Resources

About Us

AI in 3D Printing Market by Offering (Software, Hardware, Services), Technology (Machine Learning, Physics-Informed AI, Generative & Agentic AI), Application, Printing Technology, End User (Aerospace & Defense, Healthcare, Automotive), and Geography — Global Forecast to 2036

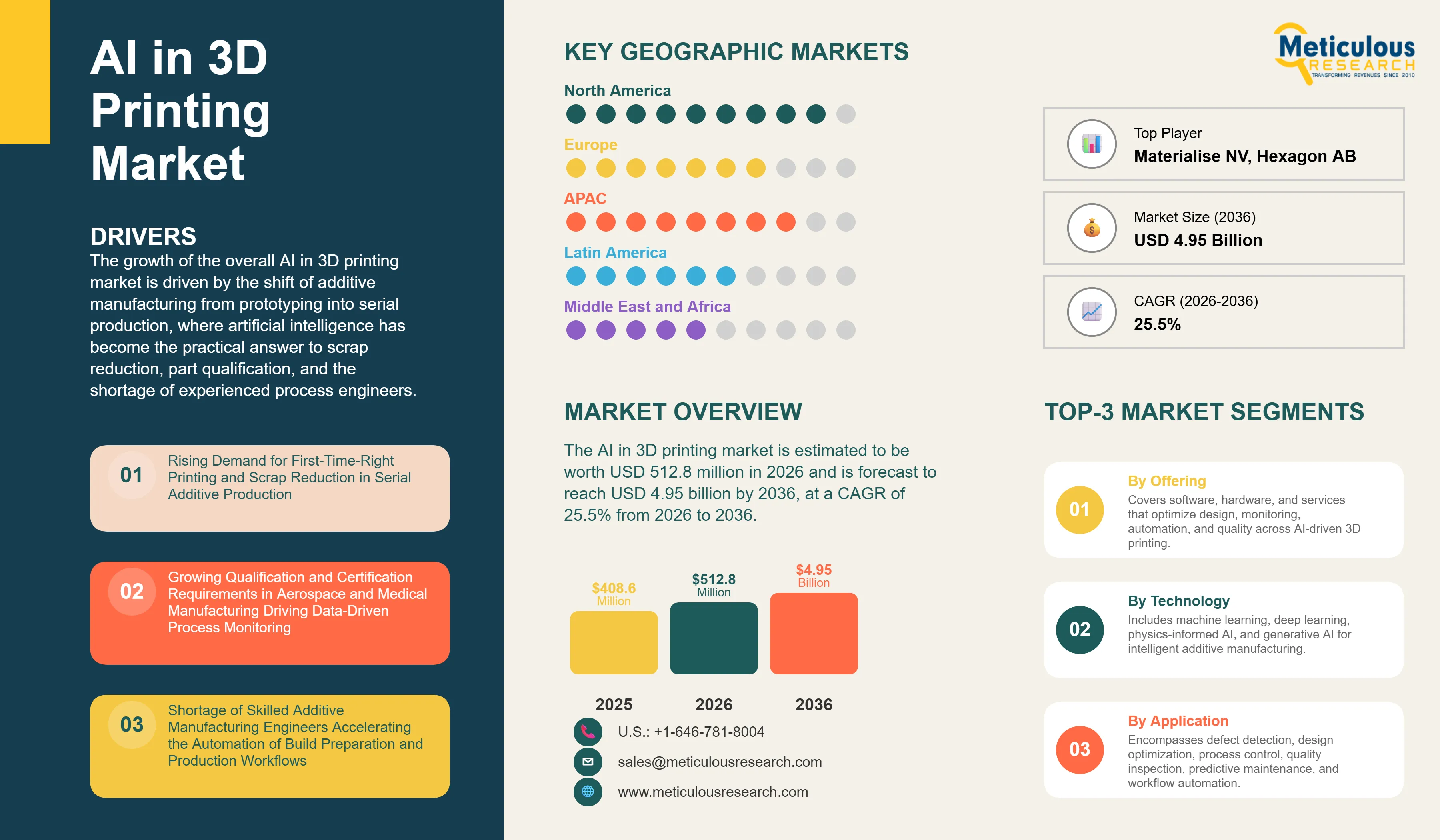

Report ID: MRSE - 1042103 Pages: 185 Jul-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe AI in 3D printing market is estimated to be worth USD 512.8 million in 2026 and is forecast to reach USD 4.95 billion by 2036, at a CAGR of 25.5% from 2026 to 2036.

The growth of the overall AI in 3D printing market is driven by the shift of additive manufacturing from prototyping into serial production, where artificial intelligence has become the practical answer to scrap reduction, part qualification, and the shortage of experienced process engineers. Machine learning is now embedded across the 3D printing workflow, from generative design and build preparation software through in-situ monitoring and defect detection to predictive maintenance of printer fleets.

Print quality in additive manufacturing depends on dozens of coupled parameters, including laser power, scan speed, layer thickness, chamber conditions, and powder characteristics. Trained models read live sensor and camera data during a build, flag porosity, recoater interactions, and geometric deviations layer by layer, and in the newest systems adjust the process before a defect propagates. This is what makes AI-enabled 3D printing attractive to aerospace, medical, and automotive manufacturers, where every failed build carries a high material and machine-time cost and every qualified part needs a documented digital record.

Click here to: Get Free Sample Pages

Click here to: Get Free Sample Pages

The AI in 3D printing market covers the software, embedded hardware, and services that apply data-driven models to design, prepare, run, inspect, and maintain additive manufacturing systems. The market has moved well past experimentation. Printer manufacturers now ship machines with in-situ sensing and AI-assisted parameter tuning as standard options, while independent software vendors sell printer-agnostic platforms that manage quoting, scheduling, traceability, and machine data across fleets from multiple OEMs. The result is a layered market in which machine-level intelligence, factory-level workflow automation, and enterprise integration each generate distinct revenue streams.

Adoption follows the economics of production. A failed metal build wastes powder that can cost several hundred dollars per kilogram along with days of machine time, and a qualified aerospace or medical part requires documented evidence of process consistency for every unit produced. AI addresses both sides of that equation at once: models trained on historical builds raise first-time-right rates, and layer-by-layer monitoring generates the digital record that qualification demands.

As additive manufacturing scales into distributed, multi-site production networks, the value of software that encodes scarce process expertise keeps rising, which is why the software segment dominates spending and why printer OEMs, industrial software majors, and specialist start-ups are all competing for position.

Convergence of machine software and build preparation software

The lines between machine control and data preparation are blurring. Software providers now offer vector-level control of lasers in powder bed fusion systems, and OEMs are deciding whether to keep building proprietary software stacks or license these capabilities from specialists. For experienced users, this creates a new way to compete: two factories running identical machines can now differentiate on quality, speed, and even part microstructure purely through the intelligence layered on top of the hardware.

Shift from post-build inspection to layer-by-layer in-situ quality assurance

Quality assurance is moving from after-the-fact inspection, such as CT scanning of finished parts, toward verification during the build itself. Structured-light heightmap measurement, melt-pool monitoring, and camera-based anomaly detection let manufacturers catch powder bed inconsistencies and lack-of-fusion indicators as they occur, stop or correct failing builds, and cut the cost of certifying serial parts. Unsupervised and semi-supervised learning methods are gaining ground here because the sensor data generated at 50 to 100 frames per layer cannot practically be labeled by hand.

Generative and agentic AI entering the additive workflow

The newest commercial layer goes beyond the print job. Agentic platforms launched in 2026 capture engineering intent from everyday tools such as email and messaging, apply context and permissions, and act inside ERP, PLM, and QMS systems, delivering real-time compliance checks and part-level provenance. On the design side, generative AI assistants now check printability, estimate cost, and propose build strategies, reducing the trial-and-error cycles that have historically kept additive expertise scarce.

Rising demand for first-time-right printing and scrap reduction in serial additive production

As manufacturers move from prototypes to production quantities, the cost of failure compounds, and AI has become the most direct lever for improving yield.

Growing qualification and certification requirements in aerospace and medical manufacturing

Flight-critical and implantable parts require documented evidence of process consistency, and data-driven monitoring is how that evidence gets produced economically.

Shortage of skilled additive manufacturing engineers

Experienced process engineers who can qualify a new alloy or dial in parameters for a new geometry remain scarce, and software that encodes this expertise lets manufacturers scale output without scaling headcount.

Scarcity and fragmentation of training data

Additive processes generate sensor data at very high rates, yet most of it is unlabeled, locked in proprietary machine formats, or held confidential by the manufacturers who produced it. Building models that generalize across machines, materials, and geometries remains difficult, and labeling data at production scale is impractical, which is pushing research toward unsupervised and semi-supervised techniques.

High integration and computational costs

Retrofitting sensing, edge computing, and closed-loop control onto installed machines requires capital and specialist integration work that small and mid-sized service bureaus struggle to justify. Real-time melt-pool inspection with high-speed cameras also carries substantial computational cost, which keeps the most advanced monitoring configurations concentrated among larger production operations.

Physics-informed AI and vector-level laser control

The integration of physics-based AI models directly into scan-head control, demonstrated through the open 3MF toolpath extension with power modulation along individual vectors, opens a new tier of process differentiation. Users of the same machine hardware can compete on quality, speed, and part microstructure through software, creating recurring high-value software revenue in the metal printing segment.

Generative and agentic AI across the part lifecycle

Agentic platforms that capture engineering activity from everyday tools and act inside ERP, PLM, and QMS systems point to a much larger addressable market than print-process optimization alone. As these assistants mature, AI spending attached to 3D printing operations will increasingly cover quoting, compliance checks, provenance, and knowledge capture in addition to the build itself.

Software Leads the Market in 2026

The software segment holds around 61% of the AI in 3D printing market in 2026, spanning generative design and build preparation tools, process monitoring and control platforms, additive manufacturing execution systems, and predictive analytics. Printer-agnostic platforms have become the operating layer of additive factories, handling quoting, nesting, scheduling, traceability, and machine data across mixed fleets. Hardware, comprising machine vision and in-situ sensing systems along with edge computing modules, contributes a growing share as OEMs make optical and thermal sensing standard on production systems, while services expand with integration and model-deployment projects.

Deep Learning & Computer Vision Holds the Largest Technology Share in 2026

Camera-based layer inspection is the most mature and widely deployed AI capability on 3D printers, which places deep learning and computer vision at roughly 38% of the market in 2026. Convolutional networks classify porosity, cracking, delamination, and surface irregularities from in-situ imagery with accuracy that manual inspection cannot match at production speed. Physics-informed and hybrid models represent the fastest-advancing technology class, combining simulation with learned corrections to govern laser-material interaction, and generative and agentic AI is the newest commercial layer.

In-Situ Process Monitoring & Defect Detection Leads by Application in 2026

With about 27% of 2026 revenue, in-situ monitoring is where AI delivers its clearest return: structured-light and melt-pool monitoring systems detect powder bed anomalies, recoater interactions, and lack-of-fusion indicators as they happen, allowing operators to stop or correct a failing build instead of discovering the defect days later in CT inspection. Process parameter optimization and build preparation follows closely, and production planning and workflow automation grows steadily as additive operations scale into multi-site networks.

Powder Bed Fusion Accounts for the Largest Printing Technology Share in 2026

Laser powder bed fusion concentrates the highest-value parts, the most complex parameter space, and the strongest economic case for AI, giving the segment close to 44% of the market in 2026. Material extrusion is the second-largest segment, where AI-assisted failure detection has reached even desktop-class machines through camera and lidar systems, and directed energy deposition adopts closed-loop control for large-format repair and near-net-shape applications.

Aerospace & Defense Leads by End User in 2026

Aerospace and defense holds about 33% of the market in 2026. The sector prints structurally critical, expensive parts in qualified processes, so every improvement in first-time-right rates and every layer of documented process evidence has direct financial and regulatory value. Healthcare is the second-largest end user, where AI-driven workflow platforms already manage high-volume dental and patient-specific implant production, and automotive adoption expands as generative design and printed tooling spread through the supply chain.

North America Leads the Global AI in 3D Printing Market in 2026

North America accounts for approximately 40% of the AI in 3D printing market in 2026, supported by the region's concentration of aerospace primes and defense funding for additive process monitoring, an established base of additive software vendors, and early enterprise adoption of AI across manufacturing operations. Europe follows with strong positions in industrial printer OEMs and process control research, led by Germany and the U.K., where physics-AI and workflow software specialists are clustered.

Asia-Pacific is projected to record the highest CAGR of 28.4% through 2036, reflecting the scale of China's printer manufacturing and installed base, Japan's and South Korea's precision manufacturing sectors, and national smart factory programs that fund AI adoption in production. Latin America and the Middle East & Africa are earlier in the adoption curve, with Israel and the UAE standing out for additive software talent and government-backed advanced manufacturing initiatives respectively.

The AI in 3D printing market comprises four broad categories of competitors. Printer OEMs, such as EOS GmbH and Stratasys Ltd., are embedding AI into their hardware, machine vision, and software ecosystems to enable intelligent process monitoring, closed-loop control, and autonomous print optimization, making AI a key differentiator for industrial additive manufacturing systems. Industrial software providers, including Siemens AG, Autodesk, Inc., Hexagon AB, and Materialise NV, are integrating AI across design, simulation, digital manufacturing, and production workflow platforms while leveraging their extensive enterprise customer base.

Independent additive manufacturing software providers, including Oqton, Inc., Authentise, Inc., 3YOURMIND GmbH, Dyndrite Corporation, and nTop, Inc., compete by delivering printer-agnostic solutions spanning computational design, build preparation, manufacturing execution, production planning, and AI-driven workflow automation. AI-native innovators, such as Ai Build Ltd., Inkbit Corporation, 1000 Kelvin GmbH, and Phase3D, Inc., are advancing next-generation capabilities in autonomous toolpath optimization, vision-guided printing, physics-informed AI process control, and real-time in-situ quality assurance.

Product launches and partnerships are the dominant growth strategies, with OEM integrations serving as the key distribution channel for specialist software. Consolidation is reshaping the field: platform assets have changed hands as hardware companies refocus, and independent ownership of fleet-level software has become a selling point for buyers who want to avoid lock-in to a single printer brand. The companies profiled in this report were selected for active 2026 operations, verified AI capabilities applied to 3D printing, and current ownership structures.

The report profiles the leading providers of AI-enabled software, intelligent manufacturing platforms, and digital solutions for 3D printing, reflecting the competitive landscape and current ownership structure as of 2026. Key companies profiled include Oqton, Inc. (Hubb Global Holdings) (U.S.), Materialise NV (Belgium), Autodesk, Inc. (U.S.), Siemens AG (Siemens Digital Industries Software) (Germany), Hexagon AB (Sweden), EOS GmbH (Germany), Stratasys Ltd. (U.S./Israel), Ai Build Ltd. (U.K.), Authentise, Inc. (U.S.), nTop, Inc. (U.S.), 3YOURMIND GmbH (Germany), Inkbit Corporation (U.S.), 1000 Kelvin GmbH (Germany), Phase3D, Inc. (U.S.), and Dyndrite Corporation (U.S.), among others.

|

Particulars |

Details |

|

Market Size Value in 2026 |

USD 512.8 Million |

|

Revenue Forecast in 2036 |

USD 4.95 Billion |

|

Growth Rate |

CAGR of 25.5% from 2026 to 2036 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026–2036 |

|

Historical Data |

2023–2024 |

|

Units |

Value (USD Million/Billion) |

|

Segments Covered |

Offering, Technology, Application, Printing Technology, End User, and Geography |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

|

Companies Profiled |

Oqton, Inc. (a Hubb Global Holdings company) (U.S.), Materialise NV (Belgium), Autodesk, Inc. (U.S.), Siemens AG (Germany), Hexagon AB (Sweden), EOS GmbH (Germany), Stratasys Ltd. (U.S./Israel), Ai Build Ltd. (U.K.), Authentise, Inc. (U.S.), nTop, Inc. (U.S.), 3YOURMIND GmbH (Germany), Inkbit Corporation (U.S.), 1000 Kelvin GmbH (Germany), Phase3D, Inc. (U.S.), and Dyndrite Corporation (U.S.), among others. |

By Offering: Software (Generative Design & Build Preparation, Process Monitoring & Control, Workflow Automation & Manufacturing Execution, Predictive Maintenance & Analytics), Hardware (Machine Vision & In-Situ Sensing Systems, Edge Computing & Control Modules), and Services (Integration & Deployment, Consulting & Training, Support & Managed Services)

By Technology: Machine Learning, Deep Learning & Computer Vision, Physics-Informed & Hybrid AI Models, and Generative & Agentic AI

By Application: In-Situ Process Monitoring & Defect Detection, Design Optimization & Generative Design, Process Parameter Optimization & Build Preparation, Quality Control & Inspection, Predictive Maintenance, and Production Planning & Workflow Automation

By Printing Technology: Powder Bed Fusion, Material Extrusion, Vat Photopolymerization, Material & Binder Jetting, Directed Energy Deposition, and Other Printing Technologies

By End User: Aerospace & Defense, Healthcare (Medical & Dental), Automotive, Industrial Machinery & General Manufacturing, Energy, Consumer Goods & Electronics, and Other End Users

By Geography: North America (U.S., Canada), Europe (Germany, U.K., France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Singapore, Australia & New Zealand, Rest of Asia-Pacific), Latin America (Brazil, Mexico, Rest of Latin America), and Middle East & Africa (Israel, UAE, Saudi Arabia, Rest of Middle East & Africa)

The market is estimated at USD 512.8 million in 2026 and is projected to reach USD 4.95 billion by 2036.

The market is forecast to grow at a CAGR of 25.5% from 2026 to 2036.

Software leads with around 61% of the market in 2026, covering build preparation, process monitoring, manufacturing execution, and predictive analytics platforms.

In-situ process monitoring and defect detection leads with about 27% of 2026 revenue, as layer-by-layer verification delivers the clearest return on AI investment in production printing.

Powder bed fusion, at close to 44% in 2026, given its concentration of high-value metal parts, complex parameter space, and melt-pool monitoring investments.

Aerospace and defense holds about 33% in 2026, driven by flight-part qualification requirements and defense funding for data-driven process control, followed by healthcare.

North America leads with approximately 40% in 2026, while Asia-Pacific is projected to grow fastest, at a CAGR of 28.4% through 2036.

The push for first-time-right printing and scrap reduction in serial production, qualification and certification requirements in aerospace and medical manufacturing, and the shortage of skilled additive process engineers.

The convergence of machine control and build preparation software, the shift from post-build inspection to layer-by-layer in-situ quality assurance, and the arrival of generative and agentic AI assistants across the part lifecycle.

Oqton, Inc. (a Hubb Global Holdings company) (U.S.), Materialise NV (Belgium), Autodesk, Inc. (U.S.), Siemens AG (Germany), Hexagon AB (Sweden), EOS GmbH (Germany), Stratasys Ltd. (U.S./Israel), Ai Build Ltd. (U.K.), Authentise, Inc. (U.S.), nTop, Inc. (U.S.), 3YOURMIND GmbH (Germany), Inkbit Corporation (U.S.), 1000 Kelvin GmbH (Germany), Phase3D, Inc. (U.S.), and Dyndrite Corporation (U.S.), among others.

Published Date: Oct-2024

Published Date: May-2023

Published Date: Jul-2022

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates