Resources

About Us

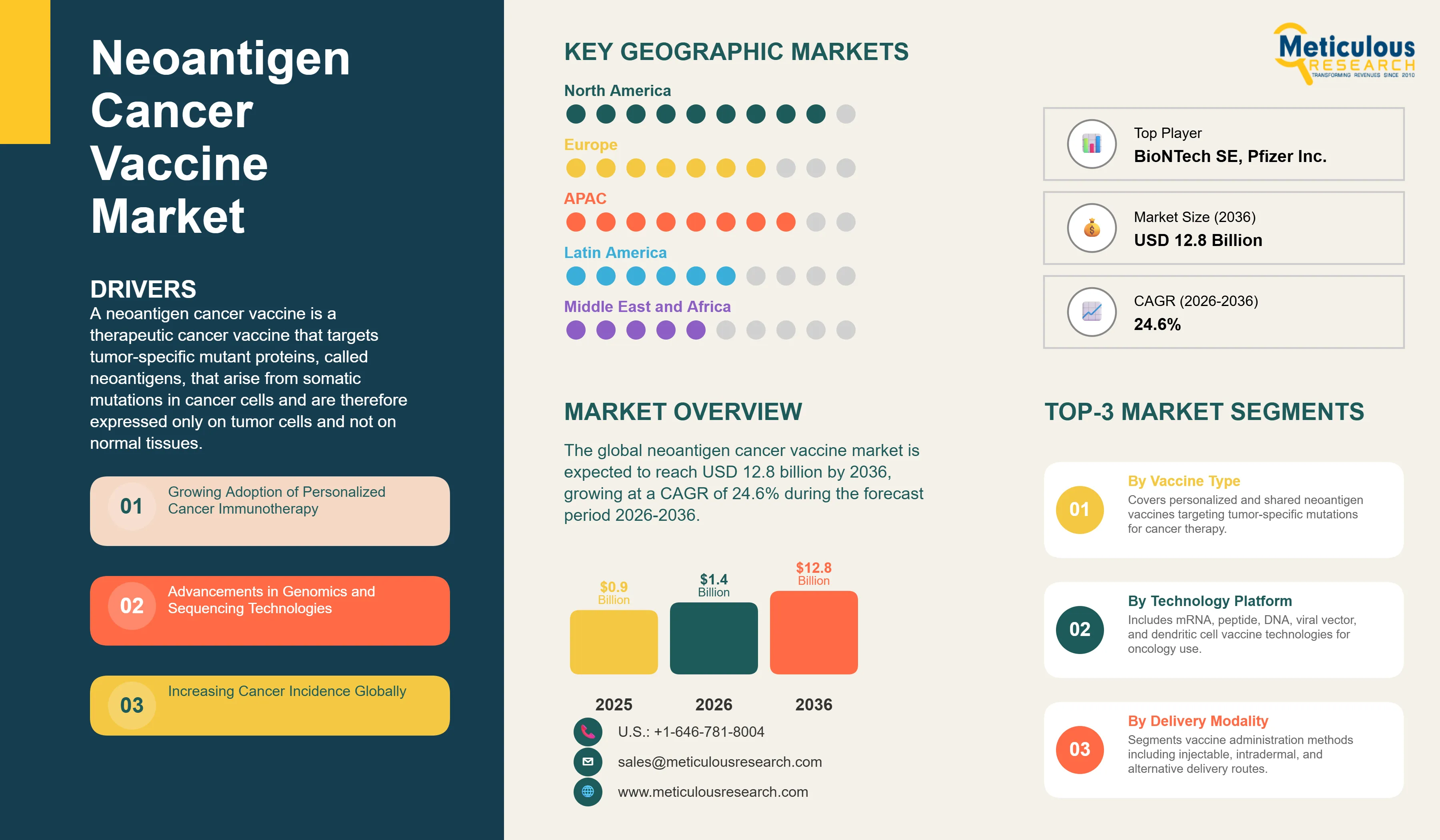

The global neoantigen cancer vaccine market was valued at USD 0.9 billion in 2025. This market is expected to reach USD 12.8 billion by 2036 from an estimated USD 1.4 billion in 2026, growing at a CAGR of 24.6% during the forecast period 2026-2036. The market's extraordinary growth rate reflects its position at the leading edge of cancer immunotherapy, where the landmark Phase 2b results of Moderna and Merck's mRNA-4157 (V940) individualized neoantigen vaccine combined with pembrolizumab demonstrated a 49% reduction in recurrence or death compared with pembrolizumab alone in resected Stage III-IV melanoma, reported at ASCO 2023 and further confirmed with updated data in 2024, establishing the clinical and commercial potential of personalized neoantigen vaccines for the first time in randomized controlled trial evidence.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

A neoantigen cancer vaccine is a therapeutic cancer vaccine that targets tumor-specific mutant proteins, called neoantigens, that arise from somatic mutations in cancer cells and are therefore expressed only on tumor cells and not on normal tissues. This tumor-exclusivity is the defining clinical advantage of neoantigen vaccines over earlier cancer vaccine approaches that targeted tumor-associated antigens also expressed on normal cells: because neoantigens are absent from normal tissues, vaccines against them can stimulate a strong anti-tumor immune response without the autoimmune risk that limits the therapeutic window of vaccines against shared tumor-associated antigens. In a personalized neoantigen vaccine program, a patient's tumor is biopsied and whole-exome sequenced alongside matched normal tissue, the somatic mutations unique to the tumor are computationally identified, algorithms predict which mutant peptides will bind to the patient's specific HLA immune presentation molecules and generate T cell responses, and a custom vaccine containing these predicted neoantigens is manufactured and administered to the patient within a window of weeks.

The market entered a transformational phase in 2023 when Moderna and Merck reported Phase 2b results from the KEYNOTE-942 trial of mRNA-4157 individualized neoantigen vaccine combined with pembrolizumab in resected melanoma. The trial demonstrated a 49% reduction in recurrence or death compared with pembrolizumab alone, with updated 3-year follow-up data presented at major oncology congresses in 2024 showing a sustained and deepening benefit, confirming that the personalized vaccine was generating durable tumor-specific immune memory. According to Moderna's 2025 annual report, the company received FDA Breakthrough Therapy Designation for mRNA-4157 in melanoma and has advanced into a Phase 3 program. BioNTech simultaneously advanced its BNT111 and BNT122 neoantigen vaccine programs, with BNT122 combined with pembrolizumab progressing through Phase 2 clinical trials in colorectal cancer and melanoma per BioNTech's 2025 pipeline communications.

The combination of mRNA vaccine platform advantages including rapid and modular manufacturing, very large antigen coding capacity, and strong immunogenicity with the clinical validation from the KEYNOTE-942 trial has generated extraordinary commercial and scientific momentum. According to PhRMA's 2025 annual report, cancer vaccines represent one of the most active areas of new clinical trial initiation in the oncology pipeline, with the neoantigen vaccine category specifically attracting the most new program initiations among therapeutic cancer vaccine approaches. The clinical development programs of Gritstone bio, Nouscom, ISA Pharmaceuticals, Vaccibody, and multiple academic consortia are collectively building a broad evidence base for neoantigen vaccine efficacy across melanoma, lung cancer, colorectal cancer, and other tumor types.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 12.8 Billion |

|

Market Size in 2026 |

USD 1.4 Billion |

|

Market Size in 2025 |

USD 0.9 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 24.6% |

|

Dominating Vaccine Type |

Personalized Neoantigen Vaccines |

|

Fastest Growing Vaccine Type |

Shared Neoantigen Vaccines |

|

Dominating Technology Platform |

mRNA-based Vaccines |

|

Fastest Growing Technology Platform |

AI-driven mRNA Vaccines |

|

Dominating Delivery Modality |

Injectable Vaccines |

|

Fastest Growing Delivery Modality |

Intradermal Delivery |

|

Dominating Clinical Stage |

Phase I |

|

Fastest Growing Clinical Stage |

Phase III |

|

Dominating Application |

Solid Tumors (Melanoma/Lung Cancer) |

|

Fastest Growing Application |

Combination Therapies with Checkpoint Inhibitors |

|

Dominating End User |

Biopharmaceutical Companies |

|

Fastest Growing End User |

Hospitals & Cancer Treatment Centers |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Moderna-Merck mRNA-4157 Phase 3 Program Defining the Commercial Pathway

The advancement of Moderna and Merck's mRNA-4157 individualized neoantigen vaccine into Phase 3 clinical development following the landmark KEYNOTE-942 Phase 2b results is the most commercially significant event in the neoantigen vaccine market's history, as it establishes a clear regulatory development pathway for the first time and provides the commercial framework against which all other neoantigen vaccine programs will be measured. The Phase 2b KEYNOTE-942 trial, first reported at ASCO 2023 and updated at major conferences in 2024, showed that mRNA-4157 plus pembrolizumab reduced the risk of recurrence or death by 49% versus pembrolizumab alone in resected high-risk melanoma. According to Moderna's 2025 annual report, the FDA's Breakthrough Therapy Designation for mRNA-4157 in melanoma provides priority review support and intensive FDA guidance for the Phase 3 program.

The manufacturing approach for mRNA-4157 requires that a custom mRNA vaccine encoding each patient's unique set of up to 34 neoantigens be designed, manufactured, quality-controlled, and delivered within approximately six weeks of tumor biopsy, using Moderna's mRNA synthesis and lipid nanoparticle formulation platform. According to Moderna's 2025 R&D update, the company has been investing in manufacturing capacity and automation to reduce the per-patient manufacturing time and cost, which are among the most significant barriers to eventual commercial deployment of personalized neoantigen vaccines. The potential approval of mRNA-4157 in melanoma, if Phase 3 results confirm the Phase 2b findings, would represent the first approved personalized cancer vaccine and the first approved neoantigen therapeutic, a milestone that would catalyze enormous commercial and clinical interest in the broader neoantigen vaccine category.

BioNTech Advancing Multiple Neoantigen Programs Across Tumor Types

BioNTech, which developed the BNT162b2 COVID-19 mRNA vaccine in partnership with Pfizer and retains world-leading mRNA manufacturing infrastructure and immunology expertise, has built one of the most comprehensive neoantigen and cancer vaccine pipelines globally, advancing multiple programs that address different tumor types, vaccine formulations, and combination strategies. BNT122, also known as autogene cevumeran, is BioNTech's personalized mRNA neoantigen vaccine that encodes up to 20 tumor-specific mutations per patient and is being developed in combination with checkpoint inhibitors. A Phase 2 clinical trial combining BNT122 with atezolizumab and mFOLFIRINOX in resected pancreatic ductal adenocarcinoma demonstrated that neoantigen-specific T cell responses could be generated in a difficult-to-treat tumor type, and these results were published in Nature in 2024.

According to BioNTech's 2025 annual report, the company reported revenues of approximately EUR 2.75 billion in 2024, with its oncology pipeline representing the primary investment focus for its post-COVID commercial build-out. BNT111, BioNTech's mRNA vaccine targeting shared melanoma antigens, is in Phase 2 clinical trials. BNT113, targeting HPV-positive head and neck squamous cell carcinoma, is in Phase 2. The breadth of BioNTech's cancer vaccine pipeline, spanning personalized neoantigen, shared neoantigen, and tumor antigen vaccine approaches across multiple tumor types, positions the company as one of the two most commercially advanced organizations in the neoantigen vaccine market alongside Moderna.

AI-driven Neoantigen Prediction Improving Vaccine Design Efficiency

The computational prediction of which tumor mutations will generate effective immune responses, specifically which mutant peptides will be presented by a patient's HLA molecules and which presented peptides will be recognized by T cells and stimulate an anti-tumor immune response, is the scientific bottleneck in neoantigen vaccine design and the area where AI is delivering the most commercially significant improvements. Conventional neoantigen prediction pipelines based on HLA binding affinity predictions alone have limited accuracy in identifying the neoantigens that will generate the strongest anti-tumor T cell responses, and a large proportion of predicted neoantigens in early clinical programs failed to generate the expected T cell responses.

According to Gritstone bio's 2025 clinical communications, its GRANITE and SLATE neoantigen vaccine programs use its proprietary EDGE neoantigen prediction algorithm, which trains on large datasets of T cell response data to improve the specificity of neoantigen selection. Gritstone reported in its 2025 publications that its AI-trained EDGE model demonstrates substantially higher T cell immunogenicity for predicted neoantigens compared with conventional HLA binding affinity-only prediction, providing evidence that AI-improved neoantigen selection translates into better vaccine immunogenicity. Researchers at the Broad Institute and Dana-Farber Cancer Institute published in Nature Methods in 2024 an AI model for neoantigen immunogenicity prediction that achieves accuracy significantly above conventional peptide-HLA binding prediction, with the model trained on T cell response data from neoantigen vaccine clinical trials, establishing the growing AI capability for neoantigen identification.

Growing Adoption of Personalized Cancer Immunotherapy

The paradigm of personalized cancer immunotherapy, in which each patient's treatment is tailored to the specific molecular characteristics of their individual tumor, is becoming the dominant approach in oncology and is creating the conceptual and commercial infrastructure for neoantigen vaccines. According to PhRMA's 2025 annual report, over 1,200 medicines are in clinical development in oncology, with precision immunotherapy representing the fastest-growing category. The clinical success of checkpoint inhibitors, which demonstrated that the immune system can eradicate advanced cancers when appropriately activated, established the immunotherapy framework that neoantigen vaccines are designed to complement and enhance by providing tumor-specific T cell targets to direct the checkpoint inhibitor-activated immune response. According to the American Society of Clinical Oncology's 2025 Clinical Cancer Advances report, neoantigen vaccines represent the most scientifically promising emerging category in cancer immunotherapy, with the KEYNOTE-942 results cited as the most significant proof-of-concept milestone in the field.

Advancements in Genomics and Sequencing Technologies

The feasibility of personalized neoantigen vaccine development is fundamentally dependent on the speed and cost of whole-exome sequencing of tumor and matched normal tissue to identify the somatic mutations that define each patient's unique set of neoantigens. According to the National Human Genome Research Institute's 2025 sequencing cost database, the cost of sequencing a human exome has fallen below USD 200, and the turnaround time for clinical whole-exome sequencing at major reference laboratories has been reduced to one to two weeks, making the sequencing step in the neoantigen vaccine workflow both cost-accessible and time-compatible with clinically meaningful vaccine delivery windows. Illumina's NovaSeq X platform, launched commercially in 2023 and becoming the standard for high-throughput clinical sequencing in 2024 and 2025, provides the sequencing throughput and quality needed for neoantigen vaccine programs at a cost and speed that supports commercial scaling.

Combination Therapies with Checkpoint Inhibitors

The combination of neoantigen vaccines with checkpoint inhibitors, which remove the immunosuppressive brakes that tumor microenvironments apply to anti-tumor T cells, is the most clinically validated and commercially advanced neoantigen vaccine strategy, with the KEYNOTE-942 trial results providing proof-of-concept that the combination produces synergistic clinical benefit. The scientific rationale is that neoantigen vaccines generate a large and diverse repertoire of tumor-specific T cells, while checkpoint inhibitors sustain and amplify the activity of these T cells by preventing immune exhaustion. According to Merck's 2025 clinical development communications, pembrolizumab is being studied in combination with multiple neoantigen vaccine programs beyond the mRNA-4157 collaboration with Moderna, reflecting the company's commercial and scientific commitment to checkpoint-neoantigen vaccine combination strategies.

Advances in AI-driven Neoantigen Prediction

The commercial opportunity from improved AI neoantigen prediction accuracy is that it directly improves vaccine immunogenicity by increasing the proportion of included neoantigens that generate productive T cell responses, and it reduces manufacturing complexity by allowing more confident selection of a smaller number of high-quality neoantigens rather than including many lower-confidence neoantigens to increase the probability of including effective ones. The Nature Methods 2024 publication from the Broad Institute demonstrating significantly improved neoantigen immunogenicity prediction accuracy from AI models trained on clinical trial T cell response data provides the scientific foundation for commercial AI neoantigen prediction platforms. Companies developing AI-enhanced neoantigen identification tools, including Gritstone bio's EDGE algorithm and several academic spin-out companies, are creating commercial value from this capability improvement.

By Vaccine Type: In 2026, Personalized Neoantigen Vaccines to Hold the Largest Share

Based on vaccine type, the global neoantigen cancer vaccine market is segmented into personalized neoantigen vaccines and shared neoantigen vaccines. In 2026, the personalized neoantigen vaccines segment is expected to account for the largest share of the global neoantigen cancer vaccine market. Personalized vaccines, which are designed from each individual patient's tumor mutational profile, represent the scientific and clinical core of the neoantigen vaccine field, as individually unique somatic mutations are the highest-quality neoantigen targets due to their complete absence from normal tissues. The Moderna-Merck mRNA-4157 program, the most clinically advanced neoantigen vaccine globally, is a personalized vaccine approach, and BioNTech's BNT122 autogene cevumeran is also personalized. These two programs collectively define the commercial frontier of the personalized vaccine segment.

However, the shared neoantigen vaccines segment is projected to register the highest CAGR during the forecast period. Shared neoantigens arise from mutations that occur recurrently across patients in the same tumor type, such as KRAS G12C in lung and colorectal cancer, and vaccines targeting these shared mutations can be manufactured as off-the-shelf products for all patients with that specific mutation, eliminating the complex and expensive personalized manufacturing requirement. The commercial appeal of shared neoantigen vaccines is their scalability: a single manufacturing run can produce vaccine doses for many patients, dramatically reducing per-patient costs compared with bespoke personalized manufacturing. Gritstone bio's SLATE program and several academic programs targeting recurrent cancer mutations represent this commercially scalable approach.

By Technology Platform: In 2026, mRNA-based Vaccines to Hold the Largest Share

Based on technology platform, the global neoantigen cancer vaccine market is segmented into mRNA-based vaccines, peptide-based vaccines, DNA-based vaccines, viral vector-based vaccines, and dendritic cell-based vaccines. In 2026, the mRNA-based vaccines segment is expected to account for the largest share of the global neoantigen cancer vaccine market and is also projected to register the highest growth during the forecast period, making it dominant on both measures. mRNA's advantages for neoantigen vaccines are profound: a single mRNA molecule can encode multiple neoantigens simultaneously up to the mRNA length limit, synthesis of customized mRNA sequences is highly automated and rapid, and lipid nanoparticle-formulated mRNA generates potent cellular immune responses including CD8+ cytotoxic T cells which are the primary anti-tumor effectors. The clinical validation from KEYNOTE-942 has cemented mRNA as the dominant platform, with Moderna and BioNTech's manufacturing infrastructure providing industrial-scale mRNA synthesis capability.

Peptide-based vaccines, which present synthetic versions of neoantigen peptides combined with adjuvants, represent a more established but also more immunologically flexible approach used by ISA Pharmaceuticals, Nouscom, and multiple academic programs. Viral vector-based approaches from Gritstone bio use adenoviral vectors to deliver neoantigen sequences with potent innate immune activation, and dendritic cell-based vaccines from academic programs offer highly personalized T cell priming.

By Delivery Modality: In 2026, Injectable Vaccines to Hold the Largest Share

Based on delivery modality, the global neoantigen cancer vaccine market is segmented into injectable vaccines, intradermal delivery, and other delivery methods. In 2026, the injectable vaccines segment is expected to account for the largest share of the global neoantigen cancer vaccine market. Intramuscular injection, which delivers mRNA-LNP formulations or adjuvanted peptides into muscle tissue for subsequent uptake by antigen-presenting cells, is the delivery route used in the Moderna-Merck mRNA-4157 program and in the majority of current neoantigen vaccine clinical trials. The established clinical infrastructure for intramuscular injection across oncology treatment settings makes this the most operationally accessible delivery approach.

However, the intradermal delivery segment is projected to register the highest CAGR during the forecast period. Intradermal injection delivers vaccine directly into the dermis, which is extraordinarily rich in professional antigen-presenting dendritic cells, potentially enabling stronger T cell priming responses per vaccine dose compared with intramuscular delivery. Multiple clinical programs for peptide-based neoantigen vaccines including ISA Pharmaceuticals' programs use intradermal delivery specifically for this immunological advantage, and growing clinical evidence supports intradermal routes as potentially superior for T cell vaccine immunogenicity.

By Clinical Stage: In 2026, Phase I to Hold the Largest Share

Based on clinical stage, the global neoantigen cancer vaccine market is segmented into preclinical, Phase I, Phase II, and Phase III. In 2026, the Phase I segment is expected to account for the largest share of the global neoantigen cancer vaccine market by number of active programs, reflecting the field's current stage of development where most programs are still in early clinical evaluation. The large number of Phase I neoantigen vaccine trials globally, across diverse tumor types and vaccine platforms, reflects the extraordinary scientific interest and investment the KEYNOTE-942 results generated. According to ClinicalTrials.gov's 2025 database, the number of registered neoantigen vaccine clinical trials exceeded 80 active studies, the majority in Phase I.

However, the Phase III segment is projected to register the highest CAGR during the forecast period, growing from a current base of one program, namely the Moderna-Merck mRNA-4157 melanoma Phase 3 study, to potentially several programs by 2036 as successful Phase 2 results mature into Phase 3 investments. According to Moderna's 2025 annual report, the mRNA-4157 Phase 3 program in melanoma is actively enrolling, and Moderna has disclosed plans to expand neoantigen vaccine Phase 2 programs in lung cancer and other tumor types that could advance to Phase 3 within the forecast period.

By Application: In 2026, Solid Tumors to Hold the Largest Share

Based on application, the global neoantigen cancer vaccine market is segmented into solid tumors (lung cancer, melanoma, breast cancer, colorectal cancer, and other solid tumors), hematological cancers (leukemia, lymphoma, and multiple myeloma), and combination therapies. In 2026, the solid tumors segment is expected to account for the largest share of the global neoantigen cancer vaccine market. Solid tumors have been the primary focus of neoantigen vaccine development because high tumor mutational burden tumors such as melanoma, non-small cell lung cancer, and microsatellite instability-high colorectal cancer provide the richest neoantigen landscapes for vaccine targeting, with the highest number of unique tumor-specific mutations available for vaccine design. According to the American Cancer Society’s 2025 Cancer Facts & Figures, about 212,200 new melanoma cases are expected in the United States in 2025, providing a large patient population for Moderna-Merck’s melanoma program.

However, the combination therapies segment is projected to register the highest CAGR during the forecast period. The clinical validation of neoantigen vaccines in combination with pembrolizumab from the KEYNOTE-942 trial has established combination with checkpoint inhibitors as the standard development approach for neoantigen vaccines, with virtually every advanced clinical program now designed as a combination strategy. The commercial logic is that checkpoint inhibitors are already standard of care in many tumor types, meaning that adding a neoantigen vaccine to existing standard therapy is the most clinically and regulatorily accessible development pathway.

By End User: In 2026, Biopharmaceutical Companies to Hold the Largest Share

Based on end user, the global neoantigen cancer vaccine market is segmented into hospitals and cancer treatment centers, research institutes, and biopharmaceutical companies. In 2026, the biopharmaceutical companies segment is expected to account for the largest share of the global neoantigen cancer vaccine market. Pharmaceutical companies are the primary funders, developers, and commercial deployers of neoantigen vaccine programs, with Moderna, BioNTech, Merck, Roche, AstraZeneca, and several specialist oncology companies each investing substantially in neoantigen vaccine development programs. The scale of biopharma investment is reflected in Moderna's 2025 annual report disclosing very significant R&D investment in its individualized neoantigen vaccine programs, and BioNTech's 2025 communications confirming oncology vaccines as the primary pipeline focus for its post-COVID commercial strategy.

However, the hospitals and cancer treatment centers segment is projected to register the highest CAGR during the forecast period. As neoantigen vaccine programs advance toward potential commercial approval, cancer centers with advanced molecular oncology capabilities, tumor sequencing infrastructure, and academic-commercial research partnerships will become the primary clinical deployment points for neoantigen vaccines. Major cancer centers including Memorial Sloan Kettering, MD Anderson, and the Dana-Farber Cancer Institute are all active clinical trial sites for leading neoantigen vaccine programs and are building the clinical capabilities to become early adopters of approved neoantigen therapies.

Neoantigen Cancer Vaccine Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global neoantigen cancer vaccine market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global neoantigen cancer vaccine market. The United States is the center of global neoantigen vaccine development, home to Moderna, Merck, and Gritstone bio as the three most commercially advanced neoantigen vaccine organizations, and to the majority of global clinical trial activity in the field. According to Moderna's 2025 annual report, the mRNA-4157 Phase 3 program is based primarily in U.S. clinical centers, and the FDA's Breakthrough Therapy Designation provides additional regulatory support for U.S.-first commercial deployment. The U.S. National Cancer Institute is a significant funder of neoantigen vaccine research through its Cancer Immunotherapy Trials Network, and academic programs at Johns Hopkins, Memorial Sloan Kettering, Dana-Farber, and MD Anderson are conducting multiple early-phase neoantigen vaccine studies. According to the American Cancer Society's 2025 Cancer Facts and Figures, approximately 2 million new cancer cases are expected in the U.S. in 2025, providing the clinical population for ongoing and expanding neoantigen vaccine trial programs.

However, the Asia-Pacific neoantigen cancer vaccine market is expected to grow at the fastest CAGR during the forecast period. Asia-Pacific carries approximately 49% of global cancer cases per the WHO's World Cancer Report 2024, providing an enormous patient population that makes the region commercially critical for neoantigen vaccine development and eventual commercialization. China's biopharmaceutical industry has invested substantially in cancer vaccine development, with domestic companies including Zymeworks China, BioMap, and several oncology-focused biotechnology companies developing neoantigen vaccine programs. Japan's leading cancer centers and its national cancer genomics program are supporting early neoantigen vaccine clinical activities. South Korea's advanced biopharmaceutical industry is investing in cancer immunotherapy including vaccine approaches. According to BioNTech's 2025 communications, the company is expanding its clinical trial network into Asian cancer centers for its BNT122 and other cancer vaccine programs, reflecting the commercial importance of Asian patient populations for neoantigen vaccine clinical development.

Europe is a strong scientific and regulatory contributor to the neoantigen vaccine field. BioNTech SE, headquartered in Mainz, Germany, is one of the two global leaders in neoantigen vaccine development, and the company's European manufacturing infrastructure provides the mRNA synthesis and LNP formulation capability for its neoantigen vaccine programs. ISA Pharmaceuticals, headquartered in the Netherlands, is a leading peptide-based cancer vaccine company with multiple neoantigen vaccine programs in clinical development. Vaccibody, headquartered in Norway, is developing a DNA-based neoantigen vaccine platform. Nouscom, headquartered in Basel, Switzerland, is advancing a viral vector-based neoantigen vaccine program. The European Medicines Agency's engagement with neoantigen vaccine regulatory frameworks, and the EU's Cancer Mission research funding supporting cancer immunotherapy including vaccine approaches, provide the regulatory and funding infrastructure for European neoantigen vaccine development.

The neoantigen cancer vaccine market is served by large pharmaceutical companies with the clinical development scale and commercial infrastructure to advance personalized cancer vaccines through Phase 3 trials, specialist oncology biotechnology companies with proprietary neoantigen prediction and vaccine platform capabilities, and genomics and bioinformatics companies providing the sequencing and computational infrastructure for neoantigen identification. Competition is based on clinical evidence of efficacy, vaccine platform immunogenicity and manufacturing scalability, neoantigen prediction algorithm performance, turnaround time from biopsy to vaccine delivery, and the breadth of tumor types being addressed.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' clinical pipeline stage, platform capabilities, regulatory milestones, and recent strategic developments. Some of the key players operating in the global neoantigen cancer vaccine market include Moderna Inc. (U.S.), BioNTech SE (Germany), Genentech/Roche (U.S./Switzerland), Gritstone bio Inc. (U.S.), Neon Therapeutics (U.S.), CureVac N.V. (Germany), AstraZeneca plc (UK), Merck & Co. Inc. (U.S.), Pfizer Inc. (U.S.), Immatics N.V. (Germany), ISA Pharmaceuticals B.V. (Netherlands), Vaccibody AS (Norway), Nouscom AG (Switzerland), Genocea Biosciences (U.S.), and Advaxis Inc. (U.S.), among others.

The global neoantigen cancer vaccine market is expected to reach USD 12.8 billion by 2036 from an estimated USD 1.4 billion in 2026, at a CAGR of 24.6% during the forecast period 2026-2036.

In 2026, the personalized neoantigen vaccines segment is expected to hold the largest share, reflecting personalized vaccines being the scientifically validated approach with the most commercially advanced programs including Moderna's mRNA-4157 and BioNTech's BNT122, both representing individually customized vaccines designed from each patient's unique tumor mutational profile.

The mRNA-based vaccines segment dominates both in current market share and projected growth rate, driven by the clinical validation from KEYNOTE-942, mRNA's ability to encode multiple neoantigens simultaneously, rapid automated synthesis for personalized manufacturing, and the world-class mRNA manufacturing infrastructure of Moderna and BioNTech that no other vaccine platform can match at comparable scale.

The market is primarily driven by the KEYNOTE-942 Phase 2b results demonstrating 49% reduction in recurrence or death that provided the first randomized clinical validation of neoantigen vaccine efficacy, Moderna's FDA Breakthrough Therapy Designation and Phase 3 program entry per its 2025 annual report, NHGRI's 2025 data showing whole-exome sequencing costs below USD 200 enabling cost-effective neoantigen identification, and over 80 active neoantigen vaccine clinical trials per ClinicalTrials.gov 2025 data confirming broad pipeline momentum.

Key players are Moderna Inc. (U.S.), BioNTech SE (Germany), Genentech/Roche (U.S./Switzerland), Gritstone bio Inc. (U.S.), Neon Therapeutics (U.S.), CureVac N.V. (Germany), AstraZeneca plc (UK), Merck & Co. Inc. (U.S.), Pfizer Inc. (U.S.), Immatics N.V. (Germany), ISA Pharmaceuticals B.V. (Netherlands), Vaccibody AS (Norway), Nouscom AG (Switzerland), Genocea Biosciences (U.S.), and Advaxis Inc. (U.S.), among others.

Asia-Pacific is expected to register the highest growth rate during the forecast period 2026-2036, driven by the WHO's World Cancer Report 2024 identifying Asia as carrying approximately 49% of global cancer cases, China's growing domestic neoantigen vaccine development industry, BioNTech's 2025 expansion of its cancer vaccine clinical trial network into Asian centers, and Japan and South Korea's advanced biopharmaceutical industries investing in cancer immunotherapy.

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Market Ecosystem

1.4 Currency and Limitations

1.4.1 Currency

1.4.2 Limitations

1.5 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation

2.2.1 Secondary Research

2.2.2 Primary Research (Oncologists, Biopharma, Researchers, CROs)

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Forecast Modeling

2.4 Data Triangulation

2.5 Assumptions

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Growing Adoption of Personalized Cancer Immunotherapy

4.2.1.2 Advancements in Genomics and Sequencing Technologies

4.2.1.3 Increasing Cancer Incidence Globally

4.2.1.4 Strong Pipeline of Neoantigen Vaccine Candidates

4.2.2 Restraints

4.2.2.1 High Cost of Personalized Vaccine Development

4.2.2.2 Complex Manufacturing and Logistics

4.2.2.3 Limited Commercial Approvals

4.2.3 Opportunities

4.2.3.1 Combination Therapies with Checkpoint Inhibitors

4.2.3.2 Advances in AI-driven Neoantigen Prediction

4.2.3.3 Expansion in mRNA Vaccine Platforms

4.2.3.4 Growth in Clinical Trials

4.2.4 Challenges

4.2.4.1 Regulatory Complexity

4.2.4.2 Variability in Patient-specific Responses

4.3 Technology Landscape

4.3.1 mRNA-based Neoantigen Vaccines

4.3.2 Peptide-based Vaccines

4.3.3 DNA-based Vaccines

4.3.4 Viral Vector-based Vaccines

4.3.5 Dendritic Cell-based Vaccines

4.3.6 AI & Bioinformatics for Neoantigen Identification

4.4 Neoantigen Vaccine Ecosystem

4.4.1 Biopharmaceutical Companies

4.4.2 Genomics & Sequencing Providers

4.4.3 CROs & CDMOs

4.4.4 Research Institutes

4.4.5 Healthcare Providers

4.5 Value Chain Analysis

4.5.1 Tumor Sample Collection

4.5.2 Genomic Sequencing & Analysis

4.5.3 Neoantigen Identification & Selection

4.5.4 Vaccine Design & Manufacturing

4.5.5 Clinical Administration

4.6 Regulatory Landscape

4.6.1 FDA & EMA Guidelines

4.6.2 Clinical Trial Regulations

4.6.3 Personalized Medicine Regulatory Frameworks

4.7 Industry Trends

4.7.1 Rise of mRNA-based Cancer Vaccines

4.7.2 Increasing Collaboration Between Pharma & Tech Firms

4.7.3 Growth of Personalized Oncology

4.7.7 Integration of AI in Vaccine Design

4.8 Cost and Pricing Analysis

4.8.1 Cost per Patient

4.8.2 Manufacturing Cost Analysis

4.8.3 Reimbursement Challenges

5. Neoantigen Cancer Vaccine Market, by Vaccine Type

5.1 Introduction

5.2 Personalized Neoantigen Vaccines

5.3 Shared Neoantigen Vaccines

6. Neoantigen Cancer Vaccine Market, by Technology Platform

6.1 mRNA-based Vaccines

6.2 Peptide-based Vaccines

6.3 DNA-based Vaccines

6.4 Viral Vector-based Vaccines

6.5 Dendritic Cell-based Vaccines

7. Neoantigen Cancer Vaccine Market, by Delivery Modality

7.1 Injectable Vaccines

7.2 Intradermal Delivery

7.3 Other Delivery Methods

8. Neoantigen Cancer Vaccine Market, by Clinical Stage

8.1 Preclinical

8.2 Phase I

8.3 Phase II

8.4 Phase III

9. Neoantigen Cancer Vaccine Market, by Application

9.1 Introduction

9.2 Solid Tumors

9.2.1 Lung Cancer

9.2.2 Melanoma

9.2.3 Breast Cancer

9.2.4 Colorectal Cancer

9.2.5 Other Solid Tumors

9.3 Hematological Cancers

9.3.1 Leukemia

9.3.2 Lymphoma

9.3.3 Multiple Myeloma

9.4 Combination Therapies

10. Neoantigen Cancer Vaccine Market, by End User

10.1 Hospitals & Cancer Treatment Centers

10.2 Research Institutes

10.3 Biopharmaceutical Companies

11. Neoantigen Cancer Vaccine Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Italy

11.3.5 Spain

11.3.6 Netherlands

11.3.7 Sweden

11.3.8 Switzerland

11.3.9 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 Japan

11.4.3 India

11.4.4 South Korea

11.4.5 Australia

11.4.6 Singapore

11.4.7 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Rest of MEA

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Emerging Players

12.5 Market Ranking/Positioning Analysis

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Moderna, Inc.

13.2 BioNTech SE

13.3 Genentech (Roche)

13.4 Gritstone bio, Inc.

13.5 Neon Therapeutics

13.6 CureVac N.V.

13.7 AstraZeneca plc

13.8 Merck & Co., Inc.

13.9 Pfizer Inc.

13.10 Immatics N.V.

13.11 ISA Pharmaceuticals B.V.

13.12 Vaccibody AS

13.13 Nouscom AG

13.14 Genocea Biosciences

13.15 Advaxis Inc.

14. Appendix

14.1 Customization Options

14.2 Related Reports

Published Date: Jun-2026

Published Date: Jun-2025

Published Date: Jan-2025

Published Date: Jul-2024

Subscribe to get the latest industry updates