Resources

About Us

Nano-Coatings Market Size, Share & Trends Analysis by Material Type (Metal Oxide-Based, Carbon-Based, Polymer-Based, Nanocomposite), Application Method (Spray, CVD, PVD), End-Use Industry, and Substrate Type - Global Opportunity Analysis & Industry Forecast (2026–2036)

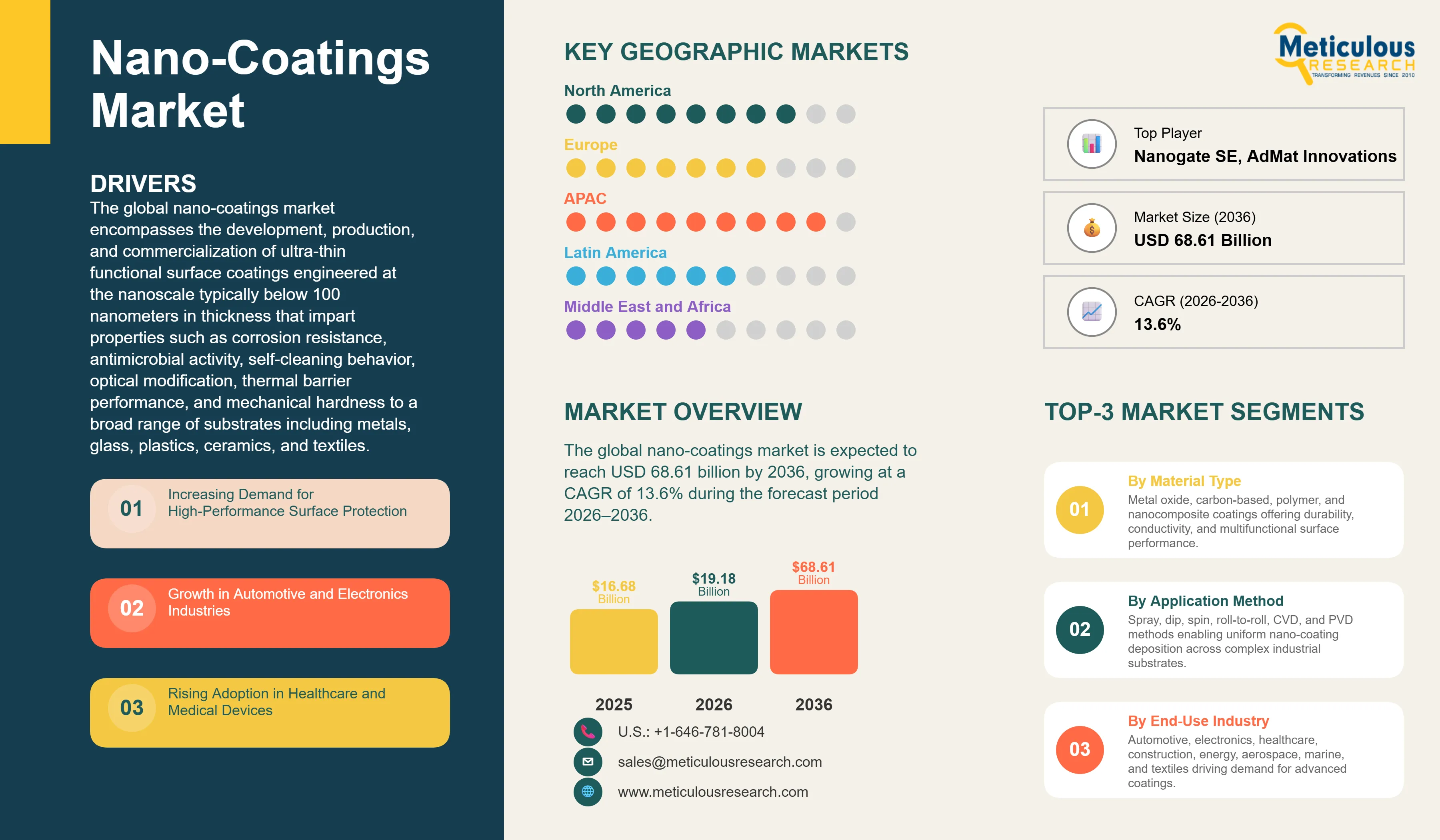

Report ID: MRCHM - 1041884 Pages: 289 Apr-2026 Formats*: PDF Category: Chemicals and Materials Delivery: 24 to 72 Hours Download Free Sample ReportThe global nano-coatings market was valued at USD 16.68 billion in 2025. This market is expected to reach USD 68.61 billion by 2036 from an estimated USD 19.18 billion in 2026, growing at a CAGR of 13.6% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global nano-coatings market encompasses the development, production, and commercialization of ultra-thin functional surface coatings engineered at the nanoscale—typically below 100 nanometers in thickness—that impart properties such as corrosion resistance, antimicrobial activity, self-cleaning behavior, optical modification, thermal barrier performance, and mechanical hardness to a broad range of substrates including metals, glass, plastics, ceramics, and textiles. The market serves end-use industries spanning automotive, electronics and semiconductors, healthcare and medical devices, construction and infrastructure, energy, aerospace and defense, marine, and textiles, applying nano-coating technologies through deposition methods including spray coating, dip coating, spin coating, chemical vapor deposition, physical vapor deposition, and layer-by-layer assembly.

The growth of the global nano-coatings market is primarily driven by the intensifying industrial demand for surface protection solutions that deliver performance characteristics inaccessible through conventional coating technologies. In the automotive sector, nano-coatings providing superior scratch resistance, hydrophobic self-cleaning behavior, and UV stability are increasingly adopted as factory-applied and aftermarket finishes, with the expanding global vehicle fleet and the transition toward electric vehicles creating new coating requirements for battery system components and lightweight structural materials. In the electronics sector, the continued miniaturization of devices and the proliferation of consumer electronics requiring moisture protection, anti-fingerprint properties, and electromagnetic interference shielding are driving strong and sustained demand for nano-coatings formulated for complex substrate geometries and sensitive electronic components. The healthcare industry's growing adoption of antimicrobial nano-coatings for hospital surfaces, medical devices, and implantable materials has been further accelerated by heightened infection control awareness, creating a rapidly expanding application segment with stringent performance and biocompatibility requirements.

Two significant opportunities are shaping the market's long-term trajectory. The global expansion of renewable energy infrastructure—particularly solar photovoltaic installations and wind turbines—is generating substantial demand for nano-coatings providing anti-reflective, self-cleaning, anti-icing, and corrosion-resistant properties that improve energy generation efficiency and reduce maintenance costs. Simultaneously, the growing adoption of smart textiles and wearable technology is creating emerging demand for flexible nano-coatings that impart water repellency, antimicrobial properties, and electronic functionality to fiber substrates without compromising breathability or comfort, opening a new and rapidly expanding product category for nano-coating formulators and application service providers.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 68.61 Billion |

|

Market Size in 2026 |

USD 19.18 Billion |

|

Market Size in 2025 |

USD 16.68 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 13.6% |

|

Dominating Material Type |

Metal Oxide-Based Nano-Coatings |

|

Fastest Growing Material Type |

Carbon-Based Nano-Coatings |

|

Dominating Application Method |

Spray Coating |

|

Fastest Growing Application Method |

Chemical Vapor Deposition (CVD) |

|

Dominating End-Use Industry |

Automotive |

|

Fastest Growing End-Use Industry |

Energy (Solar, Wind) |

|

Dominating Substrate Type |

Metals |

|

Fastest Growing Substrate Type |

Textiles |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

North America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Growth of Multifunctional Nano-Coatings

The development and commercialization of nano-coatings that simultaneously deliver multiple functional properties—such as combined corrosion resistance, antimicrobial activity, and self-cleaning behavior within a single coating layer—represents the defining innovation trend in the global nano-coatings market. Traditional coating approaches required multiple sequential layers to achieve multiple protective functions, increasing process complexity, material cost, substrate weight, and application time. Advances in nano-coating formulation chemistry, particularly in the design of composite nanomaterial systems that integrate metal oxide nanoparticles with polymer matrices and functional organic additives, are enabling single-layer coatings that deliver two to four simultaneous functional properties at coating thicknesses of 50 to 200 nanometers.

In the automotive sector, multifunctional nano-coatings providing scratch resistance, UV stability, hydrophobicity, and anti-soiling properties are being adopted by OEMs seeking to reduce body panel maintenance requirements and extend appearance durability. In the healthcare sector, coatings combining antibacterial silver nanoparticle functionality with biocompatible polymer matrices and drug-eluting capability are advancing toward clinical application in implantable devices and catheter systems. Leading nano-coating developers including PPG Industries, Nanogate, and BASF are investing significant R&D resources in multifunctional coating platforms that can serve multiple end-use markets from a shared material technology base, reducing development cost and accelerating commercialization timelines for new application segments.

Rise of Self-Healing and Anti-Fouling Coatings

The emergence of self-healing nano-coatings—materials engineered to autonomously repair surface damage such as micro-scratches and cracks without human intervention—represents one of the most technologically significant trends reshaping the advanced coatings market. Self-healing functionality is achieved through several nano-engineering approaches, including microencapsulated healing agents that rupture and release reactive monomers upon mechanical damage, reversible covalent bond chemistries that reform broken molecular connections upon mild heat or UV exposure, and shape-memory polymer networks that recover their original geometry upon activation. These technologies are advancing from laboratory demonstration toward industrial commercialization, with automotive clear coats and aerospace structural coatings representing the primary near-term application targets.

Anti-fouling nano-coatings—surface treatments that prevent the adhesion and accumulation of biological organisms, mineral deposits, and contaminating particles—are growing strongly in marine, industrial, and medical applications. In the marine sector, biocide-free nano-coating systems based on ultra-low surface energy fluoropolymer and silicone nanostructures are gaining adoption as environmentally compliant alternatives to tributyltin-based anti-fouling paints that are subject to increasingly stringent international maritime regulations. In industrial heat exchangers, pipelines, and process equipment, anti-fouling nano-coatings that prevent scale deposition and biofilm formation are generating significant energy savings and maintenance cost reductions. The convergence of self-healing and anti-fouling functionalities in next-generation nano-coating systems is a research focus that multiple major specialty coating companies are pursuing through collaborative academic and industrial R&D programs.

Increasing Adoption of Eco-Friendly and Water-Based Coatings

The progressive regulatory restriction of volatile organic compound (VOC) emissions from coating processes across North America, Europe, and increasingly Asia-Pacific is driving a fundamental formulation shift in the nano-coatings industry from solvent-based toward water-based and high-solids coating systems. The European Union's VOC Directive and the U.S. EPA's National Emission Standards for Hazardous Air Pollutants from surface coating operations have established binding VOC content limits that are incompatible with many traditional solvent-borne nano-coating formulations, creating a regulatory imperative for reformulation investment across the industry. Water-based nano-coating systems incorporating inorganic nanoparticle dispersions and waterborne polymer binders have achieved significant performance advances in recent years, with improved substrate adhesion, reduced drying times, and enhanced durability narrowing the performance gap with solvent-borne systems across many applications.

The development of bio-based and sustainable nanomaterial feedstocks—including cellulose nanocrystals, chitosan nanoparticles, and lignin-derived nano-additives—is an emerging research frontier that aligns nano-coating development with broader sustainability objectives in materials manufacturing. These bio-derived nanomaterials offer the dual advantages of renewable sourcing and inherent biodegradability, addressing both the raw material sustainability and end-of-life environmental footprint concerns that are increasingly influencing purchasing decisions among sustainability-conscious industrial end users in the automotive, construction, and packaging sectors.

Increasing Demand for High-Performance Surface Protection

The intensifying industrial requirement for surface protection solutions that deliver functional performance beyond the capability of conventional coatings is the primary structural driver of the global nano-coatings market. Conventional paints and coatings provide adequate bulk barrier protection but are limited in their ability to impart specialized surface functionalities including superhydrophobicity, photocatalytic self-cleaning, antimicrobial activity, and extreme hardness without the application of thick, heavy coating layers that add weight and processing complexity. Nano-coatings address this performance gap by enabling functional surface engineering at the molecular and nanoscale level, delivering superior property profiles at coating thicknesses of 10 to 500 nanometers that are imperceptible in terms of weight or dimensional impact on the coated substrate. This performance advantage over conventional coatings is generating sustained demand across industrial sectors where surface durability, functional performance, and weight minimization are critical design parameters, including aerospace, automotive, electronics, and medical devices.

Growth in Automotive and Electronics Industries

The automotive and electronics industries collectively represent the two largest end-use markets for nano-coatings and are both experiencing structural demand growth driven by their respective technology transitions. In the automotive sector, the global transition toward electric vehicles is creating new nano-coating requirements for battery cell and module protection, thermal management, corrosion resistance of aluminum-intensive vehicle structures, and the surface treatment of lightweight composite body panels. The global EV market is projected to grow from 17 million units in 2024 to over 40 million units annually by the mid-2030s, directly expanding the addressable market for automotive nano-coatings. In the electronics sector, the continued miniaturization of semiconductor devices and the growth of consumer electronics, 5G infrastructure, and IoT devices are generating sustained demand for conformal nano-coatings providing moisture protection, dielectric insulation, and thermal management for increasingly compact and complex electronic assemblies.

Expansion in Renewable Energy (Solar Panels, Wind)

The global expansion of solar photovoltaic and wind energy installations is creating a rapidly growing and large-scale application opportunity for nano-coatings designed to improve energy generation efficiency and reduce operational maintenance costs. Anti-reflective nano-coatings applied to solar panel glass surfaces reduce light reflection losses from approximately 8% to less than 1%, directly improving photovoltaic conversion efficiency by 2 to 4 percentage points—a performance gain with substantial economic value at gigawatt-scale solar installations. Self-cleaning nano-coatings for solar panel surfaces minimize dust accumulation losses that can reduce power output by 10 to 30% in arid regions without regular manual cleaning, providing significant value in utility-scale solar installations in the Middle East, North Africa, India, and the U.S. Southwest where water scarcity makes conventional panel cleaning economically and environmentally costly. Wind turbine blade coatings incorporating nano-additive erosion protection are addressing the leading edge erosion problem that degrades blade aerodynamic efficiency and reduces turbine operational lifetime, creating a large and growing maintenance and new installation coating market.

Growth in Anti-Microbial Coatings

The global healthcare sector's heightened focus on infection prevention and surface hygiene, amplified by the pandemic experience, is sustaining strong demand growth for antimicrobial nano-coatings across hospital environments, medical devices, and public infrastructure. Silver nanoparticle-based coatings, copper oxide nano-coatings, and photocatalytic titanium dioxide coatings that generate reactive oxygen species under UV or visible light activation represent the primary commercial antimicrobial nano-coating platforms, with demonstrated efficacy against a broad spectrum of bacterial, viral, and fungal pathogens. The application of antimicrobial nano-coatings to high-touch surfaces in healthcare facilities—including doorknobs, bed rails, IV poles, and surgical instrument handles—is expanding rapidly as hospital infection control protocols are updated to incorporate persistent surface antimicrobial protection as a complementary layer of pathogen control alongside hand hygiene and air filtration systems.

By Material Type: In 2026, Metal Oxide-Based Nano-Coatings to Dominate

Based on material type, the global nano-coatings market is segmented into metal oxide-based nano-coatings, carbon-based nano-coatings, polymer-based nano-coatings, and nanocomposite coatings. In 2026, the metal oxide-based nano-coatings segment is expected to account for the largest share of the global nano-coatings market. The large share of this segment is attributed to the broad commercial deployment of titanium dioxide (TiO2) nano-coatings in self-cleaning, photocatalytic, and UV-protective applications across building facades, solar panels, automotive glass, and medical devices; the extensive use of silicon dioxide (SiO2) nano-coatings in anti-reflective, scratch-resistant, and hydrophilic surface treatments for optical components and electronic displays; and the established commercial availability of zinc oxide (ZnO) and aluminum oxide (Al2O3) nano-coating materials from multiple industrial suppliers serving diverse end-use markets. The chemical stability, photocatalytic activity, and well-understood deposition characteristics of metal oxide nanomaterials make them the preferred nano-coating platform across the broadest range of industrial applications, establishing their dominant market position.

However, the carbon-based nano-coatings segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the commercialization of graphene-based coatings offering exceptional combinations of electrical conductivity, mechanical strength, barrier performance, and thermal conductivity that are unmatched by metal oxide nano-coatings, the advancing development of carbon nanotube composite coatings for structural and functional applications in aerospace and advanced manufacturing, and the strong pipeline of R&D investment in carbon nanomaterial coating technologies from both academic institutions and industrial companies seeking performance differentiation in competitive coating markets.

By Application Method: In 2026, Spray Coating to Hold the Largest Share

Based on application method, the global nano-coatings market is segmented into spray coating, dip coating, spin coating, roll-to-roll coating, chemical vapor deposition, and physical vapor deposition. In 2026, the spray coating segment is expected to account for the largest share of the global nano-coatings market. Spray coating's dominance reflects its versatility for coating large, complex, and irregular substrate geometries that cannot be accommodated by immersion or spin-coating processes, its compatibility with high-throughput industrial production lines in the automotive, construction, and marine sectors, and the wide commercial availability of spray-applicable nano-coating formulations from major coating suppliers including PPG, Akzo Nobel, and Sherwin-Williams that allow end users to integrate nano-coating application into existing spray booth and liquid coating infrastructure without capital-intensive process changes.

However, the chemical vapor deposition segment is projected to register the highest CAGR during the forecast period. This growth is driven by the expanding adoption of CVD processes for semiconductor and microelectronics nano-coating applications where atomic-level film uniformity, conformal step coverage over complex topographies, and precise thickness control below 10 nanometers are requirements inaccessible to liquid-phase coating methods; the growth of CVD-deposited protective coatings for cutting tools, industrial dies, and aerospace components requiring extreme hardness and wear resistance; and the increasing deployment of plasma-enhanced CVD for flexible electronics and optical device manufacturing.

By End-Use Industry: In 2026, Automotive to Hold the Largest Share

Based on end-use industry, the global nano-coatings market is segmented into automotive, electronics and semiconductors, healthcare and medical devices, construction and infrastructure, energy (solar, wind), aerospace and defense, marine, textiles, and others. In 2026, the automotive segment is expected to account for the largest share of the global nano-coatings market. The automotive segment's dominant position reflects the large-scale adoption of nano-coating technologies throughout the vehicle manufacturing process and aftermarket service ecosystem, including nano-ceramic clear coats providing superior scratch and UV resistance on body panels, hydrophobic nano-coatings for windshields improving visibility in wet conditions, nano-coating treatments for aluminum and high-strength steel structural components providing corrosion protection with minimal weight addition, and thermal barrier nano-coatings for engine and exhaust system components enabling higher operating temperatures with improved fuel efficiency. The global production of over 90 million light vehicles annually provides an immense baseline coating demand that positions automotive as the structurally dominant end-use segment.

However, the energy (solar, wind) segment is projected to register the highest CAGR during the forecast period. This growth is driven by the accelerating global deployment of utility-scale and distributed solar photovoltaic installations where anti-reflective and self-cleaning nano-coatings provide direct efficiency and maintenance benefits with clear economic value, the expanding wind turbine installation base generating demand for leading-edge erosion protection nano-coatings, and the alignment of nano-coating performance characteristics with the operational efficiency and maintenance-cost objectives of renewable energy asset operators.

By Substrate Type: In 2026, Metals to Hold the Largest Share

Based on substrate type, the global nano-coatings market is segmented into metals, glass, plastics and polymers, ceramics, textiles, and others. In 2026, the metals segment is expected to account for the largest share of the global nano-coatings market. Metal substrates including steel, aluminum, copper, and titanium alloys represent the most extensively nano-coated substrate category across industrial applications, driven by the large volume of metal components in automotive, aerospace, construction, and industrial equipment applications requiring corrosion protection, wear resistance, and functional surface enhancement. The compatibility of metal substrates with a broad range of nano-coating deposition methods—including thermal spray, CVD, PVD, electrochemical deposition, and liquid-phase spray and dip processes—provides nano-coating formulators and applicators with extensive process flexibility for serving metal substrate coating requirements across diverse performance specifications and production scales.

However, the textiles segment is projected to register the highest CAGR during the forecast period. The high growth of nano-coatings on textile substrates is driven by the rapidly expanding market for smart textiles and performance apparel incorporating water repellency, antimicrobial protection, UV resistance, and emerging electronic sensing functionalities achieved through nano-coating application to fiber surfaces, the growth of wearable technology requiring flexible and washable nano-coating treatments compatible with complex textile topographies, and the expansion of protective workwear markets requiring durable nano-coatings providing flame retardancy, chemical resistance, and cut resistance on textile substrates in industrial safety applications.

Nano-Coatings Market by Region: Asia-Pacific Leading by Share, North America by Growth

Based on geography, the global nano-coatings market is segmented into Asia-Pacific, North America, Europe, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global nano-coatings market. The largest share of this region is mainly due to China's position as the world's largest manufacturer of nanomaterials and nano-coating precursors including titanium dioxide, silicon dioxide, and zinc oxide nanoparticles, its dominant role as the global leader in consumer electronics and semiconductor manufacturing generating intensive demand for precision nano-coatings, and the scale of its automotive manufacturing industry producing over 30 million vehicles annually that consume large volumes of automotive nano-coating treatments. Japan's advanced contribution to nano-coating technology spans high-performance optical nano-coatings for display and imaging applications, specialty coatings for precision electronics, and nano-coating materials for automotive and industrial applications developed by leading companies including AGC, JSR Corporation, and Toray Industries. South Korea's semiconductor and display industries operated by Samsung and SK Hynix, and the automotive operations of Hyundai and Kia, represent additional major consumption centers for specialty nano-coatings within the Asia-Pacific market.

However, the North American nano-coatings market is expected to grow at the fastest CAGR during the forecast period. North America's rapid growth is driven by the strong federal policy support for nanotechnology research and commercialization through the National Nanotechnology Initiative, the large and growing aerospace and defense sector's adoption of advanced nano-coatings for aircraft, naval, and ground vehicle applications, the expanding U.S. renewable energy sector generating demand for solar and wind nano-coatings, and the robust healthcare industry's increasing adoption of antimicrobial and biocompatible nano-coatings for medical devices and hospital infrastructure. The Inflation Reduction Act's substantial incentives for domestic clean energy manufacturing are accelerating the growth of U.S. solar panel and wind turbine production, directly expanding the addressable market for nano-coatings applied during the domestic manufacturing process.

Europe maintains a significant nano-coatings market anchored by its advanced automotive, aerospace, and specialty chemical industries. Germany's automotive OEMs and Tier 1 suppliers are among the most sophisticated adopters of automotive nano-coating technologies globally, and the European aerospace industry's requirements for advanced surface protection coatings drive substantial demand for high-performance nano-coating solutions. The European nano-coatings market is also shaped by the EU's stringent REACH chemical regulations and VOC emission standards, which are driving reformulation investment toward water-based and lower-toxicity nano-coating systems that meet compliance requirements while maintaining functional performance.

The global nano-coatings market is moderately fragmented, with a mix of large diversified coating companies that offer nano-coating product lines alongside their conventional coating portfolios, specialty nanotechnology companies focused exclusively on nano-coating materials and technologies, and application service providers that apply nano-coating treatments using licensed or proprietary processes. Competition is focused on coating performance differentiation, nanomaterial innovation, application process compatibility, regulatory compliance, and the ability to develop and validate coating systems meeting the demanding performance specifications of automotive OEM, aerospace, and medical device customers.

PPG Industries and Akzo Nobel lead the nano-coatings market through their extensive product portfolios of nano-enhanced architectural, automotive, aerospace, and industrial coatings backed by global manufacturing scale and established distribution networks. Sherwin-Williams brings similar scale and market reach to nano-coating technologies deployed across its industrial and commercial coating product lines. BASF contributes advanced functional nanomaterial formulations including nano-silica and nano-titanium dioxide additives that are incorporated into coating systems produced by multiple coating manufacturers. Nanogate and Nanophase Technologies represent the specialized nano-coating pure-play model, developing proprietary nano-coating platforms for targeted high-performance applications in automotive, electronics, and industrial markets.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' product portfolios, application technology capabilities, geographic presence, and key strategic developments. Some of the key players operating in the global nano-coatings market include PPG Industries, Inc. (U.S.), Akzo Nobel N.V. (Netherlands), Sherwin-Williams Company (U.S.), Nanovere Technologies LLC (U.S.), Nanogate SE (Germany), Buhler AG (Switzerland), BASF SE (Germany), DuPont de Nemours, Inc. (U.S.), Nanophase Technologies Corporation (U.S.), Integran Technologies (Canada), Tesla NanoCoatings (U.S.), AdMat Innovations (U.S.), Advanced Nano Products Co., Ltd. (South Korea), Eikos Inc. (U.S.), and Surfix BV (Netherlands), among others.

The global nano-coatings market is expected to reach USD 68.61 billion by 2036 from an estimated USD 19.18 billion in 2026, at a CAGR of 13.6% during the forecast period 2026–2036.

In 2026, the metal oxide-based nano-coatings segment is expected to hold the largest share of the global nano-coatings market, driven by the broad commercial deployment of TiO2, SiO2, ZnO, and Al2O3 nano-coating platforms across self-cleaning, anti-reflective, antimicrobial, and corrosion-protection applications spanning automotive, construction, electronics, and healthcare end markets.

The carbon-based nano-coatings segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the accelerating commercialization of graphene and carbon nanotube coating technologies offering multifunctional performance advantages in electrical, mechanical, and barrier properties for aerospace, electronics, and advanced manufacturing applications.

In 2026, the spray coating segment is expected to hold the largest share of the global nano-coatings market, reflecting its versatility across large and complex substrate geometries, compatibility with existing industrial coating infrastructure, and wide availability of spray-applicable nano-coating formulations for automotive, construction, and marine applications.

In 2026, the automotive segment is expected to hold the largest share of the global nano-coatings market, as the scale of global vehicle production and the extensive adoption of nano-coating technologies in automotive OEM manufacturing and aftermarket surface treatment establish automotive as the structurally dominant demand segment.

The growth of this market is primarily driven by the intensifying industrial demand for high-performance surface protection exceeding the capability of conventional coatings, the strong growth of automotive and electronics industries adopting nano-coating technologies for functional and aesthetic surface enhancement, the expanding renewable energy sector generating demand for efficiency-improving solar and wind nano-coatings, and the healthcare sector's growing adoption of antimicrobial nano-coatings for infection prevention and medical device surface treatment.

Key players are PPG Industries, Inc. (U.S.), Akzo Nobel N.V. (Netherlands), Sherwin-Williams Company (U.S.), Nanovere Technologies LLC (U.S.), Nanogate SE (Germany), Buhler AG (Switzerland), BASF SE (Germany), DuPont de Nemours, Inc. (U.S.), Nanophase Technologies Corporation (U.S.), Integran Technologies (Canada), Tesla NanoCoatings (U.S.), AdMat Innovations (U.S.), Advanced Nano Products Co., Ltd. (South Korea), Eikos Inc. (U.S.), and Surfix BV (Netherlands), among others.

North America is expected to register the highest growth rate in the global nano-coatings market during the forecast period 2026–2036, driven by strong federal nanotechnology R&D investment, the large and growing aerospace and defense sector's adoption of advanced nano-coatings, the expanding renewable energy manufacturing base generating solar and wind coating demand, and the healthcare industry's increasing use of antimicrobial and biocompatible nano-coating technologies.

Published Date: Sep-2025

Published Date: Oct-2024

Published Date: Sep-2024

Published Date: May-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates