Resources

About Us

Specialty Minerals Market Size, Share & Trends Analysis by Mineral Type, Function, Application, End-Use Industry, Grade, and Processing Type- Global Opportunity Analysis & Industry Forecast (2026-2036)

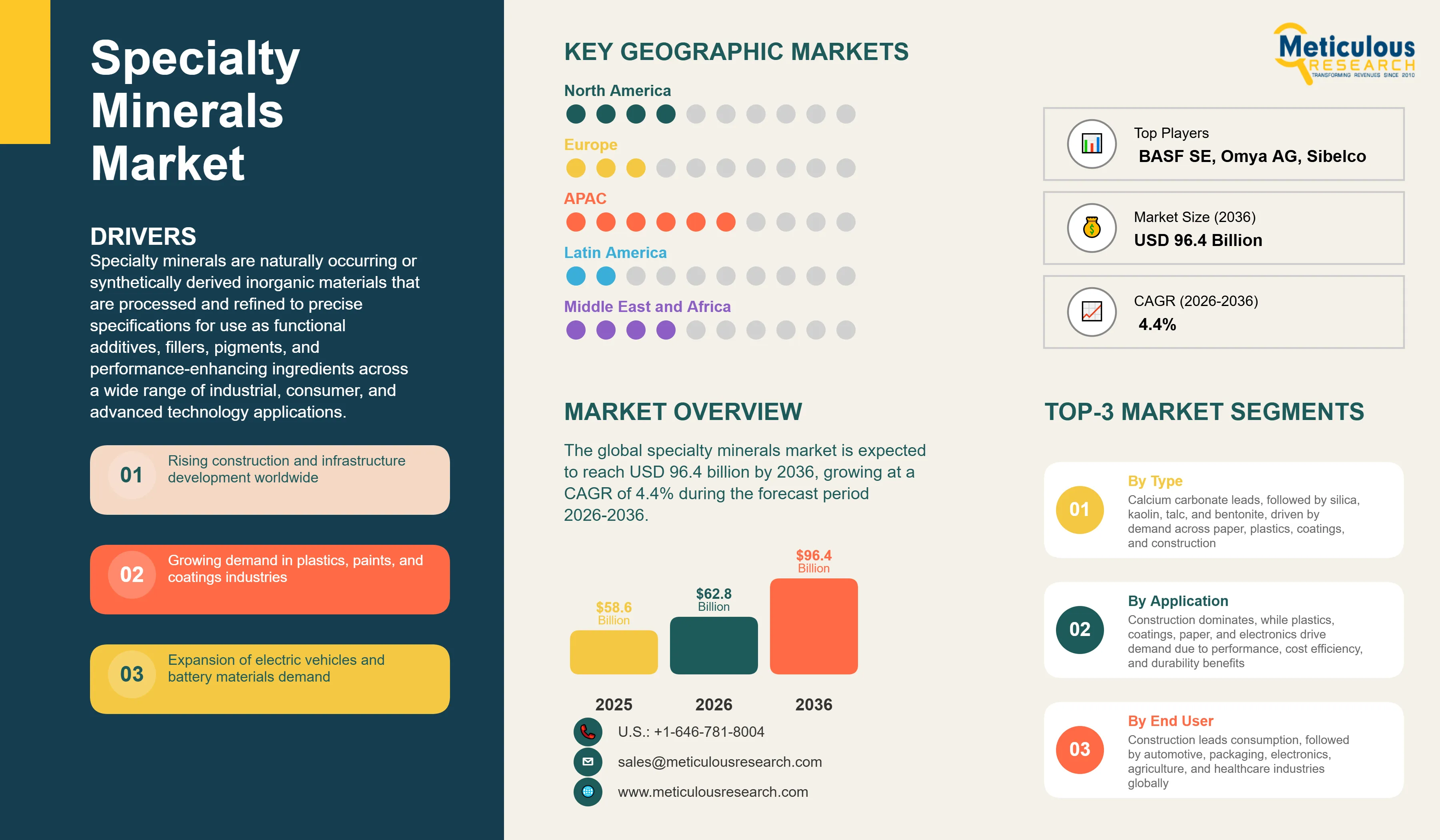

Report ID: MRCHM - 1041951 Pages: 325 May-2026 Formats*: PDF Category: Chemicals and Materials Delivery: 24 to 72 Hours Download Free Sample ReportThe global specialty minerals market was valued at USD 58.6 billion in 2025. This market is expected to reach USD 96.4 billion by 2036 from an estimated USD 62.8 billion in 2026, growing at a CAGR of 4.4% during the forecast period 2026-2036. According to the U.S. Geological Survey's Mineral Commodity Summaries 2024, the total value of nonfuel mineral production in the United States alone exceeded USD 105 billion in 2023, with industrial minerals including calcium carbonate, kaolin, talc, silica, and bentonite representing a significant share of this total, underscoring the commercial scale and industrial importance of the specialty minerals sector globally.

Click here to: Get Free Sample Pages of this Report

Specialty minerals are naturally occurring or synthetically derived inorganic materials that are processed and refined to precise specifications for use as functional additives, fillers, pigments, and performance-enhancing ingredients across a wide range of industrial, consumer, and advanced technology applications. Unlike commodity minerals extracted purely for their bulk material content, specialty minerals are valued for specific physical and chemical properties including whiteness and brightness, particle size distribution, oil absorption capacity, surface area, thermal stability, and chemical reactivity. Calcium carbonate added to paper improves brightness and print quality while reducing the amount of wood fiber required. Talc incorporated into polypropylene plastic improves stiffness, reduces warpage, and allows thinner wall sections. Precipitated silica in tire rubber reduces rolling resistance and improves wet grip, directly contributing to fuel efficiency improvements in modern passenger vehicles.

The market is growing steadily because the industrial economy continues to expand globally, and specialty minerals are integrated at the materials science level into products across construction, automotive, packaging, personal care, agriculture, and electronics. According to the United Nations Environment Programme’s Global Resources Outlook 2024, global material use is projected to increase by about 60% from 2020 levels to around 160 billion tonnes by 2060, with industrial minerals representing a significant and growing component of this total. The construction sector is the single largest consumer of specialty minerals globally, and according Oxford Economics’ Global Construction Futures 2024, the global construction market is expected to grow by about 42% from USD 9.7 trillion in 2022 to approximately USD 13.9 trillion by 2037, sustaining long‑term demand for calcium carbonate, silica, kaolin, and other construction‑critical minerals.

Two growth opportunities stand out. The electric vehicle battery supply chain is creating growing demand for high-purity specialty minerals including battery-grade silica as a silicon anode enabler, precipitated silica for battery separator coatings, and specialty bentonite for lithium extraction and battery electrolyte applications. According to the IEA's Global EV Outlook 2024, global EV sales reached 17-18 million in 2024 and continue to grow rapidly, and the battery materials supply chain requires specialty mineral inputs at multiple processing steps. In addition, the growing sophistication of engineered minerals, where natural minerals are chemically surface-treated and particle-size-engineered to provide performance characteristics impossible in natural form, is creating higher-value product categories that improve margins for specialty mineral producers and expand the technical capabilities available to their customers.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 96.4 Billion |

|

Market Size in 2026 |

USD 62.8 Billion |

|

Market Size in 2025 |

USD 58.6 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 4.4% |

|

Dominating Mineral Type |

Calcium Carbonate |

|

Fastest Growing Mineral Type |

Silica (Precipitated) |

|

Dominating Function |

Fillers |

|

Fastest Growing Function |

Reinforcing Agents |

|

Dominating Application |

Construction Materials |

|

Fastest Growing Application |

Electronics and Advanced Materials |

|

Dominating End-Use Industry |

Construction |

|

Fastest Growing End-Use Industry |

Electronics |

|

Dominating Grade |

Industrial Grade |

|

Fastest Growing Grade |

High-Purity Grade |

|

Dominating Processing Type |

Natural Minerals |

|

Fastest Growing Processing Type |

Processed/Engineered Minerals |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

Middle East & Africa |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Imerys and Minerals Technologies Leading Innovation in Engineered Mineral Products

The specialty minerals industry has been undergoing a gradual but commercially significant transition from natural mineral supply toward engineered and surface-treated mineral products that deliver performance characteristics tailored to specific customer applications. Imerys, the world's largest specialty minerals company has built its business model around this value-added approach, offering surface-treated kaolin for wire and cable insulation, functionalized calcium carbonate for polymer applications, and engineered talc grades specifically designed for automotive polypropylene composites. Minerals Technologies Inc. has developed proprietary Satellite PCC technology that installs precipitated calcium carbonate production units directly at paper mills, providing just-in-time supply of customized PCC grades that improve paper quality and reduce mill costs simultaneously.

This move toward engineered products reflects a broader industry trend of competing on performance and technical service rather than on price for commodity mineral supply. Surface treatment of mineral particles with coupling agents, stearic acid, or silane chemistry allows mineral fillers to bond chemically with polymer matrices, improving the mechanical properties of filled plastics well beyond what is achievable with untreated minerals. The global market for surface-treated specialty mineral fillers is growing faster than the underlying mineral market, and the technical service capabilities required to help customers optimize mineral performance in their formulations are becoming a key competitive differentiator for leading specialty mineral producers.

Precipitated Silica Benefiting from Tire Industry Fuel Efficiency Requirements

Precipitated silica has experienced strong demand growth driven by the tire industry's transition away from carbon black toward silica-silane technology in tire tread compounds, which delivers significant improvements in wet braking performance and rolling resistance that contribute directly to fuel efficiency and electric vehicle range. According to the European Tyre and Rubber Manufacturers Association's 2024 data, European Union regulations requiring tire labeling for wet grip and fuel efficiency have been a major driver of silica-filled tire adoption across the continent, and similar labeling requirements are being adopted in other markets including Japan, South Korea, and China. Each silica-filled tire contains approximately 10 to 15 kilograms of precipitated silica versus near zero in carbon black-filled tires, representing a large incremental demand per vehicle for every tire generation that converts to silica technology.

Evonik Industries, the world's largest precipitated silica producer through its ULTRASIL product range, reported that its specialty silica business has been a consistent growth driver, benefiting from both the tire silica transition and growing demand in food and pharmaceutical applications. Solvay and PPG Industries are also significant precipitated silica producers with strong automotive and industrial customer relationships. The growing penetration of electric vehicles, which require tires optimized for low rolling resistance to maximize battery range, is expected to further accelerate the silica-filled tire adoption rate globally, sustaining above-average demand growth for precipitated silica through the forecast period.

Energy Transition Creating New Specialty Mineral Demand Categories

The global energy transition is creating entirely new demand categories for specialty minerals beyond the traditional industrial applications that have historically defined this market. Lithium-ion battery production requires specialty minerals at multiple processing steps: high-purity synthetic graphite and silicon for anodes, lithium carbonate and lithium hydroxide derived from lithium-bearing minerals, nickel sulfate, manganese sulfate, and cobalt sulfate from processed metal sulfide minerals for cathode active materials, and specialty separators incorporating modified mineral coatings for safety and ionic conductivity. According to the IEA’s Global Critical Minerals Outlook 2024, demand for lithium is projected to increase by about 7 to 9 times by 2040 under the IEA’s Net Zero Emissions Scenario, and demand for nickel and cobalt for batteries is also projected to grow substantially.

Solar panel manufacturing requires high-purity silica for the production of polysilicon, the semiconductor material at the heart of photovoltaic cells, and the IEA reported in its Renewables 2024 report that the world installed a record 295 GW of solar capacity in 2023, generating growing demand for high-purity silica raw materials. Wind turbine generators use epoxy resins filled with mineral-based materials for blade manufacturing, and the steel and concrete used in wind turbine towers and foundations each consume mineral additives for performance improvement. These energy transition applications represent new and growing demand streams for specialty mineral producers that extend the market beyond its traditional industrial base and provide diversification into higher-growth end markets.

Growth in Construction and Infrastructure Development

Construction is the largest single end-use sector for specialty minerals globally, consuming calcium carbonate, kaolin, talc, silica, and bentonite across cement, concrete, insulation, coatings, adhesives, sealants, and flooring applications. According to Oxford Economics' Global Construction Outlook 2024, the global construction market is expected to grow 42% to reach around USD 14 trillion annually by 2037, with the strongest growth in emerging markets across Asia, Africa, and the Middle East. India's government infrastructure programs including the National Infrastructure Pipeline, which targets INR 111 lakh crore (approximately USD 1.3 trillion) of infrastructure investment through 2025, and Saudi Arabia's Vision 2030 mega-project construction programs are generating very large incremental demand for construction minerals. Each tonne of cement produced incorporates calcium carbonate as its primary raw material, and according to the Global Cement and Concrete Association’s 2024‑linked data, global cement production exceeded 4.1 billion tonnes in 2023, with Asia representing approximately three‑quarters (70–75%) of this total, providing a useful scale reference for the volumes of specialty minerals embedded in global construction.

Rising Use in Plastics, Paints, and Coatings

The plastics, paints, and coatings industries are major consumers of specialty mineral fillers and extenders that improve product performance while reducing material costs. In plastics, calcium carbonate filler in polypropylene compounds improves stiffness, dimensional stability, and surface finish while reducing polymer content, allowing manufacturers to reduce their raw material costs in an application where polymer represents 60 to 80% of total formulation cost. According to the European Plastics Manufacturers Association's 2024 data, European plastic production exceeded 54 million tonnes in 2023, and the incorporation of mineral fillers at typical loading rates of 10 to 40% by weight implies very large mineral consumption volumes. In paints and coatings, titanium dioxide replacement by calcium carbonate and kaolin extenders is a long-running commercial trend driven by the very high cost of TiO2, and the growing global paints and coatings market, which the American Coatings Association estimated at over USD 250 billion in 2024, sustains strong demand for specialty mineral extenders across all major geographic markets.

Development of High-Purity and Engineered Minerals

The commercial opportunity for specialty mineral producers to move up the value chain from natural mineral supply toward engineered and high-purity mineral products is significant and growing. Natural kaolin with typical brightness of 80 to 85 ISO can be processed through calcination, chemical bleaching, and wet centrifugal classification to produce calcined kaolin with brightness above 95 ISO and precisely controlled particle size distributions for high-end coating applications that command significantly higher selling prices per tonne than run-of-mine kaolin. Precipitated calcium carbonate, produced through a controlled chemical reaction rather than by grinding natural limestone, can be manufactured with specific crystal morphologies, particle sizes, and surface chemistries that provide performance advantages in paper, plastics, and pharmaceutical applications that ground calcium carbonate cannot match. Imerys, Minerals Technologies, and Omya have all built significant revenue streams from engineered mineral products that deliver technically superior performance for demanding applications, and the continuing development of new surface chemistries, nano-scale mineral products, and mineral-polymer composite materials represents a growing commercial frontier for the specialty minerals industry.

Growth in Electric Vehicles and Battery Materials

The rapid growth of electric vehicle production is creating growing demand for specialty mineral inputs across the EV battery supply chain, representing a new and high-growth revenue opportunity for specialty mineral producers with the technical capability to supply battery-grade materials. Silicon anode technology, which is transitioning from research to commercial production as companies including Amprius Technologies and Sila Nanotechnologies scale up silicon-dominant anode materials, requires high-purity silica as a silicon source precursor. Battery separator films, which prevent internal short circuits in lithium-ion cells, are often coated with ceramic minerals including alumina and silica to improve thermal stability, and the growing EV battery production volumes are expanding demand for these mineral-coated separators. According to the IEA's Global EV Outlook 2025, global EV sales reached 17-18 million units in 2024, and BloombergNEF's Electric Vehicle Outlook 2024 projects that EVs will account for 75% of global passenger vehicle sales by 2040, implying very large long-term growth in battery mineral demand.

By Mineral Type: In 2026, Calcium Carbonate to Dominate

Based on mineral type, the global specialty minerals market is segmented into calcium carbonate (GCC and PCC), kaolin (China clay), talc, silica (fused and precipitated), bentonite, barite, feldspar, and other specialty minerals. In 2026, the calcium carbonate segment is expected to account for the largest share of the global specialty minerals market. Calcium carbonate is the single most widely used specialty mineral globally by volume, consumed across paper, plastics, paints, construction, food, pharmaceuticals, and agriculture in quantities that exceed all other specialty minerals combined.

However, the precipitated silica segment is projected to register the highest CAGR during the forecast period. Driven by the tire industry's accelerating transition to silica-filled tread compounds for improved fuel efficiency and wet performance, combined with growing demand in battery materials, food processing, and pharmaceutical applications, precipitated silica is one of the specialty mineral categories with the clearest and most commercially compelling demand growth trajectory. Evonik Industries' ULTRASIL precipitated silica has been consistently highlighted as a growth product in the company's specialty additives segment.

By Function: In 2026, Fillers to Hold the Largest Share

Based on function, the global specialty minerals market is segmented into fillers, extenders, reinforcing agents, coating and surface modifiers, adsorbents, and others. In 2026, the fillers segment is expected to account for the largest share of the global specialty minerals market. Mineral fillers used in plastics, paper, rubber, and coatings to increase volume, improve physical properties, and reduce costs represent the largest use category for specialty minerals by volume. The very large and broadly distributed consumption of calcium carbonate, kaolin, talc, and silica as fillers across multiple industrial sectors makes this the dominant function category in the market.

However, the reinforcing agents segment is projected to register the highest CAGR during the forecast period. Specialty minerals used as reinforcing agents in rubber and polymer composites, where they improve mechanical strength, modulus, and wear resistance rather than simply adding volume, command higher prices and are seeing growing demand from the automotive and industrial rubber sectors. Precipitated silica as a reinforcing agent in tire rubber is the most commercially significant example, but treated kaolin in wire and cable insulation compounds and specialty talc in polypropylene automotive components also represent important reinforcing agent applications with growing demand.

By Application: In 2026, Construction Materials to Hold the Largest Share

Based on application, the global specialty minerals market is segmented into construction materials, plastics and polymers, paints and coatings, paper and pulp, pharmaceuticals and healthcare, agriculture, electronics and advanced materials, and other applications. In 2026, the construction materials segment is expected to account for the largest share of the global specialty minerals market. Cement and concrete alone consume limestone, calcium carbonate, silica, and other mineral inputs in volumes that make construction the dominant application by far on a tonnage basis. With global cement production exceeding 4.1 billion tonnes in 2023 according to the Global Cement and Concrete Association, and construction accounting for a large share of specialty mineral consumption across additional categories including insulation, sealants, adhesives, and coatings, this is the defining end-use application for the specialty minerals industry.

However, the electronics and advanced materials segment is projected to register the highest CAGR during the forecast period. The semiconductor, EV battery, solar panel, and advanced electronic component manufacturing sectors are creating growing and technically demanding demand for ultra-high-purity specialty minerals that command premium pricing and are among the fastest-growing applications in the global specialty minerals market. The electronics industry's requirement for mineral inputs with impurity levels in parts per billion rather than parts per million requires processing capabilities that only a small number of specialty mineral producers can provide, creating a high-barrier and high-value niche market segment.

Specialty Minerals Market by Region: Asia-Pacific Leading by Share, Middle East and Africa by Growth

Based on geography, the global specialty minerals market is segmented into Asia-Pacific, North America, Europe, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global specialty minerals market. The region's dominance reflects China's position as both the world's largest consumer and largest producer of most specialty mineral categories. According to the U.S. Geological Survey's Mineral Commodity Summaries 2024, China accounts for approximately 70% of global kaolin production, over 65% of global talc production, and a dominant share of global calcium carbonate and barite production, making it the central node of global specialty mineral supply chains. China's enormous paper, plastics, paints, ceramics, and construction industries consume very large volumes of specialty minerals domestically. India is the world's largest producer of mica and an important producer of barite and other specialty minerals, with Ashapura Group being one of the world's largest barite producers. India's rapidly growing construction sector, plastics industry, and paints market are sustaining strong domestic specialty mineral demand growth. Japan and South Korea have advanced ceramics, electronics, and specialty materials industries that require high-purity specialty mineral inputs with technical specifications that command significant premium pricing over standard industrial grades.

However, the Middle East and Africa region is expected to grow at the fastest CAGR during the forecast period. The Middle East's extraordinary construction activity, anchored by Saudi Arabia's Vision 2030 mega-projects and the UAE's continued commercial and residential construction programs, is driving above-average growth in construction mineral demand including calcium carbonate, silica, and kaolin for cement, concrete, paints, and insulation. Saudi Arabia has announced over USD 1.5-2 trillion in construction project investment under Vision 2030, and this pipeline is generating structural specialty mineral demand growth well above global averages. Sub-Saharan Africa and North Africa are also experiencing growing industrial and construction sectors that are expanding specialty mineral consumption, and Turkey, with its large ceramics, tiles, and construction materials industries, is a significant and growing specialty mineral consumer with domestic production including feldspar, which Turkey produces in significant volumes according to USGS 2024 data, and industrial minerals.

North America is a large and technically advanced specialty minerals market, with the United States being both a significant producer through domestic deposits of kaolin in Georgia, calcium carbonate in the Midwest, and silica in multiple states, and a major consumer across its large paper, plastics, paints, and construction industries. Minerals Technologies Inc. and J.M. Huber Corporation are important U.S.-headquartered specialty mineral producers with significant domestic and international operations. Europe is characterized by high technical standards and a strong tradition of engineered mineral product development, with Imerys and Omya as the two largest European specialty mineral companies both having extensive European mining and processing operations alongside global commercial footprints. Latin America, particularly Brazil which has large deposits of kaolin in the Amazon region and calcium carbonate resources, is growing as both a producer and consumer of specialty minerals.

The specialty minerals market is served by large diversified mineral producers with multi-mineral portfolios and global operations, regional specialists with particular expertise in a specific mineral or geographic market, and a large number of smaller local producers serving domestic markets. Competition is based on deposit quality and reserve life, processing technology capabilities and product quality consistency, technical service capabilities for customer formulation optimization, geographic proximity to major consuming industries, and the breadth and technical sophistication of the engineered product portfolio.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' mineral portfolios, geographic presence, processing capabilities, and recent strategic developments. Some of the key players operating in the global specialty minerals market include Imerys S.A. (France), Omya AG (Switzerland), Minerals Technologies Inc. (U.S.), BASF SE (Germany), Sibelco Group (Belgium), Quarzwerke Group (Germany), LKAB Minerals AB (Sweden), Ashapura Group (India), SCR-Sibelco N.V. (Belgium), Huber Engineered Materials (U.S.), J.M. Huber Corporation (U.S.), Carmeuse Group (Belgium), Nordkalk Corporation (Finland), Golcha Group (India), and Thiele Kaolin Company (U.S.), among others.

The global specialty minerals market is expected to reach USD 96.4 billion by 2036 from an estimated USD 62.8 billion in 2026, at a CAGR of 4.4% during the forecast period 2026-2036.

In 2026, the calcium carbonate segment is expected to hold the largest share of the global specialty minerals market.

The precipitated silica segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the tire industry's accelerating transition to silica-filled tread compounds for fuel efficiency and wet braking performance, combined with growing battery material and pharmaceutical applications. According to the European Tyre and Rubber Manufacturers Association 2024 data, EU tire labeling requirements have been a key policy driver of silica-filled tire adoption across Europe.

According to the IEA’s Global Critical Minerals Outlook 2024, demand for lithium is projected to increase by about sevenfold by 2040 under the IEA’s Net Zero Emissions Scenario, and battery materials including nickel, cobalt, and manganese are also projected to grow substantially. The IEA’s Renewables 2024 report noted record solar PV deployment in 2023 of roughly 440–450 GW, with high purity silica serving as a key raw material for polysilicon production in crystalline silicon solar modules.

The market is primarily driven by the growth of the global construction sector, which Oxford Economics projects will reach around USD 14 trillion annually by 2037 representing 42% growth from current levels, making construction the sustained primary demand driver. Additionally, the energy transition is creating new high-value demand categories for high-purity specialty minerals in EV batteries and solar manufacturing, and the progressive shift toward engineered and surface-treated mineral products is improving average revenue per tonne for leading producers.

Key players are Imerys S.A. (France), Omya AG (Switzerland), Minerals Technologies Inc. (U.S.), BASF SE (Germany), Sibelco Group (Belgium), Quarzwerke Group (Germany), LKAB Minerals AB (Sweden), Ashapura Group (India), SCR-Sibelco N.V. (Belgium), Huber Engineered Materials (U.S.), J.M. Huber Corporation (U.S.), Carmeuse Group (Belgium), Nordkalk Corporation (Finland), Golcha Group (India), and Thiele Kaolin Company (U.S.), among others.

The Middle East and Africa region is expected to register the highest growth rate in the global specialty minerals market during the forecast period 2026-2036, driven primarily by Saudi Arabia's USD 1.5-2.0 trillion-plus Vision 2030 construction investment pipeline generating very large construction mineral demand, the UAE's continued commercial construction activity, and the growing industrial sectors across North Africa and Sub-Saharan Africa.

Published Date: Feb-2026

Published Date: Feb-2026

Published Date: May-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates