Resources

About Us

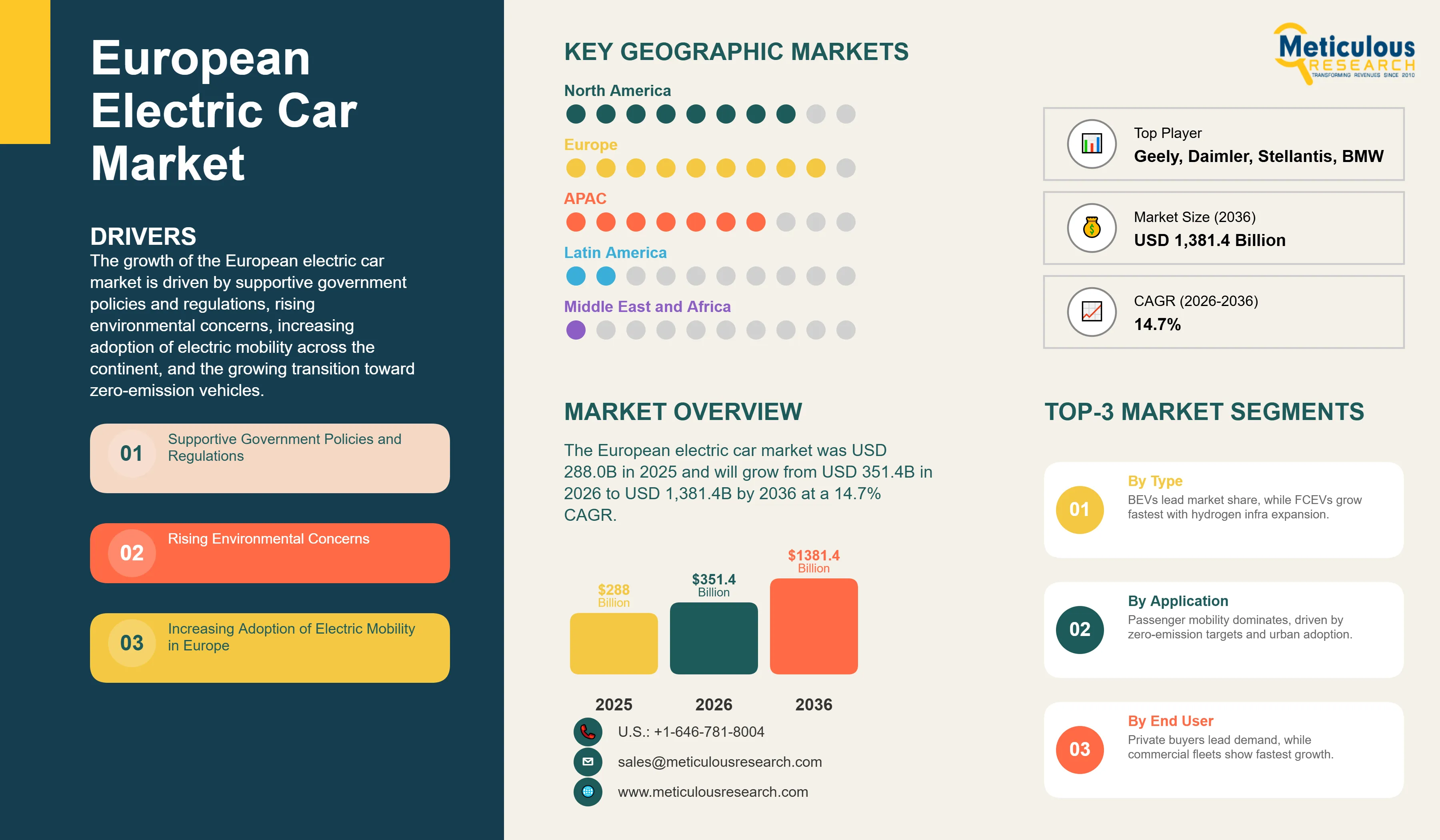

The European electric car market was valued at USD 288.0 billion in 2025. This market is expected to reach approximately USD 1,381.4 billion by 2036 from USD 351.4 billion in 2026, at a CAGR of 14.7% from 2026 to 2036. By volume, the market is expected to reach approximately 16.8 million units by 2036 from 5.0 million units in 2026, at a CAGR of 12.8% from 2026 to 2036. The growth of the European electric car market is driven by supportive government policies and regulations, rising environmental concerns, increasing adoption of electric mobility across the continent, and the growing transition toward zero-emission vehicles. The European Union's stringent emissions regulations and ambitious climate targets are compelling automotive manufacturers to accelerate their electrification strategies, thereby driving significant market expansion.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The European electric car market represents a critical segment of the automotive industry, driven by a combination of regulatory mandates, technological advancements, and shifting consumer preferences. Electric vehicles have evolved from niche products to mainstream transportation solutions, with manufacturers across the continent investing heavily in electrification. The market includes multiple propulsion technologies, including battery electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), pure hybrid electric vehicles (HEVs), and fuel cell electric vehicles (FCEVs), each serving different market segments and use cases.

The commitment of the European Union to achieve carbon neutrality by 2050, coupled with increasingly stringent CO2 emission standards for new vehicles, has created a favorable regulatory environment for electric vehicle adoption. The Euro 7 standards and the EU's Green Deal initiative are driving manufacturers to accelerate their transition away from internal combustion engines. Additionally, member states are implementing various incentive programs, including purchase subsidies, tax benefits, and investments in charging infrastructure, to encourage consumer adoption of electric vehicles.

The market is characterized by intense competition among established automotive manufacturers and emerging EV-focused companies. Traditional automakers such as Volkswagen, BMW, Daimler, and Renault are rapidly expanding their electric vehicle portfolios, while newer entrants and Chinese manufacturers are gaining market share through innovative products and competitive pricing. The availability of diverse vehicle models across different price points and segments has broadened the appeal of electric vehicles beyond early adopters to mainstream consumers.

What are the Key Trends in the European Electric Car Market?

Rapid Expansion of Charging Infrastructure and Battery Technology

A significant trend shaping the European electric car market is the rapid expansion and modernization of charging infrastructure across the continent. Governments and private companies are investing heavily in developing fast-charging networks along major highways and in urban centers, addressing one of the primary concerns of potential EV buyers—range anxiety. Simultaneously, battery technology is advancing rapidly, with improvements in energy density, charging speeds, and cost reduction. The emergence of solid-state batteries and next-generation lithium-ion technologies promises to deliver vehicles with longer ranges and shorter charging times, further accelerating market adoption.

Shift Toward Battery Electric Vehicles and Away from Plug-In Hybrids

Another major trend is the gradual shift of the market toward pure battery electric vehicles (BEVs) as the preferred choice for consumers and manufacturers alike. While plug-in hybrid electric vehicles (PHEVs) served as a transitional technology, regulatory pressures and technological improvements in BEVs are making them increasingly attractive. Manufacturers are consolidating their product strategies around BEVs, and consumers are becoming more confident in the practicality of fully electric vehicles for daily use. This trend is expected to continue as charging infrastructure improves and battery costs continue to decline.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 1,381.4 Billion |

|

Market Size in 2026 |

USD 351.4 Billion |

|

Market Size in 2025 |

USD 288 Brillion |

|

Market Growth Rate (2026-2036) |

CAGR of 14.7% (Revenue) |

|

Volume Growth Rate (2026-2036) |

CAGR of 12.8% (Units) |

|

Units by 2036 |

Approximately 16.8 Million Units |

|

Dominating Region/Country |

Germany |

|

Fastest Growing Countries |

Sweden and Italy |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Propulsion Type, Power Output, End Use, and Geography |

|

Regions Covered |

Germany, France, U.K., Italy, Spain, Netherlands, Sweden, Switzerland, Norway, Denmark, Austria, Belgium, Croatia, Finland, Greece, Hungary, Ireland, Poland, Portugal, Romania, Slovakia, and Rest of Europe |

A primary driver for the European electric car market is the combination of supportive government policies and increasingly stringent environmental regulations. The European Union's commitment to reducing greenhouse gas emissions has resulted in ambitious CO2 reduction targets for the automotive sector. Member states have implemented various policy measures, including purchase incentives, tax exemptions, and grants for charging infrastructure development. These policies have made electric vehicles more affordable and accessible to consumers. Additionally, growing environmental awareness among consumers and the desire to reduce their carbon footprint are driving demand for electric vehicles. The rising prevalence of air quality concerns in urban areas has further accelerated the adoption of zero-emission vehicles.

Opportunity: Growing Adoption of Autonomous Driving and Shared Mobility Services

The convergence of electric vehicle technology with autonomous driving capabilities and shared mobility services presents significant growth opportunities for the market. The increasing adoption of mobility-as-a-service (MaaS) platforms and ride-sharing services is creating demand for electric vehicles optimized for commercial fleet operations. Autonomous electric vehicles are expected to revolutionize urban transportation, reducing the need for private vehicle ownership and creating new business models. Companies investing in the development of autonomous electric vehicles and integrated mobility solutions are well-positioned to capture this growing opportunity.

Why Do Battery Electric Vehicles Lead the Market?

Based on propulsion type, battery electric vehicles (BEVs) are expected to account for the largest share of the European electric car market in 2026. BEVs offer zero tailpipe emissions, lower operating costs compared to conventional vehicles, and are increasingly practical for daily use thanks to improvements in battery technology and charging infrastructure. The growing availability of diverse BEV models across various price points and vehicle segments has broadened their appeal to a wider consumer base.

However, fuel cell electric vehicles (FCEVs) are projected to grow at the fastest CAGR during the forecast period. FCEVs offer several advantages, including fast refueling times comparable to conventional vehicles, longer driving ranges, and zero emissions. Rising government initiatives for establishing hydrogen fuel cell charging stations and increasing investments by leading automotive manufacturers in hydrogen fuel cell technology development are driving growth in this segment. As hydrogen production becomes increasingly renewable and infrastructure develops, FCEVs are expected to play a growing role in the European electric vehicle market, particularly for heavy-duty applications and long-distance travel.

How Does the Private Use Segment Dominate the Market?

Based on end use, the private use segment is expected to account for the largest share of the European electric car market in 2026. Private consumers represent the largest market segment for electric vehicles, driven by improving affordability, expanding model availability, and increasing environmental consciousness. Government incentive programs targeting private purchases have further boosted this segment's growth.

The commercial use segment, however, is projected to grow at the fastest CAGR during the forecast period. The increasing adoption of electric vehicles in shared mobility services, corporate taxi fleets, and commercial delivery operations is driving rapid growth in this segment. Fleet operators are recognizing the total cost of ownership benefits of electric vehicles, including lower fuel and maintenance costs. Additionally, regulatory pressure to reduce fleet emissions and corporate sustainability commitments are encouraging businesses to transition to electric vehicles for their operations.

How is Germany Maintaining Its Leadership in the European Electric Car Market?

Germany is expected to command the largest share of the European electric car market in 2026, both in terms of revenue and volume. The country's dominance is attributed to its strong automotive manufacturing base, significant investments in electric vehicle development by major OEMs such as Volkswagen, BMW, and Daimler, and supportive government policies. Germany's commitment to the energy transition (Energiewende) and ambitious climate targets have created a favorable environment for electric vehicle adoption. The country also hosts a well-developed charging infrastructure network and has established itself as a hub for battery manufacturing and electric vehicle innovation.

Which Countries Are Experiencing Rapid Growth in the European Electric Car Market?

Sweden and Italy are projected to witness the fastest growth during the forecast period. Sweden's rapid adoption is driven by strong government support for electrification, high environmental consciousness among consumers, and the country's commitment to banning diesel-powered vehicles. The country has achieved one of the highest electric vehicle penetration rates in Europe, with electric vehicles accounting for a significant share of new car sales.

Italy is experiencing accelerated growth due to government incentives for electric vehicle purchases, major automotive manufacturers' investments in developing the electric mobility ecosystem, and increasing stakeholder investment in fast-charging infrastructure. The Italian government's ambitious target to have one million electric cars on roads and its plans to ban diesel vehicles are supporting rapid market expansion. France, the Netherlands, and other Western European countries are also experiencing strong growth driven by similar policy support and infrastructure development initiatives.

The European electric car market features a diverse competitive landscape with established automotive manufacturers and emerging EV-focused companies. Key players include BMW Group, Volkswagen AG, Stellantis N.V., Daimler AG, Groupe Renault, Geely Automobile Holdings Limited, BYD Company Ltd., AB Volvo, MG Motor U.K. Ltd., and Alcraft Motor Company Ltd. These manufacturers compete on the basis of product innovation, battery technology, charging infrastructure partnerships, pricing strategies, and brand positioning. The market is characterized by rapid consolidation, strategic partnerships, and significant capital investments in electric vehicle development and manufacturing capacity expansion.

The European electric car market is expected to grow from USD 351.4 billion in 2026 to USD 1,381.4 billion by 2036.

The European electric car market is expected to grow at a CAGR of 14.7% from 2026 to 2036 in terms of revenue, and at a CAGR of 15.2% by volume.

The key players operating in the European electric car market include BMW Group, Volkswagen AG, Stellantis N.V., Daimler AG, Groupe Renault, Geely Automobile Holdings Limited, BYD Company Ltd., AB Volvo, MG Motor U.K. Ltd., and Alcraft Motor Company Ltd.

The main factors include supportive government policies and regulations, rising environmental concerns, increasing adoption of electric mobility, stringent EU emissions standards, and the growing transition toward zero-emission vehicles.

Germany will lead the European electric car market during the forecast period 2026 to 2036, while Sweden and Italy are expected to witness the fastest growth.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Assessment

2.3.1. Market Size Estimation

2.3.2. Bottom-Up Approach

2.3.3. Top-Down Approach

2.3.4. Growth Forecast

2.4. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Market Analysis, by Propulsion Type

3.3. Market Analysis, by Power Output

3.4. Market Analysis, by End Use

3.5. Market Analysis, by Geography

3.6. Competitive Analysis

4. Long-term Impact of the COVID-19 Pandemic on the European Electric Car Market

4.1. Scenario A: Severe Impact

4.2. Scenario B: Slow Recovery

4.3. Scenario C: Fast Recovery

5. Market Insights

5.1. Introduction

5.2. Market Dynamics

5.3. Drivers

5.3.1. Supportive Government Policies and Regulations

5.3.2. Rising Environmental Concerns

5.3.3. Increasing Adoption of Electric Mobility in Europe

5.4. Restraints

5.4.1. High Costs of Electric Cars

5.5. Opportunities

5.5.1. Growing Adoption of Autonomous Driving Vehicles

5.5.2. Rising Trend of Shared Mobility

5.6. Challenges

5.6.1. Range Anxiety Associated with the Use of Electric Cars

5.6.2. Lack of Fast-Charging Infrastructure

5.7. Value Chain Analysis

6. European Electric Car Market, by Propulsion Type

6.1. Introduction

6.2. Hybrid Electric Vehicles

6.2.1. Pure Hybrid Electric Vehicles

6.2.2. Plug-In Hybrid Electric Vehicles

6.3. Battery Electric Vehicles

6.4. Fuel Cell Electric Vehicles

7. European Electric Car Market, by Power Output

7.1. Introduction

7.2. Less Than 100kW

7.3. 100kW to 250kW

8. European Electric Car Market, by End Use

8.1. Introduction

8.2. Private Use

8.3. Commercial Use

9. European Electric Car Market, by Geography

9.1. Introduction

9.2. Germany

9.3. France

9.4. U.K.

9.5. Netherlands

9.6. Norway

9.7. Italy

9.8. Belgium

9.9. Spain

9.10. Sweden

9.11. Switzerland

9.12. Poland

9.13. Denmark

9.14. Austria

9.15. Finland

9.16. Portugal

9.17. Ireland

9.18. Hungary

9.19. Romania

9.20. Greece

9.21. Slovakia

9.22. Croatia

9.23. Rest of Europe

10. Competitive Landscape

10.1. Introduction

10.2. Key Growth Strategies

10.3. Key Players in the European Electric Car Market

10.3.1. BMW Group

10.3.2. Volkswagen AG

10.3.3. Stellantis N.V.

11. Company Profiles

11.1. BMW Group

11.2. Volkswagen AG

11.3. Stellantis N.V.

11.4. Daimler AG

11.5. Groupe Renault

11.6. Geely Automobile Holdings Limited

11.7. BYD Company Ltd.

11.8. AB Volvo

11.9. MG Motor U.K. Ltd.

11.10. Alcraft Motor Company Ltd.

11.11. Others

12. Appendix

12.1. Questionnaire

12.2. Available Customization

Published Date: Feb-2026

Published Date: Feb-2026

Published Date: Jun-2024

Published Date: Apr-2024

Published Date: Jan-2022

Subscribe to get the latest industry updates