Resources

About Us

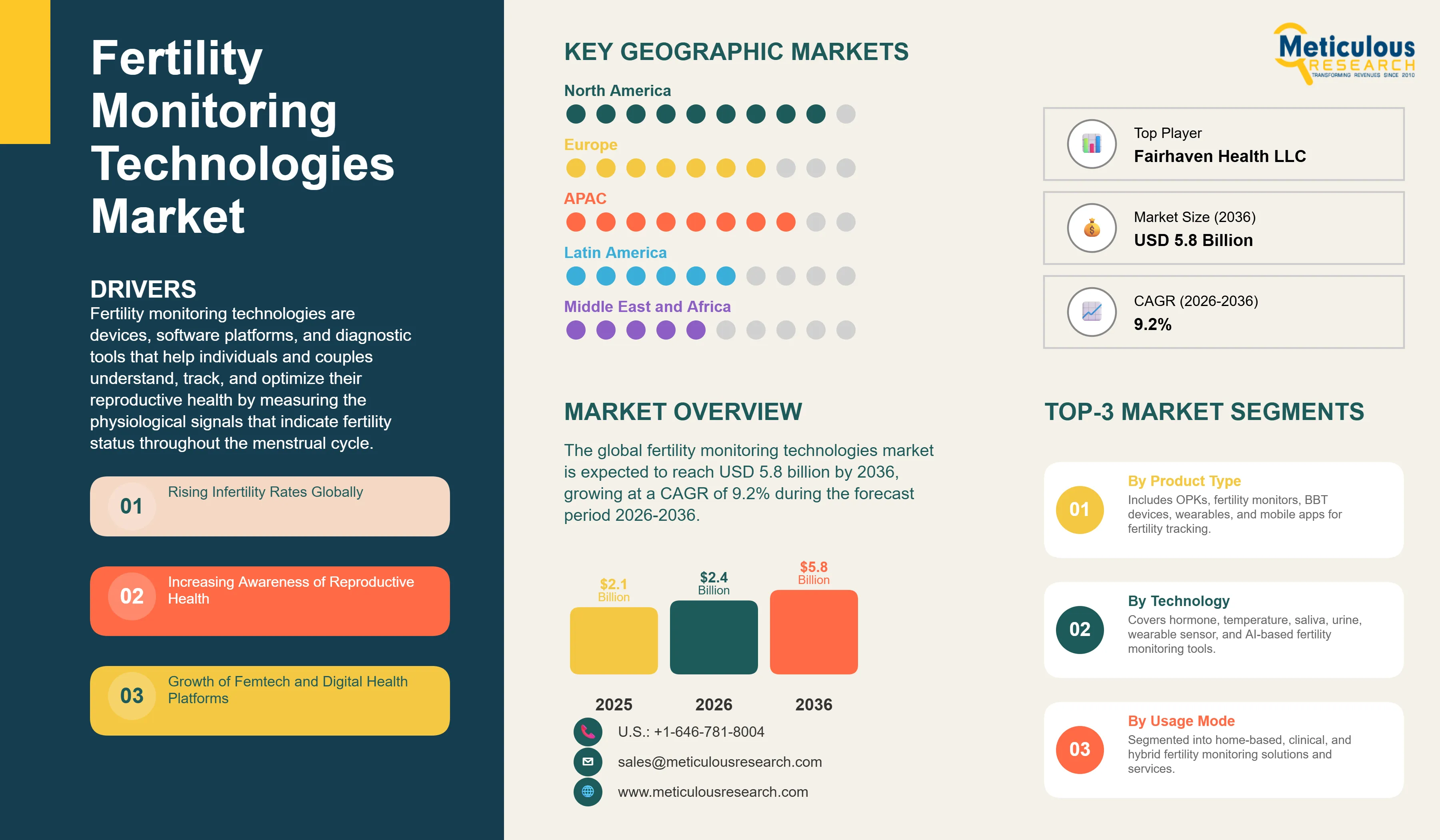

Fertility Monitoring Technologies Market Size, Share & Trends Analysis by Product Type, Technology, Usage Mode, Application, and End User - Global Opportunity Analysis & Industry Forecast (2026-2036)

Report ID: MRHC - 1041975 Pages: 310 May-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global fertility monitoring technologies market was valued at USD 2.1 billion in 2025. This market is expected to reach USD 5.8 billion by 2036 from an estimated USD 2.4 billion in 2026, growing at a CAGR of 9.2% during the forecast period 2026-2036. According to the World Health Organization’s 2023 infertility report, about 1 in 6 adults globally, roughly 17.5%, experience infertility at some point in their lives, supporting strong and growing demand for fertility care and monitoring tools ranging from ovulation kits to hormone-tracking wearables and AI-based fertility apps.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Fertility monitoring technologies are devices, software platforms, and diagnostic tools that help individuals and couples understand, track, and optimize their reproductive health by measuring the physiological signals that indicate fertility status throughout the menstrual cycle. At the simplest level, an ovulation prediction kit detects the surge in luteinizing hormone in urine that precedes ovulation by 24 to 36 hours, providing a reliable short-term fertility window signal. At the most sophisticated end, continuous wearable devices monitor basal body temperature, heart rate variability, skin conductance, and breathing patterns throughout the night to build personalized fertility window predictions calibrated to each user's unique hormonal cycle patterns, with AI algorithms that improve prediction accuracy over multiple cycles of data collection.

The market is growing because the structural drivers are broad, well-established, and intensifying. According to the WHO's infertility report, approximately 1 in 6 people are affected by infertility globally, representing approximately 17.5% of the adult population. The global trend toward delayed childbearing, with the average age of first childbirth rising in most developed countries, is both increasing the proportion of couples experiencing fertility challenges due to age-related decline and extending the period during which fertility awareness is commercially relevant. According to the Centers for Disease Control and Prevention's 2025 National Survey of Family Growth, approximately 12% of U.S. women aged 15 to 44 have used fertility monitoring or ovulation testing services, establishing a large and growing domestic market.

The femtech industry's rapid growth is a particularly important commercial context. Natural Cycles, the first FDA-cleared digital contraceptive app using algorithm-based fertility prediction, reported over 4 million users globally according to its 2025 annual report, demonstrating the scale of consumer appetite for evidence-based digital fertility solutions. Ava Science's FDA-cleared wearable fertility tracker has been peer-reviewed and validated in multiple clinical studies, establishing the clinical credibility of multi-sensor wearable fertility monitoring. The convergence of validated clinical evidence and consumer-friendly design across multiple product categories is progressively elevating the entire fertility monitoring market from a commodity-driven OPK market toward a higher-value, tech-enabled personalized health category.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 5.8 Billion |

|

Market Size in 2026 |

USD 2.4 Billion |

|

Market Size in 2025 |

USD 2.1 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 9.2% |

|

Dominating Product Type |

Ovulation Prediction Kits (OPKs) |

|

Fastest Growing Product Type |

Wearable Fertility Tracking Devices |

|

Dominating Technology |

Hormone-based Detection (LH, Estrogen) |

|

Fastest Growing Technology |

AI-based Predictive Analytics |

|

Dominating Usage Mode |

Home-based Monitoring |

|

Fastest Growing Usage Mode |

Hybrid Models |

|

Dominating Application |

Ovulation Tracking & Fertility Planning |

|

Fastest Growing Application |

Infertility Diagnosis & Treatment Support |

|

Dominating End User |

Individuals / Consumers |

|

Fastest Growing End User |

Fertility Clinics |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Natural Cycles and Ava Establishing FDA Clearance as Competitive Standard

The regulatory landscape for digital fertility monitoring has been fundamentally shaped by two landmark FDA clearances that have elevated the evidentiary standard across the category. Natural Cycles received FDA De Novo clearance in August 2018 as the first and only FDA-cleared contraceptive app. According to Natural Cycles' 2025 annual report, the company had over 4 million registered users globally, with its algorithm validated in multiple peer-reviewed studies with typical-use effectiveness comparable to hormonal contraception in motivated users.

Ava Science's fertility tracker wristband received FDA 510(k) clearance as a Class II medical device and was validated in a peer-reviewed clinical study published in Reproductive Biology and Endocrinology, which found that Ava correctly identified an average of 5.3 fertile days per cycle with 89% accuracy compared with standardized hormone testing. These clearances are setting a new commercial standard: consumer fertility monitors without clinical validation are increasingly viewed with scepticism by healthcare providers and sophisticated consumers, creating market differentiation between clinically validated premium products and commodity solutions.

Quantitative Hormone Monitoring Transforming Ovulation Prediction Precision

The emergence of quantitative hormone monitoring devices that measure specific hormone concentrations rather than providing simple positive or negative LH surge results is transforming fertility window identification precision. Mira's fertility analyzer quantifies LH and FSH concentrations using a handheld analyzer and urine test wands, providing women with their personal hormone curves rather than a generic threshold-based result. According to Mira's 2025 product communications, the device measures LH concentrations in quantitative units, identifying up to six potentially fertile days per cycle compared with the two to three days typically identified by conventional LH strip tests.

Proov's progesterone test strips assess the post-ovulatory rise in progesterone metabolites as a measure of ovulation quality, filling a clinical gap by confirming whether ovulation actually occurred and whether it was of sufficient quality to support implantation. According to Proov's 2025 clinical evidence communications, testing progesterone after the presumed ovulation date identifies clinically meaningful progesterone insufficiency in a proportion of women with regular cycles, providing actionable information for both fertility planning and clinical consultation decisions.

Femtech Investor Momentum Reshaping the Competitive Landscape

The femtech sector has attracted growing investor and corporate attention that is reshaping the fertility monitoring competitive landscape through acquisitions, partnerships, and significant funding rounds. PitchBook’s 2025 FemTech VC market snapshot indicates that femtech attracted about $1.2 billion in venture investment in 2024 and roughly $5.4 billion since 2020, with fertility remaining a major area of investor interest. Modern Fertility's acquisition by Ro and LetsGetChecked's expansion of its women's health and fertility testing offerings reflect the convergence of fertility monitoring into broader digital health platforms.

According to Flo Health's 2025 communications, the company had over 70 million users globally, representing the largest single digital women's health platform by user scale. Flo's integration of fertility tracking within its broader menstrual and reproductive health platform demonstrates how fertility monitoring is becoming embedded in comprehensive women's health digital ecosystems rather than remaining a standalone product category, creating strong cross-sell and engagement dynamics that support subscription revenue models.

Rising Infertility Rates Globally

According to the World Health Organization's report on infertility, approximately 1 in 6 people globally experience infertility, representing approximately 17.5% of the adult population. In the United States, the CDC's 2025 National Survey of Family Growth estimated approximately 12% of women aged 15 to 44 have experienced difficulty getting pregnant or carrying a pregnancy to term. The CDC also reported the average age of first birth in the United States at 27.5 years in 2024, up from 21.4 years in 1970, with the growing proportion of conceptions attempted after age 35 creating a larger population with both higher clinical need for fertility monitoring and higher awareness of fertility tracking tools.

Growth of Femtech and Digital Health Platforms

PitchBook’s 2025 femtech investment snapshot indicates that femtech attracted about $1.2 billion in 2024, with fertility monitoring and reproductive health among the leading investment areas. Consumer platforms such as Natural Cycles and Flo Health also show the scale of engagement in this segment, with large registered-user bases supporting broad distribution for fertility monitoring technologies.

Integration with AI and Predictive Analytics

AI algorithms trained on large longitudinal datasets of menstrual cycle parameters, hormonal measurements, and fertility outcomes can identify individual cycle patterns and predict fertile windows with accuracy calibrated to each user's specific physiology rather than population averages. According to Natural Cycles' 2025 clinical evidence publications, its algorithm's prediction accuracy improves with each additional cycle of data collected from a user. Flo Health has published peer-reviewed research demonstrating AI model improvements in period and ovulation prediction that significantly reduce prediction errors compared with calendar-based methods, providing clinical validation evidence for AI-enhanced fertility monitoring.

Increasing Adoption of Wearables

Ava Science's wrist-worn sensor uses nine physiological parameters including skin temperature, pulse rate, breathing rate, and heart rate variability to predict the fertile window, with a clinical study published in Reproductive Biology and Endocrinology confirming accuracy comparable to hormone-based monitoring. Tempdrop's basal body temperature sensor, worn on the upper arm during sleep and using a proprietary algorithm to correct for variable sleep timing, is specifically designed for women with irregular schedules. According to Tempdrop's 2025 user community data, its devices are particularly valued by night-shift workers, breastfeeding mothers, and women with highly irregular cycles who have not been well served by conventional BBT monitoring.

By Product Type: In 2026, Ovulation Prediction Kits (OPKs) to Hold the Largest Share

Based on product type, the global fertility monitoring technologies market is segmented into ovulation prediction kits, fertility monitors (digital devices), basal body temperature devices, wearable fertility tracking devices, and mobile apps and software platforms. In 2026, the ovulation prediction kits segment is expected to account for the largest share of the global fertility monitoring technologies market. OPKs are the most universally used fertility monitoring product, with broad retail availability, very low per-test cost, and decades of established clinical evidence. Clearblue's digital ovulation tests, which detect both LH and estrogen to provide a wider fertility window indication than LH-only tests, represent the dominant premium OPK brand globally. The accessibility and affordability of OPKs make them the entry point for the majority of women beginning fertility tracking, sustaining their dominant market share.

However, the wearable fertility tracking devices segment is projected to register the highest CAGR during the forecast period. Continuous wearable monitoring that provides passive, user-friendly fertility tracking without daily test administration is the fastest-growing premium product category, driven by the clinical validation of Ava Science's FDA-cleared tracker, growing consumer comfort with health wearables, and the appeal of multi-parameter physiological monitoring. The rapidly declining cost of wearable sensor hardware is progressively making premium wearable fertility trackers accessible at price points that a growing proportion of consumers can afford.

By Technology: In 2026, Hormone-based Detection to Hold the Largest Share

Based on technology, the global fertility monitoring technologies market is segmented into hormone-based detection, temperature-based monitoring, saliva-based testing, urine-based testing, sensor-based and wearable monitoring, and AI-based predictive analytics. In 2026, the hormone-based detection segment is expected to account for the largest share of the global fertility monitoring technologies market. Hormonal biomarkers, particularly LH which surges 24 to 36 hours before ovulation, provide the most clinically validated fertility signals available outside a clinical laboratory. Clearblue's digital hormone monitors, which simultaneously detect urinary LH and estrogen metabolite levels to provide a fertility window of up to six days per cycle, represent the most commercially successful hormone-based detection product globally.

However, the AI-based predictive analytics segment is projected to register the highest CAGR during the forecast period. AI fertility prediction platforms that integrate data from multiple monitoring modalities to generate personalized fertility predictions represent the fastest-growing technology category. Natural Cycles' FDA-cleared algorithm and Flo Health's AI prediction models are the leading commercial implementations, with combined disclosed user bases in the tens of millions that provide large-scale training data for continuous accuracy improvement.

By Usage Mode: In 2026, Home-based Monitoring to Hold the Largest Share

Based on usage mode, the global fertility monitoring technologies market is segmented into home-based monitoring, clinical monitoring, and hybrid models. In 2026, the home-based monitoring segment is expected to account by far the largest share of the global fertility monitoring technologies market. The entire consumer fertility monitoring market operates primarily in the home setting, and the fundamental value proposition of fertility monitoring technology is enabling users to access fertility health information privately and conveniently without requiring clinical appointments. Natural Cycles' over 4 million users and Flo Health's over 70 million users reflect the enormous consumer scale of this home-based segment.

However, the hybrid models segment is projected to register the highest CAGR during the forecast period. Hybrid approaches that combine home-based monitoring with clinical interpretation, telehealth consultations, and integration with fertility clinic electronic health records are growing as fertility monitoring technologies develop clinical-grade capabilities relevant to healthcare providers. Platforms that allow a woman to share her fertility monitoring data with her reproductive endocrinologist during a telehealth consultation bridge the consumer and clinical domains in ways that are creating a new and fast-growing hybrid commercial segment.

By Application: In 2026, Ovulation Tracking & Fertility Planning to Hold the Largest Share

Based on application, the global fertility monitoring technologies market is segmented into ovulation tracking and fertility planning, infertility diagnosis and treatment support, contraception and natural family planning, pregnancy planning and preconception health, and male fertility monitoring. In 2026, the ovulation tracking and fertility planning segment is expected to account for the largest share of the global fertility monitoring technologies market. Couples actively trying to conceive represent the most motivated and highest-spending user group, with willingness to purchase multiple monitoring modalities, premium devices, and subscription analytics services to maximize their probability of conception. This is the application for which the market was originally designed and where the commercial evidence base is most extensive.

However, the infertility diagnosis and treatment support segment is projected to register the highest CAGR during the forecast period. The very large and growing population seeking clinical fertility treatment, combined with the growing integration of home monitoring data into clinical fertility workflows, is creating a fast-growing segment that commands premium pricing. Quantitative hormone monitoring devices like Mira that provide data directly relevant to clinical fertility assessment, and wearables validated for use in IVF monitoring protocols, are gaining traction in this higher-value clinical support application category.

By End User: In 2026, Individuals / Consumers to Hold the Largest Share

Based on end user, the global fertility monitoring technologies market is segmented into individuals and consumers, fertility clinics, hospitals, and diagnostic laboratories. In 2026, the individuals and consumers segment is expected to account for the largest share of the global fertility monitoring technologies market. The direct-to-consumer fertility monitoring market, encompassing OPK retail sales, fertility app subscriptions, wearable device sales, and at-home hormone testing kits, is far larger in aggregate revenue than institutional procurement. Natural Cycles' over 4 million users and Flo Health's over 70 million users represent the enormous consumer scale that generates recurring subscription revenues and device sales far exceeding clinical institutional procurement.

However, the fertility clinics segment is projected to register the highest CAGR during the forecast period. Fertility clinics are increasingly integrating digital monitoring tools into their clinical protocols, using quantitative hormone monitoring devices for remote cycle monitoring during IVF stimulation, prescribing FDA-cleared fertility tracking apps as part of natural cycle monitoring protocols, and adopting wearable sensors for continuous patient monitoring between clinic visits. The growing clinical validation of home fertility monitoring devices and the efficiency gains for fertility clinics from using validated home monitoring data to reduce the frequency of clinic-based monitoring appointments are driving above-average growth in this segment.

Fertility Monitoring Technologies Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global fertility monitoring technologies market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global fertility monitoring technologies market. The United States is the world's most commercially advanced fertility monitoring market, with the highest consumer awareness and adoption, the most active regulatory framework including FDA clearances for Natural Cycles and Ava Science, and a very large population of reproductive-age women actively managing fertility. According to the CDC's 2025 National Survey of Family Growth, approximately 12% of U.S. women aged 15 to 44 have used fertility monitoring services, representing tens of millions of women. The CDC also reported the average age of first birth in the U.S. at 27.5 years in 2024, reflecting the delayed childbearing trend that expands demand. The high consumer willingness to pay premium prices for validated fertility monitoring devices makes the U.S. the highest per-user revenue market globally.

However, the Asia-Pacific fertility monitoring technologies market is expected to grow at the fastest CAGR during the forecast period. Asia-Pacific combines very large populations with growing consumer health awareness, rising disposable incomes, high smartphone penetration enabling mobile fertility app adoption, and structural demographic pressures including declining birth rates in Japan, South Korea, China, and Singapore that are making fertility monitoring a government and healthcare priority. Japan's government announced fertility treatment subsidies in 2025, creating government-supported demand for reproductive health services. South Korea faces among the world's lowest total fertility rates, with Statistics Korea 2025 data confirming the continued birth rate decline, creating strong societal demand for reproductive health support. China's government promotion of higher birth rates and its policy of supporting fertility planning services is creating government-level demand signals for fertility monitoring adoption. India's very large reproductive-age population and rapidly growing urban middle class with increasing health technology awareness are creating a large and growing OPK and fertility app market.

Europe is a technically advanced and regulation-active fertility monitoring market where Natural Cycles, founded in Sweden, maintains strong market penetration. The UK, Germany, France, and Sweden are the largest European fertility monitoring markets, with high consumer health technology adoption, well-developed pharmacy retail channels, and growing integration of digital fertility tools into gynecological clinical practice. According to Pitchbook's 2025 data, the European femtech ecosystem supported by active investor communities in London, Berlin, and Stockholm continues generating new fertility monitoring companies and products. Latin America and the Middle East and Africa are emerging markets where rising smartphone penetration and growing e-commerce access are creating early-stage but growing demand.

The fertility monitoring technologies market is served by established consumer health companies with broad OPK and fertility monitor product ranges, specialist femtech companies focused on digital and wearable fertility solutions, at-home testing companies expanding into fertility hormone panels, and digital health platforms building comprehensive women's health ecosystems with fertility tracking at the core. Competition is based on prediction accuracy and clinical validation evidence, product design and user experience, breadth of hormonal biomarkers measured, integration with fertility clinic workflows, and the strength of digital platform and subscription model offerings.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, clinical validation evidence, regulatory status, geographic presence, and recent strategic developments. Some of the key players operating in the global fertility monitoring technologies market include Clearblue/SPD Swiss Precision Diagnostics GmbH (Switzerland), Ava Science Inc. (U.S./Switzerland), Natural Cycles Nordic AB (Sweden/U.S.), OvuSense/Fertility Focus Ltd. (UK), Tempdrop Ltd. (Israel/U.S.), Kindara Inc. (U.S.), iXensor Co. Ltd. (Taiwan), Fairhaven Health LLC (U.S.), Femometer/BfBio Ltd. (U.S./China), Bloomlife Inc. (U.S.), Mira/Quanovate Tech Inc. (U.S.), YONO Labs (U.S.), Proov/MFB Fertility Inc. (U.S.), Modern Fertility/Ro (U.S.), and LetsGetChecked (Ireland/U.S.), among others.

The global fertility monitoring technologies market is expected to reach USD 5.8 billion by 2036 from an estimated USD 2.4 billion in 2026, at a CAGR of 9.2% during the forecast period 2026-2036.

In 2026, the ovulation prediction kits segment is expected to hold the largest share, driven by OPKs being the most universally accessible and lowest-cost entry point to fertility monitoring, with Clearblue's digital ovulation test range representing the dominant consumer brand globally across pharmacy and online retail channels.

The wearable fertility tracking devices segment is projected to register the highest CAGR, driven by Ava Science's FDA-cleared wristband validated in peer-reviewed clinical studies, growing consumer comfort with health wearables, and the appeal of passive continuous monitoring that removes the daily testing compliance requirement of conventional OPK or BBT monitoring approaches.

The market is primarily driven by the WHO's 2024 infertility report documenting approximately 1 in 6 people globally affected by infertility, the CDC's 2025 National Survey of Family Growth confirming approximately 12% of U.S. women aged 15 to 44 using fertility monitoring services, and the femtech investment surge with Pitchbook's 2025 report documenting approximately USD 1.2 billion in 2024 femtech investment with fertility monitoring as the leading category.

Key players are Clearblue/SPD Swiss Precision Diagnostics GmbH (Switzerland), Ava Science Inc. (U.S./Switzerland), Natural Cycles Nordic AB (Sweden/U.S.), OvuSense/Fertility Focus Ltd. (UK), Tempdrop Ltd. (Israel/U.S.), Kindara Inc. (U.S.), iXensor Co. Ltd. (Taiwan), Fairhaven Health LLC (U.S.), Femometer/BfBio Ltd. (U.S./China), Bloomlife Inc. (U.S.), Mira/Quanovate Tech Inc. (U.S.), YONO Labs (U.S.), Proov/MFB Fertility Inc. (U.S.), Modern Fertility/Ro (U.S.), and LetsGetChecked (Ireland/U.S.), among others.

Asia-Pacific is expected to register the highest growth rate during the forecast period 2026-2036, driven by Japan's government fertility treatment subsidies announced in 2025, South Korea's declining birth rates per Statistics Korea 2025 data creating strong societal demand, China's government promotion of higher birth rates, and India's very large reproductive-age population with rapidly growing consumer health technology adoption.

Published Date: Jun-2026

Published Date: May-2026

Published Date: Oct-2013

Published Date: Feb-2023

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates