Resources

About Us

Real-World Evidence (RWE) Oncology Solutions Market Size, Share & Trends Analysis by Component (Datasets, Consulting Services), Application, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026–2036)

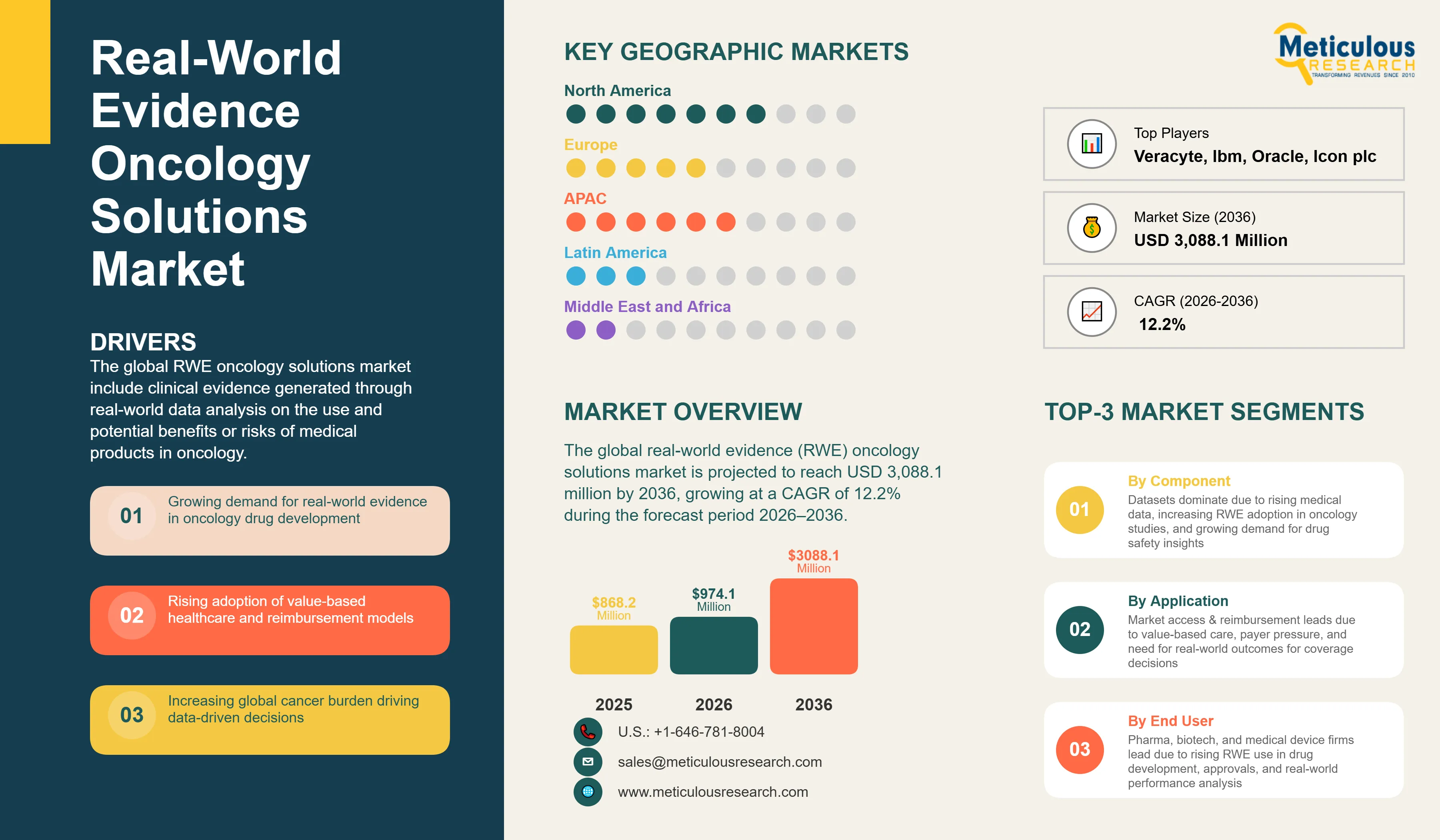

Report ID: MRHC - 104590 Pages: 204 Apr-2026 Formats*: PDF Category: Healthcare Delivery: 2 to 4 Hours Download Free Sample ReportThe global real-world evidence (RWE) oncology solutions market was valued at USD 974.1 million in 2026 and is projected to reach USD 3,088.1 million by 2036, growing at a CAGR of 12.2% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global RWE oncology solutions market include clinical evidence generated through real-world data analysis on the use and potential benefits or risks of medical products in oncology. Real-world evidence can be generated using a range of study designs, such as randomized trials, large simple trials, pragmatic trials, and both prospective and retrospective observational studies. In oncology, RWE plays a crucial role across the drug development process by helping to shorten timelines, reduce clinical trial costs, and increase the chances of technical and regulatory success.

Real-world data come from a wide range of sources that capture outcomes across diverse patient populations in everyday clinical settings. These datasets are used in secondary format, where retrospective studies are conducted to generate meaningful evidence. This evidence provides actionable insights into unmet clinical needs and the economic impact on cancer patients and healthcare systems, enables outcome determination based on much larger data samples, reduces costs, and improves the overall efficiency of clinical trials.

The growth of this market is primarily driven by the increasing demand for robust data to support oncology drug development, regulatory decision making, and value based healthcare models. Pharmaceutical companies are progressively incorporating RWE alongside randomized controlled trials to optimize clinical trial design, accelerate regulatory approvals, and support label expansions. The growing complexity and cost of oncology drug development, where therapies often require more than a decade and billions of dollars to reach approval, has further increased reliance on real-world data to allow external control arms, hybrid trials, and post marketing studies. At the same time, the shift toward value based healthcare is encouraging payers and healthcare systems to rely on real-world evidence to evaluate treatment effectiveness, long term outcomes, and economic value before granting reimbursement for high cost oncology therapies.

However, growth of this market is restrained by concerns related to data privacy and security, the lack of standardization in data collection practices, high implementation and maintenance costs, and limited interoperability between healthcare systems across different regions.

On the other hand, the expansion of RWE platforms into emerging markets, integration with precision medicine initiatives, development of AI-powered analytics solutions, and deepening partnerships between healthcare stakeholders present considerable growth opportunities for market contributors. Additionally, the ongoing shift toward patient centric healthcare models, the adoption of cloud based RWE platforms, and the real time collection and analysis of genomic and molecular data are key trends expected drive the growth of this market during the forecast period.

Driver: Growing Demand for Real-World Evidence in Drug Development

The demand for RWE in oncology drug development is accelerating as sponsors seek to optimize clinical trial design, accelerate regulatory pathways, and generate robust evidence for label expansions and post-marketing commitments. According to the Pharmaceutical Research and Manufacturers of America (PhRMA), in its January 2026 annual report, oncology accounted for nearly 40% of the global pharmaceutical pipeline, with median development timelines exceeding 10 years and costs surpassing USD 2.5 billion per approved therapy. RWE helps address these challenges by enabling external control arms, pragmatic trial designs, and hybrid decentralized studies, which can reduce patient recruitment timelines by up to 30% according to data shared by Flatiron Health in its February 2026 investor update.

Industry examples illustrate the practical application of RWE in accelerating oncology drug development. In December 2025, the FDA approved a supplemental new drug application for an immuno-oncology agent based partly on real-world data derived from Flatiron Health's oncology EHR platform, marking one of the first approvals to incorporate external control arm methodology for a metastatic indication. Similarly, IQVIA's E360 Real-world Data Platform, as referenced in the company's January 2026 corporate disclosure, now supports over 40 active oncology drug development programs globally, with dedicated modules for biomarker-stratified patient identification and real-world progression-free survival estimation.

Opportunity: Expansion In Emerging Markets

Emerging markets represent a significant growth opportunity for RWE oncology solutions, as healthcare systems in Asia-Pacific, Latin America, and the Middle East & Africa seek to build scalable evidence-generation infrastructure to support growing cancer burdens and expanding access to novel therapies. According to the International Agency for Research on Cancer (IARC), in its January 2026 GLOBOCAN update, cancer incidence in emerging economies is projected to grow at 2.1% annually through 2030, driven by population growth, aging, and lifestyle changes, creating sustained demand for RWE solutions to inform treatment decisions and policy development.

Industry examples illustrate the expanding footprint of RWE solutions in emerging markets. According to IQVIA, in its 2025 Asia-Pacific Oncology Trends report, the company's E360 platform now integrates clinical, claims, and pharmacy data from over 50 million patient lives across the region to support oncology research, with specific modules for biomarker-stratified patient identification and real-world progression-free survival estimation. Similarly, Flatiron Health, in its February 2026 public materials, reported expanded collaborations with academic cancer centers in Japan, China, and Australia to integrate de-identified oncology EHR data into its global research platform, enabling cross-border comparative effectiveness analyses.

Growing Regulatory Acceptance of RWE Accelerating Adoption Across Oncology Drug Development

Regulatory authorities in key markets are increasingly acknowledging the value of real-world evidence in healthcare decisions, offering clear guidance on how real-world data can be used in regulatory submissions and post approval studies. In December 2025, the FDA released final guidance on using real-world evidence to support medical device approvals, making it clear that patient level real-world data can be included in submissions and signaling growing regulatory acceptance of RWE for oncology applications. At the same time, DARWIN EU network of the European Medicines Agency had launched over 100 real-world data studies by mid-2025, including targeted oncological research to address regulatory questions in cancer care. These moves are helping reduce uncertainty for pharma and biotech companies using RWE in their regulatory strategies, paving the way for wider adoption across the market.

Advancements in Artificial Intelligence and Data Analytics Transforming RWE Generation

Advances in technologies like artificial intelligence, machine learning, and advanced analytics are making it easier to turn complex datasets such as electronic health records, genomic information, and claims data into actionable insights. These tools allow for more precise patient grouping, biomarker discovery, and treatment outcome prediction, increasing the usefulness of real-world evidence in oncological research and clinical care. The expanding volume of healthcare data from hospitals, along with prevalent adoption of certified health IT in acute care settings, is providing a strong foundation for AI-powered RWE platforms to generate more reliable and scalable evidence for oncology stakeholders.

Rising Global Cancer Burden Reinforcing Demand for Scalable Evidence Generation Systems

Increasing cancer incidence, driven by aging populations and lifestyle changes, is creating a strong need for scalable evidence generation systems that can analyze outcomes across diverse patient populations. Global pharmaceutical R&D spending reached approximately USD 200 to 250 billion in 2025, with oncology accounting for nearly 40% of industry pipelines, underscoring the critical role of RWE in accelerating development timelines and de risking investment decisions for sponsors. The growing complexity of oncology treatment pathways, coupled with the rapid proliferation of targeted therapies and immune oncology agents, has further intensified the need for robust real-world evidence to inform coverage and reimbursement decisions across high income and emerging markets alike.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 3,088.1 Million |

|

Market Size in 2026 |

USD 974.1 Million |

|

Revenue Growth Rate (2026–2036) |

CAGR of 12.2% |

|

Dominating Component |

Datasets |

|

Dominating Application |

Market Access & Reimbursement/Coverage Decisions |

|

Dominating End User |

Pharmaceutical, Biotechnology, and Medical Device Companies |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

By Component: In 2026, the Datasets Segment to Dominate the Global RWE Oncology Solutions Market

Based on component, the global RWE oncology solutions market is segmented into datasets and consulting services. The large share of this segment is primarily attributed to the exponential growth of medical data generated by hospitals and health systems, the increasing dependence of outcome based oncology studies on real-world data, and the rising demand for information on drug safety among healthcare payers, providers, and regulatory bodies. The growing need for evidence generated from real-world data and the shift from volume to value based care has increased focus on cancer registries, a rise in the adoption of EHR and EMR systems in hospitals, and exponential growth in mobile health data, resulting in the generation of substantial medical data volumes suitable for oncology RWE applications.

By Application: In 2026, the Market Access and Reimbursement Segment to Hold the Largest Share

Based on application, the global RWE oncology solutions market is segmented into drug development and approvals, market access and reimbursement/coverage decisions, medical device development and approvals, post market surveillance, and other applications. The large share of this segment is primarily attributed to the increasing pressure on healthcare payers to demonstrate value for high cost oncology therapies, the growing adoption of value based contracting models, and the expanding role of health technology assessment bodies in coverage determinations. Health technology assessment agencies across high income countries increasingly request real-world data to supplement clinical trial evidence during reimbursement reviews, reinforcing reliance on RWE for market access strategies.

By End User: In 2026, the Pharmaceutical and Medical Device Companies Segment to Hold the Largest Share

Based on end user, the global RWE oncology solutions market is segmented into pharmaceutical, biotechnology, and medical device companies; healthcare payers; healthcare providers; and other end users including academic and research institutions, patient advocacy groups, regulators, and health technology assessment agencies. The large share of this segment is primarily attributed to the increasing importance of RWE studies in drug development and approvals and the growing need to avoid costly drug recalls and assess drug performance in real-world settings. Beyond regulatory approvals, pharmaceutical companies need evidence to create a more holistic picture of a drug's value and demonstrate the newly developed drug's performance outside of controlled clinical trials.

Based on geography, the global RWE oncology solutions market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. The dominant position of North America is primarily attributed to the rising burden of cancer, the shift towards value based care, the growth of personalized healthcare, the availability of robust electronic datasets, a well developed healthcare industry infrastructure, and rising big data adoption in the healthcare sector. Furthermore, the increase in R&D expenditure by biopharmaceutical companies, the strong presence of established RWE solution providers, and the implementation of regulatory frameworks such as the 21st Century Cures Act and the U.S. FDA's RWE Framework continue to drive market growth in this region.

Asia Pacific is expected to witness highest growth during the forecast period, driven by the rapid expansion of healthcare digitization infrastructure across China, Japan, South Korea, India, and Taiwan; the increasing cancer burden across the region; and growing government led investment in health data and precision medicine programs.

The competition within the global RWE oncology solutions market is primarily driven by data asset depth, analytical platform capabilities, regulatory expertise, and the breadth of strategic collaborations across the pharmaceutical, technology, and healthcare value chain.

IQVIA Holdings hold a leading position through its extensive real-world data assets, advanced analytics platforms, and deep domain expertise across oncology drug development and regulatory affairs. Flatiron Health maintains a strong market presence through its oncology specific electronic health record network and research grade real-world datasets supporting both clinical and regulatory applications. Tempus Labs is gaining significant ground through its AI-enabled platform that integrates molecular and clinical data for oncology research and treatment insights.

In addition, Oracle Corporation and IBM Corporation hold notable positions through their healthcare data management and analytics infrastructure, while companies such as Parexel International, ICON plc, and Syneos Health bring deep clinical research organization capabilities to RWE study design and execution.

Some of the key players operating in the global RWE oncology solutions market include IQVIA Holdings Inc. (U.S.), Flatiron Health Inc. (U.S.), Tempus Labs Inc. (U.S.), ICON plc (Ireland), Parexel International Corporation (U.S.), Syneos Health Inc. (U.S.), Oracle Corporation (U.S.), Veracyte Inc. (U.S.), SAS Institute Inc. (U.S.), IBM Corporation (U.S.), Cognizant Technology Solutions Corporation (U.S.), UnitedHealth Group Incorporated (U.S.), Anthem Inc. (U.S.), Clinigen Group plc (U.K.), and PerkinElmer Inc. (U.S.), among others.

The global RWE oncology solutions market is expected to reach USD 3,088.1 million by 2036 from an estimated USD 974.1 million in 2026, at a CAGR of 12.2% during the forecast period 2026–2036.

In 2026, the datasets segment is expected to hold the largest share of the global RWE oncology solutions market, driven by the exponential growth of medical data and the increasing dependence of outcome based studies on real-world data.

In 2026, the market access and reimbursement/coverage decisions segment is expected to account for the largest share, driven by increasing payer pressure to demonstrate value for high cost oncology therapies and the growing role of health technology assessment agencies in coverage determinations.

In 2026, the pharmaceutical, biotechnology, and medical device companies segment is expected to hold the largest share, driven by the growing importance of RWE in drug development, regulatory approvals, and post market performance assessment.

The growth of this market is primarily driven by the increasing demand for robust real-world data to support oncology drug development and regulatory decision making, the shift toward value based healthcare, rising global cancer incidence, expanding regulatory acceptance of RWE by agencies such as the FDA and EMA, and rapid advancements in AI and data analytics technologies improving the depth and reliability of real-world evidence generation.

Key players operating in the global RWE oncology solutions market include IQVIA Holdings Inc. (U.S.), Flatiron Health Inc. (U.S.), Tempus Labs Inc. (U.S.), ICON plc (Ireland), Parexel International Corporation (U.S.), Syneos Health Inc. (U.S.), Oracle Corporation (U.S.), Veracyte Inc. (U.S.), SAS Institute Inc. (U.S.), IBM Corporation (U.S.), Cognizant Technology Solutions Corporation (U.S.), UnitedHealth Group Incorporated (U.S.), Anthem Inc. (U.S.), Clinigen Group plc (U.K.), and PerkinElmer Inc. (U.S.).

Asia Pacific is expected to register the highest growth rate in the global RWE oncology solutions market during the forecast period 2026–2036, driven by expanding healthcare digitization, rising cancer burden, and growing government investment in health data infrastructure across the region.

Published Date: Mar-2026

Published Date: Feb-2026

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates