Resources

About Us

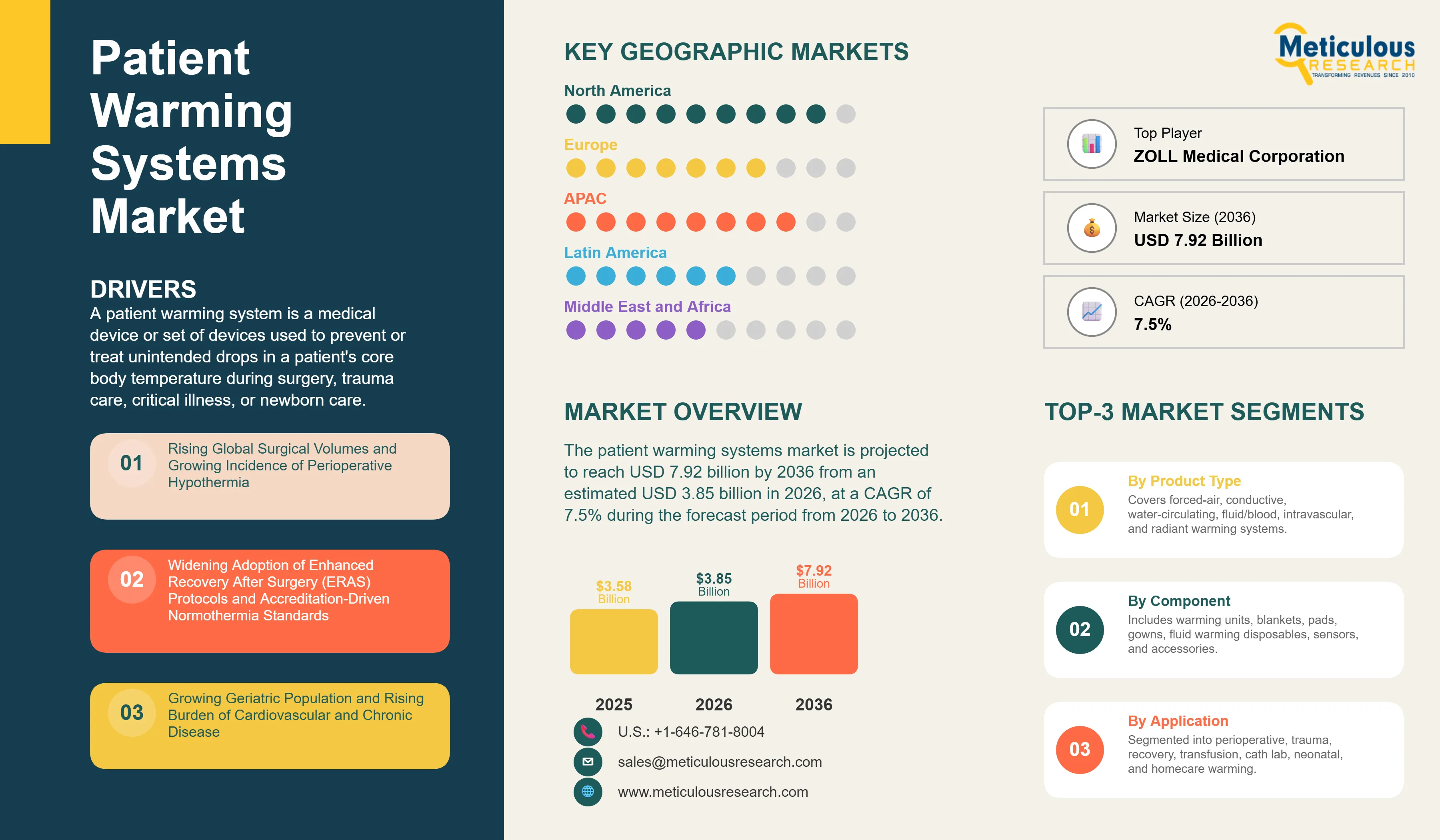

The global patient warming systems market is projected to reach USD 7.92 billion by 2036 from an estimated USD 3.85 billion in 2026, at a CAGR of 7.5% during the forecast period from 2026 to 2036.

Click here to: Get Free Sample Pages

Click here to: Get Free Sample Pages

A patient warming system is a medical device or set of devices used to prevent or treat unintended drops in a patient's core body temperature during surgery, trauma care, critical illness, or newborn care. The category spans forced-air (convective) warming units and disposable blankets, conductive and resistive warming mattresses, water-circulating warming pads, fluid and blood warmers, intravascular temperature management catheters, and radiant warmers, all built around a shared clinical goal: keeping core body temperature within the normothermic range of roughly 36.0°C to 37.5°C throughout a procedure or period of care.

Demand for these systems is closely tied to the volume and complexity of surgical care worldwide. More than 313 million surgical procedures are performed globally each year, and every one of these cases carries some risk of anesthesia-induced heat loss. Clinical literature reviewed in connection with European perioperative care guidelines indicates that between roughly 25% and 90% of patients undergoing elective surgery experience inadvertent postoperative hypothermia, a complication associated with a higher rate of wound infections, more frequent cardiac complications, and increased need for blood transfusion compared with normothermic patients. Guidance from the UK's National Institute for Health and Care Excellence recommends prewarming patients for at least 30 minutes before anesthesia induction and actively warming any procedure expected to last longer than half an hour, which has helped push forced-air and conductive warming from a niche comfort measure into a standard part of surgical protocol across many health systems.

The population most exposed to surgery is also getting older. The number of people aged 60 years or older stood at 1.1 billion in 2023 and is projected to nearly double to 2.1 billion by 2050, and this age group carries a disproportionate share of both surgical volume and thermoregulatory vulnerability, since older patients lose heat faster under anesthesia and tolerate hypothermia less well. As hospitals in developed and emerging markets alike expand operating room capacity to serve this population, they are building normothermia management, including dedicated warming units, disposable blankets, and fluid warmers, into standard surgical purchasing rather than treating it as an add-on.

Patient Warming Systems Market: Expert Perspectives from Industry Leaders

"Normothermia management has moved from a perioperative nicety to a quality metric that hospitals are held accountable for. Purchasing decisions now weigh workflow integration and disposable cost per case as heavily as raw warming performance."

– Director of Perioperative Services, Multi-Hospital Health System

"We are seeing steady replacement demand as older forced-air units reach end of life, alongside genuinely new demand from ambulatory surgical centers that are adding warming protocols for the first time as they take on more complex caseloads."

– Vice President of Sales, Surgical Device Distributor

"Fluid and blood warming is the quieter half of this market, but it's just as critical in trauma and obstetric hemorrhage response. Facilities that once treated it as optional equipment are now building it into mandatory trauma bay and OR checklists."

– Head of Procurement, Regional Trauma Network

Rising Global Surgical Volumes and Growing Incidence of Perioperative Hypothermia

The single largest driver of demand is the sheer scale of surgical activity worldwide. Globally, over 313 million patients undergo surgical procedures annually, and every general or regional anesthetic carries a risk of impaired thermoregulation. Research synthesized for European perioperative hypothermia guidelines found that patients who become hypothermic during elective surgery face substantially higher relative risk of wound infection, cardiac complications, and blood transfusion compared with patients who remain normothermic, which has made active warming a recognized lever for reducing postoperative complications and length of stay. A French multicenter study of perioperative practice found that the prevalence of hypothermia on admission to the recovery room remained at 53.5% even though a warming device had been used for over 90% of patients studied, underscoring that the clinical problem persists even where warming equipment is already in use, and that hospitals continue to invest in better-performing systems rather than treating existing equipment as sufficient.

Widening Adoption of ERAS Protocols and Accreditation-Driven Normothermia Standards

A second driver is the formalization of temperature management within structured surgical care pathways. Enhanced recovery after surgery (ERAS) protocols, now used across a growing share of elective procedures, treat maintenance of normothermia as one of several evidence-based steps that together shorten recovery and reduce complications. Clinical guidance recommends warming all surgical patients undergoing procedures longer than 30 minutes, with prewarming for at least 30 minutes before induction of anesthesia recommended as best practice. As accreditation bodies and hospital quality programs increasingly audit compliance with these standards, facilities are standardizing warming equipment across every operating room and recovery bay rather than deploying it selectively, which supports steady replacement and expansion demand for manufacturers.

Growing Geriatric Population and Rising Burden of Cardiovascular and Chronic Disease

The third major driver is the rapid growth of the global elderly population. According to the World Health Organization (WHO), the number of people aged 60 years and older is projected to double from approximately 1 billion in 2020 to 2.1 billion by 2050, while the population aged 80 years and older is expected to triple during the same period, reaching 426 million. Older adults undergo surgical procedures more frequently for cardiovascular, orthopedic, oncologic, and other chronic conditions and are at greater risk of perioperative hypothermia due to age-related declines in thermoregulatory function. Consequently, the increasing volume of complex surgeries among elderly patients is driving greater adoption of patient warming systems to maintain normothermia, reduce perioperative complications, and improve clinical outcomes. Healthcare providers are therefore increasingly incorporating advanced warming technologies into routine perioperative care, particularly for lengthy and high-risk procedures.

Growth of Portable, Battery-Operated Warming Devices in Prehospital and Emergency Care

A significant opportunity lies in portable and battery-powered warming systems designed for use outside the traditional operating room, including ambulances, military and disaster-response settings, and emergency departments. These devices extend normothermia management to the earliest point of patient contact, where uncontrolled heat loss during transport can compound later surgical risk. As emergency medical services and trauma networks formalize temperature management into their own protocols, demand is opening for compact, ruggedized fluid warmers and warming blankets that do not depend on a fixed power supply.

Expanding Opportunities Across Emerging Markets and Ambulatory Surgical Centers

Emerging markets present a parallel opportunity as hospital systems across Asia-Pacific, Latin America, and parts of the Middle East and Africa expand surgical capacity and modernize operating rooms to international standards of care. Many of these facilities are adopting active warming protocols as a baseline feature of new operating room build-outs rather than retrofitting it later. Ambulatory surgical centers represent a second growth channel, as a rising share of moderately complex procedures move out of hospitals and into outpatient settings that must independently equip themselves with warming systems previously assumed to be a hospital-only requirement.

By Product Type: Forced-Air Warming Systems Lead the Market in 2026

By product type, the market is segmented into forced-air (convective) warming systems, conductive/resistive warming systems, water-circulating warming systems, fluid and blood warming systems, intravascular temperature management systems, and radiant warming systems. Forced-air warming systems are expected to account for the largest share of the market in 2026, reflecting their established position as the default active warming modality across operating rooms, supported by a wide base of installed warming units and a recurring disposable blanket and gown business.

Intravascular temperature management systems and fluid and blood warming systems are projected to register the fastest growth during the forecast period, supported by expanding use in cardiac surgery, targeted temperature management following cardiac arrest, and trauma resuscitation protocols that call for rapid, high-volume warming of transfused fluids and blood products.

By Component: Blankets, Pads and Mattresses Lead the Market in 2026

By component, the market covers warming units and consoles, blankets, pads and mattresses, warming gowns, fluid warming sets and disposables, and temperature sensors and accessories. Blankets, pads and mattresses hold the largest share in 2026, since these single-use consumables are replaced with every patient episode, unlike the reusable warming console that anchors the system.

Fluid warming sets and disposables are expected to grow the fastest, tracking the broader shift toward disposable, single-patient-use administration sets across blood and fluid warming applications for infection control reasons.

By Application: Perioperative/Surgical Warming Leads the Market in 2026

By application, the market spans perioperative/surgical warming, critical care and trauma warming, post-anesthesia care and recovery, fluid and blood transfusion warming, interventional and cath lab procedures, newborn and pediatric warming, and home and outpatient care. Perioperative/surgical warming holds the largest share in 2026, as maintaining normothermia from prewarming through recovery remains the core, highest-volume use case for these systems.

Critical care and trauma warming is expected to grow the fastest, as emergency departments, ICUs, and trauma centers increasingly formalize temperature management protocols for resuscitation and post-cardiac-arrest care.

By End User: Hospitals Lead the Market in 2026

By end user, the market is split among hospitals, ambulatory surgical centers, trauma and emergency care centers, maternity and neonatal care units, and homecare and rehabilitation settings. Hospitals hold the largest share in 2026, reflecting their high surgical volumes, broad procedural mix, and established capital budgets for perioperative equipment.

Ambulatory surgical centers are expected to grow the fastest, as more moderate-complexity procedures shift to outpatient settings that must independently equip operating suites with warming systems.

North America Leads the Market in 2026

By region, the global patient warming systems market is split across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America holds the largest share in 2026, underpinned by early adoption of formal normothermia protocols, a dense base of leading manufacturers headquartered in the region, and established hospital purchasing infrastructure for perioperative equipment.

Asia-Pacific is expected to record the fastest growth over the forecast period. Rapid hospital construction, rising surgical volumes tied to an aging population that is projected to represent around one in five people globally by 2050, and growing government investment in surgical care access across China, India, and Southeast Asia are driving adoption of warming systems as new operating rooms come online. Europe remains an established market, supported by national clinical guidelines on perioperative hypothermia prevention in countries such as the UK and Germany that have formalized warming into standard surgical protocol.

Leading companies in the market have grown through new product launches, portfolio expansion, distribution partnerships, and targeted acquisitions. Broadening disposable product lines, extending into portable and battery-powered formats, and deepening distribution reach in emerging markets have been the most common ways players strengthen their position.

Prominent companies active in the global patient warming systems market include Solventum Corporation (U.S.), ICU Medical, Inc. (U.S.), Stryker Corporation (U.S.), Medtronic plc (Ireland), GE HealthCare Technologies Inc. (U.S.), Becton, Dickinson and Company (U.S.), Gentherm Incorporated (U.S.), ZOLL Medical Corporation (U.S.), Belmont Medical Technologies, Inc. (U.S.), Inspiration Healthcare Group plc (U.K.), Geratherm Medical AG (Germany), Stihler Electronic GmbH (Germany), Barkey GmbH & Co. KG (Germany), Atom Medical Corporation (Japan), and Encompass Group, LLC (U.S.).

Patient Warming Systems Market: Latest Developments

|

Particulars |

Details |

|

Forecast Period |

2026 to 2036 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

CAGR (Value) |

7.5% |

|

Market Size (Value) in 2026 |

USD 3.85 Billion |

|

Market Size (Value) in 2036 |

USD 7.92 Billion |

|

Segments Covered |

By Product Type - Forced-Air (Convective) Warming Systems - Conductive/Resistive Warming Systems - Water-Circulating Warming Systems - Fluid and Blood Warming Systems - Intravascular Temperature Management Systems - Radiant Warming Systems By Component - Warming Units/Consoles - Blankets, Pads and Mattresses - Warming Gowns - Fluid Warming Sets and Disposables - Temperature Sensors and Accessories By Application - Perioperative/Surgical Warming - Critical Care and Trauma Warming - Post-Anesthesia Care and Recovery - Fluid and Blood Transfusion Warming - Interventional and Cath Lab Procedures - Newborn and Pediatric Warming - Home and Outpatient Care By End User - Hospitals - Ambulatory Surgical Centers - Trauma and Emergency Care Centers - Maternity and Neonatal Care Units - Homecare and Rehabilitation Settings |

|

Countries Covered |

North America (U.S., Canada), Europe (Germany, U.K., France, Italy, Spain, and Rest of Europe), Asia-Pacific (Japan, China, India, South Korea, Australia, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and the Middle East & Africa (Saudi Arabia, UAE, South Africa, and Rest of Middle East & Africa) |

|

Key Companies |

Solventum Corporation (U.S.), ICU Medical, Inc. (U.S.), Gentherm Incorporated (U.S.), Medtronic plc (Ireland), ZOLL Medical Corporation (U.S.), Belmont Medical Technologies, Inc. (U.S.), Stryker Corporation (U.S.), Barkey GmbH & Co. KG (Germany), Dräger (Germany), GE HealthCare Technologies Inc. (U.S.), Atom Medical Corporation (Japan), Inspiration Healthcare Group plc (U.K.), Geratherm Medical AG (Germany), Stihler Electronic GmbH (Germany), Cincinnati Sub-Zero (U.S.) |

The global patient warming systems market size is estimated at USD 3.85 billion in 2026.

The market is projected to grow from USD 3.85 billion in 2026 to USD 7.92 billion by 2036, at a CAGR of 7.5%.

The patient warming systems market is projected to reach USD 7.92 billion by 2036, at a compound annual growth rate (CAGR) of 7.5% from 2026 to 2036.

Key players in the patient warming systems market include Solventum Corporation (U.S.), ICU Medical, Inc. (U.S.), Stryker Corporation (U.S.), Medtronic plc (Ireland), GE HealthCare Technologies Inc. (U.S.), Becton, Dickinson and Company (U.S.), Gentherm Incorporated (U.S.), and others.

The move toward portable, battery-operated warming systems for homecare and prehospital use, and the integration of smart sensors and automated temperature feedback into warming workflows, are prominent trends in the market.

In 2026, forced-air warming leads by product type, blankets/pads/mattresses lead by component, perioperative/surgical warming leads by application, hospitals lead by end user, and North America leads by region. Intravascular warming, fluid warming disposables, critical care and trauma warming, and ambulatory surgical centers are among the fastest-growing segments.

North America holds the largest share of the market in 2026, supported by early adoption of normothermia protocols and established reimbursement pathways. Asia-Pacific is expected to record the highest growth rate over the forecast period, driven by rising surgical volumes and hospital modernization.

Key drivers include rising global surgical volumes and the persistent incidence of perioperative hypothermia, wider adoption of ERAS protocols and accreditation-driven normothermia standards, and a growing geriatric population that raises both surgical volume and thermoregulatory vulnerability.

1. Introduction

1.1. Market Definition

1.2. Currency & Limitations

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Assessment

2.3.1. Market Size Estimation

2.3.2. Bottom-Up Approach

2.3.3. Top-Down Approach

2.3.4. Growth Forecast

2.4. Assumptions for the Study

3. Executive Summary

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Rising Global Surgical Volumes and Growing Incidence of Perioperative Hypothermia

4.2.1.2. Widening Adoption of Enhanced Recovery After Surgery (ERAS) Protocols and Accreditation-Driven Normothermia Standards

4.2.1.3. Growing Geriatric Population and Rising Burden of Cardiovascular and Chronic Disease

4.2.2. Restraints

4.2.2.1. High Cost of Advanced and Disposable Warming Systems Limiting Adoption in Budget-Constrained Settings

4.2.3. Opportunities

4.2.3.1. Growth of Portable, Battery-Operated Warming Devices Widening Access in Prehospital and Emergency Care

4.2.3.2. Expanding Opportunities Across Emerging Markets and Ambulatory Surgical Centers

4.2.4. Challenges

4.2.4.1. Clinical and Regulatory Scrutiny Around Airflow-Related Infection Control in Forced-Air Warming

4.3. Key Trends

4.3.1. Move Toward Portable, Battery-Operated Warming Systems for Homecare and Prehospital Use

4.3.2. Integration of Smart Sensors and Automated Temperature Feedback into Warming Workflows

4.4. Vendor Selection Criteria/Factors Influencing Purchase Decisions

4.5. Use Cases

4.6. Porter's Five Forces Analysis

4.6.1. Bargaining Power of Buyers: Moderate to High

4.6.2. Bargaining Power of Suppliers: Moderate

4.6.3. Threat of Substitutes: Low

4.6.4. Threat of New Entrants: Moderate

4.6.5. Degree of Competition: High

4.7. Value Chain Analysis

4.8. Pricing Analysis

4.9. Technology Analysis

4.10. PESTEL Analysis

5. Patient Warming Systems Market Assessment—By Product Type

5.1. Overview

5.2. Forced-Air (Convective) Warming Systems

5.3. Conductive/Resistive Warming Systems

5.4. Water-Circulating (Hydronic) Warming Systems

5.5. Fluid and Blood Warming Systems

5.6. Intravascular (Endovascular) Temperature Management Systems

5.7. Radiant Warming Systems

6. Patient Warming Systems Market Assessment—By Component

6.1. Overview

6.2. Warming Units/Consoles

6.3. Blankets, Pads and Mattresses

6.4. Warming Gowns

6.5. Fluid Warming Sets, Cassettes and Disposables

6.6. Temperature Sensors and Accessories

7. Patient Warming Systems Market Assessment—By Application

7.1. Overview

7.2. Perioperative/Surgical Warming

7.3. Critical Care and Trauma Warming

7.4. Post-Anesthesia Care and Recovery

7.5. Fluid and Blood Transfusion Warming

7.6. Interventional and Cath Lab Procedures

7.7. Newborn and Pediatric Warming

7.8. Home and Outpatient Care

8. Patient Warming Systems Market Assessment—By End User

8.1. Overview

8.2. Hospitals

8.3. Ambulatory Surgical Centers

8.4. Trauma and Emergency Care Centers

8.5. Maternity and Neonatal Care Units

8.6. Homecare and Rehabilitation Settings

9. Patient Warming Systems Market Assessment—By Geography

9.1. Overview

9.2. North America

9.2.1. United States

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. United Kingdom

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia Pacific

9.4.1. Japan

9.4.2. China

9.4.3. India

9.4.4. South Korea

9.4.5. Australia & New Zealand

9.4.6. Rest of Asia Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

9.6.1. Saudi Arabia

9.6.2. United Arab Emirates

9.6.3. South Africa

9.6.4. Rest of Middle East & Africa

10. Competitive Landscape

10.1. Introduction

10.2. Key Growth Strategies

10.3. Competitive Benchmarking

10.4. Competitive Dashboard

10.4.1. Industry Leaders

10.4.2. Market Differentiators

10.4.3. Vanguards

10.4.4. Emerging Companies

10.5. Market Share/Position Analysis

11. Company Profiles (Company Overview, Financial Overview, Product Portfolio, Strategic Developments)

11.1. Solventum Corporation (U.S.)

11.2. ICU Medical, Inc. (U.S.)

11.3. Gentherm Incorporated (U.S.)

11.4. Medtronic plc (Ireland)

11.5. ZOLL Medical Corporation (U.S.)

11.6. Belmont Medical Technologies, Inc. (U.S.)

11.7. Stryker Corporation (U.S.)

11.8. Barkey GmbH & Co. KG (Germany)

11.9. Dräger (Germany)

11.10. GE HealthCare Technologies Inc. (U.S.)

11.11. Atom Medical Corporation (Japan)

11.12. Inspiration Healthcare Group plc (U.K.)

11.13. Geratherm Medical AG (Germany)

11.14. Stihler Electronic GmbH (Germany)

11.15. Cincinnati Sub-Zero (U.S.)

12. Appendix

12.1. Available Customization

12.2. Related Reports

Published Date: Jun-2026

Published Date: Feb-2026

Published Date: Jan-2025

Published Date: Mar-2024

Published Date: Mar-2016

Subscribe to get the latest industry updates