Resources

About Us

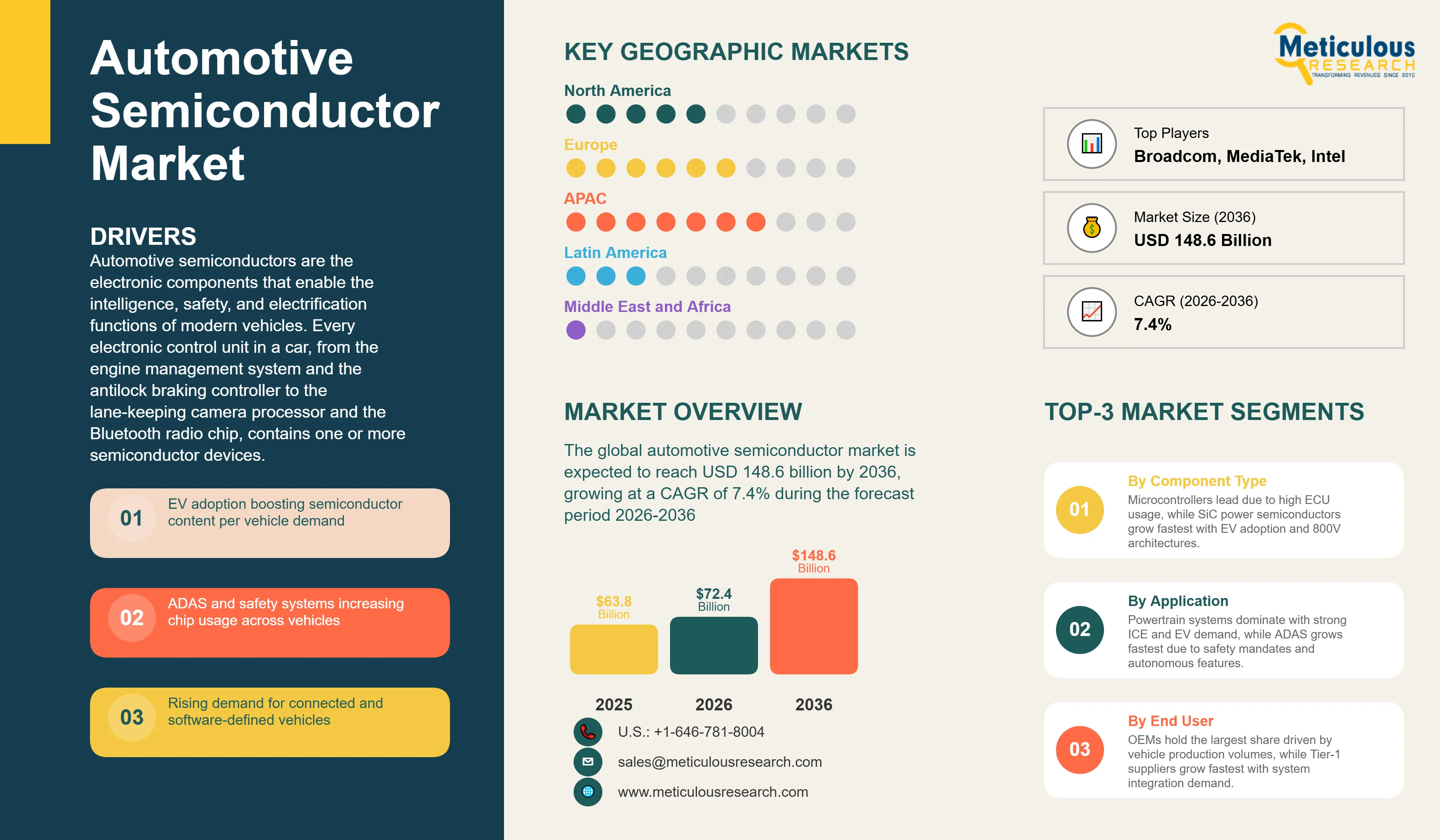

Automotive Semiconductor Market Size, Share & Trends Analysis by Component Type, Vehicle Type, Application End User, and Geography - Global Opportunity Analysis & Industry Forecast (2026-2036)

Report ID: MRAUTO - 1041957 Pages: 321 May-2026 Formats*: PDF Category: Automotive and Transportation Delivery: 24 to 72 Hours Download Free Sample ReportThe global automotive semiconductor market was valued at USD 63.8 billion in 2025. This market is expected to reach USD 148.6 billion by 2036 from an estimated USD 72.4 billion in 2026, growing at a CAGR of 7.4% during the forecast period 2026-2036. According to the Semiconductor Industry Association's 2025 Global Semiconductor Sales Report, the semiconductor market reached about $630.5 billion in 2024. Automotive remains an important growth end market as electrification, ADAS, and digital cockpit systems continue to raise semiconductor content per vehicle.

Click here to: Get Free Sample Pages of this Report

Automotive semiconductors are the electronic components that enable the intelligence, safety, and electrification functions of modern vehicles. Every electronic control unit in a car, from the engine management system and the antilock braking controller to the lane-keeping camera processor and the Bluetooth radio chip, contains one or more semiconductor devices. A conventional ICE vehicle from a decade ago contained perhaps 30 to 50 ECUs with relatively simple microcontrollers. A modern premium EV with full ADAS capability can contain over 100 ECUs and require semiconductors worth several thousand dollars per vehicle, covering microcontrollers, application processors, power semiconductors, image sensors, radar ICs, memory chips, and connectivity devices. The semiconductor is the foundation upon which every feature of the modern vehicle is built.

The market is growing because the amount of semiconductor content per vehicle is increasing rapidly across all vehicle segments, and the global vehicle production base of approximately 94 million units annually per OICA's 2025 data provides the volume foundation for this growing per-vehicle silicon spend. Infineon’s 2025 Automotive Market Outlook indicates that semiconductor content per vehicle continues to increase as EV adoption, ADAS, and digital cockpit features expand. Premium EVs with advanced driver-assistance systems already carry far higher semiconductor content per vehicle, and this is expected to rise further as autonomous driving capabilities advance.

Two technology transitions are defining the current growth phase. The shift from 400-volt to 800-volt EV architecture is transforming the power semiconductor specification across the vehicle, with silicon carbide power devices replacing silicon IGBTs in traction inverters, on-board chargers, and DC-DC converters because SiC handles the higher voltages and switching frequencies of 800-volt systems more efficiently. According to Infineon's 2025 investor presentations, its SiC revenue in automotive applications grew at triple-digit rates in 2024 and the company has booked multi-year supply agreements with major automakers and Tier-1 suppliers totaling billions of euros in committed SiC revenue through the end of the decade. The second transition is the shift from centralized domain architecture to zonal computing architecture in premium vehicles, where zone controllers and central compute platforms based on high-performance application processors replace the fragmented ECU networks of conventional vehicles, driving very large increases in processing semiconductor content per vehicle.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 148.6 Billion |

|

Market Size in 2026 |

USD 72.4 Billion |

|

Market Size in 2025 |

USD 63.8 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 7.4% |

|

Dominating Component Type |

Microcontrollers (MCUs) |

|

Fastest Growing Component Type |

Power Semiconductors (SiC) |

|

Dominating Vehicle Type |

Passenger Vehicles |

|

Fastest Growing Vehicle Type |

Electric Vehicles (EVs) |

|

Dominating Application |

Powertrain Systems |

|

Fastest Growing Application |

ADAS |

|

Dominating End User |

OEMs |

|

Fastest Growing End User |

Tier-1 Suppliers |

|

Dominating Technology Node |

>90 nm |

|

Fastest Growing Technology Node |

<45 nm |

|

Dominating Packaging Type |

Traditional Packaging |

|

Fastest Growing Packaging Type |

Advanced Packaging (SiP, Chiplets) |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

Europe |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

NVIDIA and Qualcomm Entering Automotive as a Major Growth Market

The growing computational demands of ADAS, autonomous driving, and digital cockpit systems have attracted leading data center chip companies into the automotive semiconductor market, creating a new competitive dynamic where consumer and data center chip architectures are adapted for the stringent reliability and safety requirements of automotive applications. NVIDIA's DRIVE platform, which uses GPU-based processing for autonomous driving AI workloads, has been selected by Volvo Cars, BYD, Mercedes-Benz, and several Chinese automakers as the AI compute foundation for their ADAS and autonomous driving programs. According to NVIDIA's fiscal year 2025 results presentation, its automotive segment revenue grew to approximately USD 1.7 billion in fiscal year 2025, and the company has disclosed automotive design win commitments reaching USD 11 billion over the coming six years from its NVIDIA DRIVE Orin and DRIVE Thor platforms.

Qualcomm's Snapdragon Digital Chassis platform, which provides high-performance computing for digital cockpit, ADAS, and connectivity applications using the same semiconductor architecture as its mobile processors, has secured design wins at BMW, Mercedes-Benz, Renault, and several other automakers. According to Qualcomm’s 2025 investor communications, the company’s automotive pipeline continues to grow meaningfully over the next several years, reflecting adoption of its digital cockpit, connectivity, and ADAS platforms. This entry of high-performance computing companies into automotive is raising the technology ceiling for vehicle compute architecture and is generating a new and high-value tier of automotive semiconductor procurement that is growing faster than any other application category.

SiC Supply Chain Investment Intensifying to Meet EV Demand

Silicon carbide power semiconductors have moved from a niche specialty product to a strategically critical technology in the span of just three years, driven by the rapid growth of 800-volt EV architecture adoption and the very large SiC content advantage per vehicle in 800-volt versus 400-volt systems. The SiC content in a single 800-volt EV traction inverter can exceed USD 300 to USD 400 in device value compared with USD 50 to USD 100 for a comparable silicon IGBT-based inverter, representing a very large incremental semiconductor revenue opportunity per vehicle.

The SiC wafer supply chain is a particular focus of competitive investment because high-quality 8-inch SiC wafer capacity is critically constrained relative to projected demand. Wolfspeed, the world's largest SiC wafer and device manufacturer, has invested very heavily in a new 8-inch SiC manufacturing facility in North Carolina while simultaneously negotiating to restructure its balance sheet in response to financing challenges in 2025, highlighting both the commercial importance and the capital intensity of SiC manufacturing scale-up. Bosch's SiC wafer and device manufacturing in Germany, onsemi's SiC vertically integrated manufacturing, and Renesas's SiC device development are all part of a global supply chain build-out that is defining the competitive landscape for automotive power semiconductors for the coming decade. According to Infineon's 2025 investor presentations, the company has secured multi-year SiC supply agreements totaling billions of euros in committed revenue, reflecting the strategic importance automotive customers place on securing SiC supply.

Software-Defined Vehicle Architecture Reshaping Semiconductor Requirements

The progressive transition of automotive electrical architecture from a network of dozens of ECUs each running dedicated software to a zonal or domain-consolidated architecture with fewer, more powerful zone controllers and central computers is creating a major shift in which semiconductor products the automotive industry buys. In the conventional distributed ECU architecture, each function like window control, mirror adjustment, seat memory, and parking sensor has its own dedicated microcontroller, creating a market for very large volumes of relatively simple and inexpensive MCUs. In the zonal architecture being adopted by BMW, Volkswagen, Stellantis, and others, a single zone controller handles all the electrical functions of one vehicle zone with a much more powerful processor running a hypervisor that manages multiple software functions simultaneously.

This architectural transition reduces the total number of semiconductor units per vehicle while dramatically increasing the processing power and memory content per semiconductor, shifting spend from low-cost microcontrollers toward high-performance application processors and large memory capacities. Renesas Electronics, which reported growing demand for its R-Car series automotive application processors in its 2025 results, and NXP Semiconductors, whose S32 automotive platform targets zonal and domain controller applications, are both positioned to benefit from this architectural transition. According to NXP's 2025 first-half investor communications, its automotive segment revenue grew above the company's overall average, driven by strong S32 processor and radar sensor demand across European and Asian automotive customers implementing next-generation vehicle architectures.

Increasing Electrification of Vehicles (EVs & Hybrids)

Vehicle electrification is the single strongest demand driver for automotive semiconductors because EVs require fundamentally more and more valuable semiconductor content than equivalent ICE vehicles. The traction inverter alone, which converts DC battery power to three-phase AC for the electric motor, requires SiC or IGBT power modules, gate driver ICs, current sensors, and a microcontroller managing switching at tens of kilohertz. Battery management systems require precision analog ICs for cell voltage and temperature measurement across hundreds of cells simultaneously. Charging systems require additional power semiconductor stages for both AC-DC and DC-DC conversion. According to the IEA's Global EV Outlook 2025, global electric car sales reached approximately 17-18 million units in 2024, with the China Passenger Car Association reporting over 12 million NEV sales in China alone, establishing EV electrification as the dominant structural demand driver for the automotive semiconductor market through the forecast period.

Growth in ADAS and Autonomous Driving Systems

Advanced driver assistance systems are transitioning from premium options to standard equipment across all vehicle price segments, driven by regulatory mandates and consumer safety demand, creating growing semiconductor content requirements per vehicle in camera processors, radar ICs, sensor fusion compute platforms, and AI inference chips. The EU General Safety Regulation, which requires automatic emergency braking, lane keeping, and related ADAS features on all new vehicles from July 2024, mandates the semiconductor content that supports these systems across every new vehicle sold in Europe. According to Infineon's 2025 Automotive Market Outlook, ADAS semiconductor content per vehicle is expected to grow significantly as regulatory requirements expand and as automakers move from Level 2 to Level 2+ and Level 3 ADAS capabilities that require more powerful compute and more sensing redundancy. NVIDIA's USD 14 billion automotive design win backlog and Qualcomm's USD 45 billion automotive pipeline both reflect the scale of automaker commitment to ADAS semiconductor investment over the coming years.

Growth in AI and High-Performance Computing for Vehicles

The deployment of large AI models for autonomous driving perception, prediction, and planning in vehicles requires semiconductor compute platforms that are orders of magnitude more powerful than the microcontrollers that have historically dominated automotive semiconductor content. NVIDIA's DRIVE Orin system-on-chip, which provides 254 TOPS of AI compute in a single package qualified to automotive functional safety standards, and its successor DRIVE Thor targeting 2,000 TOPS, represent the performance level required for high-level autonomous driving. According to NVIDIA's fiscal year 2025 results, automotive segment revenue grew to approximately USD 1.7 billion and the company's disclosed automotive design win pipeline reaches USD 14 billion over the coming years. This AI compute requirement creates a new and very high-value tier of automotive semiconductor content that grows steeply with autonomous driving capability level and is expected to be one of the highest-growth categories in the automotive semiconductor market through the forecast period.

Expansion of EV Power Electronics (SiC & GaN)

Silicon carbide and gallium nitride power devices are enabling a new generation of EV power electronics with higher efficiency, higher switching frequency, and smaller size than silicon-based alternatives, creating significant new revenue opportunities for power semiconductor companies willing to invest in the manufacturing technology. According to STMicroelectronics' 2025 Annual Report, the company is investing heavily in SiC capacity. Infineon has disclosed multi-year SiC supply agreements totaling billions of euros in committed automotive revenue in its 2025 investor presentations. The GaN opportunity is growing particularly in on-board charger applications where GaN's very high switching frequency enables smaller and lighter charger designs that improve vehicle packaging flexibility and reduce total system cost, creating adoption momentum across multiple OEM charger programs scheduled for launch in the 2025 to 2027 timeframe.

By Component Type: In 2026, MCUs to Hold the Largest Share

Based on component type, the global automotive semiconductor market is segmented into microcontrollers, logic ICs and processors (application processors and AI/HPC chips), power semiconductors (IGBT, SiC, and GaN), analog ICs, memory devices (DRAM and NAND), sensors (image, radar, LiDAR, and MEMS), and connectivity ICs. In 2026, the microcontrollers segment is expected to account for the largest share of the global automotive semiconductor market. MCUs are the most pervasive semiconductor device in automotive applications, present in every ECU from simple body control modules to complex transmission controllers and battery management systems, with each vehicle containing dozens to over one hundred individual MCU chips. The very large unit volumes of automotive MCUs, combined with the vehicle production base of approximately 94 million units annually, make this the largest segment by total revenue. Renesas, NXP, Infineon, STMicroelectronics, and Microchip Technology collectively dominate the automotive MCU market, and according to Renesas's 2025 results, its automotive microcontroller business remains the foundation of its revenue despite growing diversification into higher-performance application processors.

However, the power semiconductors segment, particularly silicon carbide devices, is projected to register the highest CAGR during the forecast period. The rapid growth of 800-volt EV architecture adoption, the very large SiC content per vehicle relative to conventional silicon, and the strong supply agreement pipelines disclosed by Infineon, STMicroelectronics, and onsemi in their 2025 communications collectively confirm SiC as the highest-growth product category in automotive semiconductors through the forecast period.

By Application: In 2026, Powertrain Systems to Hold the Largest Share

Based on application, the global automotive semiconductor market is segmented into powertrain systems (ICE ECUs and EV powertrain), ADAS, infotainment and digital cockpit, body electronics, safety and security systems, and connectivity and telematics. In 2026, the powertrain systems segment is expected to account for the largest share of the global automotive semiconductor market. Engine management and EV powertrain applications together represent the highest-value and most technically demanding semiconductor applications in the vehicle, combining the very large installed base of ICE powertrain control with the fast-growing and high-content EV powertrain semiconductor requirements. The powertrain application is where the SiC power semiconductor opportunity is concentrated, and the growing EV share of vehicle production is expanding the total powertrain semiconductor content per vehicle significantly.

However, the ADAS segment is projected to register the highest CAGR during the forecast period. The combination of EU General Safety Regulation ADAS mandates effective July 2024, the growing commercial deployment of Level 2+ autonomous driving features, and the very large disclosed ADAS semiconductor design win pipelines from NVIDIA and Qualcomm collectively indicate that ADAS is the fastest-growing semiconductor application category in the automotive market through the forecast period. Mobileye's 2025 revenue disclosures confirmed strong growth in its EyeQ ADAS processor shipments across European and global automaker customers.

Automotive Semiconductor Market by Region: Asia-Pacific Leading by Share, Europe by Growth

Based on geography, the global automotive semiconductor market is segmented into Asia-Pacific, North America, Europe, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global automotive semiconductor market. The region's dominance reflects China's position as both the world's largest vehicle market and the world's largest EV market. The China Passenger Car Association's 2025 data shows over 12 million NEV sales in China in 2024, representing over 40% of domestic new vehicle sales and creating the world's most concentrated source of automotive semiconductor demand for EV-specific components including SiC inverters, BMS ICs, and power management semiconductors. Japan hosts the world's leading automotive MCU and power semiconductor companies including Renesas, Rohm, and Fuji Electric, alongside major automakers Toyota, Honda, and their Tier-1 suppliers. South Korea's Samsung Semiconductor is a major supplier of automotive memory devices, and Taiwan's semiconductor manufacturing ecosystem including TSMC is foundry supplier for a large proportion of leading-edge automotive logic and connectivity chips. India's growing automotive production and the country's domestic EV ambitions are creating emerging additional demand, with the Society of Indian Automobile Manufacturers' 2025 data confirming India's vehicle production exceeding 31 million units in fiscal year 2025. The region also contains the major OSAT packaging facilities in Malaysia, Singapore, and Thailand that package and test a significant proportion of the world's automotive semiconductor production.

However, the European automotive semiconductor market is expected to grow at the fastest CAGR during the forecast period. Europe's growth is driven by two converging forces: the very large wave of EV model launches by European automakers responding to the EU's 2035 effective ICE ban, each requiring SiC inverters, BMS semiconductors, and high-performance ADAS compute platforms, and the home base of the three largest automotive semiconductor companies globally by automotive revenue, namely Infineon Technologies, NXP Semiconductors, and STMicroelectronics. Infineon's 2025 results showing above-average automotive segment growth driven by SiC and automotive microcontroller demand, NXP's strong S32 processor and radar sensor momentum noted in its 2025 communications, and STMicroelectronics' major SiC capacity investment announced in its 2025 Annual Report collectively confirm Europe as the most dynamically growing automotive semiconductor market. The EU's European Chips Act, which provides substantial funding for semiconductor manufacturing capacity expansion in Europe, is also supporting domestic automotive chip supply chain development.

North America is a large and technically advanced automotive semiconductor market, with the United States home to major fabless automotive chip companies including NVIDIA, Qualcomm, Texas Instruments, Analog Devices, and Microchip Technology, whose combined automotive revenues represent a significant share of the global market. The U.S. CHIPS and Science Act is driving domestic semiconductor manufacturing investment, with TSMC, Samsung, and Intel Foundry establishing or expanding U.S. wafer fabrication facilities that will supply automotive chips to U.S.-based automakers meeting IRA domestic content requirements. Mexico's very large automotive assembly industry, producing vehicles for U.S. export, generates significant semiconductor consumption through the Tier-1 supply chain embedded in northern Mexico's automotive corridor.

The automotive semiconductor market is served by traditional automotive semiconductor specialists that have built decades of expertise in automotive-grade reliability and functional safety qualification, alongside technology-company entrants from the data center and mobile markets bringing high-performance compute architectures into the vehicle. Competition is based on product performance specifications, automotive functional safety certification credentials, supply reliability and longevity commitments, system-level application expertise, and increasingly on AI compute performance per watt for ADAS and autonomous driving applications.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, design win pipelines, manufacturing strategies, and recent strategic developments. Some of the key players operating in the global automotive semiconductor market include Infineon Technologies AG (Germany), NXP Semiconductors N.V. (Netherlands), STMicroelectronics N.V. (Switzerland/France), Texas Instruments Incorporated (U.S.), Renesas Electronics Corporation (Japan), NVIDIA Corporation (U.S.), Qualcomm Incorporated (U.S.), ON Semiconductor Corporation/onsemi (U.S.), Analog Devices Inc. (U.S.), Microchip Technology Inc. (U.S.), Broadcom Inc. (U.S.), Samsung Electronics Co. Ltd. (South Korea), Intel Corporation (U.S.), MediaTek Inc. (Taiwan), and Rohm Semiconductor (Japan), among others.

The global automotive semiconductor market is expected to reach USD 148.6 billion by 2036 from an estimated USD 72.4 billion in 2026, at a CAGR of 7.4% during the forecast period 2026-2036.

In 2026, the microcontrollers segment is expected to hold the largest share of the global automotive semiconductor market, driven by MCUs being present in every ECU across every vehicle type and representing the highest total unit volume of any automotive semiconductor category.

The power semiconductors segment, particularly silicon carbide devices, is expected to register the highest CAGR during the forecast period, driven by the rapid adoption of 800-volt EV architecture that requires SiC inverters and chargers with significantly higher per-vehicle content value than conventional silicon-based alternatives.

In 2026, the powertrain systems segment is expected to hold the largest share of the global automotive semiconductor market, reflecting the very large combined semiconductor content of both ICE powertrain control systems and the fast-growing EV powertrain applications.

The ADAS segment is projected to register the highest CAGR during the forecast period, driven by EU General Safety Regulation mandates requiring ADAS as standard equipment on all new vehicles from July 2024, and by the very large automotive design win pipelines disclosed by NVIDIA and Qualcomm for their ADAS compute platforms.

The market is primarily driven by vehicle electrification requiring very large SiC and power management semiconductor content per EV, and by the regulatory and commercial expansion of ADAS capability across all vehicle segments requiring high-performance compute, sensor, and radar semiconductor content per vehicle.

Key players are Infineon Technologies AG (Germany), NXP Semiconductors N.V. (Netherlands), STMicroelectronics N.V. (Switzerland/France), Texas Instruments Incorporated (U.S.), Renesas Electronics Corporation (Japan), NVIDIA Corporation (U.S.), Qualcomm Incorporated (U.S.), ON Semiconductor/onsemi (U.S.), Analog Devices Inc. (U.S.), Microchip Technology Inc. (U.S.), Broadcom Inc. (U.S.), Samsung Electronics Co. Ltd. (South Korea), Intel Corporation (U.S.), MediaTek Inc. (Taiwan), and Rohm Semiconductor (Japan), among others.

Europe is expected to register the highest growth rate in the global automotive semiconductor market during the forecast period 2026-2036, driven by European automakers' large EV launch programs in response to the EU's 2035 ICE sales ban and by the home base of Infineon, NXP, and STMicroelectronics, the three largest automotive semiconductor companies globally.

Published Date: Jan-2025

Published Date: Nov-2024

Published Date: Sep-2024

Published Date: Aug-2024

Published Date: Jun-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates