Resources

About Us

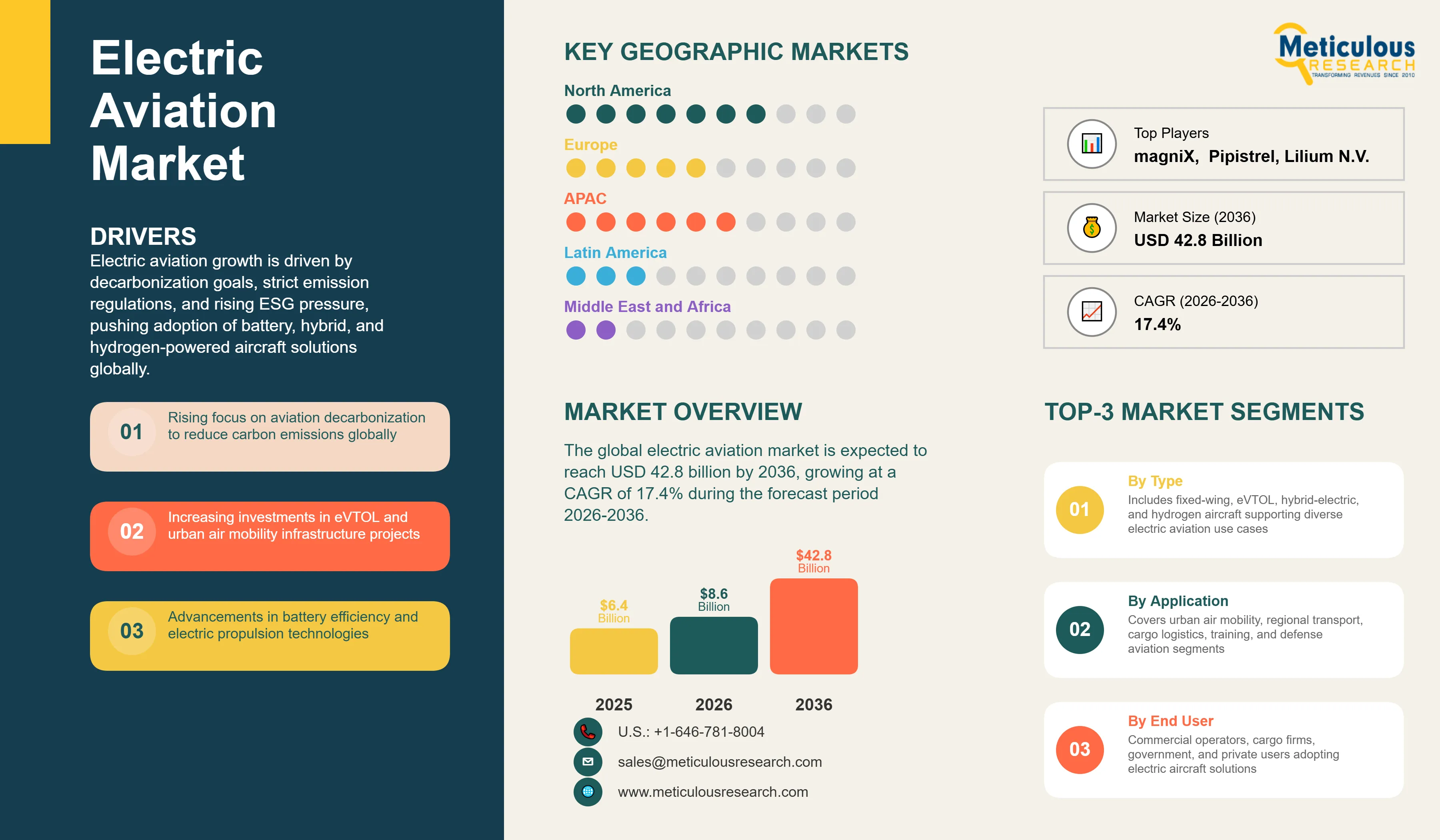

The global electric aviation market was valued at USD 6.4 billion in 2025. This market is expected to reach USD 42.8 billion by 2036 from an estimated USD 8.6 billion in 2026, growing at a CAGR of 17.4% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

The global electric aviation market covers the design, development, manufacturing, certification, and commercial operation of aircraft powered wholly or substantially by electric propulsion systems, including fully battery-electric fixed-wing aircraft and eVTOL platforms, hybrid-electric aircraft combining battery-electric and conventional propulsion for extended range, and hydrogen-electric aircraft utilizing fuel cell or direct hydrogen combustion propulsion. The market encompasses the aircraft platforms themselves together with the electric propulsion systems, battery packs, power electronics, charging infrastructure, and vertiport ground infrastructure that constitute the complete electric aviation ecosystem from component supply through commercial operation.

The growth of the global electric aviation market is primarily driven by the aviation industry's urgent decarbonization imperative in the face of growing regulatory pressure and investor ESG expectations, as aviation accounts for approximately 2.5% of global CO2 emissions and faces the most technically challenging decarbonization pathway of any major transport sector. The FAA and EASA certification progress on eVTOL aircraft, with Joby Aviation, Archer Aviation, and Vertical Aerospace advancing through the certification process toward anticipated type certificate issuance in the 2025 to 2027 timeframe, is translating the electric aviation technology pipeline into near-term commercial product launches that are creating the first significant revenue generation phase of the market. The extraordinary level of venture capital and strategic investment in eVTOL and electric aircraft developers, with cumulative investment exceeding USD 10 billion across the sector, is funding the technology development and certification programs required to bring commercial electric aviation products to market at scale.

Two significant opportunities are shaping the market's long-term trajectory. The development of hybrid-electric aircraft for regional travel, combining battery-electric power for takeoff and initial climb with conventional engine power for cruise, represents the most commercially actionable near-term pathway for extending electric aviation beyond the short-range and urban air mobility applications addressable with current battery technology, enabling the development of competitive regional air transport products in the 100 to 500 kilometer range that represent the largest commercial opportunity in the electric aviation market. The expansion of dedicated electric cargo and logistics aircraft, addressing the exploding last-mile and middle-mile air cargo demand generated by e-commerce growth with zero-emission electric aircraft optimized for freight transport rather than passenger comfort, represents a commercially compelling application where the operating economics of electric propulsion and the logistics industry's decarbonization commitments are creating strong operator demand ahead of passenger air taxi certification timelines.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 42.8 Billion |

|

Market Size in 2026 |

USD 8.6 Billion |

|

Market Size in 2025 |

USD 6.4 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 17.4% |

|

Dominating Aircraft Type |

Fixed-Wing Electric Aircraft |

|

Fastest Growing Aircraft Type |

Rotary-Wing Electric Aircraft (eVTOL) |

|

Dominating Propulsion Type |

Fully Electric Propulsion |

|

Fastest Growing Propulsion Type |

Hydrogen-Electric Propulsion |

|

Dominating Range |

Short Range (<100 km) |

|

Fastest Growing Range |

Medium Range (100-500 km) |

|

Dominating Application |

Urban Air Mobility (Air Taxis) |

|

Fastest Growing Application |

Cargo & Logistics |

|

Dominating End User |

Commercial Operators |

|

Fastest Growing End User |

Cargo Operators |

|

Dominating Seating Capacity |

1-2 Passengers |

|

Fastest Growing Seating Capacity |

7-10 Passengers |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

eVTOL Certification Progress Approaching Commercial Launch

The progressive advancement of eVTOL aircraft developers through the FAA and EASA type certification processes represents the most commercially consequential near-term trend in the electric aviation market, as certification issuance will transform the market from a venture-backed development stage into a revenue-generating commercial aviation segment for the first time. Joby Aviation's five-seat eVTOL has completed its Stage 4 certification basis agreement with the FAA and has progressed further in the Part 135 air carrier certification process than any other eVTOL developer, positioning the company for commercial launch operations as early as 2026. Archer Aviation's Midnight eVTOL completed its initial FAA airworthiness inspection and is advancing through flight test milestones, with United Airlines committed to purchasing up to USD 1 billion of Archer aircraft. Vertical Aerospace's VX4 in the UK is progressing under EASA certification, targeting the European urban air mobility market with strong airline commitments from American Airlines and Virgin Atlantic.

The FAA's Special Federal Aviation Regulation for Powered-Lift Aircraft, finalized in 2023, established the regulatory framework for eVTOL certification based on performance-based standards rather than prescriptive design rules, providing a clear and technology-neutral pathway for diverse eVTOL configurations to achieve type certification. EASA's Special Condition for VTOL category certification has been accepted by eVTOL developers as providing equivalent clarity for European market access. The convergence of near-complete certification programs at multiple eVTOL developers with committed airline and air taxi operator customers and defined vertiport infrastructure programs in multiple cities is creating the commercial ecosystem conditions for initial eVTOL service launch within the forecast period.

Growing Electric Cargo Aviation as a Near-Term Commercial Pathway

The development of dedicated electric cargo aircraft as a commercially near-term application of electric aviation technology is emerging as a significant market opportunity that may achieve commercial scale ahead of passenger eVTOL services in several markets. Eviation Aircraft's Alice all-electric commuter aircraft has been acquired by DHL for cargo conversion deployment, representing a commitment by a major logistics operator to electric aviation for freight applications. Natilus is developing a 3.8-ton payload blended wing body electric cargo aircraft targeting short-haul freight routes. Beta Technologies has built its electric aircraft development program around cargo delivery for UPS, with a firm commitment from UPS for up to 150 aircraft, and Joby Aviation's acquisition of Uber Elevate includes air cargo delivery alongside passenger air taxi development.

The logistics industry's decarbonization pressures, the favorable operating economics of electric propulsion for short-haul cargo cycles with predictable route distances and ground charging intervals, and the lower regulatory certification burden for cargo aircraft compared with passenger-carrying eVTOL platforms are creating a commercially compelling pathway for electric cargo aviation that several operators and developers are pursuing ahead of the longer certification timeline required for commercial passenger air taxi operations. The growth of e-commerce-driven air cargo demand at regional distribution hub level is creating specific route profiles, including overnight hub-to-spoke freight cycles with distances of 50 to 300 kilometers, that align well with the range capabilities of first-generation battery-electric aircraft platforms.

Hybrid-Electric Propulsion as the Bridge to Regional Electric Aviation

The development of hybrid-electric aircraft architectures that combine battery-electric power with conventional turbine or piston engine power is attracting significant investment and development activity as the most credible near-term pathway for extending the commercial range of electric aviation beyond the 100 to 150 kilometer envelope achievable with current battery energy density, toward the regional aviation market of 100 to 500 kilometer routes where the largest commercial opportunity for electric aviation lies. Parallel hybrid systems that can draw on both battery electric and conventional engine power simultaneously during high-power-demand phases including takeoff and climb, reverting to conventional propulsion only for cruise, can achieve 20 to 50% reduction in fuel consumption and emissions relative to fully conventional aircraft while using battery technology available today. VoltAero's Cassio hybrid-electric aircraft, Zunum Aero's regional hybrid-electric program, and the hybrid-electric developments within Airbus's E-Fan X program all represent advancing platforms targeting the regional hybrid-electric aviation opportunity.

The commercial appeal of hybrid-electric regional aircraft is reinforced by the aviation industry's progressive regulatory pressure toward emission reduction on short-haul routes, with the UK's Jet Zero Strategy and the EU's Fit for 55 aviation provisions creating market conditions that favor low-emission aircraft on the domestic and intra-European short-haul routes where hybrid-electric aircraft are most competitive. Regional airline operators including Air New Zealand, easyJet, and smaller regional carriers are actively evaluating hybrid-electric aircraft procurement programs as they develop decarbonization roadmaps for their domestic route networks, creating a commercial demand signal that is motivating hybrid-electric aircraft developer investment and certification program acceleration.

Increasing Focus on Sustainable Aviation and Decarbonization

The primary driver of the global electric aviation market is the aviation industry's urgent and growing pressure to decarbonize its operations in response to climate policy commitments, regulatory requirements, and the increasing cost of carbon under emissions trading systems that are making the environmental and financial case for electric aviation transition increasingly compelling for operators and investors. Aviation's contribution to global warming encompasses not only its approximately 2.5% share of global CO2 emissions but also additional non-CO2 climate effects from high-altitude contrail cirrus formation that potentially doubles its effective climate impact, making aviation one of the most consequential sectors for decarbonization despite its relatively modest CO2 share. The International Civil Aviation Organization's Long-Term Aspirational Goals framework targeting net-zero carbon aviation by 2050, the EU Emissions Trading System's inclusion of intra-EU aviation, and national net-zero commitments with aviation sector decarbonization plans in the UK, France, Netherlands, and Scandinavia are creating the regulatory and policy environment that is incentivizing airlines, aircraft manufacturers, and investors to accelerate electric aviation development and adoption.

Rising Investment in Urban Air Mobility (UAM)

The extraordinary level of investment flowing into the urban air mobility sector, with eVTOL and electric aircraft developers collectively raising over USD 10 billion in venture capital, strategic investment, and public market capital through 2024, is the primary commercial development driver of the electric aviation market, funding the technology development, flight test programs, and certification activities required to bring commercial eVTOL products to market. Infrastructure investment in vertiport networks from companies including Skyports, Urban-Air Port, and Ferrovial, and committed airline and air taxi operator customer agreements from United Airlines, American Airlines, Delta Air Lines, American Airlines, and Virgin Atlantic for eVTOL aircraft from Joby, Archer, Vertical Aerospace, and Lilium collectively demonstrate that the commercial ecosystem required for urban air mobility service launch is being assembled in parallel with aircraft development programs. The UAM market is projected to develop first in high-density urban markets where road congestion creates the time-saving value proposition that justifies premium air taxi pricing, including Los Angeles, San Francisco, New York, London, Singapore, and Dubai, with each market representing a defined near-term commercial launch opportunity for leading eVTOL operators.

Development of Hybrid-Electric Aircraft for Regional Travel

The commercial development of hybrid-electric aircraft capable of serving regional routes in the 100 to 500 kilometer range represents the largest total addressable market opportunity in the electric aviation landscape, as regional air transport represents a multi-hundred-billion-dollar global market that is poorly served by the current generation of aircraft and is most immediately addressable by hybrid-electric platforms that can reduce operating costs and emissions substantially relative to current regional jets and turboprops without requiring battery energy density improvements beyond what current lithium-ion technology can provide. The hybrid-electric regional aircraft opportunity is reinforced by the structural economics of regional aviation, where the high fuel and maintenance costs of current regional aircraft relative to their revenue-generating capacity create strong operator incentives to adopt lower operating cost electric or hybrid-electric alternatives when certified platforms become available. VoltAero, Airbus, Rolls-Royce, and multiple startup developers are pursuing hybrid-electric regional aircraft programs targeting initial certification and commercial entry in the late 2020s to early 2030s, representing a large and well-funded development pipeline that is translating the opportunity into advancing commercial programs.

Growth in Electric Cargo and Logistics Aircraft

The development of electric cargo aircraft represents a commercially near-term and operationally compelling application of electric aviation technology that is attracting significant operator commitment and aircraft developer investment as a pathway to revenue generation ahead of the longer certification timeline required for passenger air taxi operations. Logistics operators including UPS, DHL, and FedEx have made firm commitments to electric aircraft procurement, motivated by their corporate net-zero emission commitments, the documented operating cost advantages of electric propulsion for short-haul predictable route operations, and the public relations and ESG positioning value of zero-emission air cargo delivery. The specific operational requirements of cargo logistics, including predictable route distances, ground charging intervals at hub facilities, lower passenger safety certification standards, and the high utilization cycles that maximize the return on battery investment, create a favorable operating context for electric aircraft that may make cargo logistics the first large-scale commercial deployment environment for electric aviation ahead of passenger air taxi services.

By Aircraft Type: In 2026, Fixed-Wing Electric Aircraft to Dominate

Based on aircraft type, the global electric aviation market is segmented into fixed-wing electric aircraft, rotary-wing electric aircraft, hybrid-electric aircraft, hydrogen-electric aircraft, and other electric aircraft. In 2026, the fixed-wing electric aircraft segment is expected to account for the largest share of the global electric aviation market. The large share of this segment is attributed to fixed-wing electric aircraft representing the most commercially mature and operationally deployed category of electric aviation, with aircraft including the Pipistrel Velis Electro receiving the first EASA type certificate for a fully electric aircraft in 2020, Eviation's Alice entering flight testing, and a large installed base of electric light sport aircraft in training and recreational applications that represents established revenue generation. The fixed-wing format's superior aerodynamic efficiency relative to rotary-wing designs enables the longest range achievable with current battery technology, making fixed-wing platforms the most commercially deployable category for the near-term flight training and light cargo operations that represent the initial commercial market.

However, the rotary-wing electric aircraft segment including eVTOL platforms is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the approaching type certification and commercial service launch of leading eVTOL platforms including Joby Aviation, Archer Aviation, and Vertical Aerospace, the extraordinary level of investment and commercial partnership activity generating strong demand signal for urban air mobility services, and the large and rapidly growing commercial market represented by urban air taxi operations in high-density cities where eVTOL's vertical takeoff capability enables operations from urban vertiports without conventional airport infrastructure.

By Propulsion Type: In 2026, Fully Electric Propulsion to Hold the Largest Share

Based on propulsion type, the global electric aviation market is segmented into fully electric propulsion, hybrid-electric propulsion, and hydrogen-electric propulsion. In 2026, the fully electric propulsion segment is expected to account for the largest share of the global electric aviation market. The dominance of fully electric propulsion reflects the concentration of both the current installed base of electric aircraft, comprising the large population of battery-electric light sport and flight training aircraft, and the near-term commercial pipeline, comprising the eVTOL platforms approaching certification, in the fully electric propulsion category. The design simplicity, zero direct emission operation, and lower maintenance complexity of fully electric propulsion systems relative to hybrid alternatives make them the preferred architecture for short-range applications where battery range limitations are not operationally constraining.

However, the hydrogen-electric propulsion segment is projected to register the highest CAGR during the forecast period. This growth is driven by the significant investment by Airbus in its ZEROe hydrogen aircraft programs targeting commercial service entry in the mid-2030s, the development of hydrogen fuel cell propulsion systems by ZeroAvia and Universal Hydrogen for retrofit and new aircraft applications, and the aviation industry's recognition that hydrogen is the most credible pathway for decarbonizing medium and long-range aviation beyond the range limitations that battery-electric technology imposes.

By Range: In 2026, Short Range to Hold the Largest Share

Based on range, the global electric aviation market is segmented into short range (below 100 km), medium range (100 to 500 km), and long range (above 500 km). In 2026, the short range segment is expected to account for the largest share of the global electric aviation market. Short-range operations below 100 kilometers represent the primary application domain for current-generation battery-electric aircraft, encompassing urban air mobility routes between city-center vertiports and airports, inter-island and coastal short-hop routes, flight training operations, and aerial survey and inspection missions where the energy storage capacity of current lithium-ion battery technology provides adequate range without requiring hybrid propulsion augmentation. The entire eVTOL commercial launch pipeline is focused on this range segment, reinforcing its near-term market dominance.

However, the medium range segment (100 to 500 km) is projected to register the highest CAGR during the forecast period. This growth is driven by the advancing development of hybrid-electric regional aircraft specifically targeting the 100 to 500 kilometer regional air transport market, the improving energy density of next-generation lithium-ion and solid-state battery technology progressively extending the fully electric range envelope toward 200 to 300 kilometers, and the very large commercial opportunity represented by regional aviation routes in this distance band that are underserved by current aircraft economics.

By Application: In 2026, Urban Air Mobility to Hold the Largest Share

Based on application, the global electric aviation market is segmented into urban air mobility, regional transportation, cargo and logistics, military and defense, training aircraft, and others. In 2026, the urban air mobility segment is expected to account for the largest share of the global electric aviation market. UAM represents the highest-investment and most commercially active application category in electric aviation, driven by the concentration of eVTOL developer activity and commercial partner commitments around air taxi services in major urban markets, the advanced state of certification programs for UAM-configured eVTOL platforms, and the large projected addressable market for air taxi services in congested urban environments where time savings justify premium pricing. Joby Aviation's partnership with Delta Air Lines for airport connection services, Archer's partnership with United Airlines and Alaska Airlines, and Vertical Aerospace's orders from American Airlines and Virgin Atlantic collectively represent the commercial foundation of the near-term UAM market.

However, the cargo and logistics segment is projected to register the highest CAGR during the forecast period. This growth is driven by confirmed electric aircraft orders from major logistics operators including UPS's commitment to Beta Technologies aircraft and DHL's acquisition of Eviation Alice cargo aircraft, the favorable operating economics of electric propulsion for the predictable short-haul cargo routes that define hub-to-spoke logistics operations, and the strong corporate sustainability commitments of global logistics companies that are creating non-discretionary demand for zero-emission air freight solutions as airline operators face increasing carbon cost exposure on their aviation operations.

By End User: In 2026, Commercial Operators to Hold the Largest Share

Based on end user, the global electric aviation market is segmented into commercial operators, government and defense, cargo operators, and private and recreational users. In 2026, the commercial operators segment is expected to account for the largest share of the global electric aviation market. Commercial aviation operators including the airline and air taxi companies that will operate eVTOL urban air mobility services, commuter airline operators deploying electric aircraft on short-haul scheduled routes, and charter and air tour operators using electric aircraft for scenic and short-hop services represent the primary revenue-generating customer base for electric aircraft manufacturers. The very large pre-order books that eVTOL developers have accumulated from airline partners, including Joby's Delta partnership, Archer's United and Alaska orders, and Vertical Aerospace's American Airlines and Virgin Atlantic commitments, demonstrate the commercial operator segment's leading role in driving the market's commercial development.

However, the cargo operators segment is projected to register the highest CAGR during the forecast period. This growth is driven by the confirmed aircraft purchase commitments from UPS, DHL, and Amazon Air as they invest in electric cargo aircraft to reduce the carbon footprint of their air freight operations, the favorable certification pathway for cargo aircraft compared with passenger-carrying platforms, and the strong economic incentive for logistics operators to reduce fuel cost exposure on short-haul cargo routes through electrification.

By Seating Capacity: In 2026, 1-2 Passengers to Hold the Largest Share

Based on seating capacity, the global electric aviation market is segmented into 1 to 2 passengers, 3 to 6 passengers, 7 to 10 passengers, and more than 10 passengers. In 2026, the 1 to 2 passengers segment is expected to account for the largest share of the global electric aviation market. The dominance of the 1 to 2 passenger category reflects the large installed base of single and dual-seat electric light sport and flight training aircraft including the Pipistrel Velis Electro and equivalent platforms from PC-Aero, Bye Aerospace, and Aero Electric Aircraft Corporation that have established the earliest commercial deployments of electric aviation technology in the flight training and recreational flying markets. Single-seat and dual-seat electric aircraft are commercially deployed today in substantially larger numbers than any other seating category and represent the most commercially established revenue base in the market.

However, the 7 to 10 passengers segment is projected to register the highest CAGR during the forecast period. This growth is driven by the commercial focus of the most capital-intensive and commercially advanced eVTOL programs on configurations in the 4 to 6 passenger range that most closely correspond to the 7 to 10 passenger category boundary, the development of electric commuter aircraft targeting the regional shuttle market, and the emerging electric helicopter market addressing offshore energy support, medical evacuation, and premium business transport applications that typically require 6 to 8 passenger capacity.

Electric Aviation Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global electric aviation market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global electric aviation market. The largest share of this region is mainly due to the United States' position as the home of the majority of the world's leading eVTOL and electric aircraft developers, including Joby Aviation, Archer Aviation, Beta Technologies, Eviation Aircraft, Wisk Aero, Overair, and magniX, whose development programs, flight test activities, and certification engagements with the FAA generate the majority of current market revenue in the form of aircraft development spending, component procurement, and early aircraft deliveries. The FAA's development of the Powered-Lift Special Federal Aviation Regulation providing the certification pathway for eVTOL aircraft, combined with the large and congested metropolitan aviation markets of Los Angeles, San Francisco, New York, and Miami that represent the primary near-term commercial launch environments for urban air mobility services, positions the United States as the primary initial commercial deployment market for electric aviation. The substantial venture capital ecosystem of Silicon Valley and the broader U.S. technology investment community, which has provided the majority of the USD 10 billion-plus cumulative investment in the electric aviation sector, further reinforces North America's market leadership position.

However, the Asia-Pacific electric aviation market is expected to grow at the fastest CAGR during the forecast period. The region's rapid growth is driven by China's national electric aviation development programs supporting domestic eVTOL and electric aircraft companies including EHang, AutoFlight, and Aerofugia, with EHang's EH216 having received type certification from the Civil Aviation Administration of China in 2023 as the world's first eVTOL to achieve national type certification for commercial passenger operations. Japan's Society of Automotive Engineers of Japan eVTOL certification program and the Japanese government's ambitious UAM roadmap targeting commercial air taxi services launch by 2025 are driving significant private and public investment in domestic eVTOL development and infrastructure. Singapore's Civil Aviation Authority has established an advanced air mobility development framework and the city-state's compact geography and severe road congestion make it a natural early adopter market for urban air mobility services. India's nascent electric aviation market is supported by growing investor interest in air mobility solutions for its congested megacities and the Civil Aviation Ministry's Digi Yatra digital aviation platform that provides the digital infrastructure layer for future urban air mobility integration.

Europe represents a highly active electric aviation development market, anchored by Vertical Aerospace in the UK, Lilium in Germany, Volocopter in Germany, and the electric aviation programs of Airbus including E-Fan X hybrid-electric research and the ZEROe hydrogen aircraft concept program. The European Union's Green Deal aviation provisions, the UK's Jet Zero Strategy, and the advanced air mobility programs of multiple European aviation authorities are creating a favorable regulatory and policy environment for electric aviation development and early commercial operations. The Middle East and Africa market is experiencing growing interest in electric aviation, with Dubai's RTA and civil aviation authority establishing an air mobility regulatory framework and Abu Dhabi's demonstration of eVTOL trial flights, positioning the UAE as a leading Middle East electric aviation adoption market motivated by its smart city development ambitions and aviation technology leadership aspirations.

The global electric aviation market is characterized by a highly dynamic competitive landscape spanning dedicated eVTOL startups pursuing urban air mobility certification, established aerospace OEMs integrating electric propulsion into new aircraft programs, and electric propulsion system and component developers. Competition is focused on certification progress, battery and propulsion technology performance, commercial partner relationships, and the operational economics that will determine viability of commercial service at scale.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' aircraft development programs, certification progress, commercial partnerships, and key strategic developments. Some of the key players operating in the global electric aviation market include Joby Aviation Inc. (U.S.), Lilium N.V. (Germany), Archer Aviation Inc. (U.S.), Eviation Aircraft Ltd. (Israel/U.S.), Vertical Aerospace Ltd. (U.K.), Beta Technologies (U.S.), Airbus SE (Netherlands), Boeing Company (U.S.), Embraer S.A./Eve Air Mobility (Brazil), Pipistrel d.o.o. (Slovenia), Rolls-Royce Holdings plc (U.K.), Honeywell International Inc. (U.S.), magniX (Australia/U.S.), Wright Electric Inc. (U.S.), and VoltAero S.A.S. (France), among others.

The global electric aviation market is expected to reach USD 42.8 billion by 2036 from an estimated USD 8.6 billion in 2026, at a CAGR of 17.4% during the forecast period 2026-2036.

In 2026, the fixed-wing electric aircraft segment is expected to hold the largest share of the global electric aviation market, driven by the established commercial deployment of battery-electric light sport and flight training aircraft and the more mature certification status of fixed-wing platforms relative to eVTOL configurations.

The rotary-wing electric aircraft segment (eVTOL) is expected to register the highest CAGR during the forecast period 2026-2036, driven by the approaching type certification and commercial service launch of leading eVTOL platforms and the extraordinary investment and commercial partnership activity concentrated in the urban air mobility application.

In 2026, the urban air mobility segment is expected to hold the largest share of the global electric aviation market, reflecting the concentration of investment, certification activity, and commercial partnership commitments in eVTOL air taxi platforms targeting urban operations.

The cargo and logistics segment is projected to register the highest CAGR during the forecast period 2026-2036, driven by firm electric aircraft orders from UPS, DHL, and Amazon Air and the favorable certification pathway and operating economics of electric cargo aircraft relative to passenger-carrying platforms.

The growth of this market is primarily driven by the aviation industry's urgent decarbonization imperative creating structural demand for zero-emission aircraft solutions, and the extraordinary level of venture capital and strategic investment in eVTOL and electric aircraft developers that is funding the technology development and certification programs required to bring commercial electric aviation products to market within the forecast period.

Key players are Joby Aviation Inc. (U.S.), Lilium N.V. (Germany), Archer Aviation Inc. (U.S.), Eviation Aircraft Ltd. (Israel/U.S.), Vertical Aerospace Ltd. (U.K.), Beta Technologies (U.S.), Airbus SE (Netherlands), Boeing Company (U.S.), Embraer S.A./Eve Air Mobility (Brazil), Pipistrel d.o.o. (Slovenia), Rolls-Royce Holdings plc (U.K.), Honeywell International Inc. (U.S.), magniX (Australia/U.S.), Wright Electric Inc. (U.S.), and VoltAero S.A.S. (France), among others.

Asia-Pacific is expected to register the highest growth rate in the global electric aviation market during the forecast period 2026-2036, driven by China's EHang achieving the world's first eVTOL type certification, Japan's government-backed UAM commercialization roadmap, Singapore's advanced air mobility framework, and the large urban air mobility opportunity in the region's densely populated megacities.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Increasing Focus on Sustainable Aviation and Decarbonization

4.2.1.2 Rising Investment in Urban Air Mobility (UAM)

4.2.1.3 Advancements in Battery and Electric Propulsion Technologies

4.2.1.4 Growing Demand for Short-Haul and Regional Air Transport

4.2.2 Restraints

4.2.2.1 Limited Battery Energy Density

4.2.2.2 High Development and Certification Costs

4.2.2.3 Infrastructure Limitations (Charging & Vertiports)

4.2.3 Opportunities

4.2.3.1 Development of Hybrid-Electric Aircraft for Regional Travel

4.2.3.2 Expansion of Air Taxi and Urban Mobility Services

4.2.3.3 Growth in Electric Cargo and Logistics Aircraft

4.2.3.4 Government Incentives for Sustainable Aviation

4.2.4 Challenges

4.2.4.1 Safety and Certification Complexities

4.2.4.2 Battery Lifecycle and Thermal Management Issues

4.3 Technology Landscape

4.3.1 Battery Technologies (Lithium-ion, Solid-State)

4.3.2 Electric Propulsion Systems

4.3.3 Distributed Electric Propulsion (DEP)

4.3.4 Hydrogen-Electric Propulsion (Emerging)

4.3.5 Charging Infrastructure and Energy Management

4.4 Electric Aircraft Architecture (Critical Segmentation)

4.4.1 Fully Electric Aircraft

4.4.2 Hybrid-Electric Aircraft

4.4.3 Electric Vertical Take-Off and Landing (eVTOL) Aircraft

4.4.4 Hydrogen-Electric Aircraft

4.5 Value Chain Analysis

4.5.1 Battery and Component Suppliers

4.5.2 Electric Propulsion System Manufacturers

4.5.3 Aircraft OEMs

4.5.4 Infrastructure Providers (Charging, Vertiports)

4.5.5 Operators and End Users

4.6 Regulatory and Standards Landscape

4.6.1 FAA and EASA Certification Frameworks

4.6.2 Urban Air Mobility Regulations

4.6.3 Environmental and Emission Standards

4.7 Porter's Five Forces Analysis

4.8 Investment and Industry Trends

4.8.1 Venture Capital and Startup Funding

4.8.2 Strategic Partnerships and Collaborations

4.8.3 Government Funding and Incentives

4.9 Cost and Pricing Analysis

4.9.1 Aircraft Cost Structure

4.9.2 Operating Cost Comparison (Electric vs Conventional)

4.9.3 Pricing Models (Aircraft Sales, Air Taxi, Leasing)

5. Electric Aviation Market, by Aircraft Type (Primary Segmentation)

5.1 Introduction

5.2 Fixed-Wing Electric Aircraft

5.2.1 Light Aircraft

5.2.2 Regional Aircraft

5.3 Rotary-Wing Electric Aircraft

5.3.1 Electric Helicopters

5.3.2 eVTOL Aircraft

5.4 Hybrid-Electric Aircraft

5.4.1 Parallel Hybrid Systems

5.4.2 Series Hybrid Systems

5.5 Hydrogen-Electric Aircraft

5.6 Other Electric Aircraft

6. Electric Aviation Market, by Propulsion Type

6.1 Introduction

6.2 Fully Electric Propulsion

6.3 Hybrid-Electric Propulsion

6.4 Hydrogen-Electric Propulsion

7. Electric Aviation Market, by Range

7.1 Introduction

7.2 Short Range (<100 km)

7.3 Medium Range (100-500 km)

7.4 Long Range (>500 km)

8. Electric Aviation Market, by Application

8.1 Introduction

8.2 Urban Air Mobility (Air Taxis)

8.3 Regional Transportation

8.4 Cargo & Logistics

8.5 Military & Defense

8.6 Training Aircraft

8.7 Others

9. Electric Aviation Market, by End User

9.1 Introduction

9.2 Commercial Operators

9.3 Government & Defense

9.4 Cargo Operators

9.5 Private & Recreational Users

10. Electric Aviation Market, by Seating Capacity

10.1 Introduction

10.2 1-2 Passengers

10.3 3-6 Passengers

10.4 7-10 Passengers

10.5 More than 10 Passengers

11. Electric Aviation Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.2.3 Mexico

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Italy

11.3.5 Spain

11.3.6 Netherlands

11.3.7 Sweden

11.3.8 Norway

11.3.9 Switzerland

11.3.10 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 Japan

11.4.3 India

11.4.4 South Korea

11.4.5 Australia

11.4.6 Singapore

11.4.7 Malaysia

11.4.8 Thailand

11.4.9 Indonesia

11.4.10 Vietnam

11.4.11 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Chile

11.5.5 Colombia

11.5.6 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Turkey

11.6.5 Israel

11.6.6 Rest of Middle East & Africa

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Joby Aviation, Inc.

13.2 Lilium N.V.

13.3 Archer Aviation Inc.

13.4 Eviation Aircraft Ltd.

13.5 Vertical Aerospace Ltd.

13.6 Beta Technologies

13.7 Airbus SE

13.8 Boeing Company

13.9 Embraer S.A. (Eve Air Mobility)

13.10 Pipistrel d.o.o.

13.11 Rolls-Royce Holdings plc

13.12 Honeywell International Inc.

13.13 magniX

13.14 Wright Electric, Inc.

13.15 VoltAero S.A.S.

14. Appendix

14.1 Additional Customization

14.2 Related Reports

Published Date: Jun-2024

Published Date: May-2024

Published Date: Apr-2024

Published Date: Feb-2024

Published Date: Jan-2024

Subscribe to get the latest industry updates