Resources

About Us

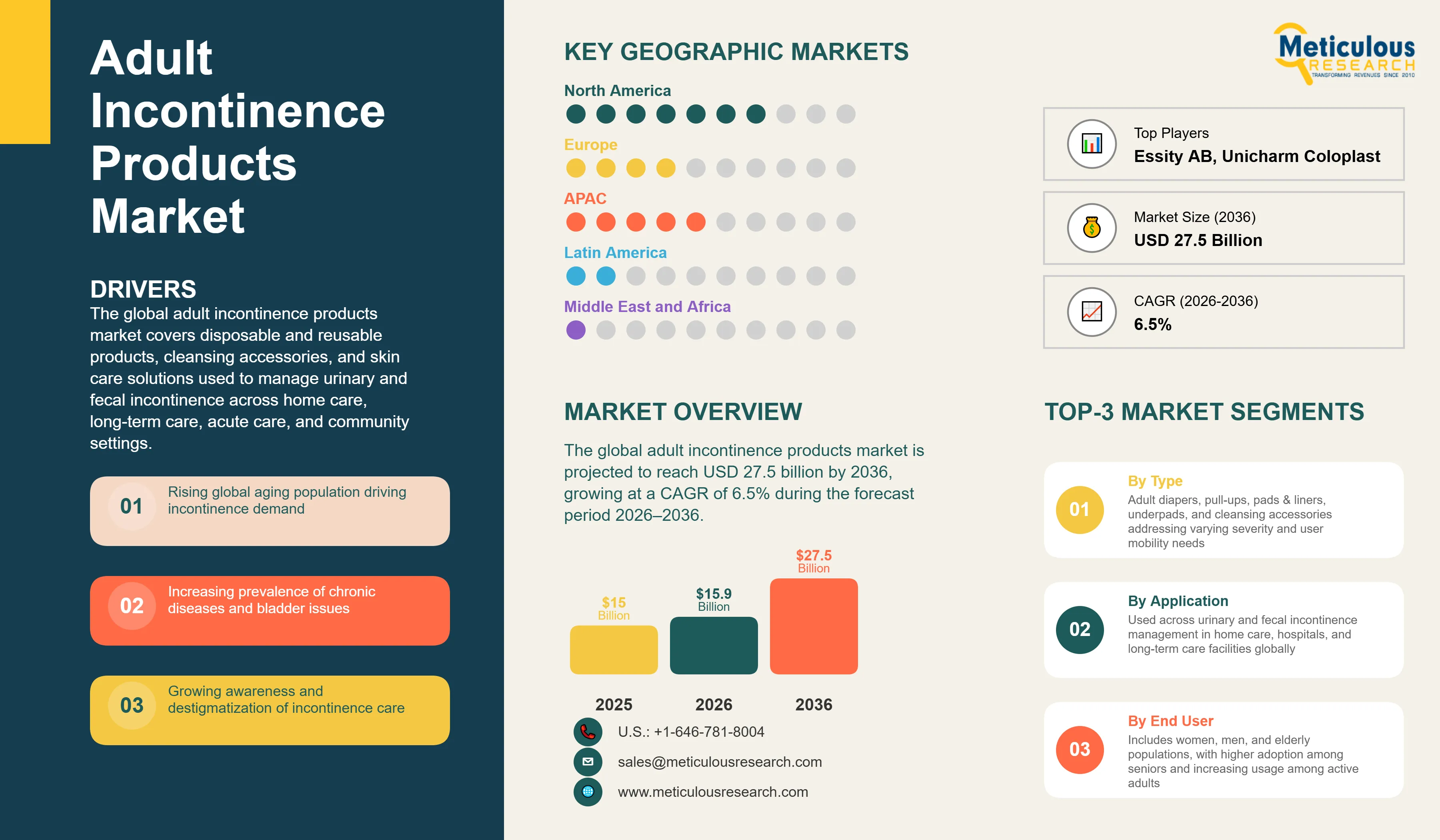

Adult Incontinence Products Market Size, Share & Trends Analysis by Product Type (Adult Diapers/Briefs, Protective Underwear/Pull-Ups, Pads & Liners, Underpads), Absorbency Level (Light, Moderate, Heavy/Overnight), Category (Disposable, Reusable), End User, Age Group, End Use (Home Care, Hospitals & ASCs, Long-Term Care Facilities), Distribution Channel, and Geography — Global Opportunity Analysis and Industry Forecast (2026–2036)

Report ID: MRHC - 1041927 Pages: 265 Apr-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global adult incontinence products market was valued at USD 15.0 billion in 2025. The market is projected to reach USD 27.5 billion by 2036 from an estimated USD 15.9 billion in 2026, growing at a CAGR of 6.5% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global adult incontinence products market covers disposable and reusable products, cleansing accessories, and skin care solutions used to manage urinary and fecal incontinence across home care, long-term care, acute care, and community settings. Core product categories include adult diapers and briefs, protective pull-up underwear, pads and liners for lighter incontinence, underpads and bed protection, and associated skincare and cleansing products. The market is characterized by strong structural demand rooted in global demographic aging, rising chronic disease prevalence, and growing consumer awareness and destigmatization of incontinence as a common and manageable health condition.

The key driver in the market is the increasing growth of the global elderly population. According to the United Nations World Population Prospects 2022, the proportion of people aged 65 and older is growing faster than any other age group globally, with 761 million people aged 65 and above as of 2025 (up from 703 million in 2023). Around 25-33% of individuals in this age group experience some form of incontinence, creating growing demand for absorbent hygiene products. The WHO's Integrated Care for Older People (ICOPE) guidelines document urinary incontinence prevalence ranging from 9% to 39% across different patient populations. In the U.S., 61 million Americans aged 65+ as of 2025 (U.S. Census Bureau) face incontinence affecting 25-33% of adults overall (~60-80 million total), representing expanding addressable market.

Beyond demographics, rising prevalence of chronic conditions that contribute to or exacerbate incontinence is driving the addressable market into younger age groups. Diabetes, obesity, neurological disorders including Parkinson's disease and multiple sclerosis, prostate-related issues in men, and the long-term effects of childbirth and menopause in women are all driving incontinence among the 40-64 age cohort at rates that justify dedicated product development and marketing toward this segment. The Alzheimer's Association reported approximately 7.2 million Americans aged 65 and older living with Alzheimer's disease as of 2025, a population with high incontinence prevalence (50-70% in late stages).

|

Parameters |

Details |

|---|---|

|

Market Size by 2036 |

USD 27.5 Billion |

|

Market Size in 2026 |

USD 15.9 Billion |

|

Market Size in 2025 |

USD 15.0 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 6.5% |

|

Dominating Product Type |

Adult Diapers / Briefs |

|

Fastest Growing Product Type |

Protective Underwear / Pull-Ups |

|

Dominating Absorbency Level |

Moderate / Heavy |

|

Fastest Growing Absorbency Level |

Light (Stress & Urgency Leakage) |

|

Dominating Category |

Disposable |

|

Fastest Growing Category |

Reusable / Washable |

|

Dominating End User |

Women |

|

Fastest Growing End User |

Women (Light Incontinence Segment) |

|

Dominating Age Group |

Seniors (65+) |

|

Fastest Growing Age Group |

Adults (18–64) |

|

Dominating End Use |

Home Care |

|

Fastest Growing End Use |

Home Care / OTC Retail |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Aging Demographics Driving Structural and Sustained Demand Growth Across All Geographies

The key trend shaping the global adult incontinence products market is the accelerating demographic aging of the global population, which is creating a multi-decade demand for the category. The United Nations World Population Prospects 2022 confirmed that the proportion of people aged 65 and older is growing faster than any other demographic globally, with this group reaching 761 million people as of 2025. The relationship between aging and incontinence is direct and physiologically well-established: weakening pelvic floor muscles, reduced bladder capacity, hormonal changes, and increasing prevalence of neurological conditions all contribute to rising incontinence rates with age.

Japan provides the most advanced illustration of this demographic dynamic, having reached a stage of demographic aging that other major markets are now approaching. Adult diapers have outsold baby diapers in Japan every year since 2011, showing the country's super-aged society in which over 36.2 million individuals are aged 65 and above as of 2023. Over 65% of nursing home residents in Japan use adult diapers regularly, representing a structurally captive institutional market. Institutional purchase volumes remain substantial globally, with healthcare facilities representing ~60% of total incontinence product end-user demand worldwide.

China is the most significant emerging volume growth market. With over 90 million adults affected by incontinence and a rapidly aging urban population, China’s incontinence product market is expected to grow at one of the highest CAGRs among major national markets globally. The combination of improving awareness, rising disposable income, expanding organized retail and e-commerce penetration, and international brands introducing affordable, innovative product options is rapidly increasing market participation. India is similarly positioned, with Tulips’ September 2025 entry into the adult diaper pants category indicating the growing commercialization of what was previously a highly underpenetrated market.

In the U.S., the aging of the Baby Boomer generation is creating a strong demand surge. With 59.3 million Americans aged 65 and older as of 2023, a number expected to reach 80 million by 2040, the demographic foundation of the U.S. market is expanding. Kimberly-Clark's USD 2 billion domestic manufacturing investment from 2025 to 2030, described as the company's largest expansion in 30+ years, indicates their confidence in this long-term demand trajectory. Institutional demand remains substantial, as evidenced by major healthcare systems and VA facilities serving millions of incontinence patients annually.

Premiumization and Destigmatization Expanding the Market Beyond the Traditional Institutional Segment

Another defining commercial trend driving the competitive landscape is the concurrent shift toward product premiumization and consumer destigmatization of incontinence, which is expanding the addressable market significantly beyond the traditional high-severity institutional segment into the broader active adult, younger consumer, and light-incontinence categories. This shift is transforming the category from a medically-oriented, often embarrassment-associated product area into a mainstream personal care segment accessible to a broader range of consumer demographics.

The leakproof apparel sub-segment is the most commercially dynamic expression of this trend. Essity estimates that leakproof apparel, products that look and feel like regular underwear while providing incontinence protection, is growing at more than 20% annually (based on Essity's market data, excluding Asia). Essity's acquisitions of Knix Wear and Modibodi extended the TENA brand ecosystem into premium, discreet washable underwear, while Kimberly-Clark's majority acquisition of Thinx and the associated Speax by Thinx incontinence underwear brand directly positions Kimberly-Clark in the intersection of menstrual and light incontinence care. AARP's 2024 Home and Community Preferences Survey confirms 75% of adults aged 50+ prefer aging in place, validating the commercial logic behind pull-up and underwear-format product innovation.

The destigmatization trend is also being actively driven by manufacturers through consumer-facing communication campaigns. Essity’s TENA SmartCare platform, its fully relaunched TENA Men brand, and its TENA Washable Absorbent Underwear launch under a ‘barrier to well-being’ communications strategy are all designed to shift consumer perception of incontinence from a source of embarrassment into a manageable, product-supported health condition. According to Essity, 77% of women with bladder weakness report discomfort, and the company’s product development pipeline is specifically oriented toward addressing skin irritation and comfort as primary consumer pain points. This consumer-centric, wellness-oriented approach is directly driving the expansion of the market into new consumer segments and age groups.

By Product Type: In 2026, Adult Diapers / Briefs to Dominate the Global Adult Incontinence Products Market

Based on product type, the adult incontinence products market is segmented into adult diapers and briefs, protective underwear and pull-ups, pads and liners, underpads and bed pads, skincare and cleansing accessories, and other products.

In 2026, adult diapers and briefs are expected to account for the largest share of the global adult incontinence products market. This segment serves the highest-severity incontinence needs across institutional care settings, nursing homes, hospitals, and assisted living facilities, where tab-style brief products are the standard of care for non-ambulatory or cognitively impaired patients. The product’s superior absorbency capacity, ease of application by caregivers without requiring the patient to stand, and compatibility with institutional waste management protocols underpin its market dominance.

However, protective underwear and pull-ups market is expected to grow at the fastest CAGR during the forecast period. The pull-up format’s resemblance to regular underwear, ease of self-application for ambulatory users, and contribution to user dignity and confidence are driving its adoption among active adults managing moderate incontinence.

By Absorbency Level: In 2026, Moderate / Heavy to Hold the Largest Share

Based on absorbency level, the adult incontinence products market is segmented into light (stress and urgency leakage), moderate, and heavy and overnight.

In 2026, the moderate-to-heavy absorbency segment is expected to account for the largest share of the global adult incontinence products market, at around 40-45% of revenue. This segment serves the core institutional and home care demand, including patients with established moderate-to-severe urinary or fecal incontinence who require products capable of reliable overnight protection and extended wear periods. Hospital patients, nursing home residents, and homebound elderly users represent the primary demand base for this segment.

However, the light absorbency segment for stress and urgency leakage is expected to register the fastest CAGR during the forecast period, driven by the growing population of active adults managing occasional or mild incontinence. Light incontinence is significantly more prevalent than severe cases but has historically been under-served by products specifically designed for this need.

By Category: In 2026, Disposable to Hold the Largest Share

Based on category, the adult incontinence products market is segmented into disposable and reusable and washable products.

In 2026, disposable products are expected to account for around 90% of the global adult incontinence product revenue, reflecting their dominance across institutional and home care settings. Disposable products’ superior performance in absorbency, odor control, and infection prevention, combined with the convenience of single-use application for both independent users and caregivers, underpins their strong commercial dominance.

Reusable and washable products market is expected to grow at the fastest CAGR during the forecast period, consistent with the leakproof apparel growth trend. Essity’s estimate of 20%+ annual growth for the leakproof apparel sub-segment, Kimberly-Clark’s Thinx acquisition, and the growing availability of washable pull-up style products from both established brands and direct-to-consumer entrants are collectively establishing reusables as the most dynamic growth sub-segment in the category. The TENA Stylish™ Washable Absorbent Underwear, launched as a consumer-facing product explicitly designed to look and feel like everyday lingerie, represents the premium end of this opportunity.

By End User: In 2026, Women to Hold the Largest Share

Based on end user, the adult incontinence products market is segmented into women and men.

In 2026, women are expected to account for the largest share of the global adult incontinence products market, at around 55% to 60% of revenue. Women experience incontinence at approximately twice the rate of men due to physiological factors including pregnancy, childbirth, and menopause, all of which weaken pelvic floor muscles and reduce bladder control. The National Association for Continence notes that women make up approximately 75% of incontinence sufferers in the U.S., indicating the gender-disproportionate prevalence of this condition.

The male incontinence segment is also growing, driven primarily by the rising awareness of prostate-related incontinence among aging men. Essity fully relaunched its TENA Men brand with product innovation, new packaging design, and a distinctive new visual identity, reflecting the commercial opportunity in a segment that was historically underserved by product design and consumer communication. A study conducted by Essity for TENA Men found that the percentage of male shoppers buying TENA Men themselves increased by 8%, indicating growing male consumer engagement with the category.

By Age Group: In 2026, Seniors (65+) to Hold the Largest Share

Based on age group, the adult incontinence products market is segmented into adults aged 18 to 64 and seniors aged 65 and above.

In 2026, seniors aged 65 and above are expected to account for around 70% of the global adult incontinence products market revenue, showing the dominant role of age-related physiological decline in driving product adoption. In the U.S., 61 million people are aged 65 and older as of 2025, with this population expected to expand to 80 million by 2040. The high prevalence of Alzheimer's disease, which affects approximately 7.2 million Americans aged 65 and older as of 2025, further increases incontinence product dependence in this age cohort.

The adult 18–64 segment is expected to grow at a faster CAGR during the forecast period, driven by rising awareness and product adoption among postpartum women, adults with obesity and diabetes-related incontinence, and younger adults managing overactive bladder conditions. The development of discreet, lifestyle-compatible products, including ultra-thin pads, leakproof underwear, and active-fit pull-ups, is specifically designed to capture this segment, which has historically been reluctant to adopt traditional incontinence products associated with severe disability or advanced old age.

Based on geography, the global adult incontinence products market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

In 2026, North America is expected to account for the largest share of the global adult incontinence products market. The U.S. dominates the regional market at approximately 90% of North American revenue, driven by a large and rapidly aging population, advanced healthcare infrastructure, high consumer awareness of incontinence management, and a culture increasingly accepting of adult hygiene products for active living. Kimberly-Clark’s USD 2 billion manufacturing investment plan (2025–2030), First Quality Enterprises’ South Carolina expansion in May 2025, and NorthShore Care Supply’s manufacturing expansion in May 2025 all reflect the industry’s confidence in strong U.S. demand growth.

Europe holds the second-largest regional share of the global adult incontinence products market. Germany, France, the U.K., and the Nordic countries are the largest national markets for adult incontinence products within Europe. European consumers are characterized by high awareness of incontinence management, strong healthcare reimbursement for institutional products, and growing demand for sustainable product formats. Essity (TENA), headquartered in Sweden, Ontex Group (Belgium/iD, Serenity), Paul Hartmann AG (Germany/MoliCare), and Abena (Denmark) are the dominant European brands, collectively shaping product innovation toward sustainability, skin health, and digital care management solutions. The regulatory environment for single-use plastics and strong ESG preferences in Europe are driving the shift toward biodegradable and reusable product formats ahead of other global markets.

Asia Pacific adult incontinence products market is expected to grow at the fastest CAGR during the forecast period, led by the demographic transformation across multiple major markets simultaneously. Japan’s adult diaper market and its institutional eldercare sector is among the most sophisticated globally in incontinence management. China, with over 90 million incontinence-affected adults and a rapidly aging urban population, represents the largest single volume growth opportunity in the region. Essity launched TENA ProSkin Pants Plus across multiple Asia-Pacific markets in January 2025, indicating the company’s strategic commitment to this region. In India, Tulips’ September 2025 entry into the adult diaper pants category marks an inflection point in a market that has historically been severely underpenetrated due to social stigma and limited product availability.

Latin America and the Middle East & Africa are smaller but growing markets. In Latin America, Brazil and Mexico are the largest national markets, with rising incontinence awareness, improving organized retail infrastructure, and a growing middle-class elderly population driving growing adoption. The Middle East & Africa market is characterized by strong healthcare spending in Gulf Cooperation Council countries, expanding elderly care infrastructure, and increasing import demand for international incontinence product brands.

The global adult incontinence products market is moderately consolidated, led by a small group of global hygiene and personal care companies with the manufacturing scale, distribution reach, and brand equity required to compete across institutional and consumer channels worldwide. Essity AB (Sweden/TENA) and Kimberly-Clark Corporation (U.S./Depend, Poise, Thinx) hold the leading competitive positions globally, supported by Procter & Gamble (Always Discreet), Unicharm Corporation (Japan/Lifree), Paul Hartmann AG (Germany/MoliCare), and Ontex Group (Belgium/iD). Key competitive dimensions include absorbency performance, skin-friendliness, discretion and aesthetics, sustainability credentials, digital care solutions, and institutional distribution relationships. Strategic priorities for market leaders include geographic expansion into Asia Pacific’s high-growth markets, acquisitions to enter the reusable and leakproof apparel segment, and product innovation toward sustainability, ultra-thin designs, and smart sensor-enabled products for institutional care.

Key players operating in the global adult incontinence products market include Essity AB (Sweden), Kimberly-Clark Corporation (U.S.), The Procter & Gamble Company (U.S.), Unicharm Corporation (Japan), Paul Hartmann AG (Germany), Ontex Group NV (Belgium), First Quality Enterprises, Inc. (U.S.), Abena Holding A/S (Denmark), Medline Industries LP (U.S.), Cardinal Health, Inc. (U.S.), Hollister Incorporated (U.S.), Hengan International Group (China), Coloplast A/S (Denmark), NorthShore Care Supply (U.S.), Nobel Hygiene Pvt. Ltd. (India), and Principle Business Enterprises, Inc. (U.S.), among others.

This report provides market size estimates and forecasts for each segment and sub-segment at the global, regional, and country levels. The report further offers an in-depth analysis of the latest industry trends, market dynamics, technological innovation, regulatory developments, and key strategic initiatives across each sub-segment for the forecast period 2026–2036.

For the purpose of this study, the global Adult Incontinence Products Market has been segmented based on product type, absorbency level, category, end user, age group, end use, distribution channel, and geography.

|

Segment |

Sub-Segments |

|---|---|

|

By Product Type |

Adult Diapers / Briefs (Disposable), Protective Underwear / Pull-Ups (Disposable), Pads & Liners, Underpads / Bed Pads, Skincare & Cleansing Accessories, Other Products |

|

By Absorbency Level |

Light (Stress & Urgency Leakage), Moderate, Heavy / Overnight |

|

By Category |

Disposable, Reusable / Washable |

|

By End User |

Women, Men |

|

By Age Group |

Adults (18–64), Seniors (65+) |

|

By End Use |

Home Care, Hospitals & Ambulatory Surgery Centers (ASCs), Long-Term Care Facilities (Nursing Homes, Assisted Living), Other End Uses |

|

By Distribution Channel |

Pharmacies & Drug Stores, Online / E-Commerce, Supermarkets & Hypermarkets, Medical Supply / Institutional, Other Channels |

|

By Geography |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

By Product Type (Revenue, USD Billion, 2026–2036)

By Absorbency Level (Revenue, USD Billion, 2026–2036)

By Category (Revenue, USD Billion, 2026–2036)

By End User (Revenue, USD Billion, 2026–2036)

By Age Group (Revenue, USD Billion, 2026–2036)

By End Use (Revenue, USD Billion, 2026–2036)

By Distribution Channel (Revenue, USD Billion, 2026–2036)

By Geography (Revenue, USD Billion, 2026–2036)

The global adult incontinence products market is expected to reach USD 27.5 billion by 2036 from an estimated USD 15.9 billion in 2026, at a CAGR of 6.5% during the forecast period 2026–2036.

In 2026, adult diapers and briefs are expected to hold the largest market share, driven by their dominance in institutional care settings including nursing homes, hospitals, and long-term care facilities, where tab-style brief products are the standard of care for patients with moderate-to-severe and fecal incontinence.

Protective underwear and pull-ups are expected to register the fastest CAGR during the forecast period 2026–2036, driven by strong consumer preference for products that support dignity, independent living, and active lifestyles.

In 2026, disposable products are expected to hold approximately 90% of global market revenue, driven by superior performance in absorbency, hygiene, and institutional compatibility. Reusable and washable products, including leakproof apparel, are expected to register the fastest CAGR, with Essity estimating the leakproof apparel sub-segment growing at more than 20% annually.

In 2026, pharmacies and drug stores are expected to hold the largest distribution channel share, supported by healthcare professional guidance in product selection for moderate-to-severe incontinence management. Online and e-commerce channels are expected to grow at the fastest CAGR, driven by consumer preference for discreet home delivery and subscription-based purchasing.

The growth of this market is primarily driven by the global aging demographic, with over 761 million people aged 65 and above globally as of 2023 per UN data; the high prevalence of urinary incontinence in the elderly, documented by WHO ICOPE guidelines at 9.9% to 36.1% across patient populations; rising awareness and destigmatization expanding the market to active adults and younger age groups; premiumization trends toward discreet pull-up formats and leakproof apparel; Kimberly-Clark’s USD 2 billion U.S. manufacturing investment (2025–2030); First Quality Enterprises’ February 2025 acquisition of Henkel’s Retailer Brands North America business; and rapid Asia Pacific growth, particularly in China and India.

Key players in the global adult incontinence products market include Essity AB (Sweden), Kimberly-Clark Corporation (U.S.), The Procter & Gamble Company (U.S.), Unicharm Corporation (Japan), Paul Hartmann AG (Germany), Ontex Group NV (Belgium), First Quality Enterprises, Inc. (U.S.), Abena Holding A/S (Denmark), Medline Industries LP (U.S.), Cardinal Health, Inc. (U.S.), Hollister Incorporated (U.S.), Hengan International Group (China), Coloplast A/S (Denmark), NorthShore Care Supply (U.S.), and Nobel Hygiene Pvt. Ltd. (India).

Asia Pacific is expected to register the highest growth rate in the global adult incontinence products market during the forecast period 2026–2036, driven by Japan’s super-aged society, China’s over 90 million incontinence-affected adults, India’s accelerating market entry including Tulips’ September 2025 adult diaper pants launch, and Essity’s January 2025 TENA ProSkin Pants Plus launch across multiple Asia-Pacific markets.

Published Date: Apr-2026

Published Date: Jan-2025

Published Date: May-2023

Published Date: Aug-2023

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates