Resources

About Us

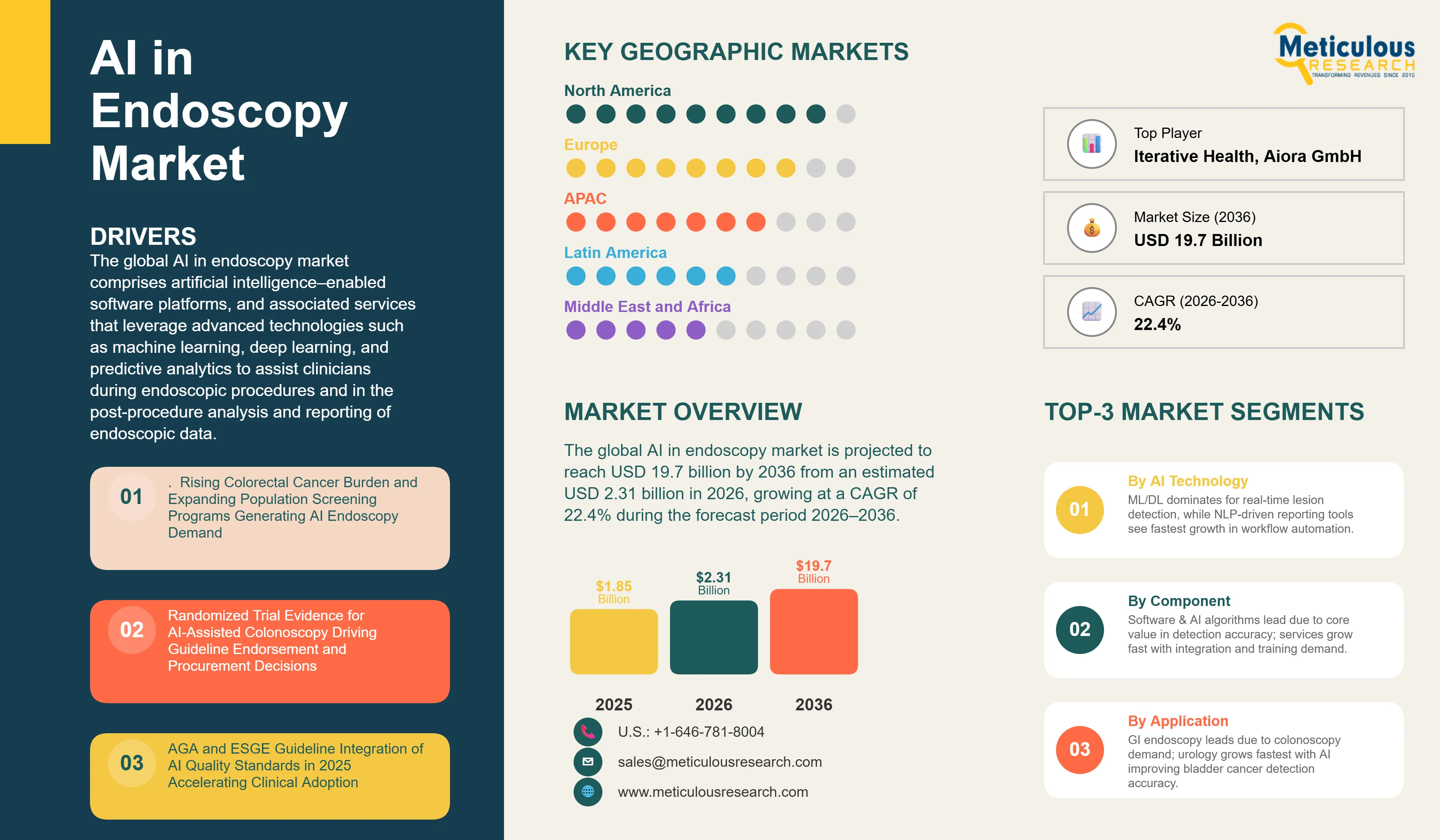

The global AI in endoscopy market was valued at USD 1.85 billion in 2025. The market is projected to reach USD 19.7 billion by 2036 from an estimated USD 2.31 billion in 2026, growing at a CAGR of 22.4% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global AI in endoscopy market comprises artificial intelligence–enabled software platforms, AI-integrated endoscopic systems, and associated services that leverage advanced technologies such as machine learning, deep learning, computer vision, natural language processing, and predictive analytics to assist clinicians during endoscopic procedures and in the post-procedure analysis and reporting of endoscopic data.

In clinical settings, AI in endoscopy is primarily deployed across two core functional paradigms: computer-aided detection (CADe) and computer-aided diagnosis/characterization (CADx). CADe systems operate in real time during endoscopic procedures, automatically identifying and highlighting suspected lesions within live video streams, thereby enhancing lesion detection rates and directing the endoscopist’s attention to areas of potential clinical significance. In contrast, CADx systems focus on the characterization of detected lesions, providing real-time optical assessments of lesion histology, morphology, and malignancy risk, and thereby supporting clinical decision-making, including resect-or-leave and biopsy-or-leave strategies at the point of care.

Beyond detection and characterization, the market covers a broadening suite of AI-driven workflow optimization solutions. These include automated bowel preparation assessment tools that evaluate and score preparation adequacy to guide procedural readiness; withdrawal time monitoring and mucosal coverage analytics to ensure adherence to quality benchmarks; and automated documentation solutions powered by natural language processing, which convert procedural data into structured, standardized endoscopy reports. Additionally, AI-enabled disease activity scoring systems are increasingly being adopted for conditions such as inflammatory bowel disease, facilitating objective and reproducible clinical assessments.

The scope of the market further extends to AI applications in capsule endoscopy, enabling automated video analysis and lesion flagging for small bowel investigations. Emerging use cases are also being observed in adjacent domains, including bronchoscopy for pulmonary nodule localization and navigation, and cystoscopy for enhanced detection of bladder malignancies.

Key end users of AI in endoscopy solutions include hospitals and large endoscopy centers, which are the primary adopters due to higher procedural volumes and infrastructure readiness; ambulatory surgical centers with established endoscopy programs; and specialized gastroenterology and endoscopy clinics. Collectively, these end users are driving the integration of AI technologies to improve diagnostic accuracy, procedural efficiency, and overall patient outcomes.

|

Parameters |

Details |

|---|---|

|

Market Size by 2036 |

USD 19.7 Billion |

|

Market Size in 2026 |

USD 2.31 Billion |

|

Market Size in 2025 |

USD 1.85 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 22.4% |

|

Dominating AI Technology |

Machine Learning & Deep Learning (Computer Vision) |

|

Fastest Growing AI Technology |

Natural Language Processing (NLP) / Automated Reporting |

|

Dominating Application |

Gastrointestinal (GI) Endoscopy / Colonoscopy |

|

Fastest Growing Application |

Urological Endoscopy |

|

Dominating Component |

Software & AI Algorithms (CADe / CADx Platforms) |

|

Fastest Growing Component |

Services (Implementation, Integration, Training) |

|

Dominating Endoscopy Type |

Flexible Endoscopy |

|

Fastest Growing Endoscopy Type |

Capsule Endoscopy |

|

Dominating Deployment Model |

On-Premise / Embedded AI Systems |

|

Fastest Growing Deployment Model |

Cloud-Based AI Platforms |

|

Dominating End User |

Hospitals & Endoscopy Centers |

|

Fastest Growing End User |

Ambulatory Surgical Centers (ASCs) |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Clinical Evidence & Guideline Adoption Accelerate AI Colonoscopy

A key trend in the AI in endoscopy market is the rapid maturation of the clinical evidence base for AI-assisted colonoscopy, transitioning from early feasibility studies to large, multicenter randomized controlled trials (RCTs) demonstrating statistically significant and clinically meaningful improvements in adenoma detection rates (ADR) in routine practice. This strengthening evidence-base combined with formal endorsements from leading gastroenterology societies is driving the transition of AI-assisted colonoscopy from an early-adopter technology to an emerging clinical quality standard across endoscopy units and healthcare systems.

From a clinical outcomes perspective, multiple longitudinal studies have consistently shown that each 1% increase in ADR is associated with an approximate 3% reduction in the risk of colorectal cancer. Accordingly, the ~8–10 percentage point improvements in ADR reported across leading AI-assisted colonoscopy trials suggest a potentially meaningful reduction in long-term colorectal cancer incidence, reinforcing the clinical and economic value proposition of AI integration.

The translation of this evidence into formal clinical guidance marks a critical inflection point for market adoption. In 2025, the American Gastroenterological Association (AGA) issued formal guidance recognizing the role of computer-aided detection (CADe) systems in improving colonoscopy quality metrics. Similarly, the European Society of Gastrointestinal Endoscopy (ESGE) incorporated AI into its 2025 guidelines for colonoscopy quality assurance. These endorsements from leading professional bodies provide strong validation of clinical utility and are expected to play a pivotal role in accelerating procurement decisions, reimbursement considerations, and broader institutional adoption.

Collectively, the convergence of robust RCT evidence and guideline-level validation is transforming AI-assisted colonoscopy into a clinically endorsed, evidence-backed standard of care, positioning it as a key growth driver in the AI in endoscopy market.

AI Endoscopy Expansion Across Adjacent Applications

While AI-assisted colonoscopy remains the most mature and commercially established application, driven by its proven impact on adenoma detection rates, the AI in endoscopy market is rapidly expanding into adjacent clinical areas, such as upper gastrointestinal (GI) endoscopy, Barrett’s esophagus surveillance, inflammatory bowel disease (IBD) assessment, capsule endoscopy, and emerging urological and pulmonary applications. This expansion is driven by the scalability of deep learning–based computer vision models across anatomical regions and imaging modalities, as well as strategic efforts by endoscopy platform providers to extend AI capabilities across their installed base.

Barrett’s esophagus is one of the most prominent upper GI use cases. As a precancerous condition associated with esophageal adenocarcinoma, it requires high-precision surveillance to detect early dysplasia, which is often subtle and easily missed. AI-based detection tools are being developed to enhance the visualization and identification of dysplastic lesions. For instance, Olympus Corporation has introduced AI-enabled solutions such as CADU within its OLYSENSE platform (integrated via Odin Vision), targeting improved detection in Barrett’s surveillance workflows. Although the evidence base in this segment is still evolving, increasing availability of annotated datasets and ongoing clinical trials are expected to accelerate adoption.

In inflammatory bowel disease, AI applications are focused on standardizing disease activity assessment. Tools such as SMARTIBD (developed by Olympus Corporation) enable automated scoring of mucosal inflammation in ulcerative colitis, addressing longstanding challenges related to inter-observer variability and improving consistency in treatment decision-making.

Beyond GI applications, AI in endoscopy is gaining traction in urology and pulmonology. AI-assisted cystoscopy for bladder cancer detection is emerging as a high-growth segment, driven by the clinical need for improved detection of recurrent tumors, including flat carcinoma in situ lesions that are frequently missed under conventional white-light imaging. Given the high recurrence rates of bladder cancer and the requirement for lifelong surveillance, AI integration offers a strong value proposition in improving diagnostic accuracy and reducing disease burden.

Similarly, in respiratory endoscopy, AI-assisted bronchoscopy is advancing, mainly for navigation and localization of peripheral pulmonary nodules. Platforms such as the Ion system developed by Intuitive Surgical incorporate AI-driven guidance to enhance procedural precision, representing a convergence of robotics and AI within endoscopic interventions.

In addition, capsule endoscopy is witnessing increased AI adoption for automated video analysis and lesion detection in small bowel imaging, significantly reducing physician reading time and improving diagnostic yield.

Collectively, the expansion of AI across these adjacent applications is broadening the total addressable market for AI in endoscopy, enabling vendors to move beyond single-use-case solutions toward integrated, multi-application AI platforms that enhance clinical value, workflow efficiency, and return on investment for healthcare providers.

By AI Technology: In 2026, Machine Learning & Deep Learning to Dominate the Global AI in Endoscopy Market

Based on AI technology, the AI in endoscopy market is segmented into machine learning and deep learning (computer vision, CADe and CADx), natural language processing and automated reporting, predictive analytics and decision support, and other AI technologies.

In 2026, machine learning (ML) and deep learning (DL) are expected to account for the largest share of the global AI in endoscopy market, driven by their central role in real-time image and video analysis. Deep learning, mainly convolutional neural networks (CNNs), is highly aligned with endoscopic use cases, as it enables high-speed processing of video streams with low latency suitable for real-time procedural guidance. These models can be trained on large, annotated datasets from high-volume endoscopy centers, achieving performance levels comparable to expert endoscopists in lesion detection tasks, while also demonstrating the ability to generalize across different endoscope platforms and imaging conditions.

Solutions such as GI Genius (developed by Cosmo Intelligent Medical Devices and distributed by Medtronic), CADDIE, and CAD EYE by Fujifilm Holdings Corporation are all built on CNN-based frameworks for real-time polyp detection. Similarly, the EVIS X1 platform from Olympus Corporation incorporates ML/DL-driven image enhancement and pattern recognition capabilities for lesion characterization, further reinforcing the technological foundation of the market.

In contrast, natural language processing (NLP) and AI-driven documentation solutions are projected to register the fastest growth rate among technology segments over the forecast period. This growth is primarily driven by the increasing need to automate endoscopy reporting workflows, which remain time-intensive and prone to variability. NLP-based systems enable automated generation of structured endoscopy reports, extraction of key quality metrics, and seamless integration with electronic medical record (EMR) systems.

By Component: In 2026, Software & AI Algorithms to Hold the Largest Share

Based on component, the AI in endoscopy market is segmented into software and AI algorithms (CADe platforms, CADx platforms, workflow automation software), hardware (AI-integrated endoscopes, dedicated AI processing modules), and services (implementation and integration, training and education, maintenance and support).

In 2026, software and AI algorithms are expected to account for the largest share of the overall AI in endoscopy market, indicating the inherently software-centric nature of value creation in this domain. The clinical and commercial differentiation of AI endoscopy solutions is primarily determined by algorithm performance, mainly in terms of detection sensitivity, specificity, false-positive rates, and robustness across varying lesion types, sizes, and morphologies, rather than the underlying hardware.

AI software can be deployed across multiple architectures, including modular integration with existing endoscopy systems (as demonstrated by GI Genius developed by Cosmo Intelligent Medical Devices and distributed by Medtronic), cloud-based platforms accessible via connected endoscopy infrastructure (such as OLYSENSE CAD/AI by Olympus Corporation), and fully embedded solutions within next-generation AI-native endoscopy platforms. Cloud and edge-based deployment models are particularly significant, as they lower upfront capital requirements, enable continuous algorithm updates, and facilitate scalable adoption across healthcare institutions.

However, the services segment is projected to register the fastest compound annual growth rate (CAGR) over the forecast period. This growth is driven by the increasing reliance of healthcare providers on specialized vendors for end-to-end implementation, including system integration with legacy endoscopy equipment and electronic medical record (EMR) systems, clinician training, workflow optimization, and ongoing technical support.

By Application: In 2026, Gastrointestinal Endoscopy to Dominate the Global AI in Endoscopy Market

Based on application, the market is segmented into gastrointestinal endoscopy (colonoscopy, upper GI endoscopy, capsule endoscopy), respiratory endoscopy (bronchoscopy), urological endoscopy (cystoscopy), and other applications.

In 2026, gastrointestinal endoscopy is expected to account for the dominant application share, driven by the clinical evidence base for AI-assisted colonoscopy and the scale of the global colorectal cancer screening program that generates the procedure volume through which AI endoscopy creates value.

Urological endoscopy is expected to register the fastest CAGR among application segments, driven by the high recurrence rate of bladder cancer that demands life-long surveillance cystoscopy for affected patients; the well-documented miss rate for flat and small bladder lesions during standard white-light cystoscopy; and the strong clinical logic of applying the proven AI detection paradigm from colonoscopy to the structurally similar surveillance cystoscopy context.

By Indication: In 2026, Colorectal Cancer & Polyp Detection to Hold the Largest Share

Based on indication, the market is segmented into colorectal cancer and polyp detection, gastric cancer and gastric lesions, esophageal cancer and Barrett’s esophagus, inflammatory bowel disease, inflammatory and other GI disorders, and other indications.

In 2026, colorectal cancer and polyp detection is expected to account for the dominant indication share, driven by the scale of the global colorectal cancer screening program, the robustness of the randomized controlled trial evidence base including the COLO-DETECT trial, and the AGA’s March 2025 formal guidance on CADe use in colonoscopy.

Gastric cancer and gastric lesion detection is expected to represent a large and growing indication, particularly in Asia Pacific markets where gastric cancer incidence is 8 to 10-fold higher than in Western countries. AI systems trained on large Japanese and South Korean gastric endoscopy datasets are now being deployed commercially and in clinical research programs across the region for early gastric cancer detection and lesion characterization.

By End User: In 2026, Hospitals & Endoscopy Centers to Hold the Largest Share

Based on end user, the market is segmented into hospitals and endoscopy centers, ambulatory surgical centers, specialty clinics, and other end users.

In 2026, hospitals and endoscopy centers are expected to account for the largest share of the AI in endoscopy market, indicating their role as the primary settings for high-volume and high-complexity procedures, including colorectal cancer screening colonoscopies, upper GI endoscopy, and advanced therapeutic interventions. These facilities are typically early adopters of advanced imaging and AI-enabled diagnostic technologies, driven by stronger capital budgets, established digital infrastructure, and access to skilled clinical personnel.

Hospital-based endoscopy programs derive significant value from AI platforms through improved workflow efficiency, enhanced quality benchmarking (e.g., adenoma detection rate monitoring), and clinician training support. In addition, procurement decisions at the hospital network or integrated delivery system level often involve multi-site deployments and long-term contracts, making this segment the primary revenue contributor in the market.

Ambulatory surgical centers (ASCs), on the other hand, are projected to register the fastest compound annual growth rate (CAGR) during the forecast period. This growth is driven by the ongoing shift of routine colonoscopy procedures from inpatient hospital settings to lower-cost outpatient environments, supported by favorable reimbursement dynamics and increasing patient preference for minimally invasive, same-day procedures.

Within ASCs, AI-assisted endoscopy is gaining traction as a tool for quality differentiation. The ability to consistently demonstrate high adenoma detection rates and standardized reporting supports physician referral growth and alignment with payer-driven quality programs. Furthermore, as professional bodies such as the American Gastroenterological Association (AGA) and the European Society of Gastrointestinal Endoscopy (ESGE) increasingly recognize AI-assisted colonoscopy as a quality-enhancing tool, adoption among ASCs is expected to accelerate.

Thus, the expansion of AI into outpatient settings, combined with increasing emphasis on measurable quality outcomes, positions ASCs as a key high-growth end-user segment in the AI in endoscopy market.

Based on geography, the global AI in endoscopy market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

North America is expected to account for the largest share of the global AI in endoscopy market in 2026. The largest share of this region is mainly attributed to the three key factors. First, regulatory precedence: the U.S. Food and Drug Administration (FDA) granted de novo clearance to GI Genius (developed by Cosmo Intelligent Medical Devices and commercialized by Medtronic) in 2021, establishing the first regulatory pathway for AI-assisted colonoscopy systems, followed by subsequent clearances for additional CADe/CADx solutions, including CADDIE. Second, strong clinical evidence generation, driven by leading academic and clinical institutions such as GI Alliance and Brigham and Women’s Hospital, which have contributed to large-scale trials validating AI efficacy. Third, a dense commercial ecosystem comprising established medtech companies and AI health startups, enabling rapid innovation and deployment.

Europe is the second-largest regional market for AI in endoscopy, with key countries including the U.K., Germany, France, Italy, and the Netherlands. The region benefits from strong clinical validation and early guideline adoption. The U.K., in particular, has played a pivotal role through large-scale randomized controlled trials that have influenced procurement decisions within public healthcare systems. Additionally, the 2025 guidelines issued by the European Society of Gastrointestinal Endoscopy (ESGE) endorsing AI for colonoscopy quality assurance mark a significant milestone, accelerating institutional adoption across EU healthcare systems. On the commercial front, Olympus Corporation has strengthened its position through CE-marked AI solutions (via the Odin Vision platform), offering an integrated suite for detection, characterization, and workflow support.

Asia-Pacific AI in endoscopy market is projected to grow at the fastest CAGR during the forecast period, driven by expanding healthcare infrastructure, large patient volumes, and strong government support for AI integration in healthcare. Japan and South Korea are the mature markets, supported by high endoscopy procedure volumes and the presence of leading manufacturers such as Olympus Corporation and Fujifilm Holdings Corporation. China has emerged as a major hub for AI research in digestive endoscopy, supported by significant academic output and policy-level prioritization of AI in healthcare. India is also witnessing increasing adoption, particularly within private hospital networks; for instance, deployments of AI-enabled systems such as CAD EYE by Fujifilm Holdings Corporation highlight the early-stage but accelerating market penetration.

Latin America and the Middle East & Africa are expected to witness gradual adoption, primarily concentrated in leading private hospitals and academic medical centers. In Latin America, Brazil, Mexico, and Colombia are emerging as key markets, driven by expanding cancer screening initiatives and improving healthcare infrastructure. Meanwhile, in the Middle East, countries such as Saudi Arabia and the UAE are investing in advanced digital health technologies as part of broader healthcare transformation programs, creating opportunities for AI-integrated endoscopy solutions.

The global AI in endoscopy market is moderately consolidated at the platform level, with the top five companies—Medtronic, Olympus Corporation, Fujifilm Holdings Corporation, HOYA Corporation / Pentax Medical, and Intuitive Surgical—collectively accounting for approximately 60–70% of the global market share. However, competition is intensifying at the software and algorithm layer, where a growing number of specialized AI companies are introducing differentiated, hardware-agnostic solutions.

Among market leaders, Medtronic maintains the strongest commercial position, supported by its extensive installed base and robust clinical evidence portfolio. Its GI Genius system (licensed from Cosmo Intelligent Medical Devices) was the first FDA-cleared AI-assisted colonoscopy platform and remains one of the most widely deployed systems, with validation from large-scale randomized controlled trials, including COLO-DETECT.

Olympus Corporation is undergoing a strategic transition toward integrated, AI-enabled care delivery, anchored by its OLYSENSE cloud-based AI suite, which spans colonoscopy, Barrett’s esophagus, and inflammatory bowel disease (IBD) applications. The company has further strengthened its capabilities through the acquisition of Odin Vision.

Fujifilm Holdings Corporation has developed the CAD EYE platform, which is tightly integrated with its ELUXEO endoscopy systems, enabling both CADe and CADx functionalities. Meanwhile, Pentax Medical (a division of HOYA Corporation) differentiates through dedicated AI hardware architectures designed for low-latency processing in real-time clinical settings.

In parallel, Intuitive Surgical is expanding AI capabilities within robotic-assisted endoscopy, particularly in bronchoscopy, reflecting convergence between robotics and AI-driven visualization.

Beyond these platform leaders, a dynamic ecosystem of specialist AI companies is shaping innovation at the software layer. Firms such as Iterative Health (formerly Iterative Scopes) focus on hardware-agnostic deep learning platforms, while Wision AI Co., Ltd. and MAGENTIQ EYE Ltd. are gaining traction in targeted detection applications.

Strategic collaborations, acquisitions, and licensing agreements remain central to competitive positioning. Notable examples include Olympus’ acquisition of Odin Vision, partnerships involving Karl Storz, and Medtronic’s licensing arrangement with Cosmo Intelligent Medical Devices. These strategies enable established medtech companies to rapidly integrate advanced AI capabilities while allowing specialized AI firms to scale through global distribution networks.

Key players operating in the global AI in endoscopy market include Medtronic, Olympus Corporation, Fujifilm Holdings Corporation, HOYA Corporation / Pentax Medical, Intuitive Surgical, Boston Scientific Corporation, Karl Storz, Iterative Health, Cosmo Intelligent Medical Devices, Wision AI Co., Ltd., MAGENTIQ EYE Ltd., Ambu A/S, Stryker Corporation, Aiora GmbH, Satisfai Health Inc., AI Medical Service Inc., EndoAid Ltd., Johnson & Johnson MedTech (including Auris Health), and Phathom Pharmaceuticals, among others.

This report provides market size estimates and forecasts for each segment and sub-segment at the global, regional, and country levels. The report further offers an in-depth analysis of the latest clinical evidence developments, technology advances, regulatory approvals, reimbursement trends, and key strategic initiatives across each sub-segment for the forecast period 2026–2036.

For the purpose of this study, the global AI in Endoscopy Market has been segmented based on AI technology, component, application, indication, deployment model, end user, and geography.

|

Segment |

Sub-Segments |

|---|---|

|

By AI Technology |

Machine Learning & Deep Learning (Computer Vision / CADe / CADx), Natural Language Processing (NLP) / Automated Reporting, Predictive Analytics & Decision Support, Other AI Technologies |

|

By Component |

Software & AI Algorithms (CADe Platforms, CADx Platforms, Workflow Automation Software), Hardware (AI-Integrated Endoscopes, Dedicated AI Processing Modules), Services (Implementation & Integration, Training & Education, Maintenance & Support) |

|

By Application |

Gastrointestinal (GI) Endoscopy (Colonoscopy, Upper GI Endoscopy, Capsule Endoscopy), Respiratory Endoscopy (Bronchoscopy), Urological Endoscopy (Cystoscopy), Other Applications |

|

By Indication |

Colorectal Cancer & Polyp Detection, Gastric Cancer & Gastric Lesions, Esophageal Cancer & Barrett’s Esophagus, Inflammatory Bowel Disease (IBD), Inflammatory & Other GI Disorders, Other Indications |

|

By Deployment Model |

On-Premise / Embedded AI Systems, Cloud-Based AI Platforms, Hybrid Deployment Models |

|

By End User |

Hospitals & Endoscopy Centers, Ambulatory Surgical Centers (ASCs), Specialty Clinics, Other End Users |

|

By Geography |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

By AI Technology (Revenue, USD Billion, 2026–2036)

By Component (Revenue, USD Billion, 2026–2036)

By Application (Revenue, USD Billion, 2026–2036)

By Indication (Revenue, USD Billion, 2026–2036)

By Deployment Model (Revenue, USD Billion, 2026–2036)

By End User (Revenue, USD Billion, 2026–2036)

By Geography (Revenue, USD Billion, 2026–2036)

The global AI in endoscopy market is expected to reach USD 19.7 billion by 2036 from an estimated USD 2.31 billion in 2026, at a CAGR of 22.4% during the forecast period 2026–2036.

In 2026, machine learning and deep learning are expected to hold the largest share of the global AI in endoscopy market, driven by the commercial deployment of deep learning CADe systems including Medtronic’s GI Genius, Olympus’s CADDIE 2, and Fujifilm’s CAD EYE. Natural language processing and automated reporting is expected to register the fastest CAGR as hospitals seek to automate endoscopy documentation and quality metric extraction to complement their lesion detection AI investments.

GI endoscopy is expected to hold the dominant application share, supported by the COLO-DETECT trial documenting a 56.6% vs 48.4% adenoma detection rate advantage for CADe-assisted colonoscopy in The Lancet Gastroenterology & Hepatology, the AGA’s March 2025 formal CADe guidance, and the ESGE’s 2025 AI quality assurance guidelines. Urological endoscopy (cystoscopy) is expected to register the fastest CAGR, driven by bladder cancer’s high recurrence rates creating large surveillance cystoscopy volumes and the clinical logic for AI detection assistance.

The growth of this market is primarily driven by the COLO-DETECT trial (Lancet GH, 2024) documenting CADe-assisted colonoscopy ADR of 56.6% vs 48.4% (p<0.0001) in 2,032 patients; Medtronic’s GI Genius demonstrating 14% absolute ADR increase and 50% miss rate reduction; the AGA publishing formal CADe guidance in March 2025; the ESGE issuing 2025 AI colonoscopy quality assurance guidelines; Olympus launching OLYSENSE CAD/AI cloud suite (CADDIE 2, CADU, SMARTIBD) in the U.S. and Europe in September 2025; CADDIE receiving FDA 510(k) clearance in July 2024; Olympus’s November 2025 strategic transformation toward AI-led intelligent care; Fujifilm India’s first CAD EYE installation in Jaipur (November 2025); China contributing 745+ AI digestive endoscopy publications; and the World Gastroenterology Organization documenting 1.9 million annual colorectal cancer cases globally.

Key players in the global AI in endoscopy market include Medtronic plc (Ireland), Olympus Corporation (Japan), FUJIFILM Holdings Corporation (Japan), HOYA Corporation / Pentax Medical (Japan), Intuitive Surgical, Inc. (U.S.), Iterative Health (U.S.), Cosmo Intelligent Medical Devices / Linkverse (Ireland), Odin Vision Ltd. (UK/Olympus), Karl Storz SE & Co. KG (Germany), Wision AI Co., Ltd. (China), MAGENTIQ EYE Ltd. (Israel), Boston Scientific Corporation (U.S.), Ambu A/S (Denmark), and AI Medical Service Inc. (Japan). The top 5 companies account for approximately 70% of global market share according to GMI.

Asia Pacific is expected to register the highest growth rate during the forecast period, driven by Japan and South Korea’s leading AI endoscopy hardware base through Olympus and Fujifilm; China’s 745+ AI digestive endoscopy publications and AI-led national cancer screening programs; and India’s rapidly expanding private hospital advanced endoscopy capability (Fujifilm CAD EYE first installation in Jaipur, November 2025).

The global AI in endoscopy market is expected to reach USD 19.7 billion by 2036 from an estimated USD 2.31 billion in 2026, at a CAGR of 22.4% during the forecast period 2026–2036.

In 2026, machine learning and deep learning are expected to hold the largest share of the global AI in endoscopy market, driven by the commercial deployment of deep learning CADe systems including Medtronic’s GI Genius, Olympus’s CADDIE 2, and Fujifilm’s CAD EYE. Natural language processing and automated reporting is expected to register the fastest CAGR as hospitals seek to automate endoscopy documentation and quality metric extraction to complement their lesion detection AI investments.

GI endoscopy is expected to hold the dominant application share, supported by the COLO-DETECT trial documenting a 56.6% vs 48.4% adenoma detection rate advantage for CADe-assisted colonoscopy in The Lancet Gastroenterology & Hepatology, the AGA’s March 2025 formal CADe guidance, and the ESGE’s 2025 AI quality assurance guidelines. Urological endoscopy (cystoscopy) is expected to register the fastest CAGR, driven by bladder cancer’s high recurrence rates creating large surveillance cystoscopy volumes and the clinical logic for AI detection assistance.

The growth of this market is primarily driven by the COLO-DETECT trial (Lancet GH, 2024) documenting CADe-assisted colonoscopy ADR of 56.6% vs 48.4% (p<0.0001) in 2,032 patients; Medtronic’s GI Genius demonstrating 14% absolute ADR increase and 50% miss rate reduction; the AGA publishing formal CADe guidance in March 2025; the ESGE issuing 2025 AI colonoscopy quality assurance guidelines; Olympus launching OLYSENSE CAD/AI cloud suite (CADDIE 2, CADU, SMARTIBD) in the U.S. and Europe in September 2025; CADDIE receiving FDA 510(k) clearance in July 2024; Olympus’s November 2025 strategic transformation toward AI-led intelligent care; Fujifilm India’s first CAD EYE installation in Jaipur (November 2025); China contributing 745+ AI digestive endoscopy publications; and the World Gastroenterology Organization documenting 1.9 million annual colorectal cancer cases globally.

Key players in the global AI in endoscopy market include Medtronic plc (Ireland), Olympus Corporation (Japan), FUJIFILM Holdings Corporation (Japan), HOYA Corporation / Pentax Medical (Japan), Intuitive Surgical, Inc. (U.S.), Iterative Health (U.S.), Cosmo Intelligent Medical Devices / Linkverse (Ireland), Odin Vision Ltd. (UK/Olympus), Karl Storz SE & Co. KG (Germany), Wision AI Co., Ltd. (China), MAGENTIQ EYE Ltd. (Israel), Boston Scientific Corporation (U.S.), Ambu A/S (Denmark), and AI Medical Service Inc. (Japan). The top 5 companies account for approximately 70% of global market share according to GMI.

Asia Pacific is expected to register the highest growth rate during the forecast period, driven by Japan and South Korea’s leading AI endoscopy hardware base through Olympus and Fujifilm; China’s 745+ AI digestive endoscopy publications and AI-led national cancer screening programs; and India’s rapidly expanding private hospital advanced endoscopy capability (Fujifilm CAD EYE first installation in Jaipur, November 2025).

1. INTRODUCTION

1.1. Market Definition & Scope

1.2. Market Ecosystem

1.3. Currency & Pricing Assumptions

1.4. Key Stakeholders

2. RESEARCH METHODOLOGY

2.1. Research Process

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research / Interviews with Key Opinion Leaders from the Industry

2.3. Market Assessment

2.3.1. Market Size Estimation

2.3.1.1. Bottom-up Approach

2.3.1.2. Top-down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

2.4. Limitations of the Study

3. EXECUTIVE SUMMARY

3.1. Overview

3.2. Market by AI Technology

3.3. Market by Component

3.4. Market by Application

3.5. Market by Indication

3.6. Market by Deployment Model

3.7. Market by End User

3.8. Market by Geography

3.9. Competitive Landscape Snapshot

3.10. Key Strategic Insights

3.11. Analyst Recommendations

4. MARKET INSIGHTS

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Rising Colorectal Cancer Burden and Expanding Population Screening Programs Generating AI Endoscopy Demand

4.2.1.2. Randomized Trial Evidence for AI-Assisted Colonoscopy Driving Guideline Endorsement and Procurement Decisions

4.2.1.3. AGA and ESGE Guideline Integration of AI Quality Standards in 2025 Accelerating Clinical Adoption

4.2.1.4. Platform Company Investment in AI Ecosystems (Olympus, Fujifilm, Medtronic) Creating Market Infrastructure

4.2.1.5. AI Endoscopy Expansion Into Upper GI, Barrett’s, IBD, and Urological Applications Expanding Addressable Market

4.2.2. Restraints

4.2.2.1. High Implementation Cost and Integration Complexity Limiting Adoption at Smaller Endoscopy Units

4.2.2.2. Data Privacy and Governance Requirements for AI Training and Cloud Deployment in Healthcare

4.2.2.3. Physician Workflow Disruption Concerns and Alert Fatigue Risk From High False Positive Detection Rates

4.2.2.4. Limited Reimbursement Frameworks for AI-Assisted Endoscopy in Most National Healthcare Systems

4.2.3. Opportunities

4.2.3.1. Payer Coverage Development for AI-Enhanced Procedures as Quality Evidence Accumulates

4.2.3.2. Emerging AI Applications in Barrett’s Esophagus, IBD Activity Assessment, and Capsule Endoscopy Reading

4.2.3.3. AI-Assisted Quality Benchmarking Platforms Enabling Hospital Network-Scale Performance Analytics

4.2.3.4. Cloud AI Deployment Reducing Hardware Investment Barrier and Enabling Multi-Site Enterprise Rollouts

4.2.4. Challenges

4.2.4.1. Algorithm Generalizability Across Different Endoscope Platforms, Bowel Preparation Quality, and Patient Populations

4.2.4.2. Regulatory Pathway Complexity for SaMD (Software as a Medical Device) Across Multiple National Jurisdictions

4.2.4.3. Clinical Validation Requirements for Each New Application (Barrett’s, Gastric, Bladder) Requiring Independent RCT Evidence

4.3. Porter’s Five Forces Analysis

4.3.1. Bargaining Power of Suppliers

4.3.2. Bargaining Power of Buyers

4.3.3. Threat of Substitutes

4.3.4. Threat of New Entrants

4.3.5. Degree of Competition

4.4. Regulatory Landscape

4.4.1. U.S. — FDA De Novo and 510(k) Clearance for SaMD, FDA AI/ML-Based Software as a Medical Device Action Plan

4.4.2. Europe — EU MDR (AI Medical Device Regulation), CE Mark Requirements, ESGE 2025 AI Colonoscopy Guidelines

4.4.3. Asia Pacific — Japan PMDA, South Korea MFDS, China NMPA AI Medical Device Framework, India CDSCO

4.4.4. Other Key Regulatory Jurisdictions

4.5. Value Chain Analysis

4.6. Impact of Macroeconomic Factors

5. AI IN ENDOSCOPY MARKET, BY AI TECHNOLOGY

5.1. Overview

5.2. Machine Learning & Deep Learning (Computer Vision)

5.2.1. Computer-Aided Detection (CADe)

5.2.2. Computer-Aided Diagnosis / Characterization (CADx)

5.2.3. Bowel Preparation & Quality Assessment AI

5.2.4. Withdrawal Speed & Coverage Monitoring AI

5.3. Natural Language Processing (NLP) / Automated Reporting

5.4. Predictive Analytics & Decision Support

5.5. Other AI Technologies

6. AI IN ENDOSCOPY MARKET, BY COMPONENT

6.1. Overview

6.2. Software & AI Algorithms

6.2.1. CADe Platforms

6.2.2. CADx Platforms

6.2.3. Workflow Automation & Documentation Software

6.3. Hardware

6.3.1. AI-Integrated Endoscopes

6.3.2. Dedicated AI Processing Modules (Add-On)

6.4. Services (Implementation, Training, Maintenance)

7. AI IN ENDOSCOPY MARKET, BY APPLICATION

7.1. Overview

7.2. Gastrointestinal (GI) Endoscopy

7.2.1. Colonoscopy

7.2.2. Upper GI Endoscopy

7.2.3. Capsule Endoscopy

7.3. Respiratory Endoscopy (Bronchoscopy)

7.4. Urological Endoscopy (Cystoscopy)

7.5. Other Applications

8. AI IN ENDOSCOPY MARKET, BY INDICATION

8.1. Overview

8.2. Colorectal Cancer & Polyp Detection

8.3. Gastric Cancer & Gastric Lesions

8.4. Esophageal Cancer & Barrett’s Esophagus

8.5. Inflammatory Bowel Disease (IBD)

8.6. Inflammatory & Other GI Disorders

8.7. Other Indications

9. AI IN ENDOSCOPY MARKET, BY DEPLOYMENT MODEL

9.1. Overview

9.2. On-Premise / Embedded AI Systems

9.3. Cloud-Based AI Platforms

9.4. Hybrid Deployment Models

10. AI IN ENDOSCOPY MARKET, BY END USER

10.1. Overview

10.2. Hospitals & Endoscopy Centers

10.3. Ambulatory Surgical Centers (ASCs)

10.4. Specialty Clinics

10.5. Other End Users

11. AI IN ENDOSCOPY MARKET, BY GEOGRAPHY

11.1. Overview

11.2. North America

11.2.1. U.S.

11.2.2. Canada

11.3. Europe

11.3.1. U.K.

11.3.2. Germany

11.3.3. France

11.3.4. Italy

11.3.5. Spain

11.3.6. Netherlands

11.3.7. Rest of Europe

11.4. Asia Pacific

11.4.1. Japan

11.4.2. China

11.4.3. South Korea

11.4.4. India

11.4.5. Australia

11.4.6. Rest of Asia Pacific

11.5. Latin America

11.5.1. Brazil

11.5.2. Mexico

11.5.3. Rest of Latin America

11.6. Middle East & Africa

11.6.1. Saudi Arabia

11.6.2. UAE

11.6.3. Israel

11.6.4. South Africa

11.6.5. Rest of Middle East & Africa

12. COMPETITIVE LANDSCAPE

12.1. Overview

12.2. Key Growth Strategies

12.2.1. Market Differentiators

12.2.2. Synergy Analysis: Acquisitions, Partnerships, and Licensing Arrangements

12.3. Competitive Dashboard

12.3.1. Industry Leaders

12.3.2. Market Differentiators

12.3.3. Vanguards

12.3.4. Emerging Companies

12.4. Competitive Benchmarking

12.5. Market Share / Ranking Analysis (2025)

13. COMPANY PROFILES

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, and SWOT Analysis)

13.1. Medtronic plc (Ireland)

13.2. Olympus Corporation (Japan)

13.3. FUJIFILM Holdings Corporation (Japan)

13.4. HOYA Corporation / Pentax Medical (Japan)

13.5. Intuitive Surgical, Inc. (U.S.)

13.6. Boston Scientific Corporation (U.S.)

13.7. Karl Storz SE & Co. KG (Germany)

13.8. Iterative Health (U.S.)

13.9. Cosmo Intelligent Medical Devices / Linkverse (Ireland)

13.10. Odin Vision Ltd. (UK / Olympus)

13.11. Wision AI Co., Ltd. (China)

13.12. MAGENTIQ EYE Ltd. (Israel)

13.13. Ambu A/S (Denmark)

13.14. Stryker Corporation (U.S.)

13.15. AI Medical Service Inc. (Japan)

13.16. Endoaid Ltd. (Israel)

13.17. Aiora GmbH (Germany)

13.18. Satisfai Health Inc. (Canada)

13.19. Others

14. APPENDIX

14.1. Questionnaire

14.2. Customization Options

14.3. Abbreviations

14.4. List of Data Sources

Published Date: Feb-2026

Published Date: Feb-2026

Published Date: Nov-2022

Published Date: Feb-2026

Subscribe to get the latest industry updates