Resources

About Us

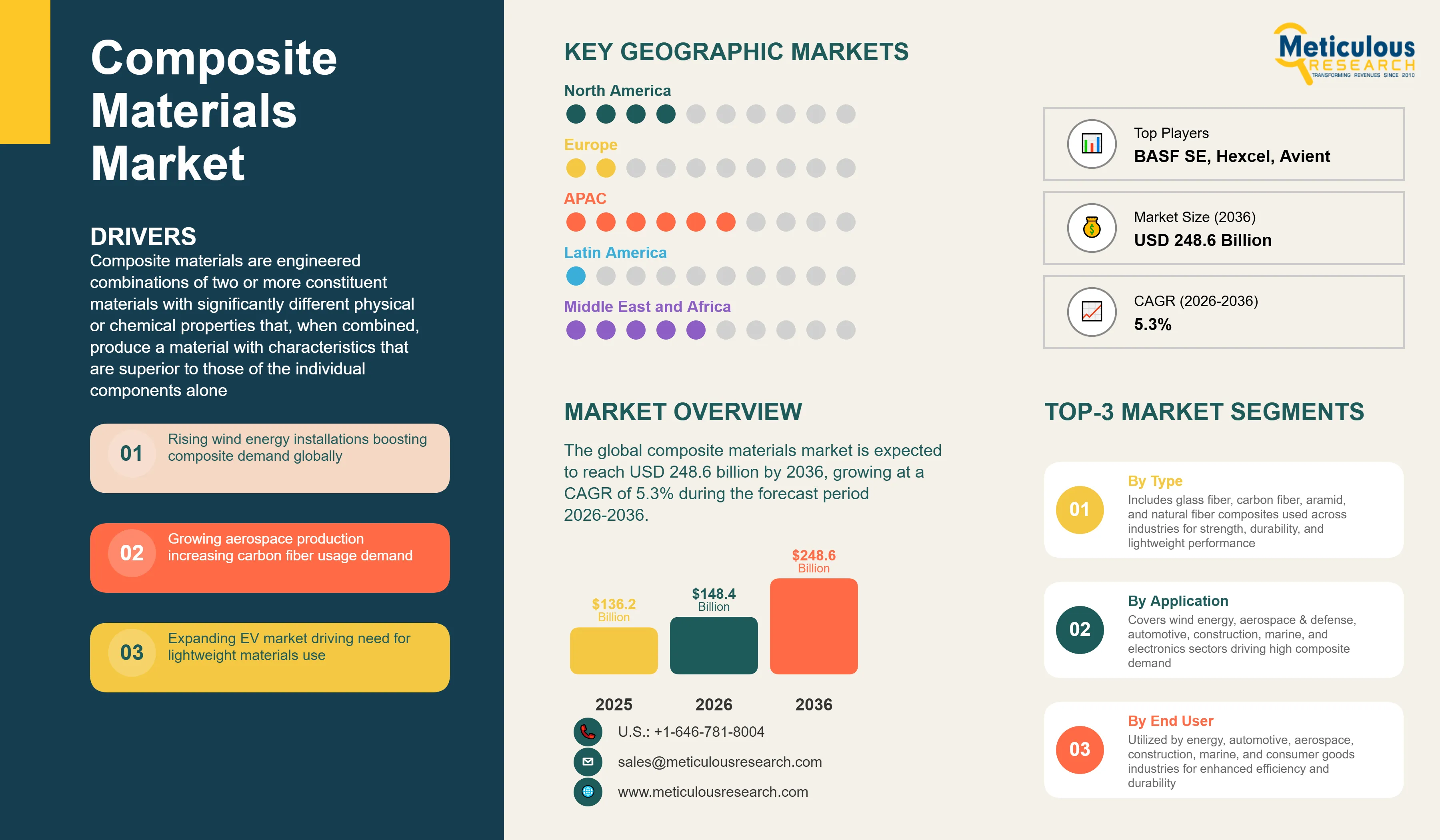

Composite Materials Market Size, Share & Trends Analysis by Fiber Type, Resin Type, Manufacturing Process, Application, and End-Use Industry - Global Opportunity Analysis & Industry Forecast (2026-2036)

Report ID: MRCHM - 1041962 Pages: 310 May-2026 Formats*: PDF Category: Chemicals and Materials Delivery: 24 to 72 Hours Download Free Sample ReportThe global composite materials market was valued at USD 136.2 billion in 2025. This market is expected to reach USD 248.6 billion by 2036 from an estimated USD 148.4 billion in 2026, growing at a CAGR of 5.3% during the forecast period 2026-2036. The IEA’s Renewables 2025 report says global renewable electricity capacity additions in 2024 grew 22% to nearly 717 GW, the majority of which was wind and solar, and wind turbine blades are among the most composite-material-intensive manufactured products in the world, with each modern offshore turbine blade consuming several tonnes of glass and carbon fiber reinforced composite material. This renewable energy build-out is one of the most reliable and growing demand drivers for composite materials globally.

Click here to: Get Free Sample Pages of this Report

Composite materials are engineered combinations of two or more constituent materials with significantly different physical or chemical properties that, when combined, produce a material with characteristics that are superior to those of the individual components alone. In a fiber-reinforced polymer composite, which is the dominant commercial composite category, high-strength fibers of glass, carbon, or aramid are embedded in a polymer matrix resin that binds the fibers, protects them from environmental damage, and transfers loads between them. The result is a material that is significantly lighter than steel or aluminum while delivering comparable or superior structural performance, excellent fatigue resistance, design flexibility enabling complex curved shapes impossible in sheet metal, and inherent corrosion resistance that eliminates the painting and maintenance requirements of metal structures.

The market is growing because the industries that benefit most from lightweight, high-strength materials are expanding simultaneously and in ways that specifically increase composite demand. The IEA’s Renewables 2025 report says global renewable electricity capacity additions in 2024 grew 22% to nearly 717 GW, and each new wind turbine blade requires glass fiber reinforced composite in very large quantities, with a single set of blades for an 8 to 12 megawatt offshore turbine consuming 40 to 60 tonnes of composite material. Airbus and Boeing's combined commercial aircraft delivery targets for 2025, as disclosed in their 2025 investor communications, indicate continuing strong aircraft production that directly drives CFRP demand, as modern widebody aircraft including the Boeing 787 and Airbus A350 contain over 50% composite materials by weight. According to the IEA's Global EV Outlook 2025, global electric vehicle sales reached approximately 17-18 million units in 2024, and composite body panels and structural components in EVs are growing as automakers pursue every kilogram of weight reduction to extend battery range.

Two growth opportunities are particularly compelling for the forecast period. The development of thermoplastic composite materials, which can be recycled and reprocessed unlike conventional thermoset composites that are permanently cross-linked and difficult to recycle, is addressing the composites industry's most significant sustainability challenge and is gaining commercial traction in automotive, aerospace, and consumer goods applications. Simultaneously, the enormous offshore wind expansion programs announced by governments in Europe, the U.S., and Asia are creating a multi-decade demand pipeline for very large composite turbine blades, with each new generation of larger offshore turbines requiring more composite material per unit than its predecessor.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 248.6 Billion |

|

Market Size in 2026 |

USD 148.4 Billion |

|

Market Size in 2025 |

USD 136.2 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 5.3% |

|

Dominating Fiber Type |

Glass Fiber Composites (GFRP) |

|

Fastest Growing Fiber Type |

Carbon Fiber Composites (CFRP) |

|

Dominating Resin Type |

Thermoset Resins (Epoxy) |

|

Fastest Growing Resin Type |

Thermoplastic Resins (PEEK) |

|

Dominating Manufacturing Process |

Hand Lay-Up |

|

Fastest Growing Manufacturing Process |

Automated Fiber Placement (AFP) |

|

Dominating Application |

Wind Energy (Turbine Blades) |

|

Fastest Growing Application |

Aerospace and Defense |

|

Dominating End-Use Industry |

Energy (Wind) |

|

Fastest Growing End-Use Industry |

Automotive & Transportation |

|

Dominating Form |

Continuous Fiber Composites |

|

Fastest Growing Form |

Discontinuous Fiber Composites |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

Middle East & Africa |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Offshore Wind Expansion Driving Record Composite Demand for Turbine Blades

The global offshore wind industry is scaling up at an extraordinary pace and is creating one of the largest and most sustained demand drivers for composite materials in the market's history. Offshore turbine blades are among the most composite-intensive manufactured products globally, with each blade for a modern 12 to 15 megawatt offshore turbine measuring 100 meters or more in length and requiring approximately 20 tonnes or more of glass and carbon fiber reinforced composite per blade. With three blades per turbine, a single large offshore wind installation consumes over 60 tonnes of composite material just for the rotor assembly.

According to the Global Wind Energy Council's 2025 Global Wind Report, global offshore wind installations reached approximately 8 GW in 2024 and are projected to grow substantially through 2030 as European, U.S., and Asian offshore programs progress from planning to construction. The EU's REPowerEU plan targets 300 GW of offshore wind by 2050, and the UK's offshore wind target, reaffirmed in 2025 government communications, is 50 GW by 2030. Each gigawatt of offshore wind capacity requires roughly 500 to 600 tonnes of composite blade material at typical turbine sizes, meaning that the projected offshore wind additions through 2030 represent a very large and predictable composite material demand pipeline that directly benefits glass fiber and carbon fiber manufacturers. Vestas, Siemens Gamesa, and GE Vernova, the three leading wind turbine manufacturers, are all expanding their blade manufacturing capacity in response to this demand.

Aerospace CFRP Demand Growing as Aircraft Production Ramps Back Up

Commercial aviation's post-pandemic recovery has created a strong and sustained upswing in aircraft production that is directly expanding carbon fiber reinforced composite demand, as modern aircraft are among the most CFRP-intensive products manufactured at commercial scale. The Boeing 787 Dreamliner contains approximately 50% composite materials by weight including very large CFRP fuselage sections, and the Airbus A350 contains approximately 53% composites by weight according to Airbus's published specifications. Both aircraft programs are ramping up production rates in 2025 following pandemic-driven cuts and supply chain recoveries.

According to Airbus’s 2026 guidance, the company aims to deliver 870 commercial aircraft in 2026, up from 790 deliveries in 2025, with ongoing investments in widebody production capacity that will consume growing volumes of CFRP. Boeing's production recovery trajectory for its 737 MAX and 787 programs, as disclosed in its 2025 investor communications, indicates substantial composite material consumption increasing through the forecast period. Toray Industries and Hexcel Corporation, the world's two largest aerospace CFRP suppliers, both disclosed strong aerospace revenue growth in their 2025 financial communications, reflecting the production ramp-up translating into material procurement. Toray, which is the world's largest carbon fiber manufacturer, reports that aerospace applications represent one of its fastest-recovering demand segments following the pandemic-era decline, with long-term supply agreements with Airbus and Boeing providing volume visibility through the decade.

Thermoplastic Composites and Recycling Addressing the Sustainability Challenge

The composites industry faces a growing sustainability challenge: thermoset composite materials, which represent the majority of current composite production, are permanently cross-linked during curing and cannot be melted and reprocessed, making them difficult and expensive to recycle. The tonnes of composite waste generated during turbine blade decommissioning, aircraft end-of-life, and manufacturing process waste are creating growing regulatory and reputational pressure on the industry to develop circular composite solutions. The EU's End-of-Life Vehicles Regulation and automotive sector sustainability commitments are reinforcing the need for recyclable composite solutions in transportation.

Thermoplastic composites, which use a thermoplastic rather than thermoset resin as the matrix, can be remelted and reprocessed at end of life, fundamentally addressing the recycling limitation of conventional composites. PEEK-based thermoplastic composites from Solvay and Victrex are growing in aerospace applications. Continuous fiber reinforced thermoplastic sheets from companies including Toray and Teijin are being adopted in automotive structural applications where the combination of high specific strength and recyclability meets both performance and sustainability requirements. According to Airbus's 2025 sustainability report, the company has set targets for thermoplastic composite adoption in next-generation aircraft structures specifically to address the end-of-life recyclability requirement, indicating that the aerospace industry's sustainability agenda will be a major driver of thermoplastic composite adoption through the forecast period.

Rising Use in Renewable Energy (Wind Energy)

Wind energy is the largest single application for composite materials globally by volume, consuming glass fiber reinforced composite in very large quantities for turbine blade manufacturing and representing a demand driver that grows directly with wind capacity additions. According to the IEA's Renewables 2025 report, global wind capacity additions reached approximately 117 GW in 2024, and the IEA projects that rate of global wind capacity additions is set to double between 2024 and 2030 under its Net Zero pathway. Each gigawatt of wind capacity, at typical onshore turbine sizes, requires approximately 200 to 350 tonnes of composite blade material, and offshore turbines at larger sizes require proportionally more. The transition to larger offshore turbines, where blade lengths exceeding 100 meters and per-turbine composite material consumption exceeding 60 tonnes make each installation a very large composite procurement event, is increasing the composite intensity per megawatt of wind capacity over time.

Growth in Aerospace and Automotive Industries

The aerospace industry's post-pandemic production recovery is driving renewed growth in carbon fiber composite demand from its most technically demanding application. Airbus's 2026 target of approximately 870 aircraft deliveries, and Boeing's production ramp-up programs for the 737 MAX and 787, are translating into growing CFRP procurement from the world's two largest commercial aircraft manufacturers. According to Hexcel Corporation's 2025 first-quarter financial results, the company's aerospace revenue was growing above its overall average, confirming that aircraft production growth is being reflected in composite material supplier revenues. In automotive, the IEA's Global EV Outlook 2025 documenting approximately 17-18 million EV sales in 2024 is driving growing adoption of composite body panels, battery enclosures, and structural components in electric vehicles where every kilogram of weight reduction directly extends range, with CFRP and glass fiber composite usage in EVs growing faster than in conventional ICE vehicles.

Expansion in Electric Vehicles (EVs)

Electric vehicles represent a growing and commercially significant application for composite materials that is adding incremental demand beyond the established automotive composite base. The weight reduction imperative in EVs is more acute than in ICE vehicles because battery packs add 300 to 600 kilograms to vehicle weight and each kilogram of structure replaced by composite saves approximately two kilograms from the battery required to maintain the same range. Carbon fiber reinforced polymer structural components, composite battery enclosure trays, and glass fiber reinforced body panels are all seeing growing EV application. BMW's use of CFRP passenger cell structure in its i-series vehicles and the growing adoption of composite battery trays by EV manufacturers are commercial reference points for this trend. According to BloombergNEF’s 2025 Electric Vehicle Outlook, global EV sales are expected to keep growing rapidly, with EVs projected to reach 56% of global passenger vehicle sales by 2035, implying continuing rapid growth in EV-specific composite material demand.

Development of Bio-Based and Recyclable Composites

The development of bio-based fibers including flax, hemp, kenaf, and jute as partial or full replacements for glass fiber in lower-performance composite applications is gaining commercial traction as the composites industry's customers demand materials with lower carbon footprints and end-of-life recyclability. Natural fiber composites deliver adequate mechanical properties for interior automotive components, consumer goods, and construction applications while offering better environmental credentials than glass or carbon fiber on a lifecycle basis. According to a 2025 industry report by the European Composites Industry Association, the natural fiber composite market is growing at above-average rates driven by automotive Tier-1 suppliers incorporating flax and hemp composites into door panels, trunk liners, and seat structures. Recycled carbon fiber, produced from end-of-life aerospace components and manufacturing waste, is also developing as a commercial product category, with companies including ELG Carbon Fibre and SGL Carbon developing processes to recover and reprocess carbon fiber at lower cost than virgin fiber production.

By Fiber Type: In 2026, Glass Fiber Composites (GFRP) to Dominate

Based on fiber type, the global composite materials market is segmented into glass fiber composites (GFRP), carbon fiber composites (CFRP), aramid fiber composites (AFRP), natural fiber composites, and other fiber types. In 2026, the glass fiber composites segment is expected to account for the largest share of the global composite materials market. Glass fiber is the most widely used reinforcement fiber globally by volume, consumed in wind turbine blades, boats and marine vessels, construction products, automotive parts, pipes and tanks, and consumer goods in quantities that far exceed carbon and aramid fiber combined. The combination of good mechanical properties, corrosion resistance, and relatively low cost makes GFRP the standard composite choice for the very large wind energy and marine application markets. Owens Corning and Jushi Group, the world's two largest glass fiber manufacturers, both reported strong revenues in their 2025 financial results, reflecting the sustained large-scale demand from wind energy and construction applications.

However, the carbon fiber composites segment is projected to register the highest CAGR during the forecast period. The combination of aerospace production recovery, growing EV structural application, and the transition of some wind turbine blade manufacturers from glass to carbon fiber in the spar caps of very large offshore blades is driving CFRP demand growth above the overall composite market rate. Toray's disclosure in its 2025 annual report of strong growth in aerospace CFRP demand and growing automotive carbon fiber composite adoption confirms this above-average growth trajectory.

By Resin Type: In 2026, Thermoset Resins (Epoxy) to Hold the Largest Share

Based on resin type, the global composite materials market is segmented into thermoset resins (polyester, epoxy, and vinyl ester) and thermoplastic resins (polypropylene, polyamide, and PEEK). In 2026, the thermoset resins segment, particularly epoxy, is expected to account for the largest share of the global composite materials market. Epoxy resins provide the best combination of mechanical performance, fiber-matrix adhesion, and chemical resistance of any thermoset matrix system, making them the standard resin for aerospace, high-performance automotive, and wind turbine blade applications where maximum structural performance is required. The very large installed base of epoxy composite processing equipment and the qualification of epoxy-based material systems across aerospace and defense programs means epoxy will remain the dominant thermoset for high-performance applications through the forecast period.

However, the thermoplastic resins segment, particularly PEEK and advanced engineering thermoplastics, is projected to register the highest CAGR during the forecast period. The sustainability pressure to develop recyclable composite materials, combined with the growing qualification of thermoplastic composite processes in aerospace and automotive production, is driving above-average growth in thermoplastic composite resin demand. According to Solvay's 2025 first-quarter results commentary, its thermoplastic composite materials for aerospace applications were seeing strong growth driven by both new aircraft program qualifications and the industry's sustainability agenda.

By Application: In 2026, Wind Energy to Hold the Largest Share

Based on application, the global composite materials market is segmented into aerospace and defense, automotive and transportation, wind energy (turbine blades), construction and infrastructure, marine applications, electrical and electronics, and other applications. In 2026, the wind energy application segment is expected to account for the largest share of the global composite materials market. Wind turbine blades are the highest single-application consumer of glass fiber composite material globally by weight, and the very large annual volumes of new blade manufacturing driven by the global wind energy expansion program make wind energy the dominant composite application. The transition to larger offshore turbines requiring longer blades further increases per-turbine composite material consumption. According to the IEA's Renewables 2024 report and the Global Wind Energy Council's 2025 data, global wind capacity additions remain at record levels, sustaining the wind energy segment's dominant position in composite material demand.

However, the aerospace and defense segment is projected to register the highest CAGR during the forecast period. The post-pandemic aerospace production recovery, the production ramp-up of composite-intensive widebody aircraft, and the growing demand for CFRP in defense applications including unmanned aerial vehicles and advanced military aircraft structures are driving aerospace composite demand growth at above-average rates. Hexcel's 2025 financial results and Toray's 2025 annual report disclosures both confirm aerospace as a fast-recovering and growing composite application.

Composite Materials Market by Region: Asia-Pacific Leading by Share, Middle East and Africa by Growth

Based on geography, the global composite materials market is segmented into Asia-Pacific, North America, Europe, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global composite materials market. The region's dominance reflects China's position as both the world's largest wind turbine manufacturer and blade producer and the home of the world's largest glass fiber manufacturing companies. Jushi Group, headquartered in China, is the world's largest single glass fiber producer, and China hosts multiple other large glass fiber manufacturers including CPIC (China Jushi) and Taishan Fiberglass that collectively account for a very large share of global glass fiber supply. China's record wind energy installations, with the National Energy Administration of China reporting approximately 80 GW of new wind capacity added in 2024, generate very large domestic composite blade material demand. Japan is home to Toray Industries, the world's largest carbon fiber manufacturer, and Teijin, the second-largest, making Japan the center of global carbon fiber composite supply for aerospace and high-performance applications. South Korea's and Taiwan's advanced electronics and industrial sectors are also meaningful composite consumers. India's growing wind energy program and rapidly expanding automotive and infrastructure sectors are creating growing composite material demand from a large and expanding industrial base.

However, the Middle East and Africa region is expected to grow at the fastest CAGR during the forecast period. The Middle East's large-scale renewable energy programs, including Saudi Arabia's National Renewable Energy Program targeting 130 GW of renewable capacity by 2030 according to the Saudi Arabian government's 2025 communications and the UAE's renewable energy targets, are creating growing wind and solar composite material demand from a very low current base. Saudi Arabia's Vision 2030 industrial diversification programs are investing in domestic manufacturing capacity across multiple sectors that will consume composite materials, and the kingdom's NEOM mega-project and related construction programs are generating demand for construction composite applications. Sub-Saharan African infrastructure development and growing industrial investment are adding to the regional demand trajectory. The combination of large renewable energy investment, infrastructure construction, and industrial development from a currently low composite penetration base creates the conditions for the highest percentage growth rate of any region.

North America is a large and technologically sophisticated composite materials market, anchored by the United States which has the world's largest commercial aerospace industry, very large wind energy installations, and an advanced automotive composite development ecosystem. The U.S. defense sector is also a major consumer of advanced carbon fiber composites for military aircraft and equipment. Europe is characterized by very strong composite technology capabilities, world-leading wind energy adoption particularly in Germany, the UK, Denmark, and the Netherlands, and a sophisticated aerospace supply chain anchored by Airbus and its European suppliers. Norway, listed in the European geography section of this report, is home to Hexagon Composites ASA, a leading supplier of composite pressure vessels and gas storage systems. Latin America's Brazil and Chile are growing composite consumers through their respective wind energy and infrastructure programs.

The composite materials market is served by integrated fiber and composite manufacturers that produce both the reinforcement fiber and finished composite materials or prepregs, specialty resin and matrix suppliers, component fabricators serving specific end-use applications, and a growing number of companies developing sustainable and recycled composite technologies. Competition is based on fiber tensile strength and modulus specifications, resin system performance and compatibility, manufacturing process capability and scalability, qualification and certification credentials in target applications, and sustainability credentials including recyclability and carbon footprint.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, application expertise, manufacturing footprints, and recent strategic developments. Some of the key players operating in the global composite materials market include Toray Industries Inc. (Japan), Hexcel Corporation (U.S.), Owens Corning (U.S.), Teijin Limited (Japan), SGL Carbon SE (Germany), Mitsubishi Chemical Group Corporation (Japan), Solvay S.A. (Belgium), BASF SE (Germany), Huntsman Corporation (U.S.), Jushi Group Co. Ltd. (China), Gurit Holding AG (Switzerland), Hexagon Composites ASA (Norway), Avient Corporation (U.S.), Nippon Electric Glass Co. Ltd. (Japan), and Chomarat Group (France), among others.

The global composite materials market is expected to reach USD 248.6 billion by 2036 from an estimated USD 148.4 billion in 2026, at a CAGR of 5.3% during the forecast period 2026-2036.

In 2026, the glass fiber composites segment is expected to hold the largest share of the global composite materials market, driven by GFRP being the most widely used composite by volume across wind turbine blades, marine, construction, and industrial applications at cost-competitive pricing relative to carbon and aramid fiber alternatives.

The carbon fiber composites segment is projected to register the highest CAGR during the forecast period, driven by aerospace production recovery requiring CFRP for new widebody aircraft programs, growing EV structural application where weight reduction directly extends range, and the adoption of carbon fiber in the spar caps of very large offshore wind turbine blades.

In 2026, the wind energy application, specifically turbine blade manufacturing, is expected to hold the largest share of the global composite materials market. Wind turbine blades are the largest single-application consumer of glass fiber composite by weight globally, with record wind capacity additions continuing to drive very large blade manufacturing volumes.

The primary sustainability challenge is the recycling limitation of thermoset composites, which cannot be melted and reprocessed. This is driving investment in thermoplastic composite materials that are inherently recyclable, in recycled carbon fiber processes that recover fiber from end-of-life components, and in bio-based natural fiber composites that offer lower embodied carbon than glass fiber for lower-performance applications. According to Airbus's 2025 sustainability report, the company has set thermoplastic composite adoption targets for next-generation aircraft specifically to address end-of-life recyclability.

The market is primarily driven by the global wind energy expansion program requiring very large volumes of glass and carbon fiber composite for turbine blades.

Key players are Toray Industries Inc. (Japan), Hexcel Corporation (U.S.), Owens Corning (U.S.), Teijin Limited (Japan), SGL Carbon SE (Germany), Mitsubishi Chemical Group Corporation (Japan), Solvay S.A. (Belgium), BASF SE (Germany), Huntsman Corporation (U.S.), Jushi Group Co. Ltd. (China), Gurit Holding AG (Switzerland), Hexagon Composites ASA (Norway), Avient Corporation (U.S.), Nippon Electric Glass Co. Ltd. (Japan), and Chomarat Group (France), among others.

The Middle East and Africa region is expected to register the highest growth rate in the global composite materials market during the forecast period 2026-2036, driven by Saudi Arabia's renewable energy program targeting 130 GW by 2030 per government communications generating large composite wind blade demand, Vision 2030 industrial development driving broader composite material consumption, and Sub-Saharan infrastructure investment growing composite demand from a currently low base.

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Feb-2025

Published Date: Oct-2024

Published Date: May-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates