Resources

About Us

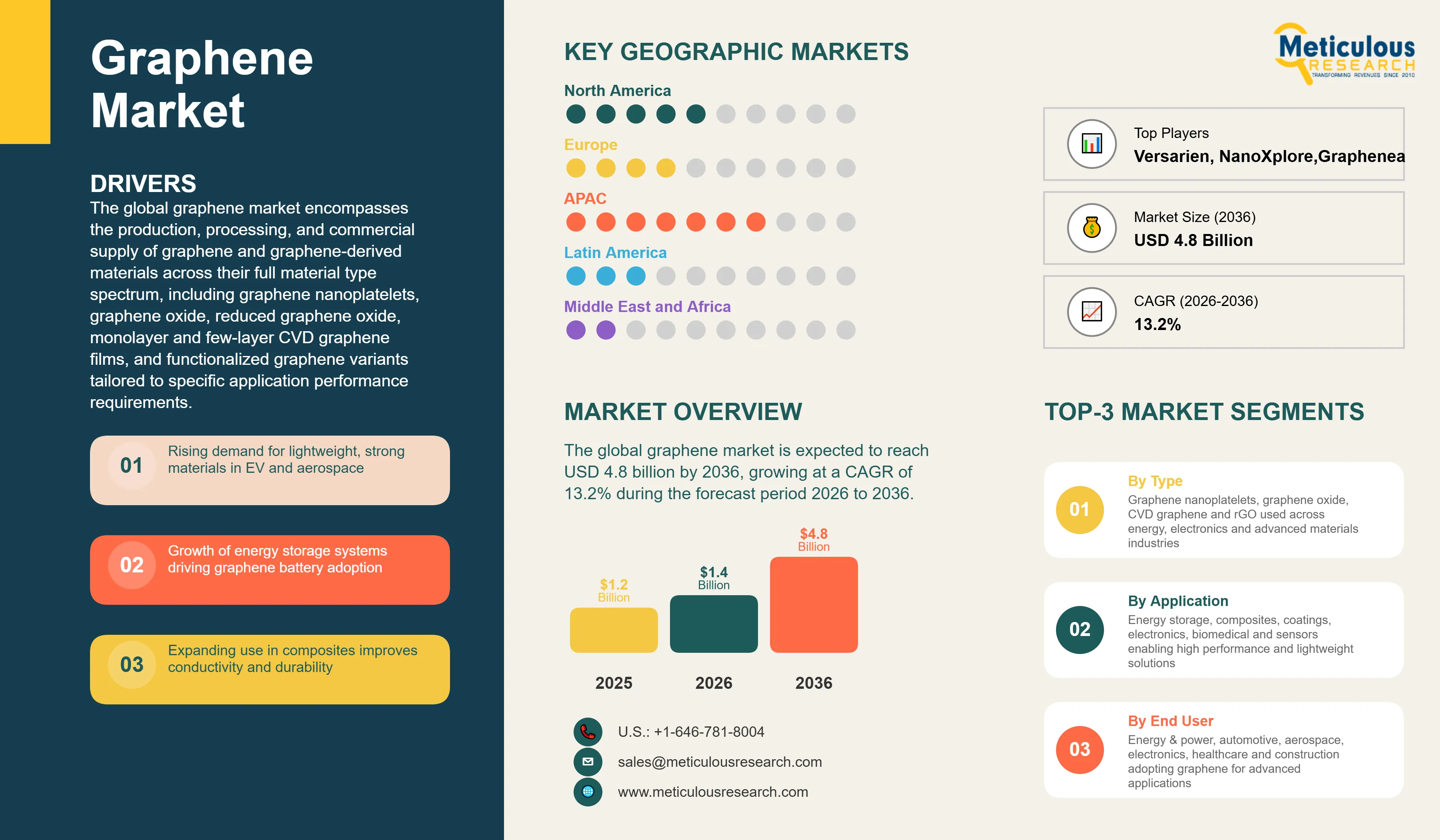

The global graphene market was valued at USD 1.2 billion in 2025. This market is expected to reach USD 4.8 billion by 2036 from an estimated USD 1.4 billion in 2026, growing at a CAGR of 13.2% during the forecast period 2026 to 2036.

The global graphene market encompasses the production, processing, and commercial supply of graphene and graphene-derived materials across their full material type spectrum, including graphene nanoplatelets, graphene oxide, reduced graphene oxide, monolayer and few-layer CVD graphene films, and functionalized graphene variants tailored to specific application performance requirements. Graphene, the single-atom-thick allotrope of carbon arranged in a two-dimensional hexagonal lattice structure, possesses an extraordinary combination of material properties that position it as a platform advanced material across multiple high-value application domains: an intrinsic carrier mobility of approximately 200,000 square centimeters per volt-second making it the fastest known electron conductor, a Young's modulus of approximately 1 TPa making it the stiffest known material, thermal conductivity exceeding 5,000 watts per meter-kelvin surpassing diamond, and near-perfect optical transparency of 97.7% combined with impermeability to even the smallest gas molecules. The market serves end-use industries including energy and power, electronics and semiconductor, automotive and aerospace, healthcare and biomedical, construction, and chemicals and materials, applying graphene in powder, dispersion, film and sheet, and foam forms across applications spanning energy storage, composites, electronics, coatings, biomedical devices, and environmental remediation.

The growth of the global graphene market is primarily driven by the convergence of maturing graphene production technologies that are progressively reducing material costs toward commercial viability thresholds across a broadening range of applications, and the intensifying demand from high-growth industries including electric vehicle batteries, flexible electronics, advanced composites, and biomedical devices for the performance enhancements that graphene addition uniquely enables. In energy storage, graphene additives in lithium-ion battery anodes are demonstrating commercially meaningful improvements in charge rate, energy density, and cycle life that battery manufacturers are increasingly incorporating into production formulations for premium cell products. In composites, graphene nanoplatelet reinforcement of polymer matrices is delivering tensile strength, electrical conductivity, and barrier property improvements at additive loadings of 1 to 5% by weight that substantially enhance composite performance without the weight penalty associated with conventional reinforcement approaches. The progressive reduction of graphene nanoplatelet production costs from several hundred dollars per kilogram in 2015 toward below fifty dollars per kilogram for commercial-grade material in 2025 is the enabling economic factor expanding graphene's addressable commercial application space beyond the niche high-performance segments that could absorb premium material pricing.

Two transformative opportunities are defining the graphene market's long-term trajectory. The development of graphene-enhanced next-generation battery chemistries, including graphene-silicon composite anodes that combine the high theoretical capacity of silicon with graphene's mechanical flexibility and electrical conductivity to address the cycle life limitations that have constrained silicon anode commercialization, and graphene-based supercapacitor electrode materials that are closing the energy density gap with batteries while preserving supercapacitors' inherent power density and cycle life advantages, represents a potentially very large commercial opportunity that multiple companies are advancing toward commercial readiness. Simultaneously, the expanding adoption of graphene in biomedical applications including targeted drug delivery carriers, ultrasensitive biosensor platforms, neural interface electrodes, and antimicrobial surface coatings is advancing through clinical validation stages that are establishing the safety and efficacy evidence base necessary to support regulatory approval of graphene-containing medical products, opening a high-value application market with significant long-term commercial potential.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 4.8 Billion |

|

Market Size in 2026 |

USD 1.4 Billion |

|

Market Size in 2025 |

USD 1.2 Billion |

|

Revenue Growth Rate (2026 to 2036) |

CAGR of 13.2% |

|

Dominating Material Type |

Graphene Nanoplatelets (GNPs) |

|

Fastest Growing Material Type |

Monolayer and Few-Layer Graphene |

|

Dominating Production Method |

Chemical Vapor Deposition (CVD) |

|

Fastest Growing Production Method |

Liquid Phase Exfoliation |

|

Dominating Application |

Energy Storage |

|

Fastest Growing Application |

Electronics and Semiconductors |

|

Dominating End-Use Industry |

Energy and Power |

|

Fastest Growing End-Use Industry |

Healthcare and Biomedical |

|

Dominating Form |

Powder |

|

Fastest Growing Form |

Dispersion |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

North America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Accelerating Commercialization of Graphene in Energy Storage

The commercialization of graphene as a functional additive and active material in energy storage devices represents the most commercially significant near-term application trend in the global graphene market, as the performance requirements of electric vehicle battery systems and grid-scale energy storage are creating powerful economic incentives for battery manufacturers and material suppliers to develop and qualify graphene-enhanced electrode materials that deliver measurable improvements in specific capacity, charge rate, and cycle durability. Graphene's exceptional electrical conductivity enables more efficient electron transport through battery electrode structures, reducing internal resistance and enabling faster charge and discharge rates that are critical performance attributes for EV battery applications where rapid charging capability is a key consumer acceptance factor. At anode material additive concentrations of 0.1 to 2% by weight in graphite anodes, graphene nanoplatelets have demonstrated in peer-reviewed studies capacity retention improvements of 10 to 20% at high charge rates relative to graphene-free baseline electrodes, a commercially meaningful performance improvement that battery manufacturers including Samsung SDI and Panasonic have incorporated into product development evaluations.

The most transformative graphene energy storage opportunity lies in graphene-silicon composite anode systems that combine the theoretical specific capacity of silicon at approximately 3,579 milliampere-hours per gram versus 372 milliampere-hours per gram for graphite with graphene's mechanical flexibility and conductivity to manage the 300 to 400% volume expansion of silicon during lithiation that has historically caused rapid anode degradation and cell failure. Multiple graphene producers including Global Graphene Group, XG Sciences, and NanoXplore are developing graphene-silicon composite anode materials that demonstrate cycle retention above 80% after 500 full charge-discharge cycles in coin cell validation testing, approaching the cycle life threshold required for commercial EV battery qualification. Commercial deployment of graphene-silicon composite anodes in production EV battery cells would represent a step-change expansion of graphene volume demand and market revenue, and the competitive timeline toward this milestone is the single most consequential variable in graphene market volume forecasting through the early 2030s.

Growing Adoption of Graphene in Composites and Advanced Coatings

The integration of graphene nanoplatelets into polymer matrix composites, anti-corrosion coatings, and thermally conductive adhesives represents the largest by-volume commercial market for graphene currently, and sustained growth in these material application segments is providing the production volume foundation that is enabling graphene manufacturers to achieve the cost reduction and quality consistency necessary for broader market expansion. In polymer composites, graphene nanoplatelet addition at loadings of 1 to 5% by weight to epoxy, polyamide, polypropylene, and polyurethane matrices delivers multifunctional reinforcement that simultaneously improves tensile modulus, tensile strength, barrier properties against gas and moisture permeation, and electrical or thermal conductivity depending on the application requirement, providing composite formulators with a single additive capable of replacing or supplementing multiple conventional filler systems. The automotive sector is a leading adopter of graphene-reinforced composites for lightweight structural components, underbody panels, and battery enclosure structures where the combination of weight reduction and mechanical performance improvement that graphene reinforcement enables contributes directly to vehicle mass reduction targets that improve EV range efficiency.

Graphene-enhanced anti-corrosion coatings represent a commercially validated and growing application segment where the impermeability of graphene to oxygen, water, and ionic species provides an exceptionally effective barrier layer in coating formulations applied to steel, aluminum, and copper substrates in marine, infrastructure, and industrial equipment applications. Directa Plus and Applied Graphene Materials have developed commercial graphene-enhanced coating formulations demonstrating multi-year corrosion protection performance advantages over graphene-free conventional coating baselines in salt spray and electrochemical testing, and are expanding their commercial sales through established industrial coating distribution networks. The large addressable market for industrial anti-corrosion coatings, combined with the clearly demonstrated performance advantage of graphene enhancement and the modest graphene additive loadings of 0.1 to 1% by weight required in coating formulations, positions graphene-enhanced coatings as a near-term high-volume commercial segment with sustained growth potential throughout the forecast period.

Emergence of Graphene in Flexible and Wearable Electronics

The growing development and commercialization of flexible electronics applications including rollable displays, electronic skin sensors, smart textile integration, and conformable health monitoring patches is creating a new and rapidly expanding demand category for CVD graphene films and graphene-based conductive inks that can deliver electrical conductivity and mechanical flexibility simultaneously in thin, lightweight device formats that conventional rigid electronics materials cannot serve. CVD graphene's unique combination of high electrical conductivity, optical transparency exceeding 97%, and mechanical flexibility enabling bending to sub-millimeter radii without conductivity degradation makes it an exceptionally well-suited transparent electrode material for flexible display applications where the brittleness of conventional indium tin oxide (ITO) transparent electrodes is a critical limitation constraining the commercial deployment of genuinely flexible display products. Samsung and LG are among the major display manufacturers that have conducted extensive R&D evaluation of CVD graphene as an ITO replacement in flexible OLED display electrode stacks, and the commercial qualification of graphene transparent electrodes in production flexible displays would represent a high-volume, high-value commercial milestone for the CVD graphene segment.

Graphene-based conductive inks formulated from graphene nanoplatelet dispersions in compatible solvent systems are achieving commercial adoption in printed electronics applications including RFID antenna printing, flexible circuit interconnects, and wearable sensor electrode printing where the combination of printability, conductivity, mechanical flexibility, and biocompatibility that graphene inks offer is creating performance advantages over silver nanoparticle inks at competitive material cost points. Haydale Graphene Industries and Thomas Swan are among the graphene producers commercially supplying functionalized graphene dispersion materials to conductive ink formulators serving the printed electronics market. The integration of graphene-based electrodes and sensing elements into smart textile platforms for continuous health monitoring is advancing through research prototype stages toward commercialization, with graphene's biocompatibility, skin conductance sensing capability, and washability durability in textile integration environments representing key performance advantages for this application segment.

Rising Demand for Lightweight and High-Strength Materials

The accelerating global demand for lightweight, high-strength structural and functional materials across automotive, aerospace, sporting goods, and consumer electronics industries is providing a powerful commercial pull for graphene as a reinforcement and enhancement additive that can deliver exceptional mechanical performance improvements at weight fractions of 1 to 5% that have negligible impact on the processed part weight or density. The automotive industry's imperative to reduce vehicle mass in pursuit of improved fuel efficiency and EV range extension is driving sustained investment in advanced composite materials that substitute graphene-reinforced polymers for heavier metal components, with major automotive OEMs and Tier 1 suppliers actively developing graphene composite formulations for structural and semi-structural applications. The aerospace industry applies similarly rigorous weight reduction requirements to structural components, interior systems, and thermal management materials, and graphene's extraordinary strength-to-weight ratio and thermal conductivity are generating research and development interest from aerospace composite manufacturers and system designers seeking performance advantages beyond those achievable with carbon fiber reinforced polymers alone. The commercial adoption of graphene-reinforced composites is being further accelerated by the maturation of graphene nanoplatelet dispersion technology, with improved surface functionalization methods enabling more effective graphene distribution within polymer matrices and more reproducible composite mechanical property outcomes that are essential for the quality consistency requirements of structural aerospace and automotive applications.

Increasing Adoption in Energy Storage Applications

The global expansion of electric vehicle markets and grid-scale energy storage deployment is creating rapidly growing demand for advanced battery and supercapacitor materials, and graphene's demonstrated capability to improve electrode performance across multiple key parameters is establishing it as a commercially important additive in the energy storage material supply chain. The lithium-ion battery industry's sustained competitive pressure to improve specific energy density, charge rate capability, and cycle durability while reducing cost per kilowatt-hour is driving battery material developers to incorporate graphene additives that provide incremental but commercially meaningful improvements in these critical performance metrics at additive cost levels compatible with battery cell economics. Supercapacitor manufacturers are adopting graphene as an active electrode material in graphene-based electrical double layer capacitors that achieve specific capacitance values significantly exceeding those of conventional activated carbon electrode supercapacitors, extending the energy density range of supercapacitor technology into application territories previously requiring battery energy sources while preserving supercapacitors' fundamental advantages of extremely high power density, very long cycle life exceeding one million charge-discharge cycles, and broad operating temperature range. The growing deployment of renewable energy storage requiring high-cycle-life energy storage solutions that can withstand the frequent charge-discharge cycling of solar and wind energy buffering applications is creating a particularly favorable demand environment for graphene-enhanced supercapacitor technologies.

Graphene in Next-Generation Batteries and Supercapacitors

The development and commercialization of graphene-enhanced next-generation energy storage systems represents the highest potential value commercial opportunity in the graphene market over the forecast period, as the convergence of maturing graphene production technology, advancing battery material formulation science, and the enormous commercial scale of the EV and grid storage battery markets is creating the conditions for graphene to transition from a specialty battery additive into a mainstream electrode material component. The graphene-silicon composite anode opportunity is particularly significant: silicon anodes can theoretically store approximately ten times more lithium per unit weight than graphite anodes, but the severe volume expansion of silicon during lithiation causes electrode cracking, loss of electrical contact, and rapid capacity fade that has prevented silicon anode commercialization in high-cycle-life applications. Graphene's role as a structural and conductive matrix that accommodates silicon volume changes while maintaining electrical connectivity is enabling silicon-graphene composite anodes to achieve cycle stability profiles approaching commercial viability, and the successful commercial deployment of such anodes in production EV cells would unlock annual graphene demand volumes orders of magnitude larger than current market consumption. The U.S. Department of Energy's Vehicle Technologies Office and the EU's Graphene Flagship program are both actively funding graphene-silicon anode development programs that are advancing this technology toward commercial readiness.

Expansion in Biomedical Applications

The expanding application of graphene and graphene oxide in biomedical contexts represents one of the most scientifically exciting and commercially promising long-term growth opportunities in the graphene market, as graphene's unique combination of surface area, electrical conductivity, mechanical flexibility, chemical versatility, and demonstrated biocompatibility in appropriately functionalized forms is enabling novel medical device and drug delivery innovations that conventional materials cannot replicate. Graphene oxide and functionalized reduced graphene oxide are being developed as targeted drug delivery carriers for cancer therapeutics, exploiting graphene oxide's high surface area for drug loading, its pH-responsive drug release behavior in the acidic tumor microenvironment, and the potential to attach tumor-specific targeting ligands to its surface chemistry that direct drug-loaded graphene carriers preferentially to tumor tissue while minimizing systemic toxicity. Neural interface electrode applications represent another high-value biomedical graphene application, where graphene's flexibility, biocompatibility, and electrical conductivity enable neural recording and stimulation electrode arrays that maintain stable tissue contact with reduced inflammatory foreign body response relative to rigid metal electrodes, with potential applications in brain-computer interfaces, cochlear implants, and deep brain stimulation devices. Biosensor applications of graphene exploit its exceptional sensitivity to molecular adsorption events that produce measurable changes in electrical conductance, enabling graphene field-effect transistor biosensors capable of detecting individual virus particles, femtomolar concentrations of disease biomarker proteins, and specific DNA sequences at sensitivities that challenge or exceed the best conventional biosensor platforms.

By Material Type: In 2026, Graphene Nanoplatelets (GNPs) to Dominate

Based on material type, the global graphene market is segmented into graphene nanoplatelets (GNPs), graphene oxide (GO), reduced graphene oxide (rGO), monolayer and few-layer graphene, and functionalized graphene. In 2026, the graphene nanoplatelets segment is expected to account for the largest share of the global graphene market. GNPs dominate the commercial graphene market because they represent the graphene material type most amenable to large-scale production at commercially viable costs using liquid phase exfoliation and other scalable methods, delivering a useful subset of graphene's exceptional properties at material costs that are compatible with the economics of composites, coatings, and energy storage applications constituting the current mainstream commercial graphene demand base. GNPs typically consist of stacks of two to ten graphene layers with lateral dimensions of one to twenty-five micrometers, providing a high-aspect-ratio nanofiller morphology that is effective for mechanical reinforcement, barrier enhancement, and electrical and thermal conductivity improvement in polymer matrix systems at loading levels where the cost contribution to formulated composite or coating products is commercially acceptable. Leading GNP producers including NanoXplore, XG Sciences, and Sixth Element (Changzhou) have established multi-ton annual production capacities that are progressively reducing GNP material costs and enabling volume commercial supply agreements with industrial customers in composites, coatings, and battery materials markets.

However, the monolayer and few-layer graphene segment is poised to register the highest CAGR during the forecast period. High-quality monolayer and bilayer graphene produced by CVD processes on copper or nickel catalyst foils represents the graphene material type with the most extraordinary individual property profile, possessing the full theoretical carrier mobility, mechanical strength, optical transparency, and impermeability of ideal graphene that is progressively degraded by the additional inter-layer interactions and defect density of thicker GNP materials. The growth of this segment is driven by the advancing commercialization of flexible electronics, next-generation semiconductor devices, and specialized sensor and biosensor applications that require the exceptional electronic and optical properties of single-layer graphene and are prepared to absorb the higher cost of CVD graphene at the nanogram to microgram material quantities consumed per device unit. Graphenea has established itself as a leading commercial supplier of CVD graphene films and wafers to the electronics research and development community and is scaling production to serve emerging commercial electronics applications.

By Production Method: In 2026, Chemical Vapor Deposition (CVD) to Hold the Largest Share

Based on production method, the global graphene market is segmented into chemical vapor deposition (CVD), mechanical exfoliation, liquid phase exfoliation, chemical reduction methods, and other emerging methods. In 2026, the CVD segment is expected to account for the largest share of the global graphene market by value, reflecting the premium pricing of high-quality CVD graphene films relative to exfoliation-derived graphene materials and the critical importance of CVD graphene in the highest-value electronics, semiconductor, and specialty sensor application markets. CVD graphene production involves the catalytic decomposition of hydrocarbon precursor gases such as methane on heated metal catalyst substrates, typically copper foil, at temperatures of 1,000 degrees Celsius or above, producing continuous monolayer or few-layer graphene films of exceptionally high crystalline quality with defect densities and carrier mobilities substantially superior to any graphene material produced by exfoliation or chemical methods. The premium quality of CVD graphene supports premium pricing of USD 50 to over USD 500 per square centimeter for research-grade material, establishing CVD as the dominant method by market value despite producing substantially lower material volumes than exfoliation-based production methods.

However, the liquid phase exfoliation segment is projected to register the highest CAGR during the forecast period. Liquid phase exfoliation, which produces graphene nanoplatelets by ultrasonically processing graphite in suitable solvent or surfactant-stabilized aqueous dispersion systems, is the most scalable and cost-effective graphene production method compatible with industrial production volumes and the low material cost requirements of high-volume composites, coatings, and energy storage additive applications. Progressive improvements in liquid phase exfoliation process parameters including optimized solvent systems, high-shear processing equipment adaptations, and improved centrifugal classification of exfoliated graphene thickness distributions are enabling producers to increase the yield of few-layer graphene content in exfoliated product and improve the consistency and reproducibility of exfoliated graphene material specifications, addressing two of the primary limitations that have historically constrained the commercial adoption of liquid phase exfoliated graphene in industrial applications requiring consistent material performance.

By Application: In 2026, Energy Storage to Hold the Largest Share

Based on application, the global graphene market is segmented into energy storage (lithium-ion batteries, supercapacitors, fuel cells), composites and advanced materials (polymer composites, metal matrix composites, ceramic composites), electronics and semiconductors (flexible electronics, conductive inks and films, sensors and transistors), coatings and paints (anti-corrosion, conductive, thermal), biomedical applications (drug delivery, biosensors, tissue engineering), environmental applications (water treatment, air purification), and other applications. In 2026, the energy storage segment is expected to account for the largest share of the global graphene market. The energy storage segment's dominant position reflects the combination of the very large and rapidly growing commercial battery market driven by EV and grid storage demand, the commercially demonstrated performance improvement that graphene additives deliver in lithium-ion battery electrodes, and the progressive qualification of graphene-enhanced battery materials by leading cell manufacturers. Graphene's role in improving the rate capability and cycle life of lithium-ion battery anodes and its application as a conductive additive in cathode slurry formulations are both generating commercial demand from battery manufacturers seeking incremental performance improvements to differentiate their products in competitive EV cell supply markets. The supercapacitor subsegment is growing strongly as graphene-based electrode materials enable higher energy density supercapacitor products serving applications including regenerative braking energy recovery, grid frequency regulation, and industrial UPS systems.

However, the electronics and semiconductors segment is projected to register the highest CAGR during the forecast period. The growth of this segment is driven by the advancing commercialization of flexible and wearable electronics applications requiring graphene's unique combination of electrical conductivity and mechanical flexibility, the growing adoption of graphene-based conductive inks in printed electronics manufacturing, the development of graphene field-effect transistor sensors for healthcare diagnostics and environmental monitoring, and the potential long-term substitution of CVD graphene for indium tin oxide as the transparent electrode material of choice in flexible display and photovoltaic applications. The progressive maturation of graphene transfer and integration processes that enable CVD graphene to be incorporated into practical device manufacturing workflows without prohibitive defect introduction or yield loss is the key technical enabler driving the electronics application segment's growth trajectory.

By End-Use Industry: In 2026, Energy and Power to Hold the Largest Share

Based on end-use industry, the global graphene market is segmented into energy and power, electronics and semiconductor, automotive and aerospace, healthcare and biomedical, construction, chemicals and materials, and others. In 2026, the energy and power segment is expected to account for the largest share of the global graphene market. The energy and power sector's dominant consumption of graphene reflects the large and rapidly growing commercial scale of the EV battery supply chain and grid energy storage markets that are the primary commercial demand drivers for graphene-enhanced electrode materials, conductive additives, and thermal management materials. The adoption of graphene as a battery anode additive and supercapacitor electrode material by energy storage product manufacturers is generating sustained volume demand growth that is scaling in line with the extraordinary expansion of global battery production capacity. The energy sector's demand for graphene in thermal management applications for power electronics, battery thermal interface materials, and heat spreader films is also growing as the thermal management challenge of high-power-density EV battery systems and power conversion electronics drives adoption of graphene's exceptional thermal conductivity in engineered thermal management material formulations.

However, the healthcare and biomedical segment is projected to register the highest CAGR during the forecast period. The advancing maturation of graphene biomedical research from laboratory investigation toward clinical translation and eventual product commercialization is driving rapidly accelerating investment in graphene biomedical application development. The progression of graphene oxide drug delivery carrier systems toward preclinical animal study validation, the commercialization of graphene-based biosensor platforms for point-of-care diagnostic applications, and the development of graphene neural electrode arrays for brain-computer interface research are collectively advancing a portfolio of graphene biomedical innovations that are establishing the safety, efficacy, and manufacturability evidence base required for regulatory pathway engagement and eventual commercial product launch. The healthcare sector's premium pricing tolerance for advanced materials demonstrating clear clinical performance advantages positions graphene biomedical applications as a high-value commercial segment with strong margin potential for producers that successfully navigate the biocompatibility validation and regulatory approval requirements of medical device and drug delivery markets.

By Form: In 2026, Powder to Hold the Largest Share

Based on form, the global graphene market is segmented into powder, dispersion, film and sheet, and foam. In 2026, the powder segment is expected to account for the largest share of the global graphene market. Graphene powder, encompassing graphene nanoplatelet powders, graphene oxide powders, and reduced graphene oxide powders, represents the most versatile commercial graphene form because it can be processed, dispersed, and incorporated into an extremely broad range of end-use formulations including polymer composite matrices, coating formulations, battery electrode slurries, and specialty chemical systems by the purchaser using their own compounding or dispersion processing equipment. The powder form's compatibility with existing industrial material handling, blending, and compounding infrastructure widely deployed in the composites, coatings, plastics, and chemical manufacturing industries minimizes the process adaptation requirements for industrial customers adopting graphene as a raw material input, supporting broader commercial adoption relative to graphene forms that require specialized handling or deposition equipment. Leading powder graphene producers including NanoXplore, Sixth Element (Changzhou), and Angstron Materials are supplying commercial-grade GNP and GO powders in kilogram to multi-ton quantities to industrial customers across composites, coatings, battery materials, and lubricants application markets.

However, the dispersion segment is projected to register the highest CAGR during the forecast period. Pre-dispersed graphene liquid formulations, in which graphene nanoplatelets or graphene oxide are stably suspended in water, common organic solvents, or polymer resin systems at optimized concentrations and surface chemistries, are increasingly preferred by industrial customers in coatings, adhesives, and printed electronics applications because they eliminate the dispersion quality variability that arises when customers independently process dry graphene powder into application formulations. The technical challenge of achieving uniform, stable, and defect-free dispersion of graphene nanoplatelets in liquid media without re-aggregation requires specialized processing technology and surface functionalization expertise that graphene producers possess and that many of their industrial customers lack. By supplying pre-dispersed graphene in ready-to-use liquid formulations, graphene producers can deliver more consistent application performance to their customers while capturing additional value added relative to commodity powder supply. The growth of conductive ink, anti-corrosion coating, and functional adhesive applications that specifically require liquid graphene dispersion forms is driving strong demand growth for this product category.

Graphene Market by Region: Asia-Pacific Leading by Share, North America by Growth

Based on geography, the global graphene market is segmented into Asia-Pacific, North America, Europe, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global graphene market. Asia-Pacific's dominant position in the global graphene market reflects China's status as the world's largest graphene producer by volume, with an estimated production capacity representing the majority of global commercial graphene output distributed across a large ecosystem of graphene manufacturers concentrated in graphene industrial parks established in Jiangsu Province, Shandong Province, and Chongqing Municipality with government support under China's national advanced materials development programs. China's domestic graphene demand is driven by the world's largest battery manufacturing base consuming graphene-enhanced electrode materials, the large electronics and semiconductor manufacturing sector requiring conductive inks and specialty films, and the automotive composite applications of a vehicle manufacturing industry producing over 30 million vehicles annually. South Korea's advanced semiconductor and display manufacturing industry, including Samsung Electronics and LG Display, represents a major Asia-Pacific demand center for high-quality CVD graphene films evaluated for next-generation display electrode applications. Japan's precision materials and specialty chemicals industry contributes both graphene material production capability and sophisticated application demand across thermal management, electronics, and advanced composite categories. India's rapidly growing graphene research activity, supported by the Department of Science and Technology's nano-mission funding and the establishment of the Centre for Nano and Soft Matter Sciences, is building an early-stage domestic graphene industry that is beginning to transition laboratory graphene research outcomes toward commercial application development.

However, the North American graphene market is expected to grow at the fastest CAGR during the forecast period. North America's rapid growth trajectory is driven by the accelerating commercialization of graphene applications in the United States' large and innovation-driven advanced materials, energy storage, and electronics industries. The U.S. graphene research ecosystem, which encompasses hundreds of university research groups, Department of Energy national laboratories, and defense research programs generating graphene intellectual property and application innovations at a pace that exceeds any other global region outside China, is providing a robust pipeline of commercial opportunities that U.S.-based and international graphene producers are competing to serve. The Inflation Reduction Act's substantial incentives for domestic battery manufacturing are accelerating U.S. gigafactory investment and creating a large captive domestic market for battery-grade graphene materials that North American graphene producers including NanoXplore's U.S. operations are positioned to serve. Canada's NanoXplore has established a significant commercial graphene production operation in Quebec and is developing graphene-enhanced battery material formulations in collaboration with automotive and battery manufacturing partners, positioning Canada as a growing graphene production and application development hub within the North American market.

Europe occupies a distinctive position in the global graphene market as the region with the world's largest publicly funded graphene research and commercialization program: the EU Graphene Flagship, a ten-year, one-billion-euro research and innovation initiative that has funded graphene research and application development activities at over 150 academic and industrial partner organizations across EU member states and associated countries. The Graphene Flagship's sustained funding of applied graphene research in energy storage, composites, electronics, biomedical, and sensors applications has created a rich portfolio of graphene technology innovations and industrial partnerships that are progressively transitioning toward commercial product development and market entry. UK-based graphene companies including Directa Plus, Haydale Graphene Industries, Applied Graphene Materials, and Versarien have benefited from proximity to the University of Manchester's National Graphene Institute, the global center of graphene research excellence established where Andre Geim and Konstantin Novoselov first isolated and characterized graphene in 2004, and have developed commercial graphene products for coatings, composites, textiles, and functional material applications serving European and international industrial customers. Spain's Graphenea has established a leading position in the supply of high-quality CVD graphene films and graphene oxide materials to the global research and early commercial electronics market from its San Sebastian production facility.

The global graphene market is highly fragmented, with a large number of producers competing across different graphene material types, production methods, and application market segments without any single company achieving dominant market position across the full scope of the commercial graphene market. Competition is focused on graphene material quality and consistency, production cost and scalability, application development support capability, customer-specific material customization, and the ability to demonstrate commercially relevant performance improvements in customer end-use applications that justify graphene adoption over conventional material alternatives. The market includes both specialized graphene-pure-play companies that have built their entire business around graphene production and application development, and subsidiaries or business units of larger chemical and materials companies that have added graphene to their advanced materials portfolios.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' graphene material portfolios, production capabilities, application development programs, geographic market presence, and key strategic developments. Some of the key players operating in the global graphene market include Directa Plus S.p.A. (Italy), First Graphene Ltd. (Australia), Haydale Graphene Industries plc (U.K.), Graphenea S.A. (Spain), Versarien plc (U.K.), XG Sciences Inc. (U.S.), ACS Material LLC (U.S.), Thomas Swan and Co. Ltd. (U.K.), NanoXplore Inc. (Canada), Global Graphene Group (U.S.), Angstron Materials Inc. (U.S.), Applied Graphene Materials plc (U.K.), Talga Group Ltd. (Australia), Graphite India Limited (India), and Sixth Element (Changzhou) Materials Technology Co., Ltd. (China), among others.

The global graphene market is expected to reach USD 4.8 billion by 2036 from an estimated USD 1.4 billion in 2026, at a CAGR of 13.2% during the forecast period 2026 to 2036.

In 2026, the graphene nanoplatelets (GNPs) segment is expected to hold the largest share of the global graphene market, driven by GNPs' scalable production economics, broad commercial application compatibility across composites, coatings, and energy storage markets, and the large established production capacity of global GNP manufacturers that enables volume supply at commercially viable material costs.

The monolayer and few-layer graphene segment is expected to register the highest CAGR during the forecast period 2026 to 2036, driven by the advancing commercialization of flexible electronics, next-generation semiconductor devices, and high-sensitivity biosensor applications that require the exceptional electronic and optical properties of single and bilayer CVD graphene and are prepared to absorb its premium production cost.

In 2026, the chemical vapor deposition (CVD) segment is expected to hold the largest share of the global graphene market by value, reflecting the premium pricing of high-quality CVD graphene films serving electronics, semiconductor, and specialty sensor applications that require the superior crystalline quality and carrier mobility achievable only through CVD production methods.

In 2026, the energy storage segment is expected to hold the largest share of the global graphene market, driven by the commercially demonstrated performance improvements that graphene additives deliver in lithium-ion battery electrodes and supercapacitor electrode materials, supported by the very large and rapidly growing commercial scale of EV battery and grid energy storage markets that are the primary demand drivers for graphene-enhanced energy storage materials.

The growth of this market is primarily driven by the progressive reduction of graphene production costs expanding commercial application viability across composites, coatings, and energy storage markets; the rapidly growing demand from electric vehicle and grid energy storage battery manufacturers for graphene-enhanced electrode materials delivering improved rate capability and cycle life; the development of flexible and wearable electronics creating new commercial demand for CVD graphene films and conductive inks; and the advancing biomedical application pipeline establishing graphene's potential in drug delivery, biosensing, and neural interface applications with substantial long-term commercial value.

Key players are Directa Plus S.p.A. (Italy), First Graphene Ltd. (Australia), Haydale Graphene Industries plc (U.K.), Graphenea S.A. (Spain), Versarien plc (U.K.), XG Sciences Inc. (U.S.), ACS Material LLC (U.S.), Thomas Swan and Co. Ltd. (U.K.), NanoXplore Inc. (Canada), Global Graphene Group (U.S.), Angstron Materials Inc. (U.S.), Applied Graphene Materials plc (U.K.), Talga Group Ltd. (Australia), Graphite India Limited (India), and Sixth Element (Changzhou) Materials Technology Co., Ltd. (China), among others.

North America is expected to register the highest growth rate in the global graphene market during the forecast period 2026 to 2036, driven by the accelerating commercialization of graphene applications in the U.S. advanced materials, EV battery, and electronics industries; substantial federal investment in graphene research and application development through DOE, NSF, and DARPA programs; the Inflation Reduction Act's incentives for domestic battery manufacturing creating large captive demand for graphene battery materials; and Canada's NanoXplore establishing a commercially significant graphene production and application development platform serving North American industrial markets.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection and Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research and Validation

2.2.2.1. Primary Interviews with Experts

2.2.2.2. Approaches for Country/Region-Level Analysis

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Rising Demand for Lightweight and High-Strength Materials

4.2.1.2. Increasing Adoption in Energy Storage Applications

4.2.1.3. Growth in Electronics and Semiconductor Applications

4.2.1.4. Expanding Use in Composites and Coatings

4.2.2. Restraints

4.2.2.1. High Production Costs

4.2.2.2. Lack of Standardization and Quality Variability

4.2.2.3. Scalability Challenges

4.2.3. Opportunities

4.2.3.1. Graphene in Next-Generation Batteries and Supercapacitors

4.2.3.2. Growth in Flexible and Wearable Electronics

4.2.3.3. Expansion in Biomedical Applications

4.2.3.4. Increasing Use in Sustainable Materials

4.2.4. Challenges

4.2.4.1. Commercialization Gap Between Research and Industry

4.2.4.2. Integration with Existing Manufacturing Processes

4.3. Technology Landscape

4.3.1. Chemical Vapor Deposition (CVD)

4.3.2. Mechanical Exfoliation

4.3.3. Liquid Phase Exfoliation

4.3.4. Reduction of Graphene Oxide (rGO)

4.3.5. Emerging Scalable Production Techniques

4.4. Graphene Value Chain and Material Architecture

4.4.1. Raw Material (Graphite Sources)

4.4.2. Graphene Production

4.4.3. Material Processing and Functionalization

4.4.4. Integration into End Products

4.5. Value Chain Analysis

4.5.1. Raw Material Suppliers

4.5.2. Graphene Producers

4.5.3. Composite and Material Manufacturers

4.5.4. End-Use Industry Players

4.6. Regulatory and Standards Landscape

4.6.1. Material Safety and Handling Regulations

4.6.2. Standardization Efforts (ISO, ASTM)

4.6.3. Environmental and Sustainability Regulations

4.7. Porter's Five Forces Analysis

4.8. Investment and Industry Trends

4.8.1. Government Funding and Research Initiatives

4.8.2. Commercialization Strategies

4.8.3. Strategic Partnerships and Collaborations

4.9. Cost and Pricing Analysis

4.9.1. Cost by Production Method

4.9.2. Price Trends by Graphene Type

4.9.3. Cost vs Performance Trade-offs

5. Graphene Market, by Material Type

5.1. Introduction

5.2. Graphene Nanoplatelets (GNPs)

5.3. Graphene Oxide (GO)

5.4. Reduced Graphene Oxide (rGO)

5.5. Monolayer and Few-Layer Graphene

5.6. Functionalized Graphene

6. Graphene Market, by Production Method

6.1. Introduction

6.2. Chemical Vapor Deposition (CVD)

6.3. Mechanical Exfoliation

6.4. Liquid Phase Exfoliation

6.5. Chemical Reduction Methods

6.6. Other Emerging Methods

7. Graphene Market, by Application

7.1. Introduction

7.2. Energy Storage

7.2.1. Lithium-Ion Batteries

7.2.2. Supercapacitors

7.2.3. Fuel Cells

7.3. Composites and Advanced Materials

7.3.1. Polymer Composites

7.3.2. Metal Matrix Composites

7.3.3. Ceramic Composites

7.4. Electronics and Semiconductors

7.4.1. Flexible Electronics

7.4.2. Conductive Inks and Films

7.4.3. Sensors and Transistors

7.5. Coatings and Paints

7.5.1. Anti-Corrosion Coatings

7.5.2. Conductive Coatings

7.5.3. Thermal Coatings

7.6. Biomedical Applications

7.6.1. Drug Delivery Systems

7.6.2. Biosensors

7.6.3. Tissue Engineering

7.7. Environmental Applications

7.7.1. Water Treatment and Filtration

7.7.2. Air Purification

7.8. Other Applications

8. Graphene Market, by End-Use Industry

8.1. Introduction

8.2. Energy and Power

8.3. Electronics and Semiconductor

8.4. Automotive and Aerospace

8.5. Healthcare and Biomedical

8.6. Construction

8.7. Chemicals and Materials

8.8. Others

9. Graphene Market, by Form

9.1. Introduction

9.2. Powder

9.3. Dispersion

9.4. Film and Sheet

9.5. Foam

10. Graphene Market, by Geography

10.1. Introduction

10.2. North America

10.2.1. U.S.

10.2.2. Canada

10.3. Europe

10.3.1. Germany

10.3.2. U.K.

10.3.3. France

10.3.4. Italy

10.3.5. Spain

10.3.6. Sweden

10.3.7. Norway

10.3.8. Netherlands

10.3.9. Rest of Europe

10.4. Asia-Pacific

10.4.1. China

10.4.2. Japan

10.4.3. South Korea

10.4.4. India

10.4.5. Taiwan

10.4.6. Australia

10.4.7. Singapore

10.4.8. Rest of Asia-Pacific

10.5. Latin America

10.5.1. Brazil

10.5.2. Mexico

10.5.3. Argentina

10.5.4. Chile

10.5.5. Colombia

10.5.6. Rest of Latin America

10.6. Middle East and Africa

10.6.1. UAE

10.6.2. Saudi Arabia

10.6.3. South Africa

10.6.4. Turkey

10.6.5. Rest of Middle East and Africa

11. Competitive Landscape

11.1. Overview

11.2. Key Growth Strategies

11.3. Competitive Benchmarking

11.4. Competitive Dashboard

11.4.1. Industry Leaders

11.4.2. Market Differentiators

11.4.3. Vanguards

11.4.4. Emerging Companies

11.5. Market Ranking/Positioning Analysis of Key Players, 2025

12. Company Profiles

12.1. Directa Plus S.p.A.

12.2. First Graphene Ltd.

12.3. Haydale Graphene Industries plc

12.4. Graphenea S.A.

12.5. Versarien plc

12.6. XG Sciences Inc.

12.7. ACS Material LLC

12.8. Thomas Swan and Co. Ltd.

12.9. NanoXplore Inc.

12.10. Global Graphene Group

12.11. Angstron Materials Inc.

12.12. Applied Graphene Materials plc

12.13. Talga Group Ltd.

12.14. Graphite India Limited

12.15. Sixth Element (Changzhou) Materials Technology Co., Ltd.

13. Appendix

13.1. Additional Customization

13.2. Related Reports

Published Date: Feb-2026

Published Date: Sep-2025

Published Date: Apr-2026

Subscribe to get the latest industry updates