Resources

About Us

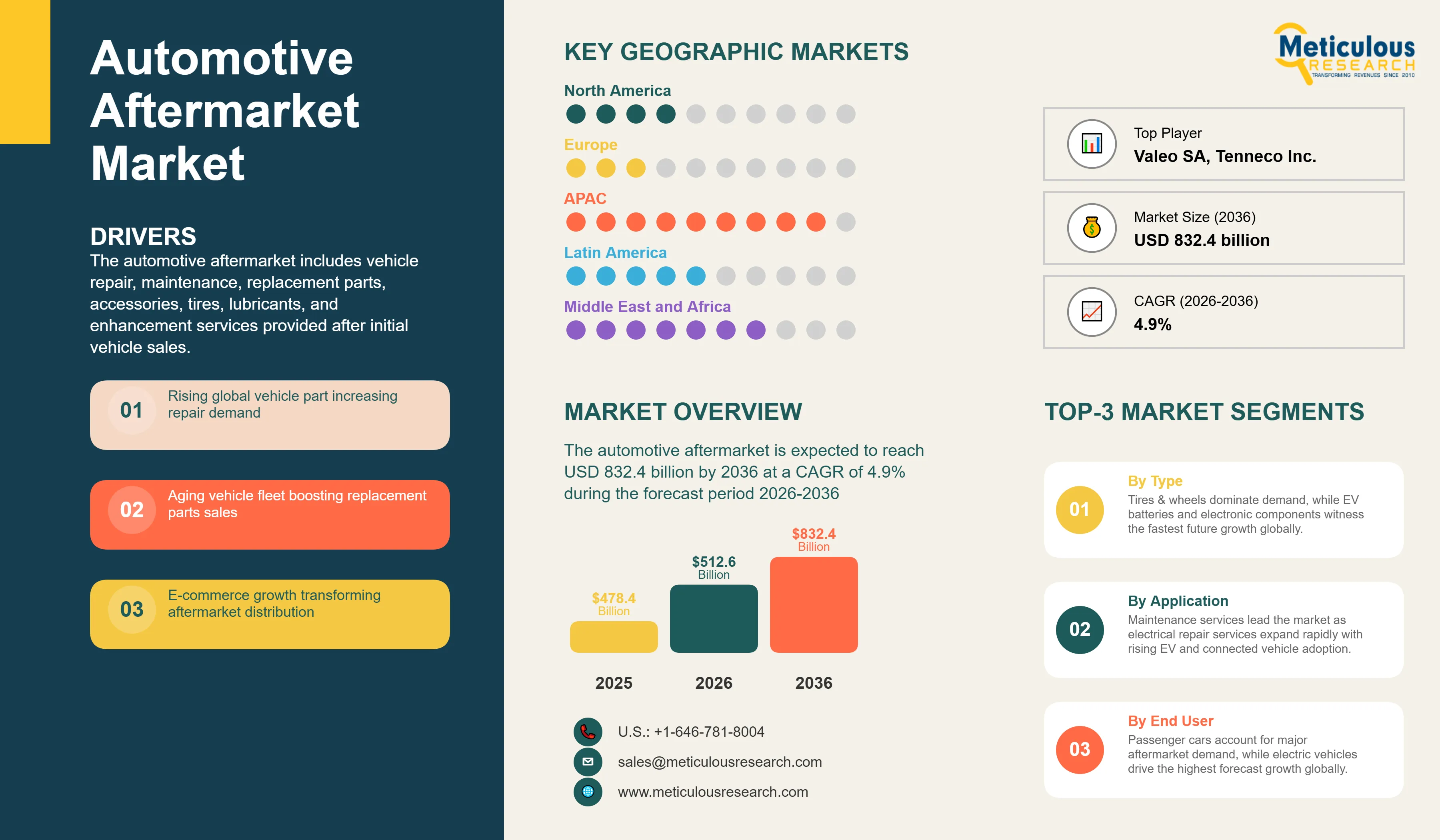

Automotive Aftermarket Market Size, Share & Trends Analysis by Replacement Part, Service, Vehicle, Application, Distribution Channel, and End User - Global Opportunity Analysis & Industry Forecast (2026-2036)

Report ID: MRAUTO - 1041965 Pages: 315 May-2026 Formats*: PDF Category: Automotive and Transportation Delivery: 24 to 72 Hours Download Free Sample ReportThe global automotive aftermarket market was valued at USD 478.4 billion in 2025. This market is expected to reach USD 832.4 billion by 2036 from an estimated USD 512.6 billion in 2026, growing at a CAGR of 4.9% during the forecast period 2026-2036. According to Hedges & Company’s 2025 analysis, there are approximately 1.645 billion vehicles in the world. The growing installed base of vehicles requiring regular maintenance, repair, and parts replacement that is the fundamental demand engine of the automotive aftermarket.

Click here to: Get Free Sample Pages of this Report

The automotive aftermarket encompasses all products and services related to vehicle maintenance, repair, and enhancement after a vehicle's initial sale, including replacement parts, accessories, lubricants, tires, and the labor services of repair workshops and service centers. Every vehicle on the road requires maintenance throughout its service life, from routine oil changes and filter replacements that occur multiple times per year to less frequent but higher-value replacement of brake components, suspension parts, and eventually powertrain components. The aftermarket serves this demand through a supply chain that runs from parts manufacturers through distributors and retailers to the workshops and service centers that install components and perform services.

The market is growing because its two most fundamental demand drivers, the size of the global vehicle fleet and the age of that fleet, are both increasing simultaneously. Older vehicles require more frequent maintenance and are more likely to need component replacements than newer vehicles, meaning a fleet that is both larger and older than it has ever been generating the most intensive aftermarket demand in the industry's history.

Two transformations are defining the market's next decade. The growth of e-commerce in automotive parts, which the Auto Care Association identified as one of the fastest-growing distribution channels in the aftermarket, is fundamentally changing how parts are procured and how price competition works across the independent aftermarket. Amazon Automotive, RockAuto, eBay Motors, and the major parts retailer online platforms collectively represent a growing share of parts sales that is compressing margins in the traditional brick-and-mortar distribution channel while expanding consumer access to a much broader product range than any single physical store can carry. The second transformation is the EV aftermarket, which is still in its early stages but is creating a new and growing service category for high-voltage battery health assessment, battery replacement, electric drive system maintenance, and charging system service that requires new tools, training, and supplier relationships across the independent repair sector.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 832.4 Billion |

|

Market Size in 2026 |

USD 512.6 Billion |

|

Market Size in 2025 |

USD 478.4 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 4.9% |

|

Dominating Replacement Part |

Tires and Wheels |

|

Fastest Growing Replacement Part |

Electrical & Electronic Components (EV Batteries) |

|

Dominating Service Type |

Maintenance Services |

|

Fastest Growing Service Type |

Repair Services (Electrical) |

|

Dominating Vehicle Type |

Passenger Cars |

|

Fastest Growing Vehicle Type |

Electric Vehicles |

|

Dominating Application |

Wear and Tear Parts |

|

Fastest Growing Application |

EV-Specific Components |

|

Dominating Distribution Channel |

Independent Aftermarket (IAM) |

|

Fastest Growing Distribution Channel |

Online/E-commerce |

|

Dominating End User |

Individual Vehicle Owners |

|

Fastest Growing End User |

Fleet Operators |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

Middle East & Africa |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Record Vehicle Age Driving Above-Average Maintenance and Repair Spending

The aging of the global vehicle fleet is the most powerful structural trend supporting automotive aftermarket demand, and the U.S. market provides the clearest data point. According to S&P Global Mobility's 2025 annual vehicle age report, the average age of light vehicles on U.S. roads reached a record 12.8 years in 2024, up from 12.1 years in 2020. This represents a significant shift in the composition of the vehicle parc toward older vehicles that require more frequent servicing, more extensive repairs, and higher-value component replacements than newer vehicles still under manufacturer warranty. The same aging trend is visible in European markets, where the average vehicle age increased across most major markets in 2024 according to the European Automobile Manufacturers Association's 2025 data.

The commercial implication for the aftermarket is that each incremental year of average fleet age shifts a larger proportion of vehicles out of the manufacturer warranty period where OEM-authorized dealers capture the majority of service business, and into the independent aftermarket where the full ecosystem of independent repair shops, parts retailers, and distributors competes for the service spend. According to the Auto Care Association's 2025 data, vehicles that are four to twelve years old generate the highest aftermarket spending per vehicle, as this age bracket combines significant wear-driven parts replacement requirements with the fact that out-of-warranty owners seek the cost advantages of independent repair over dealer service. The current and projected age of the vehicle fleet positions this high-spending age bracket as the dominant segment of the global aftermarket through the forecast period.

E-Commerce Reshaping Parts Distribution and Consumer Expectations

The shift of automotive parts procurement toward online channels is one of the most structurally significant competitive changes in the aftermarket's recent history, compressing margins in traditional distribution while expanding the total addressable market by making parts accessible to consumers and small workshops in locations that lacked local inventory. Amazon Automotive has grown to become a major parts sales channel, offering millions of part numbers with prime delivery to consumers' homes and to professional installer accounts, and according to the Auto Care Association's 2025 Fact Book, online channels were the fastest-growing distribution format in the U.S. aftermarket in 2024. European e-commerce parts platforms including Autodoc and Mister Auto are experiencing similarly rapid growth across European markets where the independent aftermarket has traditionally been served by multi-tier distributor networks.

The major traditional aftermarket retailers are responding by building their own robust e-commerce capabilities. AutoZone, O'Reilly Auto Parts, and Advance Auto Parts have all invested heavily in digital ordering, same-day delivery, and buy-online-pick-up-in-store capabilities. According to AutoZone's fiscal year 2025 results, its commercial and online channels both grew at above-average rates, with same-day delivery to professional installer accounts growing as a key competitive differentiator. LKQ Corporation, the world's largest independent distributor of alternative parts, has been expanding its digital platform capabilities to serve its large network of professional installer customers with faster order-to-delivery cycles and broader catalog access than traditional phone and counter ordering.

EV Aftermarket Emerging as the Defining New Service Category

The growing global electric vehicle fleet, which according to the IEA's Global EV Outlook 2025 reached approximately 17-18 million annual sales and over 55 million total vehicles on the road by end of 2024, is creating an entirely new service category in the automotive aftermarket that the independent repair sector is only beginning to develop the tools, training, and supply chain relationships to serve. EV battery packs, which represent 30 to 40% of the total vehicle cost according to McKinsey 2026 analysis, are the highest-value replaceable component in any vehicle by a large margin, and as the first generations of mass-market EVs approach the end of their initial battery warranty periods, the battery service and replacement market is beginning to emerge as a commercial reality.

Independent repair shops face significant challenges in entering the EV service market: high-voltage battery systems require specialized safety training and certification, dedicated high-voltage diagnostic equipment, and either battery module replacement capability or relationships with battery refurbishment providers. According to the National Institute for Automotive Service Excellence's 2025 communications, the demand for ASE EV certification programs has grown substantially as independent shops recognize the competitive necessity of building EV service capability before the EV fleet grows large enough to represent a significant fraction of their service volume. Bosch, Snap-on, and Autel have all launched dedicated EV service training programs and tool packages targeting independent workshops, and the Auto Care Association has established an EV service working group to develop industry standards for independent EV service.

Increasing Average Vehicle Age

The aging of the global vehicle fleet is the primary structural driver of automotive aftermarket demand, as older vehicles generate more frequent and more extensive maintenance and repair requirements per vehicle than newer ones. According to S&P Global Mobility's 2025 data, the average age of light vehicles on U.S. roads reached a record 12.8 years in 2024, and this trend is broadly consistent across European, Australian, and increasingly Asian markets. The vehicle age increase is driven by improvements in vehicle durability and reliability that allow vehicles to remain operational for longer, combined with economic factors including high new vehicle prices that are encouraging owners to maintain existing vehicles longer rather than replacing them.

Rising Vehicle Parc (Global Car Population)

The global vehicle parc surpassed 1.5 billion registered vehicles according to S&P Global Mobility's 2025 data, and it continues to grow as vehicle production adds millions of new vehicles annually across all markets. According to OICA’s data, global motor vehicle production reached about 92.7 million units in 2024 and rose to 96.4 million in 2025. Each new vehicle added to the global parc represents a new aftermarket customer that will generate parts and service demand for its entire operational life of 15 to 20 years. The rapid growth of the vehicle parc in emerging markets including India, Southeast Asia, and the Middle East is adding very large numbers of new vehicles to the global aftermarket customer base, driven by rising vehicle ownership and expanding middle-class demand.

Growth in EV Aftermarket (Battery, Electronics)

The EV aftermarket represents the most significant new growth opportunity in the automotive aftermarket for the forecast period, as the global EV fleet of over 55 million vehicles per the IEA's Global EV Outlook 2025 begins its transition from the initial ownership period into the service and maintenance cycle. Battery health assessment and eventual battery replacement are the highest-value EV service categories, with battery pack replacement costs for mainstream EVs ranging from several thousand to over ten thousand dollars depending on the vehicle and chemistry. As more EVs exit their initial battery warranties, the demand for third-party battery service and replacement will grow rapidly. According to BloombergNEF’s Electric Vehicle Outlook 2025, global EV sales are projected to keep rising rapidly, reaching about 39 million passenger EV sales by 2030 and creating a fast-growing vehicle population that the aftermarket must be ready to serve.

Digitalization of Service Platforms

The digitalization of automotive service platforms, including online appointment booking, digital vehicle health monitoring, connected vehicle diagnostic data access, and predictive parts replenishment, is creating new efficiency and customer engagement capabilities for aftermarket service providers that improve workshop utilization and customer retention. Connected vehicle platforms from major OEMs are generating diagnostic data that, with appropriate regulatory access frameworks, can provide independent workshops with advance warning of developing faults before customers experience a breakdown, enabling proactive service outreach. According to the Auto Care Association's 2025 data on Right-to-Repair developments, the U.S. memorandum of understanding between automakers and independent repairers on telematics data access provides a framework for independent shops to access connected vehicle data, and European regulations are also expanding independent access to vehicle diagnostic data. This data access is enabling new predictive maintenance service models that convert the traditional reactive repair relationship into a proactive service partnership that generates more frequent but lower-cost service interactions.

By Replacement Part: In 2026, Tires and Wheels to Hold the Largest Share

Based on replacement part, the global automotive aftermarket market is segmented into engine components, transmission and drivetrain parts, brake system components, electrical and electronic components, suspension and steering parts, tires and wheels, filters, and lighting and interior components. In 2026, the tires and wheels segment is expected to account for the largest share of the global automotive aftermarket market. Tires are the most universally purchased replacement product across the entire vehicle fleet, with every vehicle requiring tire replacement at intervals of typically three to five years regardless of age, make, or model. The very high volume of tire replacements across the global vehicle parc generates the highest total aftermarket parts revenue of any single product category. Bridgestone, Michelin, and Continental are the world's three largest tire companies by revenue, with tire replacement representing a large and stable recurring revenue stream across their global distribution networks.

However, the electrical and electronic components segment, particularly batteries including EV batteries, is projected to register the highest CAGR during the forecast period. The growing EV fleet requires high-voltage battery service and replacement products that are entirely new to the aftermarket supply chain, alongside the continued growth of 12-volt starter battery replacement which is a regular aftermarket item across all ICE vehicles. EV battery replacement, as the first generation of mass-market EVs approaches warranty expiration, represents the highest per-unit-value replacement part opportunity in the aftermarket's history.

By Distribution Channel: In 2026, Independent Aftermarket (IAM) to Hold the Largest Share

Based on distribution channel, the global automotive aftermarket market is segmented into OEM authorized service centers, independent aftermarket, retail stores, and online and e-commerce platforms. In 2026, the independent aftermarket segment is expected to account for the largest share of the global automotive aftermarket market. The independent aftermarket, comprising independent repair workshops, multi-brand service chains, and independent parts distributors and retailers, serves the majority of vehicles in most major markets once they exit the initial manufacturer warranty period. The IAM's competitive advantages of lower labor rates, broader parts choice, and greater geographic accessibility than OEM dealer networks make it the preferred service channel for the majority of vehicle owners with out-of-warranty vehicles.

However, the online and e-commerce segment is projected to register the highest CAGR during the forecast period. The structural shift of automotive parts procurement toward digital channels, driven by Amazon Automotive, major retailer online platforms, and specialist e-commerce parts retailers, is growing the online channel's share of total parts distribution at consistently above-average rates. According to the Auto Care Association's 2025 Fact Book, online was the fastest-growing distribution format in the U.S. aftermarket in 2024, a trend mirrored across European and emerging markets.

Automotive Aftermarket Market by Region: Asia-Pacific Leading by Share, Middle East and Africa by Growth

Based on geography, the global automotive aftermarket market is segmented into Asia-Pacific, North America, Europe, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global automotive aftermarket market. The region's dominance reflects the world's largest vehicle parc concentrated in China, India, Japan, and South Korea, combined with very large and rapidly growing vehicle sales volumes that continuously expand the regional aftermarket customer base. China is the world's largest vehicle market by both new sales and total parc, with the China Passenger Car Association reporting total vehicle population exceeding 460 million units per its 2025 data, creating the world's largest single-country aftermarket demand base. According to SIAM's 2025 data, India's domestic vehicle sales exceeded 28 million units in fiscal year 2025, making India one of the world's top five vehicle markets and a rapidly growing aftermarket opportunity as these vehicles enter the service cycle. Japan's very large and sophisticated automotive aftermarket, served by a well-developed network of dealerships and independent repair shops, is a major regional contributor. Indonesia, Thailand, and Vietnam have large and growing vehicle populations with significant two-wheeler aftermarket activity alongside growing four-wheeler maintenance demand.

However, the Middle East and Africa region is expected to grow at the fastest CAGR during the forecast period. The Middle East has among the world's highest vehicle ownership rates relative to population, particularly in Gulf Cooperation Council countries, and the extreme heat, dust, and driving conditions of the region accelerate wear on multiple vehicle systems including cooling components, filters, brake parts, and tires, driving above-average parts replacement frequency per vehicle compared with temperate climate markets. Saudi Arabia's Vision 2030 industrialization programs are expanding domestic automotive service infrastructure, and the UAE continues to attract large volumes of imported vehicles that require ongoing aftermarket service. Sub-Saharan Africa's rapidly growing urban populations and rising vehicle ownership rates, combined with a predominantly older vehicle fleet that requires intensive maintenance, are creating growing aftermarket demand. Turkey's large automotive market and its position as a manufacturing and distribution hub for the broader Middle East and North Africa region adds to the regional growth trajectory.

North America is the world's most mature and developed automotive aftermarket, with the United States home to the largest concentration of major aftermarket retailers and distributors globally including AutoZone, O'Reilly Auto Parts, Advance Auto Parts, LKQ Corporation, and Genuine Parts Company NAPA. The combination of record vehicle age, the very large U.S. vehicle parc, and the well-established independent aftermarket infrastructure makes North America the highest-revenue individual regional market. Europe is a large and technically sophisticated aftermarket characterized by strong independent aftermarket networks, pan-European distribution by LKQ Corporation and other large distributors, and the Right-to-Repair regulatory framework that ensures independent repairers maintain access to OEM technical data and diagnostic tools.

The automotive aftermarket is one of the most diverse and fragmented large industries in the global economy, spanning Tier-1 automotive suppliers that sell replacement parts through aftermarket channels, large national and regional parts retailers and distributors, tire companies with large replacement tire businesses, and service chain operators. Competition in parts distribution is based on parts availability breadth, delivery speed, pricing competitiveness, technical support quality, and increasingly digital platform capabilities. In service, competition is based on technical competence, pricing, geographic accessibility, and brand trust.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, distribution networks, geographic presence, and recent strategic developments. Some of the key players operating in the global automotive aftermarket market include Robert Bosch GmbH (Germany), DENSO Corporation (Japan), Continental AG (Germany), ZF Friedrichshafen AG (Germany), Valeo SA (France), Magna International Inc. (Canada), BorgWarner Inc. (U.S.), AutoZone Inc. (U.S.), LKQ Corporation (U.S.), Genuine Parts Company/NAPA (U.S.), O'Reilly Automotive Inc. (U.S.), Advance Auto Parts Inc. (U.S.), Bridgestone Corporation (Japan), Michelin Group (France), and Tenneco Inc. (U.S.), among others.

The global automotive aftermarket market is expected to reach USD 832.4 billion by 2036 from an estimated USD 512.6 billion in 2026, at a CAGR of 4.9% during the forecast period 2026-2036.

In 2026, the tires and wheels segment is expected to hold the largest share of the global automotive aftermarket market, driven by tires being the most universally replaced product across the entire global vehicle fleet with replacement intervals of three to five years applicable regardless of vehicle age, make, or market.

The electrical and electronic components segment, particularly batteries including EV batteries, is projected to register the highest CAGR during the forecast period, driven by the growing EV fleet requiring high-voltage battery service and replacement as the first generation of mass-market EVs approaches end of initial warranty periods, representing the highest per-unit-value replacement category in the aftermarket.

The online and e-commerce segment is projected to register the highest CAGR during the forecast period, driven by Amazon Automotive, major retailer digital platforms, and specialist e-commerce parts retailers growing their share of parts procurement.

The growing EV fleet is creating an entirely new high-value aftermarket service category, with EV battery health assessment and replacement representing the highest-value per-unit service opportunity the aftermarket has ever seen. EVs require fewer routine maintenance items than ICE vehicles but add specialized high-voltage electrical service requirements. According to the IEA's Global EV Outlook 2025, the global EV stock exceeded 55 million vehicles by end of 2024, establishing the beginning of a meaningful EV aftermarket that will grow rapidly through the forecast period as more EVs exit their initial warranty periods.

Key players are Robert Bosch GmbH (Germany), DENSO Corporation (Japan), Continental AG (Germany), ZF Friedrichshafen AG (Germany), Valeo SA (France), Magna International Inc. (Canada), BorgWarner Inc. (U.S.), AutoZone Inc. (U.S.), LKQ Corporation (U.S.), Genuine Parts Company/NAPA (U.S.), O'Reilly Automotive Inc. (U.S.), Advance Auto Parts Inc. (U.S.), Bridgestone Corporation (Japan), Michelin Group (France), and Tenneco Inc. (U.S.), among others.

The Middle East and Africa region is expected to register the highest growth rate in the global automotive aftermarket market during the forecast period 2026-2036, driven by the region's high vehicle ownership rates in Gulf states, extreme climate conditions that accelerate parts replacement intervals, rapidly growing urban vehicle fleets across Sub-Saharan Africa, and Saudi Arabia's Vision 2030 infrastructure expansion generating a larger and younger vehicle fleet requiring ongoing service.

Published Date: Jan-2025

Published Date: Nov-2024

Published Date: Sep-2024

Published Date: Aug-2024

Published Date: Jun-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates