Resources

About Us

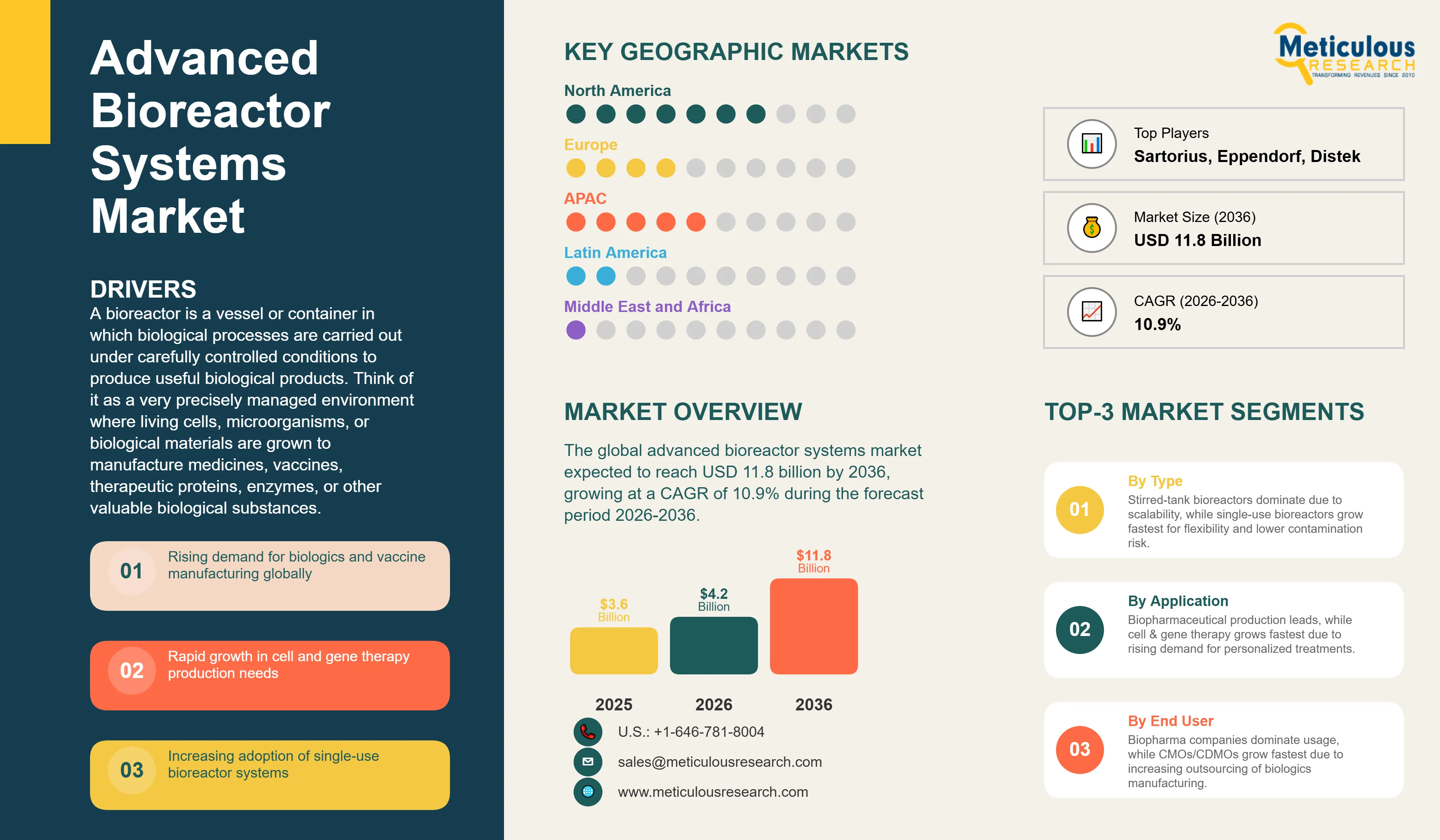

Advanced Bioreactor Systems Market Size, Share & Trends Analysis by Bioreactor Type (Stirred-Tank, Single-Use/Disposable), Scale, Application, End User, Mode of Operation, and Control Type - Global Opportunity Analysis & Industry Forecast (2026-2036)

Report ID: MRHC - 1041929 Pages: 312 Apr-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global advanced bioreactor systems market was valued at USD 3.6 billion in 2025. This market is expected to reach USD 11.8 billion by 2036 from an estimated USD 4.2 billion in 2026, growing at a CAGR of 10.9% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

A bioreactor is a vessel or container in which biological processes are carried out under carefully controlled conditions to produce useful biological products. Think of it as a very precisely managed environment where living cells, microorganisms, or biological materials are grown to manufacture medicines, vaccines, therapeutic proteins, enzymes, or other valuable biological substances. Advanced bioreactor systems go beyond simple fermentation tanks to include sophisticated monitoring, control, and automation capabilities that allow manufacturers to maintain the exact conditions of temperature, oxygen level, pH, and nutrient supply that biological production processes require. The output of these systems can be a monoclonal antibody used to treat cancer, a vaccine antigen, a therapeutic protein for a rare disease, or a living cell therapy product manufactured for a specific patient.

The market is growing strongly because the pharmaceutical industry has fundamentally shifted toward biological medicines over the past two decades. Monoclonal antibodies, the treatment of choice for many cancers, autoimmune diseases, and inflammatory conditions, are manufactured almost entirely using bioreactor-based cell culture processes. The global market for monoclonal antibody drugs alone exceeds USD 200 billion annually and is growing rapidly, driving proportional demand for the bioreactor systems used to produce them. The COVID-19 pandemic demonstrated the critical importance of large-scale bioreactor capacity by revealing that messenger RNA vaccine manufacturing required very rapid scale-up of bioprocessing infrastructure, and this experience has driven governments and pharmaceutical companies globally to invest in expanding domestic biomanufacturing capacity in a way that is sustaining growth well beyond the pandemic period.

Two particularly significant opportunities are driving additional market growth beyond the established monoclonal antibody and vaccine applications. The emerging cell and gene therapy sector, which includes CAR-T cell therapies that reprogram a patient's own immune cells to fight cancer and viral vector gene therapy products that deliver corrective genetic material to treat previously untreatable inherited diseases, requires bioreactor systems specifically designed for the very small batch sizes and specialized cell culture conditions of these personalized therapies. This is a fast-growing and high-value application that is creating demand for new types of small-scale, highly controlled bioreactor systems. In addition, the transition from batch and fed-batch bioprocessing to continuous bioprocessing, where cells are kept growing and producing product continuously rather than in discrete batches, has the potential to dramatically reduce manufacturing costs and increase productivity, creating strong demand for perfusion bioreactors and the integrated process control platforms that continuous manufacturing requires.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 11.8 Billion |

|

Market Size in 2026 |

USD 4.2 Billion |

|

Market Size in 2025 |

USD 3.6 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 10.9% |

|

Dominating Bioreactor Type |

Stirred-Tank Bioreactors |

|

Fastest Growing Bioreactor Type |

Single-Use (Disposable) Bioreactors |

|

Dominating Scale |

Commercial-Scale Bioreactors |

|

Fastest Growing Scale |

Pilot-Scale Bioreactors |

|

Dominating Application |

Biopharmaceutical Production |

|

Fastest Growing Application |

Cell and Gene Therapy |

|

Dominating End User |

Biopharmaceutical Companies |

|

Fastest Growing End User |

Contract Manufacturing Organizations (CMOs/CDMOs) |

|

Dominating Mode of Operation |

Fed-Batch Processing |

|

Fastest Growing Mode of Operation |

Continuous Processing (Perfusion) |

|

Dominating Control Type |

Automated Systems |

|

Fastest Growing Control Type |

AI-Driven Smart Bioreactors |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Single-Use Bioreactors Becoming the Standard for Modern Biomanufacturing

The most significant operational trend reshaping the bioreactor systems market is the widespread adoption of single-use, also called disposable, bioreactor systems that use pre-sterilized plastic bags and components for each production run rather than the large fixed stainless steel vessels with complex cleaning and sterilization cycles that traditional biomanufacturing relied on. A single-use bioreactor system eliminates the need to clean and sterilize the vessel between batches, which typically requires hours of hot water flushing, chemical cleaning agents, steam sterilization, and subsequent validation that the cleaning was effective. For a pharmaceutical manufacturer running many different products or needing to switch quickly between production campaigns, eliminating cleaning cycles saves significant time, reduces the risk of cross-contamination between products, and greatly simplifies the manufacturing process. Single-use systems are also faster and cheaper to set up for new products because there is no need to qualify and validate fixed stainless steel equipment for each new production process.

Sartorius, Thermo Fisher Scientific through its HyClone and Thermo Scientific brands, and Cytiva formerly GE Healthcare Life Sciences have all built large product portfolios around single-use bioreactor systems and have seen strong growth as pharmaceutical manufacturers shifted toward this technology. The COVID-19 vaccine manufacturing response, where single-use systems allowed multiple manufacturers to rapidly set up production capacity for new products without the long lead times required for stainless steel bioreactor installation, demonstrated the operational advantages of single-use technology in a visible and commercially important way that has further accelerated its adoption. Single-use systems are now the standard technology choice for new biopharmaceutical manufacturing facilities and for clinical manufacturing applications where flexibility and speed to market are priorities.

Cell and Gene Therapy Creating an Entirely New Bioreactor Product Category

The emergence of cell and gene therapy as a major new area of medicine is creating demand for a completely different category of bioreactor systems than those used for conventional monoclonal antibody or vaccine manufacturing. Traditional biopharmaceuticals are produced in very large batches, where a single production run in a 2,000-liter or 20,000-liter bioreactor produces enough product to treat many thousands of patients. Cell and gene therapies by contrast are often manufactured in very small batches, sometimes in quantities intended for a single specific patient, using the patient's own cells that have been collected, processed in a bioreactor to expand their numbers or modify their genetic instructions, and then returned to the patient. A CAR-T cell therapy manufacturing process might involve growing cells from a specific patient in a bioreactor with a working volume of just a few liters over a period of days before the finished product is shipped back to the treating hospital for infusion into that patient.

This very different manufacturing model requires bioreactor systems that are quite different from conventional large-scale bioreactors: small working volumes, very precise environmental control, automated cell handling to minimize the manual steps that could introduce variability or contamination into patient-specific products, and the ability to run many small batches simultaneously to serve multiple patients at the same time. Companies including PBS Biotech with its vertical wheel bioreactor technology, Miltenyi Biotec with its CliniMACS Prodigy platform, and several other specialist suppliers are developing bioreactor systems specifically designed for cell therapy manufacturing. As the cell therapy market grows rapidly with multiple approved CAR-T products already generating substantial revenues and a large pipeline of new cell and gene therapy candidates in clinical development, the demand for specialized small-scale cell therapy bioreactor systems is one of the fastest-growing segments in the bioreactor market.

Continuous Bioprocessing and Digitalization Transforming Manufacturing Efficiency

A major strategic direction for the biopharmaceutical manufacturing industry is the transition from traditional batch bioprocessing, where cells are grown in a bioreactor for a fixed period and then the entire contents are harvested, to continuous bioprocessing where cells are kept growing indefinitely while product is continuously removed and replaced with fresh nutrients. Continuous bioprocessing, also called perfusion culture, allows a bioreactor to produce product around the clock rather than only during the final phases of a batch culture, which can multiply productivity per unit of bioreactor volume by three to five times compared with fed-batch processes. For expensive biologics where the bioreactor and downstream processing costs are a major component of total manufacturing cost, this productivity improvement translates directly into lower manufacturing costs and potentially lower drug prices.

The integration of digital technologies including advanced sensors, real-time process analytics, and AI-based process control with continuous bioprocessing systems is creating intelligent bioprocessing platforms that can monitor hundreds of process parameters simultaneously, detect deviations from optimal conditions before they affect product quality, and automatically adjust operating conditions to maintain the biological process within defined parameters. Sartorius's Biostat STR and Ambr platforms, Thermo Fisher's HyPerforma bioreactors, and Cytiva's ReadyToProcess Wave systems all incorporate increasingly sophisticated digital monitoring and control capabilities. The FDA's Process Analytical Technology guidance and the European Medicines Agency's continuous manufacturing framework are providing regulatory encouragement for the adoption of these advanced manufacturing approaches, which are expected to progressively transform biopharmaceutical manufacturing toward more productive, more predictable, and more affordable processes through the forecast period.

Increasing Demand for Biopharmaceuticals and Vaccines

The primary driver of the advanced bioreactor equipment market is the sustained and rapid growth of the global biopharmaceuticals market, which has become the largest and fastest-growing segment of the pharmaceutical industry over the past two decades. Monoclonal antibodies, which are manufactured using bioreactor-based mammalian cell culture processes, generated over USD 200 billion in global sales and represent the majority of the world's top-selling drugs, including blockbuster cancer treatments, autoimmune disease therapies, and inflammatory condition treatments that each individually generate billions of dollars in annual revenue. Every gram of monoclonal antibody product requires dedicated bioreactor capacity to manufacture, and the continued growth of the global monoclonal antibody market at double-digit annual rates creates proportional demand growth for the bioreactor systems used to produce them. The global COVID-19 vaccination campaign also demonstrated that rapid large-scale vaccine manufacturing requires substantial bioreactor capacity, and the resulting investment by governments and pharmaceutical companies in domestic vaccine manufacturing infrastructure has created lasting new demand for bioreactor systems at manufacturing sites around the world.

Growth in Cell and Gene Therapy Manufacturing

The rapid commercial development of cell and gene therapies represents the most significant new application driving bioreactor market growth, as these highly specialized biological medicines require dedicated bioreactor systems that are quite different from conventional pharmaceutical bioreactors and command premium pricing. The six approved CAR-T cell therapy products including Kymriah, Yescarta, Breyanzi, Abecma, Carvykti, and Tecartus collectively generated over USD 2 billion in annual revenues and are growing rapidly as clinical indications expand and as more hospitals gain experience with these treatments. The large pipeline of cell and gene therapy candidates in clinical development, with hundreds of programs across CAR-T, TCR, NK cell, and various gene therapy modalities, represents a growing wave of future demand for specialized bioreactor systems as these programs progress through clinical development and toward commercial manufacturing. The manufacturing complexity of cell and gene therapies, combined with the high commercial value of these treatments, makes this the highest-value and fastest-growing application segment in the bioreactor market.

Continuous Bioprocessing Adoption

The transition from conventional batch and fed-batch bioprocessing to continuous perfusion bioprocessing represents a very large commercial opportunity for bioreactor manufacturers that can provide the specialized perfusion bioreactor systems, cell retention devices, and integrated process control platforms that continuous manufacturing requires. Continuous bioprocessing can produce the same amount of drug product in a smaller bioreactor operating continuously than a much larger batch bioreactor running intermittently, reducing the capital cost of new manufacturing facilities significantly. For established pharmaceutical manufacturers building new production capacity or upgrading existing facilities, the ability to achieve higher productivity in a smaller footprint through continuous bioprocessing justifies the investment in new perfusion bioreactor systems and continuous manufacturing technology. Sartorius, Cytiva, and Repligen are the leading suppliers in the continuous bioprocessing equipment category, and the growing number of pharmaceutical companies running continuous manufacturing development programs creates a strong and growing commercial pipeline for continuous bioprocessing equipment and services.

Integration with Automation and AI-Based Process Control

The integration of artificial intelligence and machine learning with bioreactor control systems is creating a new generation of smart bioreactor platforms that can monitor biological processes with greater sensitivity and sophistication than human operators, detect developing process deviations before they affect product quality, and automatically optimize operating conditions for maximum yield and quality. Traditional bioreactor control systems maintain individual parameters like temperature, pH, and dissolved oxygen within set ranges but do not integrate information from multiple parameters to build a dynamic model of the biological process. AI-based process control systems can analyze the patterns across dozens of simultaneously measured process variables, develop a predictive model of how the biological process is progressing, and make proactive adjustments to prevent problems rather than reacting to them after they have occurred. For pharmaceutical manufacturers, the value of AI-based process control is that it reduces the variability between production batches, which is critical for regulatory approval and for maintaining consistent drug quality. Sartorius has invested significantly in digital bioprocessing through its acquisition of Umetrics and its Ambr automation platform, Thermo Fisher through its DeltaV-based bioreactor control systems, and Cytiva through its BioProcess Intelligence platform.

By Bioreactor Type: In 2026, Stirred-Tank Bioreactors to Dominate

Based on bioreactor type, the global advanced bioreactors market is segmented into stirred-tank bioreactors, single-use bioreactors, perfusion bioreactors, airlift bioreactors, packed bed bioreactors, fluidized bed bioreactors, and hollow fiber bioreactors. In 2026, the stirred-tank bioreactors segment is expected to account for the largest share of the global advanced bioreactor systems market. Stirred-tank bioreactors are the most widely used configuration in biopharmaceutical manufacturing, using mechanical agitation from an impeller to mix cells, nutrients, and gases within the bioreactor vessel. This is the established and proven technology for large-scale monoclonal antibody, vaccine, and recombinant protein production, with an enormous installed base at commercial manufacturing facilities globally ranging from small 200-liter development systems to large 20,000-liter commercial production bioreactors.

However, the single-use bioreactors segment is projected to register the highest CAGR during the forecast period. Single-use bioreactors, which use pre-sterilized disposable plastic bags instead of fixed stainless steel vessels, eliminate the time-consuming cleaning and sterilization cycles between production runs and offer significantly faster facility setup and greater manufacturing flexibility. The COVID-19 pandemic response demonstrated that single-use systems can scale production of new biological products much faster than stainless steel bioreactor installations, which typically require 18 to 24 months for design, construction, and validation. This flexibility advantage is driving pharmaceutical manufacturers to prefer single-use systems for new facility investments and clinical manufacturing applications.

By Scale: In 2026, Commercial-Scale Bioreactors to Hold the Largest Share

Based on scale, the global advanced bioreactors market is segmented into lab-scale bioreactors, pilot-scale bioreactors, and commercial-scale bioreactors. In 2026, the commercial-scale bioreactors segment is expected to account for the largest share of the global advanced bioreactor systems market. Commercial-scale systems used in the production of approved biopharmaceutical products generate the largest revenue per unit and collectively represent the majority of total installed bioreactor capacity at the major pharmaceutical manufacturers globally. The large number of approved biological drugs with significant commercial scale production requirements creates sustained replacement and expansion demand for commercial-scale bioreactor systems.

However, the pilot-scale bioreactors segment is projected to register the highest CAGR during the forecast period. The rapid expansion of biopharmaceutical clinical development pipelines means that more drugs are moving from discovery through process development and into clinical manufacturing, each step requiring pilot-scale bioreactor systems to develop and demonstrate the manufacturing process before committing to commercial-scale facility investment. The very large number of biologic drug candidates currently in clinical development globally ensures sustained and growing demand for pilot-scale development bioreactors.

By Application: In 2026, Biopharmaceutical Production to Hold the Largest Share

Based on application, the global advanced bioreactor systems market is segmented into biopharmaceutical production, cell and gene therapy, industrial biotechnology, food and beverage biotechnology, and academic and research applications. In 2026, the biopharmaceutical production segment is expected to account for the largest share of the global advanced bioreactor systems market. The production of monoclonal antibodies, vaccines, and recombinant proteins for therapeutic use represents the highest-volume and highest-value application of advanced bioreactor systems globally. The large annual procurement requirements of major pharmaceutical manufacturers including Roche, AbbVie, Johnson & Johnson, Pfizer, and Novartis for bioreactor systems to support their commercial biological drug manufacturing programs make biopharmaceutical production the dominant application by revenue.

However, the cell and gene therapy segment is projected to register the highest CAGR during the forecast period. The combination of rapid commercial growth in approved CAR-T cell therapy products, a very large and advancing pipeline of new cell and gene therapy candidates, and the premium pricing of bioreactor systems designed for cell therapy applications makes this the fastest-growing application in the market. As more cell and gene therapy products receive approval and as the manufacturing industry builds out dedicated cell therapy manufacturing infrastructure, the demand for specialized bioreactor systems in this application is expected to grow at a significantly faster rate than any other segment.

By End User: In 2026, Biopharmaceutical Companies to Hold the Largest Share

Based on end user, the global advanced bioreactors market is segmented into biopharmaceutical companies, contract manufacturing organizations (CMOs/CDMOs), research institutes and academic labs, and food and biotechnology companies. In 2026, the biopharmaceutical companies segment is expected to account for the largest share of the global advanced bioreactor systems market. Large pharmaceutical companies including Roche Genentech, AbbVie, Regeneron, AstraZeneca, and Pfizer operate extensive in-house biomanufacturing capacity for their approved biological drugs and maintain significant ongoing investment in bioreactor systems for capacity expansion, technology upgrades, and new product launches. Their large scale of operations and high production volumes make them the dominant end-user category by purchasing volume.

However, the contract manufacturing organizations segment is projected to register the highest CAGR during the forecast period. The growing trend of pharmaceutical companies outsourcing biological drug manufacturing to specialist CDMOs rather than investing in their own manufacturing capacity is creating rapidly growing demand for bioreactor systems at contract manufacturing facilities. Companies including Samsung Biologics, Lonza, Wuxi Biologics, Boehringer Ingelheim Biopharmaceuticals, and Fujifilm Diosynth Biotechnologies are all investing heavily in expanding their bioreactor capacity to serve growing outsourcing demand, and these major capital investment programs are translating into large bioreactor equipment procurement.

By Mode of Operation: In 2026, Fed-Batch Processing to Hold the Largest Share

Based on mode of operation, the global advanced bioreactor systems market is segmented into batch processing, fed-batch processing, and continuous processing through perfusion. In 2026, the fed-batch processing segment is expected to account for the largest share of the global advanced bioreactor systems market. Fed-batch culture, where nutrients are periodically added to the bioreactor to extend the productive phase of cell growth, is the most widely used production mode for monoclonal antibody manufacturing and represents the current industry standard for most large-scale biological drug production. The enormous installed base of fed-batch bioreactor systems at commercial manufacturing facilities and the regulatory approval of most existing biological drugs as fed-batch processes makes this the dominant mode of operation by market share.

However, the continuous processing segment is projected to register the highest CAGR during the forecast period. The compelling productivity and cost advantages of continuous perfusion culture, combined with the regulatory frameworks being developed by FDA and EMA to accommodate continuous manufacturing, are driving pharmaceutical manufacturers to develop continuous manufacturing processes for new biological drugs and to consider converting high-volume existing products to continuous processes where the manufacturing cost savings justify the development investment. As more continuous bioprocessing programs reach commercial implementation, the demand for perfusion bioreactor systems and related continuous manufacturing infrastructure will grow significantly.

Advanced Bioreactor Systems Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global advanced bioreactor systems market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global advanced bioreactors market. The United States is the world's largest biopharmaceutical market by both consumption and production, home to the majority of the world's leading biopharmaceutical companies including Amgen, Genentech/Roche, Regeneron, Biogen, Gilead Sciences, and dozens of other major biological drug manufacturers, all of which operate or contract for large-scale bioreactor manufacturing capacity. The U.S. is also the center of the global cell and gene therapy industry, with the majority of CAR-T cell therapy approvals, clinical programs, and dedicated manufacturing facilities concentrated in North America. The leading bioreactor manufacturers including Thermo Fisher Scientific and several divisions of Danaher/Cytiva have strong U.S. operations, and the FDA's progressive regulatory framework for advanced biological manufacturing provides a supportive environment for technology adoption and innovation. The very large U.S. CDMO sector, anchored by companies including Lonza's U.S. operations, Samsung Biologics' U.S. client base, and numerous domestic CDMOs, generates substantial bioreactor procurement demand alongside the in-house manufacturing programs of major pharmaceutical companies.

However, the Asia-Pacific advanced bioreactor systems market is expected to grow at the fastest CAGR during the forecast period. China's biopharmaceutical industry has grown very rapidly over the past decade, with a large and growing pipeline of domestically developed biological drugs and biosimilars creating strong domestic demand for bioreactor manufacturing capacity. Chinese CDMOs including WuXi Biologics and Shanghai Pharma Biologic have made very large investments in bioreactor capacity, making China one of the largest and most rapidly growing bioreactor markets in the world. India's biosimilar manufacturing industry, which exports to both emerging and developed markets, relies heavily on large-scale bioreactor systems and represents an important and growing Asia-Pacific market. Japan's advanced biopharmaceutical industry, South Korea's growing biologics sector supported by Samsung Biologics and Celltrion, and Singapore's strategic positioning as a regional biomanufacturing hub with government-supported life sciences manufacturing investments all contribute to the region's high growth trajectory. The rapid growth of cell and gene therapy development programs in China, Japan, and South Korea is creating new demand for specialized cell therapy bioreactor systems in Asia-Pacific.

Europe is a major and technically sophisticated bioreactor equipment market, driven by the large biopharmaceutical manufacturing operations of Roche, Novartis, AstraZeneca, and UCB, the strong European CDMO sector including Lonza Switzerland, Boehringer Ingelheim Germany, and Rentschler Biopharma, and the home base of leading bioreactor manufacturers including Sartorius in Germany, Eppendorf in Germany, Infors in Switzerland, and Kuhner in Switzerland. Switzerland in particular is disproportionately important as both the home of major biological drug producers and several leading bioreactor technology companies. Germany's strong industrial biotechnology sector and its leadership in both pharmaceutical manufacturing and bioprocess equipment manufacturing reinforces Europe's position as a major market. The strong European cell and gene therapy development ecosystem, centered in the UK, Germany, and the Netherlands, is creating growing demand for specialized cell therapy bioreactor systems alongside the large established market for conventional biopharmaceutical production systems.

The advanced bioreactor systems market is moderately concentrated among large life science equipment companies with broad bioprocessing portfolios, specialized bioreactor manufacturers focused on specific technology types, and emerging companies targeting the cell and gene therapy manufacturing sector. Competition is based on system performance, manufacturing scalability, single-use portfolio breadth, digital control system capability, regulatory compliance support, and the depth of process development and technical service capabilities that support customers through the complex process of developing and validating biological manufacturing processes.

Sartorius AG leads the market for single-use bioreactor systems through its Biostat range and its Ambr automated development platform, supported by a comprehensive bioprocess portfolio including filtration, chromatography, and fluid management products that position Sartorius as a complete bioprocessing solution provider. Thermo Fisher Scientific through its HyPerforma and DASbox bioreactor lines and its comprehensive bioprocessing consumables and equipment portfolio is a close competitor for broad bioreactor market leadership. Cytiva, formerly GE Healthcare Life Sciences and now part of Danaher, offers the WAVE rocking bioreactor and Xcellerex stirred-tank systems alongside a broad upstream and downstream bioprocessing portfolio. Eppendorf provides bioreactor systems for research and pilot-scale applications with a focus on precision control and ease of use. Merck KGaA through its MilliporeSigma life science division offers bioreactor systems as part of its comprehensive bioprocessing portfolio.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, customer relationships, geographic presence, and recent strategic developments. Some of the key players operating in the global advanced bioreactor systems market include Sartorius AG (Germany), Thermo Fisher Scientific Inc. (U.S.), Cytiva/Danaher Corporation (U.S.), Eppendorf AG (Germany), Merck KGaA/MilliporeSigma (Germany), GEA Group AG (Germany), Applikon Biotechnology/Getinge Group (Netherlands/Sweden), PBS Biotech Inc. (U.S.), Distek Inc. (U.S.), Solaris Biotechnology Srl (Italy), Infors AG (Switzerland), Pierre Guerin Technologies (France), BBI Biotech GmbH (Germany), ZETA Holding GmbH (Austria), and Kuhner AG (Switzerland), among others.

The global market is expected to reach USD 11.8 billion by 2036 from an estimated USD 4.2 billion in 2026, at a CAGR of 10.9% during the forecast period 2026-2036.

In 2026, the stirred-tank bioreactors segment is expected to hold the largest share of the global market, reflecting stirred-tank systems being the established and most widely deployed bioreactor configuration across commercial biological drug manufacturing globally.

The single-use bioreactors segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the operational advantages of eliminating cleaning and sterilization cycles, the manufacturing flexibility that disposable systems provide, and pharmaceutical manufacturers' preference for single-use technology in new facility investments and clinical manufacturing.

In 2026, the biopharmaceutical production segment is expected to hold the largest share of the global market, reflecting the dominant position of monoclonal antibody, vaccine, and recombinant protein manufacturing as the highest-volume and highest-value application of advanced bioreactor systems.

The cell and gene therapy segment is projected to register the highest CAGR during the forecast period, driven by rapid commercial growth of approved CAR-T products, a very large pipeline of new cell and gene therapy candidates advancing through clinical development, and the premium pricing of specialized bioreactor systems designed for these personalized medicine manufacturing applications.

The market is primarily driven by the sustained rapid growth of the global biopharmaceuticals market creating growing demand for bioreactor manufacturing capacity, and by the emergence of cell and gene therapy as a commercially important new application requiring specialized bioreactor systems that are creating a fast-growing new market segment alongside the established biopharmaceutical production market.

Key players are Sartorius AG (Germany), Thermo Fisher Scientific Inc. (U.S.), Cytiva/Danaher Corporation (U.S.), Eppendorf AG (Germany), Merck KGaA/MilliporeSigma (Germany), GEA Group AG (Germany), Applikon Biotechnology/Getinge Group (Netherlands/Sweden), PBS Biotech Inc. (U.S.), Distek Inc. (U.S.), Solaris Biotechnology Srl (Italy), Infors AG (Switzerland), Pierre Guerin Technologies (France), BBI Biotech GmbH (Germany), ZETA Holding GmbH (Austria), and Kuhner AG (Switzerland), among others.

Asia-Pacific is expected to register the highest growth rate in the global advanced bioreactor systems market during the forecast period 2026-2036, driven by China's rapidly growing domestic biopharmaceutical industry and the very large bioreactor capacity investments of Chinese CDMOs including WuXi Biologics, India's expanding biosimilar manufacturing sector, and South Korea's growing biologics production capabilities.

Published Date: May-2024

Published Date: Jan-2024

Published Date: May-2023

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates