FAA and EASA type certification, requires purpose-designed avionics suites that integrate electric powertrain management, distributed propulsion control, fly-by-wire systems adapted for multi-rotor configurations, and urban airspace connectivity capabilities that current-generation commercial aviation avionics products do not address. Honeywell, Collins Aerospace, and Garmin have all announced dedicated urban air mobility and electric aircraft avionics development programs targeting the eVTOL certification and production ramp as their primary near-term advanced avionics growth market, representing the emergence of a new avionics product category with high growth potential through the forecast period.

Increasing Demand for Retrofit and Upgrades

The very large global installed base of commercial, business, and general aviation aircraft requiring avionics retrofit upgrades to comply with regulatory mandates, improve operational efficiency through advanced navigation and communications capabilities, and extend service life economically represents a large and commercially accessible near-term growth opportunity for avionics suppliers with certified retrofit product lines and established installation and support networks. The FAA's Performance-Based Navigation mandate implementation requiring RNAV and RNP capability on commercial aircraft operating in U.S. controlled airspace, the European Union's Single European Sky ATM Research program avionics requirements, the 8.33 kHz channel spacing mandate for European VHF communications, and the NextGen ADS-B In implementation programs all create defined and time-bounded retrofit equipment procurement requirements across large commercial aircraft populations. Business aviation represents a particularly active retrofit market, with the large fleet of older Cessna Citations, Bombardier Challengers, and Gulfstream aircraft representing avionics upgrade candidates for modern glass cockpit retrofits, SATCOM installations, and advanced navigation system upgrades that improve operational capability and residual aircraft values.

By System Type: In 2026, Communication Systems to Dominate

Based on system type, the global advanced avionics systems market is segmented into communication systems, navigation systems, surveillance systems, flight control systems, display systems, mission and tactical systems, and health monitoring systems. In 2026, the communication systems segment is expected to account for the largest share of the global advanced avionics systems market. The large share of this segment is attributed to communication systems representing the broadest-installed and highest-procurement-volume avionics category across commercial, military, and business aviation platforms, encompassing SATCOM terminals, VHF and HF radio transceivers, and digital datalink systems that are installed on virtually every commercial and military aircraft and that are generating significant upgrade procurement driven by SATCOM broadband adoption for passenger connectivity and operational data applications, datalink communication mandates, and the progressive transition from analog to digital radio communication across global airspace.

However, the health monitoring systems segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to airlines' accelerating adoption of aircraft health management and predictive maintenance programs that use real-time sensor data streaming from structural, engine, and systems health monitoring avionics to detect anomalies and predict maintenance requirements before failure, reducing unplanned maintenance events and improving aircraft operational availability. The expanding regulatory and OEM emphasis on aircraft health monitoring data as a tool for improving aviation safety and reducing maintenance costs is driving both new aircraft installation and retrofit investment in health monitoring avionics across the global commercial fleet.

By Platform: In 2026, Commercial Aircraft to Hold the Largest Share

Based on platform, the global advanced avionics systems market is segmented into commercial aircraft, military aircraft, business jets, helicopters, and unmanned aerial vehicles. In 2026, the commercial aircraft segment is expected to account for the largest share of the global advanced avionics systems market. Commercial aircraft represent the highest aggregate avionics procurement volume category globally, driven by the large annual production rates at Airbus and Boeing generating substantial line-fit avionics orders, the mandatory retrofit requirements of regulatory mandates affecting the large global commercial fleet of over 25,000 active aircraft, and the high per-aircraft avionics content of modern narrowbody and widebody aircraft platforms that each carry multiple avionics system categories representing millions of dollars in avionics equipment value per aircraft.

However, the UAV segment is projected to register the highest CAGR during the forecast period. This growth is driven by the extraordinary expansion of military unmanned system procurement across all major defense establishments for intelligence, surveillance, and reconnaissance and strike missions, the rapid development of commercial UAV applications in logistics, inspection, agriculture, and mapping that require FAA and EASA-certified avionics for beyond-visual-line-of-sight operations, and the emerging urban air mobility market creating demand for eVTOL avionics platforms as these systems advance toward commercial certification.

By Fit Type: In 2026, Line-Fit to Hold the Largest Share

Based on fit type, the global advanced avionics systems market is segmented into line-fit (OEM installation) and retrofit/aftermarket. In 2026, the line-fit segment is expected to account for the largest share of the global advanced avionics systems market. Line-fit avionics installed at aircraft manufacturing facilities through long-term launch supplier agreements between Boeing, Airbus, and military aircraft OEMs and avionics suppliers represent the highest aggregate revenue category, as new aircraft deliveries generate multi-year contracted avionics procurement programs at defined rates and prices that provide revenue visibility and high per-aircraft avionics content. The large Boeing and Airbus commercial delivery backlogs extending into the early 2030s ensure sustained line-fit avionics demand across the forecast period.

However, the retrofit/aftermarket segment is projected to register the highest CAGR during the forecast period. This growth is driven by the large global installed aircraft fleet requiring avionics upgrades to comply with regulatory mandates for ADS-B, Performance-Based Navigation, and communications system modernization, the business aviation fleet's strong avionics upgrade demand for glass cockpit retrofits and SATCOM installations, and the military aircraft avionics modernization programs that are upgrading existing airframes rather than procuring new aircraft in many national air force programs.

By Architecture Type: In 2026, IMA to Hold the Largest Share

Based on architecture type, the global advanced avionics systems market is segmented into federated avionics systems and integrated modular avionics. In 2026, the integrated modular avionics segment is expected to account for the largest share of the global advanced avionics systems market. IMA architecture, which consolidates multiple avionics functions on shared processing hardware modules with time-space partitioned operating environments, has become the standard architecture for modern commercial and military aircraft platforms including the Airbus A380 and A350, Boeing 787, F-35 Lightning II, and Eurofighter Typhoon. IMA's advantages in reducing hardware weight and volume, simplifying maintenance through line-replaceable module standardization, and enabling software-based avionics function upgrades without hardware replacement have established it as the dominant architecture for all new-design aircraft programs.

However, the software-defined avionics segment is projected to register the highest CAGR during the forecast period. Software-defined avionics extend IMA principles toward greater flexibility by enabling avionics functions to be reconfigured, updated, and expanded through software changes to standardized hardware platforms, reducing the time and cost of avionics capability upgrades and enabling in-service performance improvements without physical hardware modification. The growing demand for rapid avionics capability updates in response to evolving air traffic management requirements, threat environment changes in military applications, and the introduction of new communication standards is driving the adoption of software-defined architectures across both new aircraft programs and retrofit applications.

By Application: In 2026, Flight Operations and Navigation to Hold the Largest Share

Based on application, the global advanced avionics systems market is segmented into flight operations and navigation, safety and surveillance, mission and combat operations, aircraft health monitoring, and passenger and connectivity services. In 2026, the flight operations and navigation segment is expected to account for the largest share of the global advanced avionics systems market. Flight operations and navigation systems encompassing flight management computers, GPS and GNSS receivers, inertial navigation systems, and autopilot platforms are installed on every commercial, military, and business aviation aircraft and represent the core functional avionics category whose procurement volume across new aircraft and retrofit installations generates the highest aggregate segment revenue. Regulatory mandates for advanced navigation capability including RNAV and RNP approach procedures are driving sustained retrofit investment that reinforces the segment's dominant position.

However, the aircraft health monitoring segment is projected to register the highest CAGR during the forecast period. This growth is driven by airlines' strong financial motivation to adopt predictive maintenance programs that reduce unplanned aircraft on-ground events by detecting developing maintenance issues through real-time sensor data analysis, the OEM-driven expansion of aircraft condition monitoring system capabilities on new-generation aircraft that generate larger data volumes and more sophisticated health monitoring insights, and the growing regulatory emphasis on continuous airworthiness monitoring that is creating compliance-driven aircraft health monitoring investment across the global commercial fleet.

By End User: In 2026, Commercial Aviation Operators to Hold the Largest Share

Based on end user, the global advanced avionics systems market is segmented into commercial aviation operators, defense forces, business aviation operators, and UAV operators. In 2026, the commercial aviation operators segment is expected to account for the largest share of the global advanced avionics systems market. Commercial airlines represent the largest avionics procurement channel through their influence on OEM line-fit selection decisions and their direct retrofit investment programs, driven by the large global commercial fleet scale, the multiple regulatory avionics mandates affecting commercial operators, the airline industry's adoption of advanced connectivity and health management avionics for operational efficiency, and the high per-aircraft avionics content of narrowbody and widebody aircraft representing the majority of global commercial traffic capacity.

However, the UAV operators segment is projected to register the highest CAGR during the forecast period. This growth is driven by the explosive expansion of military unmanned system procurement across U.S. and allied defense forces for persistent surveillance, strike, and logistics missions requiring advanced avionics certification, the growing commercial UAV market adoption of FAA-certified avionics enabling beyond-visual-line-of-sight operations in controlled airspace, and the emerging eVTOL urban air mobility operator market requiring purpose-designed avionics suites for type certificate achievement and commercial operations launch.

Advanced Avionics Systems Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global advanced avionics systems market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global advanced avionics systems market. The largest share of this region is mainly due to the United States' position as the home of the world's two largest commercial aircraft manufacturers in Boeing and the major U.S. partner in Airbus programs, the dominant U.S. avionics supplier ecosystem anchored by Honeywell Aerospace, Collins Aerospace, Garmin Aviation, and L3Harris that collectively supply the majority of avionics content on both U.S.-manufactured and foreign aircraft, and the very large U.S. military aviation avionics market driven by the world's largest defense aviation fleet modernization programs. The U.S. commercial aviation fleet, comprising over 7,000 commercial jet aircraft operated by major U.S. airlines, generates the world's largest single-country commercial avionics retrofit and service market driven by the ongoing NextGen ATC modernization requirements and the large airline fleet investment programs in SATCOM connectivity and health management avionics. Canada's Bombardier business aviation and regional aircraft programs contribute additional North American avionics procurement demand, and Mexico's growing MRO and avionics installation services sector supports the regional market's aftermarket activities.

However, the Asia-Pacific advanced avionics systems market is expected to grow at the fastest CAGR during the forecast period. The region's rapid growth is driven by Asia-Pacific's position as the world's fastest-growing commercial aviation market, with Chinese, Indian, Southeast Asian, and Oceanian airline fleets expanding rapidly to serve the region's growing middle-class air travel demand, generating very large new aircraft delivery-driven line-fit avionics procurement programs at CAAC-regulated Chinese airlines and India's IndiGo, Air India, and Akasa Air expansion programs. China's Commercial Aircraft Corporation of China's C919 and C929 commercial aircraft development programs, though initially relying on international avionics suppliers including Honeywell, Collins, and Thales, are establishing Chinese domestic aviation industry capabilities and generating domestic avionics component demand. India's Tejas fighter jet program and the advancing AMCA fifth-generation fighter development are generating military avionics procurement demand for domestically developed and internationally sourced systems. Japan's F-35 program, South Korea's KF-21 Boramae indigenous fighter, and Australia's very large F-35 acquisition collectively contribute substantial Asia-Pacific military avionics procurement

Europe represents a large and technologically advanced avionics market anchored by Airbus's dominant commercial aircraft manufacturing programs generating very large line-fit avionics procurement for European suppliers including Thales, Safran, and Liebherr Aerospace, the large European commercial airline fleet's retrofit avionics investment driven by SESAR ATM modernization requirements and the EU's Single European Sky performance-based navigation mandates, and the substantial European military avionics procurement across Eurofighter, Rafale, Gripen, and NH90 helicopter programs. The Middle East's rapidly growing commercial aviation market, dominated by Emirates, Qatar Airways, and Etihad expanding their widebody fleets with high avionics content aircraft, combined with the Gulf states' substantial military aviation investment programs, positions the Middle East and Africa region as an important and growing avionics procurement market.

The global advanced avionics systems market is moderately consolidated among large diversified aerospace and defense electronics companies with broad avionics portfolios and established OEM platform supplier relationships, alongside specialist avionics companies focusing on specific system categories. Competition is focused on avionics system performance and reliability, FAA and EASA certification capability and speed, OEM platform supplier qualification status, product breadth across civil and military avionics categories, and the software and digital capability investments that differentiate advanced avionics products in an increasingly software-driven industry.

Honeywell Aerospace leads the market with the broadest civil and military avionics portfolio spanning navigation, communication, flight management, displays, surveillance, and connected aircraft platforms, with strong positions as launch avionics supplier on the Boeing 737 MAX, 787, and Airbus A320 and A350 families. Collins Aerospace, a business unit of RTX Corporation, competes as a full-spectrum avionics supplier with particular strength in commercial aviation communication and navigation systems, military avionics, and the Advanced Precision Kill Weapon System in the defense domain. Thales Group is the leading European avionics supplier with strong positions on Airbus commercial programs and European military platforms. Garmin has established a strong position in general aviation and business aviation avionics through its G3000, G5000, and G700 integrated flight deck systems that have captured substantial market share in the business jet and turboprop segments.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' product portfolios, platform supplier positions, geographic presence, and key strategic developments. Some of the key players operating in the global advanced avionics systems market include Honeywell International Inc. (U.S.), Collins Aerospace/RTX Corporation (U.S.), Thales Group (France), Garmin Ltd. (Switzerland/U.S.), Safran S.A. (France), Northrop Grumman Corporation (U.S.), BAE Systems plc (UK), L3Harris Technologies Inc. (U.S.), General Dynamics Corporation (U.S.), Leonardo S.p.A. (Italy), Elbit Systems Ltd. (Israel), Boeing Company (U.S.), Airbus SE (Netherlands), Mitsubishi Electric Corporation (Japan), and Panasonic Avionics Corporation (U.S.), among others.

The global advanced avionics systems market is expected to reach USD 142.8 billion by 2036 from an estimated USD 78.4 billion in 2026, at a CAGR of 6.2% during the forecast period 2026-2036.

In 2026, the communication systems segment is expected to hold the largest share of the global advanced avionics systems market, reflecting communication systems' position as the most broadly installed avionics category across commercial, military, and business aviation platforms with strong upgrade procurement driven by SATCOM broadband adoption and datalink mandate programs.

The health monitoring systems segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by airlines' accelerating adoption of predictive maintenance programs, the expanding OEM-installed aircraft health monitoring capabilities on new-generation aircraft, and growing regulatory emphasis on continuous airworthiness monitoring.

In 2026, the commercial aircraft segment is expected to hold the largest share of the global advanced avionics systems market, driven by Boeing and Airbus delivery programs generating large line-fit avionics procurement and the extensive retrofit requirements of the large global commercial fleet.

In 2026, the flight operations and navigation segment is expected to hold the largest share of the global advanced avionics systems market, as flight management, navigation, and autopilot systems are installed on virtually every commercial, military, and business aviation aircraft and represent the core functional avionics category.

The growth of this market is primarily driven by the strong recovery and sustained expansion of commercial aircraft deliveries from Boeing and Airbus generating very large line-fit avionics procurement programs, and the aviation industry's broad digital transformation toward connected aircraft architectures requiring SATCOM broadband, health monitoring, and digital datalink avionics investments across new aircraft and retrofit installation programs.

Key players are Honeywell International Inc. (U.S.), Collins Aerospace/RTX Corporation (U.S.), Thales Group (France), Garmin Ltd. (Switzerland/U.S.), Safran S.A. (France), Northrop Grumman Corporation (U.S.), BAE Systems plc (UK), L3Harris Technologies Inc. (U.S.), General Dynamics Corporation (U.S.), Leonardo S.p.A. (Italy), Elbit Systems Ltd. (Israel), Boeing Company (U.S.), Airbus SE (Netherlands), Mitsubishi Electric Corporation (Japan), and Panasonic Avionics Corporation (U.S.), among others.

Asia-Pacific is expected to register the highest growth rate in the global advanced avionics systems market during the forecast period 2026-2036, driven by the region's position as the world's fastest-growing commercial aviation market generating very large new aircraft line-fit avionics demand, China's domestic commercial aircraft development programs, and the substantial military avionics procurement across Japan, South Korea, India, and Australia's defense aviation expansion programs.

Published Date: May-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates