Resources

About Us

Patient Flow Management Market Size, Share & Trends Analysis by Type, Component, Delivery Mode, Application, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

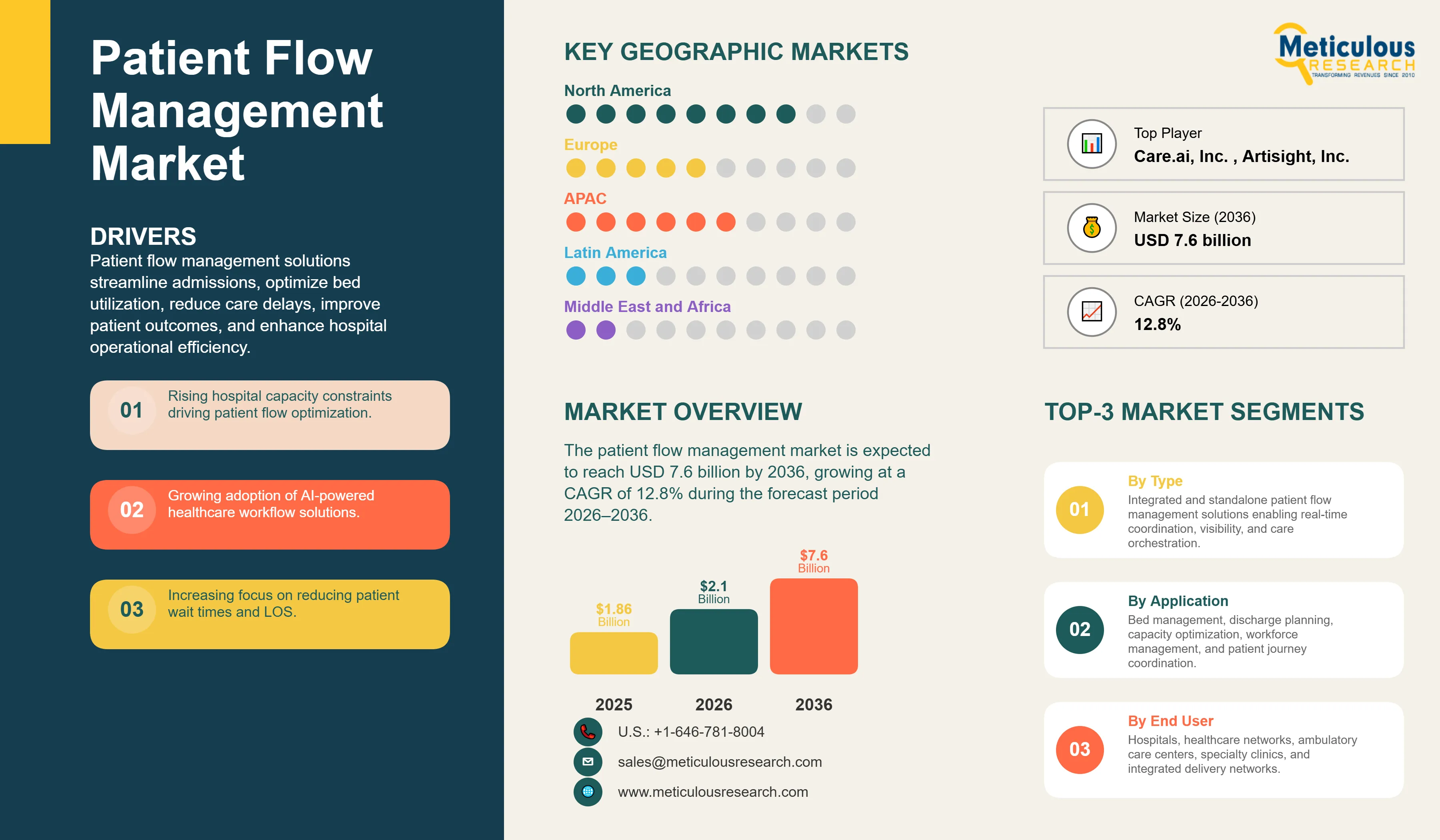

Report ID: MRHC - 1042041 Pages: 283 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global patient flow management market is valued at USD 2.1 billion in 2026. This market is expected to reach USD 7.6 billion by 2036, growing at a CAGR of 12.8% during the forecast period 2026–2036.

Market Insights: Optimizing Hospital Throughput to Address Rising Patient Complexity and Capacity Constraints

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global patient flow management market is a critical pillar of modern healthcare operations, providing the essential infrastructure for optimizing patient throughput and managing the complex journey from admission to discharge. Patient flow optimization solutions enable healthcare organizations to maintain institutional integrity and clinical productivity by providing real-time visibility into bed availability, patient status, and resource allocation. As of 2026, the market is undergoing a significant transformation, driven by the global imperative to address chronic emergency department (ED) boarding and the increasing complexity of patient care. According to industry reports, efficient patient flow management is essential for reducing hospital-acquired conditions and improving patient satisfaction scores.

The transition toward integrated and AI-powered patient flow management platforms is essential for improving clinical workflows and hospital throughput in the healthcare industry. Modern solutions leverage advanced analytics and event-driven orchestration to provide a unified view of the patient journey, ensuring that stakeholders have immediate access to actionable insights. As healthcare systems transition toward value-based care models, the demand for flow management solutions that can demonstrably reduce length of stay (LOS) and improve bed utilization is expected to surge.

Drivers: Optimizing Hospital Throughput to Address Rising Patient Complexity and Capacity Constraints

The primary driver for the patient flow management market is the escalating global cost of healthcare and the increasing volume of high-acuity patients, which necessitates a more efficient and data-driven approach to throughput management. According to the AHA, hospital capacity constraints and ED boarding account for significant annual losses in hospital revenue and patient safety. This massive financial burden is driving the adoption of integrated flow management platforms to manage the entire patient journey and clinical documentation. Furthermore, the shift toward digital health and the increasing demand for real-time location visualization are significant drivers. Government initiatives promoting the adoption of connected health solutions and the exchange of health information are compelling healthcare organizations to invest in flow management solutions that can seamlessly integrate with broader healthcare IT ecosystems.

Restraints: High Implementation Costs and Organizational Change Resistance

Market growth is restrained by the high cost of implementing comprehensive patient flow management solutions and the technical challenges of achieving seamless data interoperability across disparate legacy IT systems and EHR platforms. For many mid-sized hospitals, the initial capital investment and ongoing maintenance costs of a facility-wide flow management network can be a significant barrier. Additionally, the lack of standardized data protocols between different technology providers often leads to data silos, making it difficult to achieve a truly unified patient journey record. Concerns regarding data privacy and cybersecurity in centralized information hubs also act as deterrents to market expansion. Furthermore, the significant organizational change management and specialized training required for successful implementation can lead to slower adoption rates.

Opportunities: Advancing AI-Driven Flow Analytics and Virtual Care Orchestration

The integration of artificial intelligence (AI) and machine learning (ML) into patient flow management platforms offers substantial growth opportunities. AI-powered tools can analyze complex flow data and clinical evidence to identify potential bottlenecks, facilitating more precise clinical intervention. By 2026, AI-driven predictive analytics are being used to forecast patient admissions and discharge readiness, enabling proactive bed distribution and improving patient safety. Furthermore, the shift toward cloud-native (SaaS) flow management platforms provides healthcare organizations with superior scalability, flexibility, and lower upfront costs. Cloud-based solutions also facilitate real-time data sharing among diverse clinical specialists, supporting multi-disciplinary collaboration, which is particularly beneficial for regional healthcare networks.

Evolution toward Holistic and AI-Powered Clinical Care Orchestration

Patient flow management platforms are evolving from standalone bed-management tools into enterprise-wide care orchestration systems that integrate EHRs, RTLS platforms, patient monitoring devices, and operational data to optimize throughput across the care continuum. The trend is being driven by persistent capacity constraints and patient boarding challenges in hospitals, particularly in emergency departments. Healthcare providers are increasingly deploying AI-enabled forecasting, predictive discharge planning, and capacity management tools to improve resource utilization, reduce delays, and support real-time operational decision-making. Recent studies have demonstrated the growing use of predictive analytics to forecast inpatient demand and emergency department boarding volumes, enabling proactive patient flow interventions.

Integration of Ambient Clinical Intelligence and Virtual Nursing

The integration of ambient clinical intelligence and virtual nursing capabilities is becoming a key differentiator in patient flow management solutions. Healthcare organizations are leveraging ambient AI technologies to automate clinical documentation, reduce administrative burden, and enable clinicians to spend more time on direct patient care. A 2025 multi-health-system study found that clinician burnout declined from 51.9% to 38.8% after 30 days of ambient AI scribe usage, while users reported improvements in after-hours documentation and patient engagement. Additional research has shown that ambient clinical intelligence can significantly reduce documentation workload and save clinicians approximately 2.5 hours of off-hours documentation time per week. These benefits are accelerating adoption of AI-enabled workflow automation and virtual care support tools across hospitals seeking to address workforce shortages and improve operational efficiency.

Analysis by Type

Based on type, the integrated patient flow management segment is expected to hold the largest share in 2026. This dominance is driven by the increasing demand for enterprise-wide solutions that can manage the entire patient journey across multi-facility health systems. Integrated platforms provide a centralized 'source of truth' for patient status and bed availability, enabling more efficient regional patient flow coordination. The standalone flow management segment continues to be significant for smaller facilities or department-specific applications, such as emergency department flow centers and radiology operations hubs. However, the shift toward holistic clinical care orchestration is driving the rapid growth of integrated platforms.

Analysis by Component

The software segment is expected to account for the largest share in 2026, reflecting the critical role of data processing and visualization in flow management. This segment includes real-time visualization dashboards, predictive analytics and AI/ML engines, and resource and bed orchestration modules. The shift toward cloud-native (SaaS) software is a major trend, providing superior scalability and support for multi-facility integration. The services segment—including strategic consulting, custom implementation, and post-deployment support—is also growing in importance as healthcare organizations seek expert guidance for organizational change management and technical integration.

Analysis by Application

By application, the patient flow and capacity management segment is expected to hold the largest share in 2026. This reflects the primary operational focus on reducing length of stay (LOS) and optimizing bed utilization. Other key applications include discharge management, which is critical for reducing hospital readmission penalties, and workforce and staffing optimization, which uses flow data to align clinical staff with patient demand. Clinical triage and monitoring centers are also an emerging application, particularly for managing high-acuity patients and improving sepsis bundle compliance.

North America is expected to dominate the global patient flow management market in 2026, accounting for around 45% of total revenue. The region's leadership is supported by a high adoption of advanced healthcare IT solutions, a mature healthcare IT landscape, and significant investments in hospital command centers by major IDNs. Favorable reimbursement policies and a strong regulatory focus on patient safety and clinical quality continue to drive market growth in the U.S. and Canada. The presence of leading flow management vendors and a robust ecosystem for medical innovation also contribute to North America's dominant position.

The Asia Pacific region is projected to witness the fastest growth during the forecast period. This growth is fueled by the rising burden of hospital operations and government initiatives to modernize healthcare infrastructure and expand access to flow standards across China, India, and Australia. As these countries implement large-scale digital health initiatives and increase their focus on expanding access to specialized patient monitoring, the demand for integrated flow management solutions is expected to rise significantly. The increasing adoption of cloud-based platforms and the digital transformation of public health agencies in the region are creating substantial opportunities for global and local vendors.

The competitive landscape of the global patient flow management market is characterized by intense innovation and strategic consolidations as vendors seek to provide end-to-end clinical care orchestration platforms. Leading players are differentiating themselves through the sophistication of their AI engines and their ability to provide seamless integration with EHRs and other clinical management platforms. Strategic acquisitions of niche analytics and communication companies are a common trend as vendors seek to enhance their diagnostic capabilities. The market is also seeing increased collaboration between flow management vendors and healthcare providers to ensure seamless patient monitoring across the care continuum.

Key players operating in the global market include GE HealthCare Technologies Inc. (U.S.), TeleTracking Technologies, Inc. (U.S.), Oracle Health (Cerner) (U.S.), Epic Systems Corporation (U.S.), CentralLogic (Acquire Health) (U.S.), Koninklijke Philips N.V. (Netherlands), Siemens Healthineers AG (Germany), McKesson Corporation (U.S.), Allscripts Healthcare Solutions, Inc. (U.S.), and various emerging technology providers specializing in AI-driven flow analytics and virtual nursing tools.

The market is projected to reach USD 7.6 billion by 2036, growing at a CAGR of 12.8% from 2026 to 2036.

Hospitals report a significant reduction in length of stay (LOS) and an improvement in bed utilization and patient throughput.

The Artificial Intelligence & Machine Learning (AI/ML) segment is expected to grow the fastest as predictive analytics becomes essential for forecasting.

Around 80% of new deployments are cloud-native, enabling regional coordination and rapid scalability.

North America holds the largest share, estimated at 45% in 2026, driven by a mature IT infrastructure and high demand for efficiency.

AI enables the prediction of patient admissions and discharge readiness, improving clinical consistency and patient safety.

The pressure to reduce length of stay (LOS) is driving the demand for integrated platforms to manage the high volume of patients.

Hospitals and clinics are the primary adopters, managing the highest volumes of diverse patient journeys.

These systems provide the continuous, data-driven flow management necessary to improve clinical outcomes and reduce the total cost of care.

The top 5 players are GE HealthCare, TeleTracking Technologies, Oracle Health (Cerner), Epic Systems, and CentralLogic.

Published Date: Jul-2026

Published Date: Feb-2026

Published Date: Jan-2025

Published Date: Mar-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates