Resources

About Us

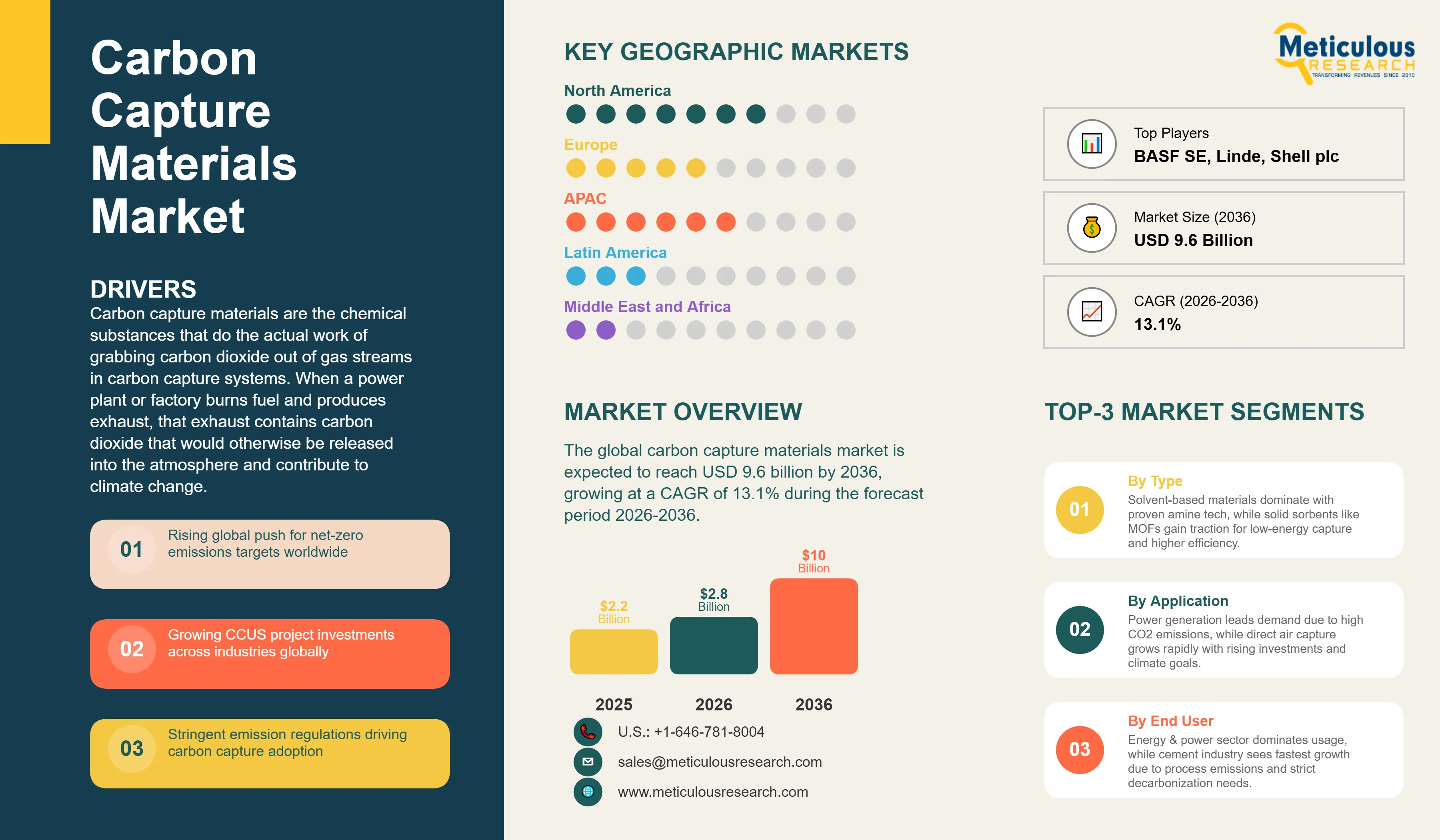

Carbon Capture Materials Market Size, Share & Trends Analysis by Material Type, Capture Mechanism, Application, End-Use Industry, and Form - Global Opportunity Analysis & Industry Forecast (2026-2036)

Report ID: MRCHM - 1041930 Pages: 280 Apr-2026 Formats*: PDF Category: Chemicals and Materials Delivery: 24 to 72 Hours Download Free Sample ReportThe global carbon capture materials market was valued at USD 2.2 billion in 2025. This market is expected to reach USD 9.6 billion by 2036 from an estimated USD 2.8 billion in 2026, growing at a CAGR of 13.1% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Carbon capture materials are the chemical substances that do the actual work of grabbing carbon dioxide out of gas streams in carbon capture systems. When a power plant or factory burns fuel and produces exhaust, that exhaust contains carbon dioxide that would otherwise be released into the atmosphere and contribute to climate change. A carbon capture system passes the exhaust through a material that selectively binds to carbon dioxide and removes it from the gas stream. The carbon dioxide can then be separated from the capture material, compressed, and either stored underground in geological formations or used as a raw material to make products like fuels, chemicals, or construction materials. The capture materials themselves are the essential consumable component of these systems, much like the catalysts or filters in other industrial chemical processes, and they need to be replaced or regenerated on a regular basis as they wear out or degrade.

The market is growing because governments, energy companies, and industrial manufacturers around the world are under increasing pressure to reduce their carbon dioxide emissions under national climate commitments and corporate sustainability targets. For many industries, simply switching to renewable energy is not enough to eliminate their emissions. A cement plant releases carbon dioxide not just from burning fuel but from the chemical process of making cement itself, and a steel mill produces carbon dioxide as a fundamental part of how steel is made from iron ore. For these industries, carbon capture is not an optional add-on but one of the only available pathways to meeting emission reduction targets, making them committed buyers of carbon capture materials and systems over the coming decade. The U.S. Inflation Reduction Act of 2022 provided very large tax credits for carbon capture projects, and similar support mechanisms in the European Union, Canada, and several Asian countries are making carbon capture projects financially viable at scales that were previously uneconomical.

Two significant opportunities are shaping the next phase of market growth. The development of advanced solid sorbent materials and novel membrane technologies promises to deliver carbon capture at significantly lower cost and with less energy consumption than current amine-based liquid solvent systems, and the companies that successfully commercialize these next-generation materials will have a strong cost advantage in the growing carbon capture market. In addition, the expansion of carbon capture into hard-to-abate sectors including cement, steel, and chemicals, which collectively produce a very large share of global industrial emissions and have very limited alternatives to carbon capture for deep decarbonization, represents a large and growing addressable market that is just beginning to adopt carbon capture technology at commercial scale.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 9.6 Billion |

|

Market Size in 2026 |

USD 2.8 Billion |

|

Market Size in 2025 |

USD 2.2 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 13.1% |

|

Dominating Material Type |

Solvent-Based Materials (Amine-Based) |

|

Fastest Growing Material Type |

Solid Sorbents (MOFs) |

|

Dominating Capture Mechanism |

Chemical Absorption |

|

Fastest Growing Capture Mechanism |

Physical Adsorption |

|

Dominating Application |

Power Generation |

|

Fastest Growing Application |

Direct Air Capture (DAC) |

|

Dominating End-Use Industry |

Energy & Power |

|

Fastest Growing End-Use Industry |

Cement |

|

Dominating Form |

Liquid |

|

Fastest Growing Form |

Solid |

|

Dominating Deployment Type |

Point Source Capture |

|

Fastest Growing Deployment Type |

Direct Air Capture (DAC) |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

U.S. Inflation Reduction Act Transforming the Economics of Carbon Capture

The single most commercially significant policy development in the carbon capture materials market in recent years has been the Inflation Reduction Act signed into law in the United States in August 2022, which dramatically increased the tax credit available for captured and permanently stored carbon dioxide under the Internal Revenue Code Section 45Q from USD 50 per tonne to USD 85 per tonne for carbon capture at industrial facilities and USD 180 per tonne for direct air capture. These credit levels, which are available for 12 years after a project begins construction, make a very large number of carbon capture projects financially attractive that were previously uneconomical, and the resulting wave of new project announcements, investment commitments, and capacity expansion plans by carbon capture technology providers and their industrial customers is driving rapid growth in demand for carbon capture materials.

The IRA credits have particularly transformed the economics of carbon capture at natural gas processing facilities, ethanol plants, and industrial manufacturing sites in the U.S. where the concentration of carbon dioxide in the process gas makes capture relatively straightforward and affordable. Carbon capture developers including Carbon Clean, Svante, and several major oil and gas companies have announced numerous new project developments in the U.S. since the IRA's passage, and the resulting increase in project activity is generating growing near-term demand for amine solvents and other carbon capture materials. The IRA's investment tax credit provisions for carbon capture equipment have also made the capital cost of building carbon capture facilities significantly more affordable, further expanding the addressable market for carbon capture materials suppliers.

Direct Air Capture Attracting Enormous Investment as a Climate Solution

Direct air capture, which refers to systems that pull carbon dioxide directly out of the open atmosphere rather than from the concentrated exhaust of a factory or power plant, has attracted a remarkable level of investor attention and government support in recent years, with Climeworks in Switzerland and Heirloom Carbon in the United States among the leading commercial DAC developers. While atmospheric carbon dioxide is only present at about 420 parts per million, much more dilute than in industrial exhaust streams, DAC offers the theoretically important capability to remove carbon dioxide that has already been released to the atmosphere and is contributing to climate change, which point source carbon capture cannot do. The U.S. Department of Energy's commitment of over USD 3.5 billion to four regional DAC hub projects in 2023, and similar government support programs in the UK, Canada, and the European Union, are providing the large-scale demonstration and deployment funding that the DAC industry needs to prove the technology at commercial scale and begin driving down costs through scale.

The DAC market is important for carbon capture materials suppliers because DAC systems require novel capture materials specifically designed for the challenging conditions of low-concentration atmospheric carbon dioxide capture, creating demand for advanced solid sorbent materials, liquid solvent formulations, and hybrid material systems that are different from the materials used in conventional point source carbon capture. Companies including Svante with its structured solid sorbent technology, Carbon Clean with its proprietary solvent formulations, and several research-stage companies developing MOF-based and polymer sorbent materials for DAC applications are developing the next generation of capture materials that will be needed as the DAC industry scales up through the forecast period.

Next-Generation Solid Sorbents and Membranes Targeting Lower Capture Costs

The current commercial standard for carbon capture is amine-based liquid solvent absorption, a technology that has been used in industrial gas processing for decades and works reliably at scale. However, amine solvent systems have well-known cost disadvantages including the energy required to heat the solvent to release the captured carbon dioxide for regeneration, the need to handle large volumes of liquid solvent, and the degradation of amine solvents over time when exposed to oxygen and other contaminants in industrial exhaust streams. The materials research community and a growing number of commercial companies are actively developing alternative capture materials that address these limitations, with the goal of delivering carbon capture at a lower cost per tonne of carbon dioxide removed than current amine systems can achieve.

Metal-organic frameworks, which are engineered porous materials with very high surface areas and precisely designed chemical binding sites for carbon dioxide, are one of the most actively researched classes of next-generation capture materials. MOFs can be designed to selectively bind carbon dioxide with high capacity at low temperatures and release it at relatively low temperatures compared with amine solvents, potentially reducing the energy required for capture and regeneration significantly. Companies including BASF, which has commercialized several MOF products for other applications, and several specialist MOF developers are working toward the commercialization of MOF-based carbon capture materials. Membrane-based separation, which separates carbon dioxide from other gases by passing them through a selective membrane rather than using a chemical binding process, offers another route to lower-energy carbon capture and is being actively developed by membrane technology companies including Membrane Technology and Research.

Increasing Global Focus on Decarbonization and Net-Zero Targets

The primary driver of the carbon capture materials market is the accelerating global commitment to reducing carbon dioxide emissions to net zero, with over 140 countries and hundreds of major corporations having made formal net-zero commitments that require significant reductions in carbon dioxide emissions from industrial processes, power generation, and other sources. The Intergovernmental Panel on Climate Change's assessments have consistently found that meeting global temperature targets requires carbon capture and storage at very large scale alongside massive expansion of renewable energy, energy efficiency, and demand reduction. For industrial sectors including cement, steel, and chemicals where the production processes themselves generate carbon dioxide as a fundamental byproduct of the chemistry involved, carbon capture is identified as an essential technology for achieving net-zero emissions. The policy commitments flowing from the Paris Agreement, reinforced by country-level legislation including the U.S. Inflation Reduction Act, the EU's Carbon Border Adjustment Mechanism, and Canada's carbon pricing system, are creating the regulatory and financial framework that makes carbon capture investment economically rational for industrial operators who would otherwise face increasing costs from carbon pricing systems.

Growth of Carbon Capture, Utilization and Storage Projects

The rapid increase in the number and scale of commercially operating and under-construction carbon capture, utilization, and storage projects globally is creating growing near-term demand for the carbon capture materials that these projects consume. The Global CCS Institute tracks over 400 CCUS facilities in various stages of development globally, a number that has grown substantially in the past five years as policy support and project economics have improved. Large-scale CCUS projects including the Quest Carbon Capture and Storage project operated by Shell in Canada, the Northern Lights offshore storage project in Norway that accepts carbon dioxide from multiple industrial sources for permanent geological storage, the Sleipner CO2 storage project also in Norway that has been operating since 1996, and the large carbon capture facilities associated with natural gas processing in the United States and the Middle East collectively represent a growing installed base of carbon capture capacity that generates ongoing demand for replacement and replenishment of capture materials. The pipeline of new projects across the U.S., Europe, Australia, and Asia-Pacific represents several multiples of current installed capacity and will generate very large future procurement of carbon capture materials as these projects reach construction and operation.

Development of Advanced Sorbents and Membranes

The development of next-generation carbon capture materials that can capture carbon dioxide at lower energy cost and higher efficiency than current amine solvents represents the most commercially transformative opportunity in the carbon capture materials market, because a material that reduces the capture cost from the current USD 50 to USD 100 per tonne range for point source capture toward USD 30 or lower would make carbon capture economically attractive at a much wider range of industrial sites and concentration levels than current technology enables. The research pipeline for advanced capture materials is very active, with metal-organic frameworks offering tunable pore sizes and binding affinities that can be optimized for specific capture applications, polymer sorbent materials that can operate at lower temperatures than amine solvents and avoid the degradation issues that amine systems face in oxygen-containing gas streams, and facilitated transport membranes that achieve high carbon dioxide permeability and selectivity. The companies that successfully scale production of next-generation capture materials with demonstrated performance advantages at commercially relevant scales will have a strong competitive position in a market where cost reduction is the primary commercial priority and where current material costs represent a large share of total system operating expense.

Expansion of Carbon Capture in Hard-to-Abate Sectors

The industrial sectors that produce carbon dioxide as an unavoidable byproduct of their production chemistry, including cement manufacturing which releases carbon dioxide when limestone is converted to calcium oxide, steel production which uses coal as a reducing agent in the blast furnace process, and chemical and petrochemical manufacturing, represent a large and growing addressable market for carbon capture materials that is driven by regulatory necessity rather than optionality. These hard-to-abate sectors collectively account for a large fraction of global industrial carbon dioxide emissions and have very limited technological alternatives to carbon capture for deep emission reductions. The European Union's Carbon Border Adjustment Mechanism, which will impose carbon costs on imports of cement, steel, aluminum, and fertilizers from countries without equivalent carbon pricing, is creating a direct financial incentive for producers in these sectors globally to invest in carbon capture to avoid the trade disadvantage that will result from CBAM implementation. This regulatory driver is expected to catalyze a large wave of carbon capture investment in cement and steel manufacturing specifically, creating growing demand for carbon capture materials in application segments that have so far seen limited deployment.

By Material Type: In 2026, Solvent-Based Materials to Dominate

Based on material type, the global market is segmented into solvent-based materials, solid sorbents, membrane materials, cryogenic materials, and hybrid and emerging materials. In 2026, the solvent-based materials segment is expected to account for the largest share of the global carbon capture materials market. Amine-based liquid solvents, which have been the standard carbon capture technology for industrial gas processing for several decades, remain the most commercially deployed capture material in the world and are used in the majority of currently operating large-scale carbon capture facilities. Monoethanolamine and its derivatives have well-understood performance characteristics, established manufacturing supply chains, and a long operating track record that makes them the default choice for commercial carbon capture projects that need proven technology and regulatory precedent.

However, the solid sorbents segment, particularly metal-organic frameworks, is projected to register the highest CAGR during the forecast period. The strong research and development momentum behind MOF-based and advanced polymer sorbent materials, driven by their potential to significantly reduce the energy requirements and operating costs of carbon capture compared with liquid amine systems, is translating into growing commercial investment and the first pilot and demonstration-scale deployments of advanced solid sorbent capture systems. As these materials progress toward commercial scale and as the cost reduction potential becomes more clearly demonstrated, solid sorbent carbon capture materials are expected to grow significantly faster than the established amine solvent market.

By Capture Mechanism: In 2026, Chemical Absorption to Hold the Largest Share

Based on capture mechanism, the global materials market is segmented into chemical absorption, physical adsorption, membrane separation, and cryogenic separation. In 2026, the chemical absorption segment is expected to account for the largest share of the global carbon capture materials market. Chemical absorption using amine-based liquid solvents that chemically react with carbon dioxide to form stable compounds that can then be broken down by heating to release concentrated carbon dioxide is the most widely deployed and commercially proven carbon capture mechanism. The large installed base of amine absorption carbon capture systems at natural gas processing plants, ammonia production facilities, and the growing number of post-combustion capture projects at power plants and industrial facilities collectively make chemical absorption the dominant revenue mechanism.

However, the physical adsorption segment is projected to register the highest CAGR during the forecast period. Physical adsorption using solid sorbent materials including zeolites, activated carbons, and MOFs that bind carbon dioxide through physical rather than chemical interactions and can be regenerated at lower temperatures than amine solvents is at an earlier stage of commercial deployment but is attracting growing investment as the energy efficiency and operating cost advantages of solid sorbent adsorption become better understood through pilot and demonstration projects.

By Application: In 2026, Power Generation to Hold the Largest Share

Based on application, the global carbon capture materials market is segmented into power generation, oil and gas industry, industrial manufacturing, direct air capture, hydrogen production (blue hydrogen), and other applications. In 2026, the power generation segment is expected to account for the largest share of the global carbon capture materials market. Power generation from coal and natural gas remains the largest single source of carbon dioxide emissions globally, and the deployment of post-combustion carbon capture at coal and gas power plants represents one of the largest potential applications of carbon capture materials. Several large-scale carbon capture projects at power plants have been completed or are under construction, including the Boundary Dam project in Saskatchewan Canada and the Sleipner gas processing facility in Norway, and the large number of planned carbon capture retrofits at natural gas power plants in the U.S. following the Inflation Reduction Act credits represents very large near-term potential demand.

However, the direct air capture segment is projected to register the highest CAGR during the forecast period. The combination of very large government funding commitments to DAC hub projects in the U.S. and Europe, the growing corporate demand for verified carbon removal credits from DAC facilities that can demonstrably remove carbon dioxide from the atmosphere, and the rapid commercial development of DAC systems by Climeworks, Heirloom, and several other companies is driving DAC from a small-scale demonstration technology toward its first commercial-scale deployments, generating fast-growing demand for the novel capture materials these systems require.

By End-Use Industry: In 2026, Energy and Power to Hold the Largest Share

Based on end-use industry, the global carbon capture materials market is segmented into energy and power, oil and gas, cement, steel and metals, chemicals and petrochemicals, and others. In 2026, the energy and power segment is expected to account for the largest share of the global carbon capture materials market. Energy and power generation facilities represent the largest single industrial category for carbon dioxide emissions globally, and the deployment of carbon capture at power plants and gas processing facilities in the U.S., Europe, and Australia is the most commercially advanced application of the technology. The large scale of individual power generation projects means that even a relatively small number of projects generate significant demand for carbon capture materials.

However, the cement segment is projected to register the highest CAGR during the forecast period. Cement production is responsible for approximately 8% of global carbon dioxide emissions, making it one of the largest contributors to industrial emissions. The unique challenge of cement is that roughly half of its carbon dioxide emissions come from the chemical decomposition of limestone in the kiln, not from fuel combustion, which means that no amount of fuel efficiency or renewable energy adoption alone can eliminate cement's emissions. Carbon capture is therefore not optional but essential for the cement industry to meet emission reduction commitments, and the growing regulatory pressure from the EU CBAM and similar mechanisms is compelling cement producers to invest in carbon capture. HeidelbergMaterials, Holcim, and several other major cement producers have announced carbon capture projects at specific plants, creating the beginning of what is expected to be a very large deployment wave.

Carbon Capture Materials Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global market. The United States has become the world's most commercially active market for new carbon capture projects following the Inflation Reduction Act, which created the most generous and accessible set of financial incentives for carbon capture investment of any country globally. The 45Q tax credit at USD 85 per tonne for geological storage and USD 180 per tonne for direct air capture makes a very large number of projects financially viable, and the resulting wave of new project announcements across natural gas processing, ethanol production, industrial manufacturing, and power generation is generating growing near-term demand for carbon capture materials. The U.S. Department of Energy's USD 3.5 billion investment in regional DAC hubs, the substantial investment in carbon capture technology companies including Svante, Carbon Clean, and Climeworks in their North American operations, and the large oil and gas sector that is the primary early customer for carbon capture at natural gas processing facilities collectively make the U.S. the world's leading carbon capture investment market. Canada contributes important additional North American market activity through its federal carbon pricing system that makes carbon capture economically attractive at industrial facilities, and through major projects including the Quest CCS project and several planned industrial carbon capture programs.

However, the Asia-Pacific carbon capture materials market is expected to grow at the fastest CAGR during the forecast period. China has the world's largest industrial carbon dioxide emissions and has made carbon neutrality by 2060 a national goal, creating very large long-term demand for carbon capture technology across its enormous coal power, cement, steel, and chemical manufacturing sectors. China's national carbon trading market, which covers the power generation sector and is expanding to include industrial sectors, is creating financial incentives for carbon capture investment that are growing progressively stronger as the carbon price increases over time. Japan has one of the world's longest-running commercial CCS projects at the Tomakomai facility in Hokkaido, and the Japanese government has committed very large funding to CCS deployment as part of its GX Green Transformation strategy. South Korea, India, and Australia all have active national carbon capture programs and growing industrial demand. Australia's Northern Territory and Queensland are developing large-scale CCS projects associated with natural gas processing, and the country's large liquefied natural gas export sector is a major potential source of carbon capture demand.

Europe is a technically advanced and policy-driven carbon capture materials market, anchored by Norway's world-leading CCS experience through the Sleipner and Snohvit offshore storage projects and the Northern Lights carbon transport and storage infrastructure that provides shared storage services to multiple industrial emitters across Europe. The Netherlands has one of the most active near-term industrial carbon capture development programs in the world, with multiple planned carbon capture projects at Rotterdam's industrial cluster including at the Shell Energy and Chemicals Park and several other facilities. The UK's East Coast Cluster and HyNet North West industrial decarbonization programs are developing some of the world's most ambitious near-term industrial carbon capture cluster projects. Sweden's BioEnergy Carbon Capture and Storage projects, which capture carbon dioxide from bioenergy plants to achieve negative emissions, and Germany's growing interest in carbon capture for its hard-to-abate industrial sectors are adding to European demand. Qatar and Saudi Arabia in the Middle East and Africa region represent important markets through the large carbon capture programs associated with natural gas processing and liquefied natural gas facilities.

The carbon capture materials sector includes large chemical companies that supply established solvent products, specialized carbon capture technology companies that develop proprietary materials as part of their integrated system offerings, industrial gas companies with carbon management capabilities, and major oil and gas companies that are both significant customers for carbon capture technology and developers of proprietary capture materials for their own operations. Competition is based on the cost and performance of capture materials per tonne of carbon dioxide captured, material durability and degradation resistance, energy requirements for regeneration, and the strength of the integrated system offering that surrounds the core materials product.

BASF is a leading supplier of amine-based carbon capture solvents through its OASE product line, which is used in natural gas processing and industrial carbon capture applications globally and represents one of the largest commercially deployed carbon capture material brands in the world. Climeworks is the leading commercial DAC operator and developer, operating large facilities in Iceland and planning significant capacity expansion that creates direct demand for the solid sorbent capture materials used in its systems. Carbon Clean Solutions has developed proprietary solvent formulations that it claims can reduce capital costs for carbon capture systems significantly, and has deployed systems at cement and steel plants. Svante has developed a structured solid sorbent carbon capture system specifically targeting industrial applications including cement and aluminum, and has raised significant funding from industrial partners. Linde and Air Liquide bring their industrial gas expertise and large-scale process capabilities to carbon capture materials and system integration.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' material portfolios, project track records, customer relationships, geographic presence, and recent strategic developments. Some of the key players operating in the global carbon capture materials market include BASF SE (Germany), Mitsubishi Heavy Industries Ltd. (Japan), Carbon Clean Solutions Ltd. (UK), Climeworks AG (Switzerland), Svante Inc. (Canada), Linde plc (UK/Ireland), Air Liquide S.A. (France), Aker Carbon Capture ASA (Norway), Fluor Corporation (U.S.), Shell plc (UK/Netherlands), ExxonMobil Corporation (U.S.), Honeywell International Inc. (U.S.), Siemens Energy AG (Germany), Toshiba Corporation (Japan), and Schlumberger Limited (U.S.), among others.

The global carbon capture materials market is expected to reach USD 9.6 billion by 2036 from an estimated USD 2.8 billion in 2026, at a CAGR of 13.1% during the forecast period 2026-2036.

In 2026, the solvent-based materials segment is expected to hold the largest share of the global market, reflecting amine-based liquid solvents being the most commercially deployed and operationally proven carbon capture material in the majority of currently operating large-scale carbon capture facilities globally.

The solid sorbents segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by active development of metal-organic frameworks and advanced polymer sorbents that offer the potential to reduce carbon capture energy requirements and operating costs significantly compared with current amine solvent systems.

In 2026, the power generation segment is expected to hold the largest share of the global market, driven by power generation being the largest single source of industrial carbon dioxide emissions and the most commercially advanced application of large-scale post-combustion carbon capture.

The direct air capture segment is projected to register the highest CAGR during the forecast period, driven by very large government funding commitments to DAC hub projects in the U.S. and Europe, growing corporate demand for verified atmospheric carbon removal credits, and the rapid commercial development of DAC facilities by Climeworks and several other companies.

The market is primarily driven by the accelerating global commitment to net-zero emissions creating regulatory and financial pressure on industrial sectors to adopt carbon capture as a necessary decarbonization tool, and by the transformative impact of the U.S. Inflation Reduction Act's carbon capture tax credits, which have made a very large number of previously uneconomical carbon capture projects financially viable and generated a wave of new project activity that is creating growing demand for carbon capture materials.

Key players are BASF SE (Germany), Mitsubishi Heavy Industries Ltd. (Japan), Carbon Clean Solutions Ltd. (UK), Climeworks AG (Switzerland), Svante Inc. (Canada), Linde plc (UK/Ireland), Air Liquide S.A. (France), Aker Carbon Capture ASA (Norway), Fluor Corporation (U.S.), Shell plc (UK/Netherlands), ExxonMobil Corporation (U.S.), Honeywell International Inc. (U.S.), Siemens Energy AG (Germany), Toshiba Corporation (Japan), and Schlumberger Limited (U.S.), among others.

Asia-Pacific is expected to register the highest growth rate in the global carbon capture materials market during the forecast period 2026-2036, driven by China's very large industrial emission base and its carbon neutrality by 2060 commitment, Japan's GX strategy committing large government funding to CCS deployment, and Australia's growing CCS project pipeline associated with its large natural gas export sector.

Published Date: May-2026

Published Date: May-2026

Published Date: Feb-2025

Published Date: Sep-2024

Published Date: May-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates