Resources

About Us

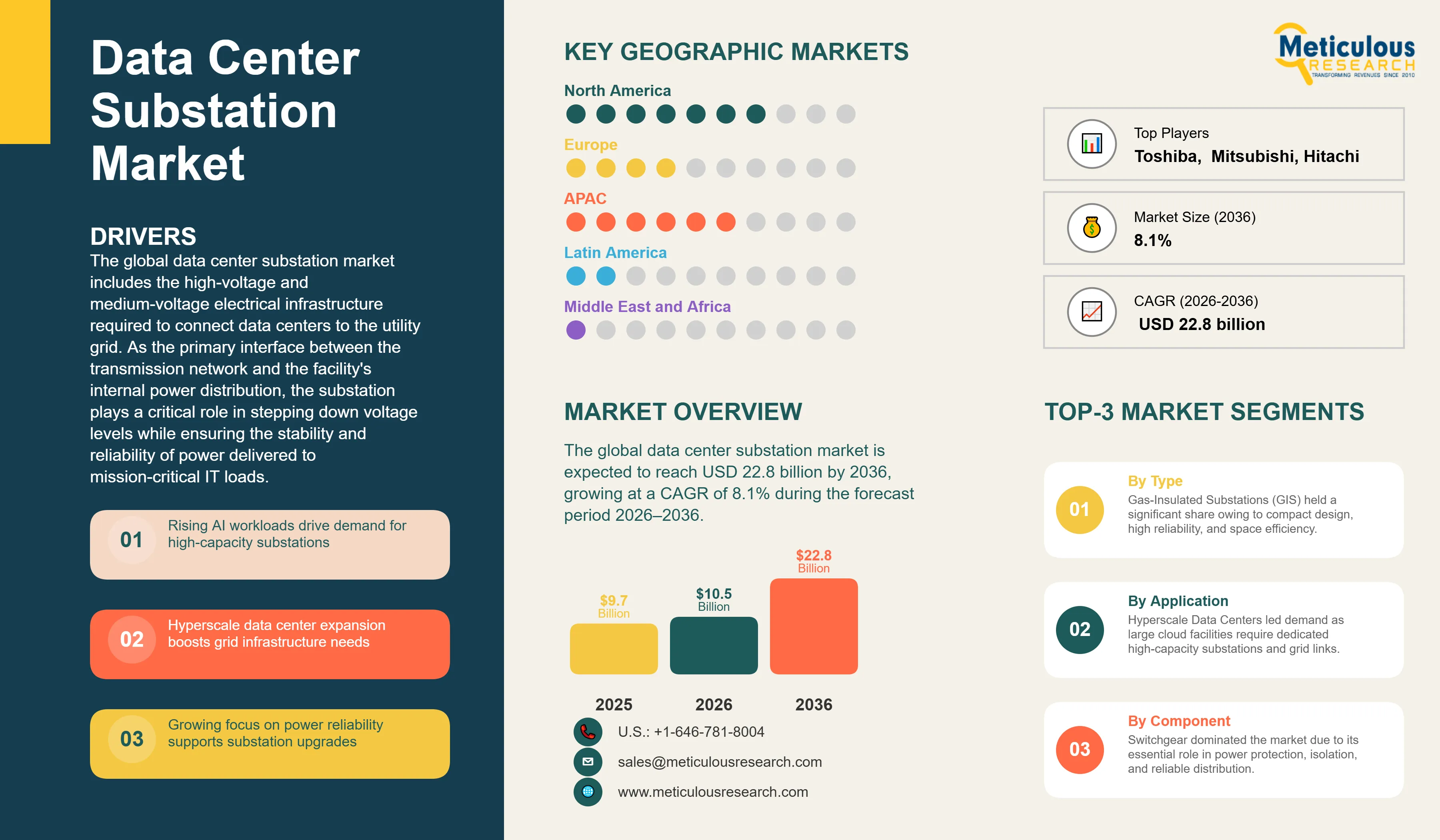

The global data center substation market was valued at USD 10.5 billion in 2026. This market is expected to reach USD 22.8 billion by 2036, growing at a CAGR of 8.1% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global data center substation market includes the high-voltage and medium-voltage electrical infrastructure required to connect data centers to the utility grid. As the primary interface between the transmission network and the facility's internal power distribution, the substation plays a critical role in stepping down voltage levels while ensuring the stability and reliability of power delivered to mission-critical IT loads. The market covers a broad range of components, including power transformers, switchgear, circuit breakers, and advanced automation systems.

According to the International Energy Agency (IEA), global electricity demand from data centers reached approximately 415 TWh in 2024, accounting for nearly 1.5% of global demand, and is projected to approach 945 TWh by 2030 as computational requirements for artificial intelligence and cloud services expand.

The growth of the overall data center substation market is primarily driven by the proliferation of hyperscale data centers, the increasing power density requirements of AI-driven workloads, and the global push for modernized grid infrastructure. As data centers transition from megawatt-scale to gigawatt-scale campuses, the complexity of grid interconnection has escalated, positioning the substation as a strategic asset in the development lifecycle. The U.S. Department of Energy (DOE) reports that data center load growth has tripled over the past decade and is projected to double or triple by 2028, necessitating significant investment in dedicated substation facilities. Furthermore, the rising adoption of Tier III and Tier IV data center standards, which require high levels of redundancy and fault tolerance, is driving the demand for sophisticated substation architectures featuring multiple utility feeds and automated failover systems.

However, the growth of this market is restrained by the high initial capital expenditure and the significant lead times associated with critical electrical components. Procurement cycles for large power transformers have extended to over 100 weeks in certain regions due to shortages in raw materials such as grain-oriented electrical steel and copper. Additionally, the complex regulatory and permitting processes involved in substation siting and grid interconnection can lead to project delays of several years. Maintaining operational safety and cybersecurity in an increasingly digitized environment also presents a persistent challenge for market participants, requiring ongoing investment in advanced protection relays and secure communication protocols.

On the other hand, emerging opportunities in digital substations, grid-interactive data centers, and sustainable insulating technologies are creating new growth avenues. The implementation of the IEC 61850 standard for communication enables real-time monitoring and predictive maintenance, while the integration of renewable energy sources and battery storage systems aligns with the industry's move toward carbon neutrality. The development of SF6-free switchgear and the use of biodegradable ester oils in transformers are expected to attract continued investment, especially in regions with stringent environmental regulations such as Europe.

The key driver for the global data center substation market is the growing demand for power infrastructure to support AI and hyperscale computing. Training large language models (LLMs) and running generative AI applications require rack power densities that can exceed 50-100kW, necessitating high-capacity grid connections. The expansion of hyperscale facilities by major cloud providers is a significant factor; for instance, the industry added 137 new hyperscale facilities in 2024 alone. These facilities often require dedicated 110kV or 220kV substations to interface directly with high-voltage transmission lines, ensuring the necessary load capacity is available for rapid scaling.

Another key driver is the increasing focus on power reliability and grid resilience. Data center operators are investing in advanced substation designs to minimize the risk of utility-side outages. This includes the deployment of redundant transformers and gas-insulated switchgear (GIS) that offer higher reliability and lower maintenance requirements compared to traditional air-insulated options. The modernization of aging electrical grids in developed markets also provides a tailwind, as utilities and data center operators collaborate to build more robust interconnection points that can handle the bi-directional power flows associated with on-site renewable energy integration.

A major restraint in the data center substation market is the extended lead time for critical substation equipment. The global supply chain for power transformers has faced significant pressure, with lead times reaching up to 140 weeks for certain high-voltage units. This is exacerbated by a shortage of specialized manufacturing capacity and raw materials. Furthermore, the high capital cost of constructing a dedicated substation, which can range from USD 20 million to over USD 100 million depending on capacity and voltage, poses a financial barrier for smaller colocation and enterprise operators. The complexity of obtaining grid interconnection agreements, which can take several years in congested markets like Northern Virginia or Amsterdam, also acts as a significant bottleneck for new data center developments.

The transition to digital substations offers a substantial opportunity for players operating in this market. By leveraging the IEC 61850 process bus technology, operators can replace traditional copper wiring with fiber-optic cables, reducing installation costs and improving data visibility. This digitalization enables advanced analytics and digital twin modeling, allowing for more efficient asset management. Additionally, the growth of grid-interactive data centers offers an opportunity for substations to play a key role in demand response programs. Data centers can act as virtual power plants (VPPs), providing frequency regulation and other ancillary services to the grid, thereby creating new revenue streams for operators while enhancing grid stability.

The data center substation industry faces a critical challenge in complying with environmental regulations regarding the use of Sulfur Hexafluoride (SF6). SF6 is a potent greenhouse gas, and its phase-out is being mandated in several jurisdictions. For example, the EU F-gas Regulation bans new SF6-based medium-voltage switchgear up to 24kV starting in 2026. Developing and deploying SF6-free alternatives that maintain the same compact footprint and reliability is a significant technical and economic challenge. Furthermore, the increasing connectivity of substation automation systems introduces cybersecurity risks. Protecting critical electrical infrastructure from sophisticated cyber threats requires robust security frameworks and continuous monitoring, adding complexity to substation design and operation.

The shift toward modular and prefabricated substation solutions is one of the most significant trends reshaping the market. Data center operators are increasingly moving away from traditional on-site construction toward factory-tested eHouses and skids. This approach can reduce on-site installation time by up to 30-50%, which is critical for hyperscale operators who need to bring capacity online as quickly as possible. Modular substations also offer improved quality control and standardized designs that can be replicated across global data center portfolios, ensuring consistency in performance and maintenance.

The adoption of digital substation technology is gaining momentum as operators seek better visibility into their electrical infrastructure. Digital substations replace conventional analog signals with digital communication over fiber optics, based on the IEC 61850 standard. This allows for the integration of intelligent electronic devices (IEDs) that can provide real-time diagnostics and predictive maintenance alerts. By monitoring the health of transformers and switchgear continuously, operators can identify potential issues before they lead to failure, thereby maximizing uptime and extending the lifespan of expensive substation assets.

Based on component, the global data center substation market is segmented into switchgear, transformers, circuit breakers, relays & protection systems, power automation & control systems, and others. In 2026, the switchgear segment is expected to account for the largest share of the market. The large share of this segment is primarily attributed to the critical role of switchgear in controlling, protecting, and isolating electrical equipment. High-voltage and medium-voltage switchgear are essential for managing the massive power loads of modern data centers, and the shift toward gas-insulated switchgear (GIS) for its reliability and compact footprint further supports this segment's dominance.

However, the power automation & control systems segment is projected to grow at the highest CAGR during the forecast period. The rapid growth of this segment is driven by the increasing digitalization of substations and the need for advanced monitoring and control capabilities. The integration of SCADA systems, intelligent relays, and IEC 61850-compliant communication networks is becoming a standard requirement for high-availability data centers.

Based on construction, the market is segmented into conventional (on-site built) and modular/prefabricated. In 2026, the conventional segment is expected to hold the largest share, as many large-scale substation projects still rely on traditional civil engineering and on-site assembly for high-voltage transmission-level substations. However, the modular/prefabricated segment is projected to register the highest CAGR. This growth is fueled by the 'speed-to-market' demands of hyperscale operators and the benefits of reduced on-site labor and improved quality control offered by factory-integrated solutions.

North America is expected to dominate the global data center substation market in 2026, driven by the strong presence of hyperscale providers and the concentration of data center hubs in regions like Northern Virginia, which has the highest density of data centers globally. The mature utility infrastructure and significant investments in grid modernization support the demand for high-capacity substation equipment. The U.S. alone has over 4,000 data centers, and the ongoing expansion of AI-ready facilities is a major growth driver. The key companies operating in the North American market are ABB Ltd., Schneider Electric SE, Siemens Energy AG, Eaton Corporation plc, and GE Vernova.

Asia-Pacific data center substation market is projected to witness the fastest growth during the forecast period. This growth is driven by rapid digitalization, increasing internet penetration, and the expansion of cloud services in China, India, and Southeast Asia. China's state-led infrastructure projects and India's growing status as a global data center hub are significant factors. The emerging markets in the region are investing heavily in new power infrastructure to support the world's fastest-growing internet user base. The key companies operating in the Asia-Pacific market are Hitachi Energy Ltd., Mitsubishi Electric Corporation, Toshiba Energy Systems & Solutions Corporation, LS ELECTRIC Co., Ltd., and TBEA Co., Ltd.

The global data center substation market is projected to reach USD 22.8 billion by 2036, growing at a CAGR of 8.1% from 2026 to 2036.

The switchgear segment is expected to hold the largest share in 2026, due to its essential role in circuit protection and power distribution.

The primary drivers include the need for rapid deployment (speed-to-market), standardized designs, and reduced on-site construction requirements.

The regulation bans new SF6-based medium-voltage switchgear up to 24kV starting in 2026, driving the adoption of SF6-free insulation technologies.

Asia-Pacific is projected to witness the highest CAGR during the forecast period, fueled by rapid digital transformation and expanding internet infrastructure.

It enables interoperability between different manufacturers' equipment and supports the transition to digital substations through a standardized communication protocol.

Hyperscale facilities require massive, dedicated power loads (often 100MW+), necessitating dedicated high-voltage substations for grid connection.

Key challenges include long lead times for specialized materials like grain-oriented electrical steel and a shortage of global manufacturing capacity.

They enable real-time monitoring, predictive maintenance, and reduced cabling, leading to higher reliability and lower long-term maintenance costs.

Substation design is primarily governed by international standards such as IEEE C37, IEC 61850, and NFPA 70/70E.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency and Pricing

2. Research Methodology

3. Executive Summary

4. Market Insights

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Exponential Growth in AI and Hyperscale Data Centers

4.2.1.2. Increasing Demand for High-Reliability Power Infrastructure

4.2.2. Restraints

4.2.2.1. High Initial Capital Investment

4.2.2.2. Supply Chain Bottlenecks for Critical Components

4.2.3. Opportunities

4.2.3.1. Deployment of Digital Substations and Digital Twins

4.2.3.2. Integration of Renewable Energy and BESS

4.2.4. Challenges

4.2.4.1. Environmental Impact and Phase-out of SF6 Gas

4.2.4.2. Cybersecurity Risks in Automated Systems

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Data Center Substation Market Assessment, by Component/Offering

5.1. Introduction

5.2. Switchgear

5.2.1. High-Voltage Switchgear

5.2.2. Medium-Voltage Switchgear

5.3. Transformers

5.3.1. Power Transformers

5.3.2. Distribution Transformers

5.4. Circuit Breakers

5.5. Relays & Protection Systems

5.6. Power Automation & Control Systems

5.7. Others

6. Data Center Substation Market Assessment, by Type

6.1. Introduction

6.2. Air-Insulated Substations (AIS)

6.3. Gas-Insulated Substations (GIS)

6.4. Hybrid Substations

7. Data Center Substation Market Assessment, by Voltage Level

7.1. Introduction

7.2. High Voltage (Above 100 kV)

7.3. Medium Voltage (1 kV to 100 kV)

8. Data Center Substation Market Assessment, by Construction/Deployment

8.1. Introduction

8.2. Conventional (On-site Built)

8.3. Modular/Prefabricated (eHouses, Skids)

9. Data Center Substation Market Assessment, by Application

9.1. Introduction

9.2. Hyperscale Data Centers

9.3. Colocation Data Centers

9.4. Enterprise Data Centers

9.5. Edge Data Centers

10. Data Center Substation Market Assessment, by Geography

10.1. Introduction

10.2. North America

10.2.1. U.S.

10.2.2. Canada

10.3. Europe

10.3.1. Germany

10.3.2. UK

10.3.3. France

10.3.4. Netherlands

10.3.5. Italy

10.3.6. Spain

10.3.7. Ireland

10.3.8. Rest of Europe

10.4. Asia-Pacific

10.4.1. China

10.4.2. India

10.4.3. Japan

10.4.4. Singapore

10.4.5. Australia

10.4.6. Rest of Asia-Pacific

10.5. Latin America

10.5.1. Brazil

10.5.2. Mexico

10.5.3. Rest of Latin America

10.6. Middle East & Africa

10.6.1. UAE

10.6.2. Saudi Arabia

10.6.3. South Africa

10.6.4. Rest of MEA

11. Competitive Landscape

12. Company Profiles

12.1. ABB Ltd.

12.2. Schneider Electric SE

12.3. Siemens Energy AG

12.4. Hitachi Energy Ltd.

12.5. Eaton Corporation plc

12.6. GE Vernova

12.7. Mitsubishi Electric Corporation

12.8. Toshiba Energy Systems & Solutions Corporation

12.9. Hyundai Electric & Energy Systems Co., Ltd.

12.10. Fuji Electric Co., Ltd.

12.11. LS ELECTRIC Co., Ltd.

12.12. Powell Industries, Inc.

12.13. S&C Electric Company

12.14. TBEA Co., Ltd.

12.15. NR Electric Co., Ltd.

12.16. Ormazabal (Velatia)

12.17. CHINT Group

12.18. Bharat Heavy Electricals Limited (BHEL)

12.19. CG Power and Industrial Solutions Limited

12.20. Meidensha Corporation

12.21. Other Players

13. Appendix

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Feb-2026

Subscribe to get the latest industry updates