Resources

About Us

Artificial Intelligence in Genomics Market by Offering (Software, Services), Functionality (Genome Sequencing, Gene Editing, Genome Assembly & Annotation, Pharmacogenomics), Application (Drug Discovery & Development, Precision Medicine, Diagnostics, Agricultural Genomics), Delivery Mode (On-premises, Cloud & Web-Based), and End User – Global Forecast to 2036

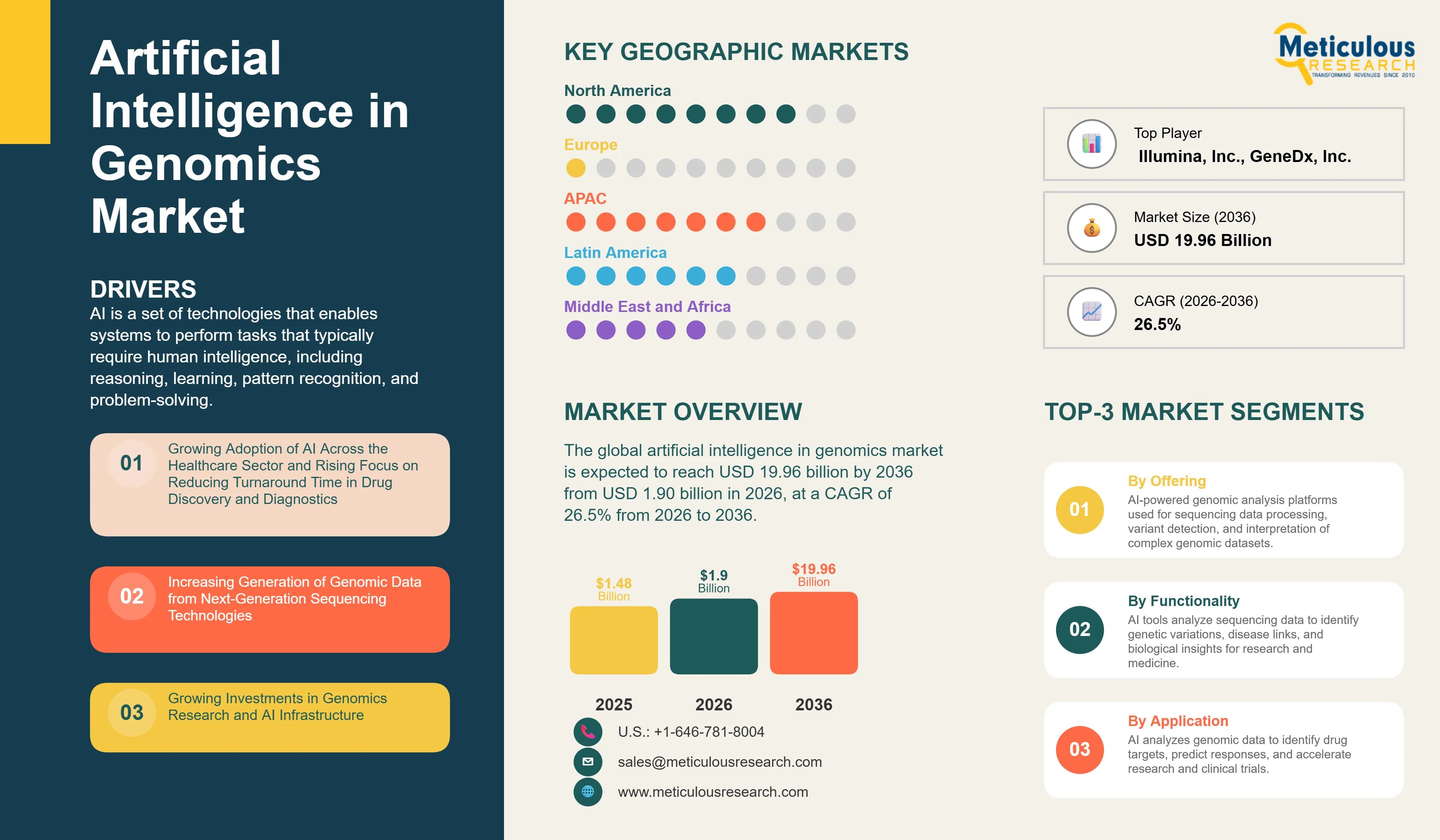

Report ID: MRHC - 104660 Pages: 170 Feb-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 48 Hours Download Free Sample ReportThe global artificial intelligence in genomics market was valued at USD 1.48 billion in 2025. This market is expected to reach USD 19.96 billion by 2036 from USD 1.90 billion in 2026, at a CAGR of 26.5% from 2026 to 2036.

AI is a set of technologies that enables systems to perform tasks that typically require human intelligence, including reasoning, learning, pattern recognition, and problem-solving. In genomics, AI includes a range of software tools and services built on machine learning, deep learning, and natural language processing algorithms that are applied to the analysis, interpretation, and application of genomic data. The integration of AI into genomics enables the processing of large-scale genomic datasets that are beyond the capacity of conventional analytical methods, supporting applications in drug discovery and development, precision medicine, diagnostics, and agricultural genomics.

The growing adoption of AI across the healthcare and life sciences sectors, the rising focus on reducing the time and cost of drug discovery and development, the increasing generation of genomic data from next-generation sequencing platforms, and the growing demand for personalized and precision medicine are the key factors driving the growth of the artificial intelligence in genomics market. Furthermore, increasing public and private investments in genomics research and AI infrastructure, the proliferation of cloud-based genomics platforms, and the growing adoption of AI in clinical diagnostics and rare disease identification are expected to offer significant opportunities for players operating in this market.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Artificial intelligence in genomics refers to the application of AI technologies, including machine learning, deep learning, and natural language processing, to the analysis, interpretation, and utilization of genomic data. AI in genomics includes a set of software tools and services offered on-premises or through cloud and web-based delivery modes. The integration of AI in genomics has played a significant role across functionalities, including genome sequencing, genome editing, genome assembly and annotation, and pharmacogenomics. The adoption of AI has expanded genomic applications across drug discovery and development, precision medicine, diagnostics, and agricultural genomics.

The increasing volume of genomic data generated by next-generation sequencing technologies, combined with the limitations of traditional bioinformatics tools in processing and interpreting this data at scale, is a fundamental driver of AI adoption in genomics. Illumina, Inc., the global leader in DNA sequencing, reported revenue of around USD 4.33 billion for fiscal year 2024 and is actively integrating AI-driven software tools including its DRAGEN bioinformatics platform into its sequencing workflows to enable faster and more accurate genomic analysis. In January 2025, NVIDIA Corporation and Illumina announced a strategic partnership at the 43rd Annual J.P. Morgan Healthcare Conference to implement AI technologies in genomics to analyze and interpret multi-omics data in clinical research and drug discovery.

The market is further driven by the rapid growth of AI-driven precision medicine companies. Tempus AI, Inc. reported revenue of USD 693 million for fiscal year 2024, representing 30% year-over-year growth, and increased its revenue guidance to approximately USD 1.24 billion for full year 2025 following its acquisition of Ambry Genetics, which closed on February 3, 2025.

GeneDx, Inc., a leader in AI-enabled whole exome and whole genome sequencing, reported preliminary full year 2024 revenues of at least USD 299 million, reflecting 54% year-over-year growth in total revenue and 88% year-over-year growth in exome and genome test revenue.

In April 2025, GeneDx announced the acquisition of Fabric Genomics to enable decentralized AI-powered genomic interpretation at a global scale.

These developments reflect the rapid growth and increasing commercial maturity of the artificial intelligence in genomics market, which is projected to reach USD 19.96 billion by 2036, growing at a CAGR of 26.5% from 2026 to 2036.

Growing Integration of Large Language Models and Generative AI in Genomic Data Analysis

One of the significant trends driving the AI in genomics market is the growing application of large language models and generative AI to genomic data analysis, biological sequence interpretation, and drug target identification. AI models trained on large genomic and proteomic datasets are enabling researchers to predict protein structures, identify disease-associated genetic variants, and generate hypotheses for new therapeutic targets at a speed and scale that was not previously possible with conventional bioinformatics approaches. In January 2025, NVIDIA Corporation and Illumina announced a strategic partnership at the J.P. Morgan Healthcare Conference to integrate NVIDIA's accelerated computing and AI toolsets with Illumina's DRAGEN bioinformatics platform and Connected Analytics ecosystem, enabling faster multi-omics data analysis and the development of biology foundation models for drug discovery and precision health.

Further advancing this trend, in November 2025, Arc Institute, Icahn School of Medicine at Mount Sinai, and NVIDIA launched a three-year collaboration to develop a genomic large language model capable of decoding regulatory elements across the previously unexplored 98% of the human genome, with the goal of linking genetic variation to disease risk and therapeutic response. Additionally, in February 2025, a multi-institutional team co-led by Stanford University and NVIDIA introduced Evo 2, an open-source generative AI model trained on nearly 9 trillion nucleotides spanning all domains of life, which can predict protein function, design novel genetic sequences, and distinguish pathogenic from benign variants in minutes rather than years.

This trend is creating new product development opportunities for both established technology companies and specialized AI genomics startups. Major technology companies including Microsoft Corporation and Google LLC are expanding their cloud-based genomics AI platforms, while specialized companies including Deep Genomics, Inc. and BenevolentAI Limited are developing proprietary AI engines for genomic sequence interpretation and therapeutic target identification. The growing accessibility of foundation models and open-source AI frameworks is also enabling academic research institutes and smaller biotech companies to adopt AI-driven genomics tools, broadening the end-user base for this market.

Expansion of AI-Driven Genomic Diagnostics and Rare Disease Identification

The growing application of AI in clinical genomic diagnostics, particularly for rare disease identification and neonatal care, is a significant trend driving demand for AI in genomics software and services. Whole exome sequencing and whole genome sequencing interpreted by AI algorithms are increasingly being adopted in neonatal intensive care units and pediatric settings to accelerate the diagnosis of rare genetic diseases, reducing the time to diagnosis from weeks to days or hours. GeneDx reported that as of 2024, 14 U.S. state Medicaid programs had expanded coverage of rapid genome sequencing in neonatal intensive care units, reflecting growing clinical and reimbursement acceptance of AI-enabled genomic diagnostics.

This trend is supported by the growing availability of large, curated rare disease genomic datasets that are improving the accuracy of AI diagnostic algorithms. GeneDx has sequenced over 750,000 clinical exomes and genomes as of 2024, building one of the world’s largest rare disease genomic datasets. The growing clinical evidence base for AI-driven genomic diagnostics and the expansion of reimbursement coverage are increasing the adoption of these tools across hospitals, clinical laboratories, and healthcare systems, particularly in North America and Europe.

|

Report Coverage |

Details |

|

Market Size by 2036 |

USD 19.96 Billion |

|

Market Size in 2025 |

USD 1.48 Billion |

|

Market Size in 2026 |

USD 1.90 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 26.5% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

By Offering: Software, Services |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Why Does the Software Segment Dominate the AI in Genomics Market?

Based on offering, in 2026, the software segment is expected to account for the largest share of the artificial intelligence in genomics market. The large market share of this segment is attributed to the recurring revenue model of AI genomics software, the growing adoption of subscription-based and licensing-based software models by pharmaceutical companies, academic research institutes, and clinical laboratories, and the essential role of AI software in processing and interpreting the large volumes of genomic data generated by next-generation sequencing platforms. Software is used to capture, process, and analyze data from sequencing instruments and apply AI algorithms to generate clinically or scientifically actionable outputs, contributing to a steady and growing stream of revenue.

The services segment is expected to witness the fastest CAGR during the forecast period. The faster growth of the services segment is driven by the growing demand for genomic data analysis and interpretation services from pharmaceutical and biopharmaceutical companies that do not have in-house AI genomics capabilities, the increasing adoption of contract data analytics and bioinformatics services by academic and research institutes, and the growing market for cloud-based genomics data management and analysis services.

Why Does the Genome Sequencing Segment Dominate the Artificial Intelligence in Genomics Market?

Based on functionality, in 2026, the genome sequencing segment is expected to account for the largest share of the AI in genomics market. Genome sequencing supported by AI algorithms helps in the drug discovery process by accurately characterizing diseases and identifying genetic variants associated with disease susceptibility and drug response. AI-driven genome sequencing helps researchers and medical experts to understand genetic variants and to identify the origin, behavior, and structure of pathogens and disease-causing mutations, which supports the development of vaccines, antiviral drugs, and targeted preventive strategies. The growing clinical adoption of whole exome and whole genome sequencing for rare disease diagnosis, cancer profiling, and newborn screening is sustaining strong demand for AI-enabled sequencing analysis tools.

The pharmacogenomics segment is expected to witness significant CAGR during the forecast period. The growth of this segment is driven by the increasing application of AI in analyzing the relationship between an individual’s genome and their response to drugs, supporting the development of more targeted and effective drug therapies and reducing the risk of adverse drug reactions. Growing pharmaceutical industry investment in pharmacogenomics-guided drug development and the increasing adoption of pharmacogenomics testing in clinical practice are supporting demand for AI tools in this area.

Why Does the Drug Discovery & Development Segment Dominate the Artificial Intelligence in Genomics Market?

Based on application, in 2026, the drug discovery and development segment is expected to account for the largest share of the AI in genomics market. The large share of this segment is mainly attributed to the growing demand for innovative and new therapies for infectious and chronic diseases, the growing emphasis on quickly developing new therapies, and the significant time and cost savings that AI can deliver in the drug discovery process. The integration of AI in genomics accelerates target identification, lead optimization, and clinical trial design, reducing the turnaround time and cost of bringing new drugs to market and offering significant opportunities for pharmaceutical and biopharmaceutical companies.

The precision medicine segment is expected to witness the fastest CAGR during the forecast period. The faster growth of the precision medicine segment is driven by the growing adoption of genomic data in clinical decision-making, the increasing availability of AI tools that can analyze multi-omics datasets to identify patient subgroups for targeted therapies, the commercial success of AI-driven precision medicine platforms such as Tempus AI and GeneDx, and the growing reimbursement coverage for genomic testing and precision medicine applications in major markets.

Why is the Cloud & Web-Based Segment Expected to Grow at the Fastest CAGR?

Based on delivery mode, the cloud & web-based segment is projected to register the fastest CAGR in the AI in genomics market during the forecast period of 2026 to 2036. The growing adoption of cloud and web-based platforms and the advantages offered by cloud-based models pertaining to security and scalability, high-capacity data storage, easy accessibility, and cost-effectiveness are increasing the preference for cloud-based platforms among pharmaceutical companies, academic research institutes, and clinical laboratories. Cloud-based genomics platforms enable real-time data analysis, collaboration across geographically distributed research teams, and the scalable processing of large genomic datasets without requiring significant on-premises infrastructure investment.

Why Do Pharmaceutical & Biopharmaceutical Companies Lead the Artificial Intelligence in Genomics Market?

Based on end user, in 2026, the pharmaceutical and biopharmaceutical companies segment is expected to account for the largest share of the artificial intelligence in genomics market. Pharmaceutical and biopharmaceutical companies are using AI in genomics for drug discovery, development, and precision medicine applications. These companies face constant pressure to reduce the operational costs of drug discovery and development and to bring therapies to market more quickly. The increasing burden of chronic and infectious diseases is intensifying the need for new and more targeted therapies, driving pharmaceutical and biopharmaceutical companies to integrate AI in genomics for drug discovery, target identification, patient stratification, and clinical trial optimization.

U.S. Artificial Intelligence in Genomics Market Size and Growth 2026 to 2036

The U.S. artificial intelligence in genomics market is projected to grow at a significant CAGR from 2026 to 2036, supported by a well-established AI and genomics research infrastructure, the presence of leading market participants including Illumina, Inc., Tempus AI, Inc., GeneDx, Inc., NVIDIA Corporation, and Microsoft Corporation, growing adoption of AI in clinical genomic diagnostics, and increasing public funding for genomics research through institutions such as the National Institutes of Health.

How is North America Maintaining Dominance in the Artificial Intelligence in Genomics Market?

Based on geography, in 2026, North America is expected to account for the largest share of the artificial intelligence in genomics market. The major market share of North America is attributed to the growing adoption of AI in genomics across the healthcare and life sciences sectors, the presence of a large number of leading pharmaceutical and biopharmaceutical companies and academic research institutes, significant private and public investment in genomics research and AI infrastructure, and a well-developed regulatory framework that supports clinical adoption of AI-enabled genomic diagnostics and precision medicine tools. The U.S. leads the North American market, with leading AI genomics companies including Tempus AI, GeneDx, DNAnexus, Inc., and Freenome Holdings, Inc. generating significant and growing revenues from AI-driven genomics software, services, and diagnostics platforms.

Which Factors Support the Growth of the Asia-Pacific Artificial Intelligence in Genomics Market?

Asia-Pacific is expected to register the fastest growth rate during the forecast period of 2026 to 2036. The growth in this market is attributed to factors such as the growing integration of AI in genomics across countries including China, India, Singapore, and South Korea, increasing research initiatives in genomics, and developing infrastructure for genomic research and AI. Additionally, emerging startups and increasing funding for genomics and AI, and the growing focus of governments in the region on precision medicine and genomics-driven healthcare contribute to market growth in this region.

China is a particularly significant growth market, with BGI Genomics Co., Ltd. operating as one of the world’s largest genomics research and services organizations and the Chinese government investing in national genomics initiatives. India is emerging as a growing market for AI in genomics, supported by increasing genomics research activity, a large and growing pharmaceutical and biotechnology industry, and government-supported precision medicine programs. Japan and South Korea are also growing AI genomics markets, supported by strong research institutions and increasing clinical adoption of genomic sequencing and AI-based diagnostic tools.

The report includes a competitive landscape based on an extensive assessment of the key strategic developments adopted by leading market participants in the artificial intelligence in genomics market between 2023 and 2026. The key players profiled in the global artificial intelligence in genomics market report are Microsoft Corporation (U.S.), NVIDIA Corporation (U.S.), Illumina, Inc. (U.S.), Tempus AI, Inc. (U.S.), GeneDx, Inc. (U.S.), Deep Genomics, Inc. (Canada), DNAnexus, Inc. (U.S.), SOPHiA GENETICS SA (Switzerland), BenevolentAI Limited (U.K.), Freenome Holdings, Inc. (U.S.), BGI Genomics Co., Ltd. (China), Fabric Genomics, Inc. (U.S.) [acquired by GeneDx in April 2025], Predictive Oncology Inc. (U.S.), and Congenica Ltd. (U.K.) among others.

Artificial Intelligence in Genomics Market, by Offering

Artificial Intelligence in Genomics Market, by Functionality

Artificial Intelligence in Genomics Market, by Application

Artificial Intelligence in Genomics Market, by Delivery Mode

Artificial Intelligence in Genomics Market, by End User

Artificial Intelligence in Genomics Market, by Geography

This study offers a detailed assessment of the artificial intelligence in genomics market, including market sizes and forecasts for various segmentations such as offering, functionality, application, delivery mode, and end user. The study also involves the value analysis of various segments of the artificial intelligence in genomics market at regional and country levels.

The global artificial intelligence in genomics market is projected to reach USD 19.96 billion by 2036, at a CAGR of 26.5% from 2026 to 2036.

The software segment is estimated to hold the largest share in 2026. Recurring revenue from subscription-based and licensing models offered by AI genomics software companies contributes to the largest market share.

The cloud & web-based segment is expected to grow at the highest CAGR over the forecast period. The growing preference for cloud-based and web-based platforms owing to their advantages in security, scalability, high-capacity data storage, easy accessibility, and cost-effectiveness is a key factor for this segment’s growth.

The growth of this market is attributed to the increasing use of AI in healthcare and genomics, growing investments in genomics research and AI infrastructure, and a rising focus on reducing turnaround time in drug discovery and diagnostics. Moreover, the growing trend toward personalized and precision medicine and the expansion of AI-driven clinical genomic diagnostics offer significant opportunities for market growth.

The key players operating in the global artificial intelligence in genomics market are Microsoft Corporation (U.S.), NVIDIA Corporation (U.S.), Illumina, Inc. (U.S.), Tempus AI, Inc. (U.S.), GeneDx, Inc. (U.S.), Deep Genomics, Inc. (Canada), DNAnexus, Inc. (U.S.), SOPHiA GENETICS SA (Switzerland), BenevolentAI Limited (U.K.), Freenome Holdings, Inc. (U.S.), BGI Genomics Co., Ltd. (China), Predictive Oncology Inc. (U.S.), and Congenica Ltd. (U.K.) among others.

Emerging economies including China and India are projected to offer significant growth opportunities to market players due to the growing integration of AI in genomics, increasing research initiatives, and developing infrastructure for genomic research and AI in these countries.

Published Date: Oct-2013

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates