Resources

About Us

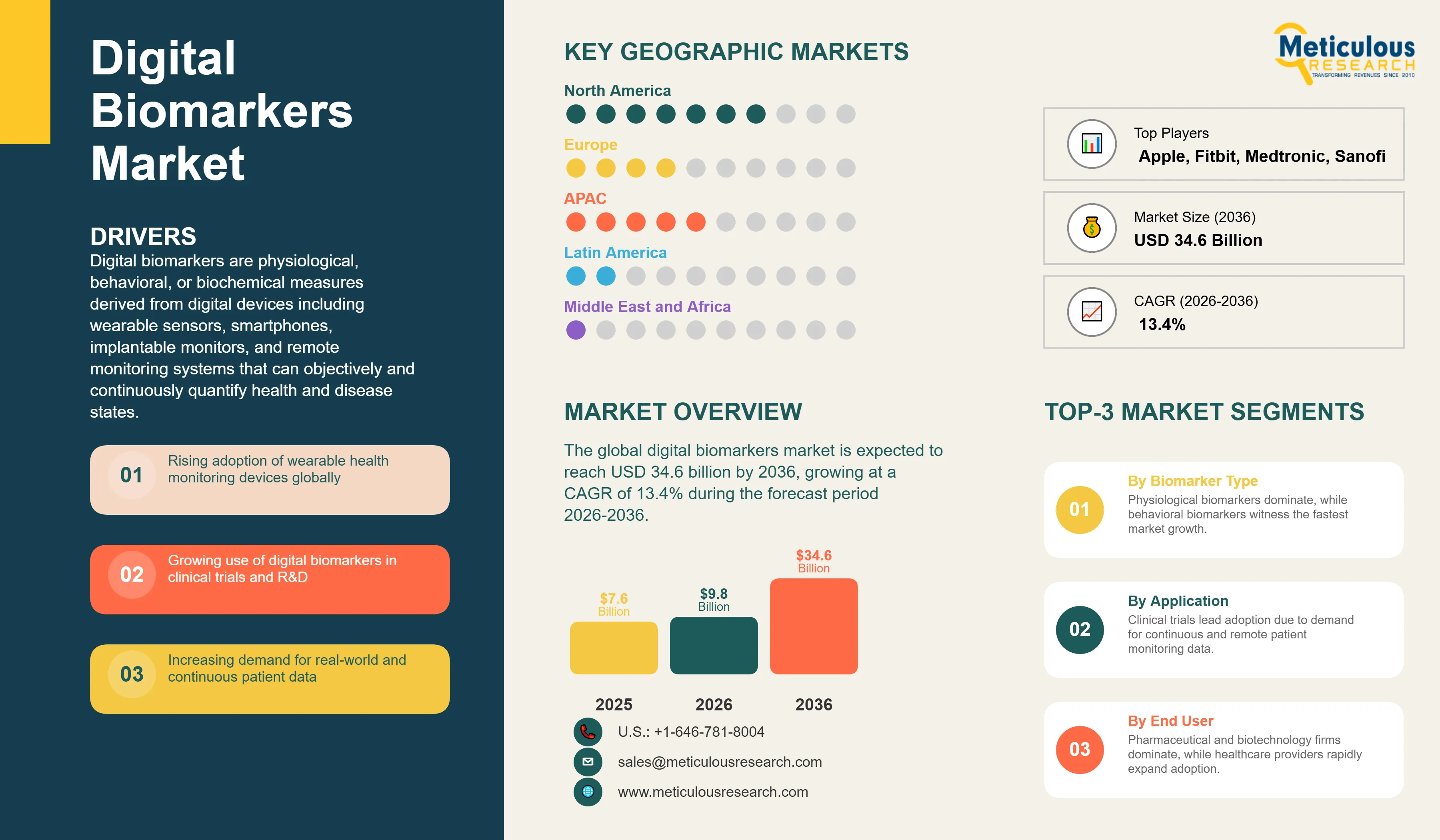

Digital Biomarkers Market Size, Share & Trends Analysis by Biomarker Type, Data Source / Device Type (Wearables, Smartphones, Implantables, Remote Monitoring), and End User- Global Opportunity Analysis & Industry Forecast (2026-2036)

Report ID: MRHC - 1041981 Pages: 265 May-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global digital biomarkers market was valued at USD 7.6 billion in 2025. This market is expected to reach USD 34.6 billion by 2036 from an estimated USD 9.8 billion in 2026, growing at a CAGR of 13.4% during the forecast period 2026-2036. According to the FDA’s 2025 reporting on digital health and translational science, submissions and clinical development activities involving wearable and digital biomarker data are increasing, reflecting the transition of digital biomarkers from research tools toward more routine clinical-trial measurement methods.

Click here to: Get Free Sample Pages of this Report

Digital biomarkers are physiological, behavioral, or biochemical measures derived from digital devices including wearable sensors, smartphones, implantable monitors, and remote monitoring systems that can objectively and continuously quantify health and disease states. Unlike conventional biomarkers that require laboratory analysis of biological specimens collected at discrete time points, digital biomarkers are captured passively and continuously from the patient's daily environment, providing a richer temporal picture of disease activity and treatment response that point-in-time measurements cannot deliver. A digital biomarker might be the six-minute walk test score calculated by an accelerometer in a heart failure patient's smartwatch, the tremor frequency and amplitude measured by a gyroscope in a Parkinson's disease patient's smartphone, the sleep efficiency and architecture derived from a continuous wristband sensor in a clinical trial for an insomnia treatment, or the irregular cardiac rhythm pattern detected by the single-lead ECG in an Apple Watch that triggers a notification for potential atrial fibrillation.

The market is growing because the pharmaceutical industry, healthcare providers, and regulators are collectively recognizing that digital biomarkers can solve the most persistent and costly problem in clinical drug development: the inability to measure disease status and treatment response accurately, continuously, and objectively outside of clinic visits. According to the Tufts Center for the Study of Drug Development's 2025 analysis, patient burden from clinic visits accounts for a large fraction of clinical trial dropout rates, and digital biomarker-based endpoints that can be assessed at home rather than at a clinic site reduce this burden while simultaneously increasing the density and objectivity of the outcome data collected. According to IQVIA’s Digital Health Trends reporting, digital biomarker and wearable-based measures are gaining broader acceptance in clinical development, reflecting a steadily growing regulatory and commercial role for digital health tools.

Two commercial catalysts are particularly significant. Apple's health research platform has enabled pharmaceutical companies to conduct research involving Apple Watch-collected digital biomarkers in large populations, with several published studies demonstrating that consumer wearables can generate research-grade digital biomarker data. According to Apple's 2025 Health Research publications, studies using Apple Watch-collected data including the Apple Heart Study have enrolled hundreds of thousands of participants at a scale that was impossible with conventional clinic-based data collection, providing enormous datasets for digital biomarker validation. Simultaneously, the FDA's September 2023 guidance on digital health technologies for remote data acquisition in clinical investigations provided regulatory clarity on how FDA evaluates wearable-collected data, removing the uncertainty that had previously slowed pharmaceutical company adoption of digital biomarker endpoints in pivotal trials.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 34.6 Billion |

|

Market Size in 2026 |

USD 9.8 Billion |

|

Market Size in 2025 |

USD 7.6 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 13.4% |

|

Dominating Biomarker Type |

Physiological Biomarkers |

|

Fastest Growing Biomarker Type |

Behavioral Biomarkers |

|

Dominating Data Source / Device Type |

Wearable Devices |

|

Fastest Growing Data Source / Device Type |

Implantable Devices |

|

Dominating Technology |

AI & Machine Learning |

|

Fastest Growing Technology |

IoT-enabled Platforms |

|

Dominating Application |

Clinical Trials |

|

Fastest Growing Application |

Remote Patient Monitoring |

|

Dominating End User |

Pharmaceutical & Biotechnology Companies |

|

Fastest Growing End User |

Healthcare Providers |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

FDA Regulatory Clarity Accelerating Digital Biomarker Adoption in Clinical Trials

The FDA's September 2023 guidance on digital health technologies for remote data acquisition in clinical investigations, followed by the agency's 2024 qualification review of multiple digital biomarker endpoints submitted under the Drug Development Tool qualification program, has created a significantly clearer regulatory framework for digital biomarker use in drug development than existed before. The guidance explicitly addresses the FDA's expectations for analytical validation, clinical validation, and usability of wearable-collected digital biomarker endpoints, providing pharmaceutical sponsors with the evidentiary standards they need to meet before submitting trial designs incorporating digital biomarker endpoints to FDA. According to the FDA's 2025 Digital Health Center of Excellence Annual Report, the number of pre-submission meetings discussing digital biomarker endpoints grew by approximately 45% in fiscal year 2024 compared with 2023, demonstrating the direct commercial effect of regulatory clarity on sponsor engagement.

The FDA's Drug Development Tool qualification program has provided the most rigorous pathway for digital biomarker validation, with several digital endpoints now having qualified DDT status that allows sponsors to use them in clinical trials without needing to re-validate the endpoint in each new study. The qualification of the six-minute walk test digital endpoint measured by accelerometer for heart failure and pulmonary hypertension trials, and the qualification of wrist-worn accelerometry measures for Duchenne muscular dystrophy trials, represent the FDA's first DDT qualifications for wearable-based digital biomarker endpoints and establish the regulatory template for future qualifications. Biogen's work with Roche and the Critical Path Institute on digital biomarkers for neurological disease using ActiGraph and Empatica devices provided foundational validation data that informed FDA's qualification framework.

Apple Watch and Consumer Wearables Generating Research-Grade Digital Biomarker Data

The Apple Watch's combination of clinical-grade sensors, large global user base exceeding 100 million according to Morgan Stanley's 2025 Wearables Market analysis, and Apple's Research Kit and Health Kit developer frameworks enabling large-scale data collection is transforming the scale at which digital biomarker research can be conducted. The Apple Heart Study, which enrolled over 419,000 participants and demonstrated that the Apple Watch could detect atrial fibrillation with high specificity in an asymptomatic population, established consumer smartwatches as viable platforms for population-scale digital health research and demonstrated that meaningful biomarker data can be collected passively from an enormous number of participants without dedicated research infrastructure.

According to Apple's 2025 Health Research publications, multiple pharmaceutical companies and academic medical centers have conducted approved studies using Apple Watch-collected data including movement metrics for Parkinson's disease characterization, sleep and activity data for depression and anxiety research, and cardiovascular metrics for heart failure monitoring. AliveCor's KardiaMobile and KardiaCard ECG devices, which received FDA clearances for detecting atrial fibrillation, have been integrated into multiple clinical trial digital biomarker programs as FDA-cleared cardiac rhythm digital biomarker tools. Abbott's FreeStyle Libre continuous glucose monitoring sensor, which generates continuous blood glucose digital biomarker data from tens of millions of wearers according to Abbott's 2025 annual report, represents the most commercially scaled pharmaceutical-grade digital biomarker platform in current deployment.

Behavioral Digital Biomarkers Emerging as Breakthrough in Neurological and Psychiatric Research

Behavioral digital biomarkers derived from analysis of passive smartphone usage patterns, including keystroke dynamics, voice quality, scrolling behavior, and GPS mobility patterns, are emerging as particularly sensitive and objective measures of neurological and psychiatric disease status that can be captured continuously from the device the patient already carries without any additional hardware. The scientific rationale is that neurological and psychiatric diseases alter the fine motor control, language processing, circadian function, and social behavior that are reflected in measurable patterns of smartphone interaction. Biogen's digital biomarker programs for multiple sclerosis and Alzheimer's disease, developed in collaboration with Flatiron Health and digital health partners, use passive smartphone-derived behavioral biomarkers including walking speed, balance, and dexterity measures to continuously monitor disease progression between clinic visits.

According to a 2025 meta-analysis published in the Lancet Digital Health, passive smartphone behavioral biomarkers for depression demonstrated sensitivity and specificity comparable to validated clinical assessment scales when trained on longitudinal datasets of several hundred patients, providing the clinical validation evidence needed to support regulatory consideration of behavioral digital biomarker endpoints in psychiatric drug trials. Roche's Floodlight Open app, which collects motor and cognitive digital biomarker data from multiple sclerosis patients using smartphone tasks, has generated peer-reviewed publications confirming correlations between app-measured digital biomarkers and clinical outcomes, supporting its qualification as a digital endpoint in Roche's MS clinical programs.

Increasing Adoption of Wearables & Remote Monitoring

The expanding adoption of health-focused wearable devices is creating a robust hardware foundation for the deployment of digital biomarkers at scale. Devices such as smartwatches, continuous glucose monitors, and connected physiological sensors are increasingly integrated into everyday healthcare and wellness management, enabling continuous, real-time data collection outside traditional clinical settings. Platforms like the Apple Watch and FreeStyle Libre illustrate how wearable technologies are evolving into clinically relevant tools capable of supporting both disease management and research applications.

At the same time, the rapid expansion of remote patient monitoring programs is accelerating the clinical integration of wearable-derived data. Healthcare providers are increasingly leveraging these technologies to track patient conditions such as cardiac and respiratory health in real-world environments, improving both care continuity and early intervention capabilities. Insights from organizations such as American Hospital Association highlight the growing role of wearable-enabled monitoring in modern care delivery. Collectively, these trends are driving demand for digital biomarker platforms and reinforcing the role of wearables as a key enabler of decentralized and data-driven healthcare models.

Growth in Digital Clinical Trials

The integration of digital biomarkers into clinical trials is accelerating, reflecting growing industry confidence in their ability to enhance data collection and patient-centric study design. Insights from IQVIA indicate a clear increase in the number of trials incorporating digital biomarker endpoints, highlighting their expanding role in modern clinical development. At the same time, the U.S. Food and Drug Administration Digital Health Center of Excellence has reported rising engagement from sponsors seeking regulatory guidance on digital endpoints, underscoring the importance of regulatory clarity in supporting adoption.

Research from Tufts Center for the Study of Drug Development demonstrates that digital clinical outcome assessments can reduce patient burden compared to traditional site-based evaluations, helping to address one of the key contributors to trial dropout. In parallel, findings from Veeva Systems highlight the rapid growth in the integration of wearable and sensor-generated data into clinical trial platforms. Together, these trends reflect a broader shift toward decentralized, data-rich clinical trials, where digital biomarkers play a central role in improving efficiency, patient engagement, and data quality.

Integration with AI & Predictive Analytics

AI and machine learning are enabling digital biomarker algorithms to detect clinical signals in sensor data streams with a sensitivity that human clinicians and conventional statistical methods cannot match by identifying subtle multi-parameter patterns in high-dimensional time-series data. Deep learning models trained on large annotated datasets of wearable sensor recordings are achieving diagnostic accuracy for atrial fibrillation, Parkinson's tremor characterization, and fall risk prediction that meets or exceeds clinical assessment standards. According to a 2025 review in Nature Digital Medicine, AI-derived digital biomarkers for neurological disease demonstrated significantly higher sensitivity for detecting clinically meaningful changes in disease status compared with conventional clinical assessments in a meta-analysis of published validation studies, providing quantitative evidence of AI's diagnostic advantage for digital biomarker applications.

Expansion in Chronic Disease Management

The growing global burden of chronic diseases is creating a substantial opportunity for digital biomarker-based remote management solutions. Conditions such as cardiovascular disease, diabetes, cancer, and respiratory disorders require continuous monitoring and long-term care, making them well suited for digital health approaches that extend beyond traditional clinical settings. Organizations such as the Centers for Disease Control and Prevention and the International Diabetes Federation highlight the widespread prevalence of chronic conditions, underscoring the need for scalable and patient-centric monitoring solutions.

Digital biomarkers, enabled by connected devices and wearable technologies, are increasingly being integrated into routine disease management. Platforms such as FreeStyle Libre and Dexcom CGM demonstrate how continuous, real-time data can support improved clinical decision-making and patient self-management. As healthcare systems shift toward proactive and value-based care models, the adoption of digital biomarkers in chronic disease management is expected to accelerate, driving improved outcomes while reducing the burden on traditional healthcare infrastructure.

By Biomarker Type: In 2026, Physiological Biomarkers to Hold the Largest Share

Based on biomarker type, the global digital biomarkers market is segmented into physiological biomarkers (heart rate and cardiac metrics, respiratory metrics, and activity and mobility), behavioral biomarkers (sleep patterns, cognitive function, and digital interaction patterns), biochemical digital biomarkers, and other biomarker types. In 2026, the physiological biomarkers segment is expected to account for the largest share of the global digital biomarkers market. Physiological digital biomarkers including heart rate, heart rate variability, SpO2, ECG-derived metrics, step count, and gait parameters are the most commercially established and most widely validated category, measured by the very large installed base of consumer wearables including Apple Watch and Fitbit as well as clinical-grade devices from ActiGraph, Empatica, and AliveCor. Abbott's FreeStyle Libre CGM representing continuous glucose physiological biomarker data in approximately USD 5.7 billion annual revenues per its 2025 annual report illustrates the commercial scale of this segment.

However, the behavioral biomarkers segment is projected to register the highest CAGR during the forecast period. Behavioral digital biomarkers derived from passive smartphone and wearable data are emerging as uniquely sensitive indicators of neurological and psychiatric disease status with clinical validation evidence growing rapidly. The Lancet Digital Health 2025 meta-analysis confirming passive smartphone behavioral biomarkers' clinical utility for depression, combined with the growing Biogen and Roche clinical programs using behavioral digital endpoints, are creating the evidence base for a fast-growing new biomarker category that is particularly compelling for CNS drug development where objective continuous measurement has historically been almost impossible.

By Data Source / Device Type: In 2026, Wearable Devices to Hold the Largest Share

Based on data source and device type, the global digital biomarkers market is segmented into wearable devices (smartwatches and fitness bands), smartphones and mobile apps, implantable devices, remote monitoring systems, and other devices. In 2026, the wearable devices segment is expected to account for the largest share of the global digital biomarkers market. The very large global installed base of health wearables provides the hardware foundation for wearable digital biomarker deployment at population scale. Apple Watch, Garmin, and Fitbit collectively represent the dominant consumer wearable platforms, while ActiGraph and Empatica provide research-grade wearable digital biomarker solutions with FDA-reviewed credentials for use in clinical trials.

However, the implantable devices segment is projected to register the highest CAGR during the forecast period. Implantable cardiac monitors including Medtronic's Reveal LINQ, which continuously records cardiac rhythms and wirelessly transmits data to a clinician monitoring center, represent a high-value clinical digital biomarker platform for arrhythmia detection and cardiac monitoring in implant-grade patients. Abbott's implantable CGM development program targeting sensors with multi-year implant durations for continuous glucose digital biomarker data represents the next frontier of implantable metabolic monitoring. As implant procedures become less invasive and device longevity increases, the implantable digital biomarker segment is expected to grow rapidly from its currently smaller base.

By Technology: In 2026, AI & Machine Learning to Hold the Largest Share

Based on technology, the global digital biomarkers market is segmented into AI and machine learning, cloud and big data analytics, IoT-enabled platforms, and sensor technologies. In 2026, the AI and machine learning segment is expected to account for the largest share of the global digital biomarkers market. AI algorithms are the foundational enabler of digital biomarker utility: without sophisticated machine learning models to extract clinically meaningful signals from high-dimensional, high-frequency sensor data streams, the raw sensor data would be too noisy, too voluminous, and too complex to interpret clinically. Apple's atrial fibrillation detection algorithm in Apple Watch, AliveCor's FDA-cleared AI arrhythmia detection, and Biogen's behavioral biomarker algorithms are all AI-based digital biomarker implementations generating commercially deployed clinical value.

However, the IoT-enabled platforms segment is projected to register the highest CAGR during the forecast period. The growing ecosystem of Internet of Things-connected medical devices, home monitoring sensors, and connected health platforms is creating the integration infrastructure through which multiple digital biomarker streams from different devices can be consolidated, transmitted securely, and made available to clinical monitoring platforms in near-real-time. The maturation of IoT connectivity standards, cloud API frameworks, and device interoperability protocols is progressively lowering the integration cost and complexity of multi-device digital biomarker deployments in clinical and home settings.

By Application: In 2026, Clinical Trials to Hold the Largest Share

Based on application, the global digital biomarkers market is segmented into clinical trials, disease diagnosis, remote patient monitoring, drug development and R&D, digital therapeutics, and wellness and preventive care. In 2026, the clinical trials application segment, which is labeled as the largest segment in the original TOC, is expected to account for the largest share of the global digital biomarkers market. Pharmaceutical companies are the highest-spending adopters of digital biomarker technology, integrating wearable endpoints and remote monitoring into clinical trial protocols to improve endpoint sensitivity, reduce patient burden, and generate richer and more continuous outcome data.

However, the remote patient monitoring segment is projected to register the highest CAGR during the forecast period. The sustained expansion of remote patient monitoring programs enabled by telehealth reimbursement infrastructure, combined with the growing availability of FDA-cleared wearable devices generating clinical-grade digital biomarker data, is creating a rapidly expanding commercial market for digital biomarker-based RPM. According to the American Hospital Association's 2025 data, RPM programs incorporating digital biomarker-equipped wearables demonstrated improved clinical outcomes and reduced hospital readmissions in multiple published studies, creating the clinical evidence that is driving payer coverage and hospital system investment.

By End User: In 2026, Pharmaceutical & Biotechnology Companies to Hold the Largest Share

Based on end user, the global digital biomarkers market is segmented into pharmaceutical and biotechnology companies, CROs, healthcare providers, research institutes, and patients and consumers. In 2026, the pharmaceutical and biotechnology companies segment is expected to account for the largest share of the global digital biomarkers market. Large pharmaceutical companies including Biogen, Roche, Novartis, and Sanofi are investing in proprietary digital biomarker programs as competitive differentiators in drug development, recognizing that superior endpoint sensitivity from validated digital biomarkers can reduce required trial sample sizes, shorten trial duration, and provide more compelling regulatory submission packages.

However, the healthcare providers segment is projected to register the highest CAGR during the forecast period. Hospital systems and health networks are rapidly deploying digital biomarker-based remote patient monitoring programs for chronic disease management, post-discharge cardiac monitoring, and diabetes management, driven by both clinical evidence of improved outcomes and reimbursement support from CMS. According to CMS's 2025 Remote Patient Monitoring reimbursement data, RPM program reimbursement grew at above-average rates in 2024 as more healthcare provider organizations deployed FDA-cleared wearable digital biomarker monitoring programs for their chronic disease patient populations.

Digital Biomarkers Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global market for digital biomarkers is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global digital biomarkers market. The United States leads this market due to its concentration of advanced digital health and biomarker technology companies, including Apple, Alphabet, AliveCor, ActiGraph, Biofourmis, and Empatica. The region also benefits from strong pharmaceutical R&D investment and early adoption of digital endpoints within clinical trials, reflecting a broader shift toward data-driven and patient-centric development models.

Supportive regulatory and reimbursement frameworks further reinforce North America’s leadership. The U.S. Food and Drug Administration Digital Health Center of Excellence has reported increasing engagement from sponsors around digital biomarker endpoints, highlighting growing integration into clinical development. In parallel, commercially established platforms such as FreeStyle Libre demonstrate the real-world scalability of digital biomarker technologies. Additionally, reimbursement expansion by the Centers for Medicare & Medicaid Services for remote patient monitoring is enabling broader provider adoption of wearable-based monitoring solutions, further accelerating market growth in the region.

However, the Asia-Pacific digital biomarkers market is expected to grow at the fastest rate during the forecast period. The region combines a large and expanding population of patients with chronic diseases with rapidly advancing digital health infrastructure and high smartphone penetration, enabling widespread adoption of digital biomarker solutions. Countries across the region are increasingly leveraging connected devices and mobile health platforms to support continuous monitoring and data-driven disease management, creating strong demand for scalable digital biomarker technologies.

Government-led initiatives are playing a central role in accelerating this growth. For example, China’s Healthy China 2030 strategy emphasizes the use of digital health tools for chronic disease management, while Japan’s rapidly aging population is driving demand for remote monitoring of age-related conditions. South Korea further strengthens the regional landscape through its advanced digital health ecosystem and platforms developed by companies such as Samsung. Collectively, these factors—along with growing adoption of connected health devices across the region—are positioning Asia-Pacific as the fastest-growing market for digital biomarkers.

Europe is a large and technically sophisticated market for digital biomarkers, with strong pharmaceutical company investment through Roche, Novartis, and Boehringer Ingelheim's digital biomarker programs and an active regulatory environment from the EMA that is progressively developing frameworks for digital health endpoint assessment. The UK's NHS digital strategy and its digital biomarker research programs at major academic medical centers are generating valuable digital biomarker validation data. Germany's Digital Healthcare Act creating reimbursement for digital health applications supports the commercial deployment of digital biomarker-based monitoring tools. Switzerland hosts Roche and Novartis, both of which have significant digital biomarker research programs, and the European femtech and digital health startup ecosystem is generating innovative new digital biomarker applications.

The digital biomarkers industry is served by consumer technology companies with large wearable device platforms and growing health data capabilities, medical device companies with FDA-cleared clinical digital biomarker tools, pharmaceutical companies developing digital biomarkers as drug development endpoints, specialist digital health companies building digital biomarker platforms for specific disease areas, and analytics and AI companies providing the data processing infrastructure. Competition is based on biomarker measurement accuracy and FDA clearance or qualification status, wearable device comfort and user acceptance, data security and privacy compliance, breadth of disease application validation, and platform integration with clinical trial and healthcare IT systems.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' sensor capabilities, FDA clearance and qualification status, clinical evidence portfolios, and recent strategic developments. Some of the key players operating in the global digital biomarkers market include Apple Inc. (U.S.), Alphabet Inc. (U.S.), Fitbit/Google (U.S.), Garmin Ltd. (Switzerland/U.S.), Empatica Inc. (U.S./Italy), ActiGraph LLC (U.S.), Biofourmis (U.S.), AliveCor Inc. (U.S.), Philips Healthcare (Netherlands), Medtronic plc (Ireland), Abbott Laboratories (U.S.), Biogen Inc. (U.S.), Roche Holding AG (Switzerland), Novartis AG (Switzerland), and Sanofi (France), among others.

The global digital biomarkers market is expected to reach USD 34.6 billion by 2036 from an estimated USD 9.8 billion in 2026, at a CAGR of 13.4% during the forecast period 2026-2036.

In 2026, the physiological biomarkers segment is expected to hold the largest share.

The behavioral biomarkers segment is projected to register the highest CAGR.

Clinical trials holds the largest share, while remote patient monitoring is the fastest-growing application.

Key players are Apple Inc. (U.S.), Alphabet Inc. (U.S.), Fitbit/Google (U.S.), Garmin Ltd. (Switzerland/U.S.), Empatica Inc. (U.S./Italy), ActiGraph LLC (U.S.), Biofourmis (U.S.), AliveCor Inc. (U.S.), Philips Healthcare (Netherlands), Medtronic plc (Ireland), Abbott Laboratories (U.S.), Biogen Inc. (U.S.), Roche Holding AG (Switzerland), Novartis AG (Switzerland), and Sanofi (France), among others.

Asia-Pacific is expected to register the highest growth rate during the forecast period 2026-2036.

Published Date: Nov-2025

Published Date: Jan-2025

Published Date: May-2024

Published Date: May-2024

Published Date: Jun-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates