Resources

About Us

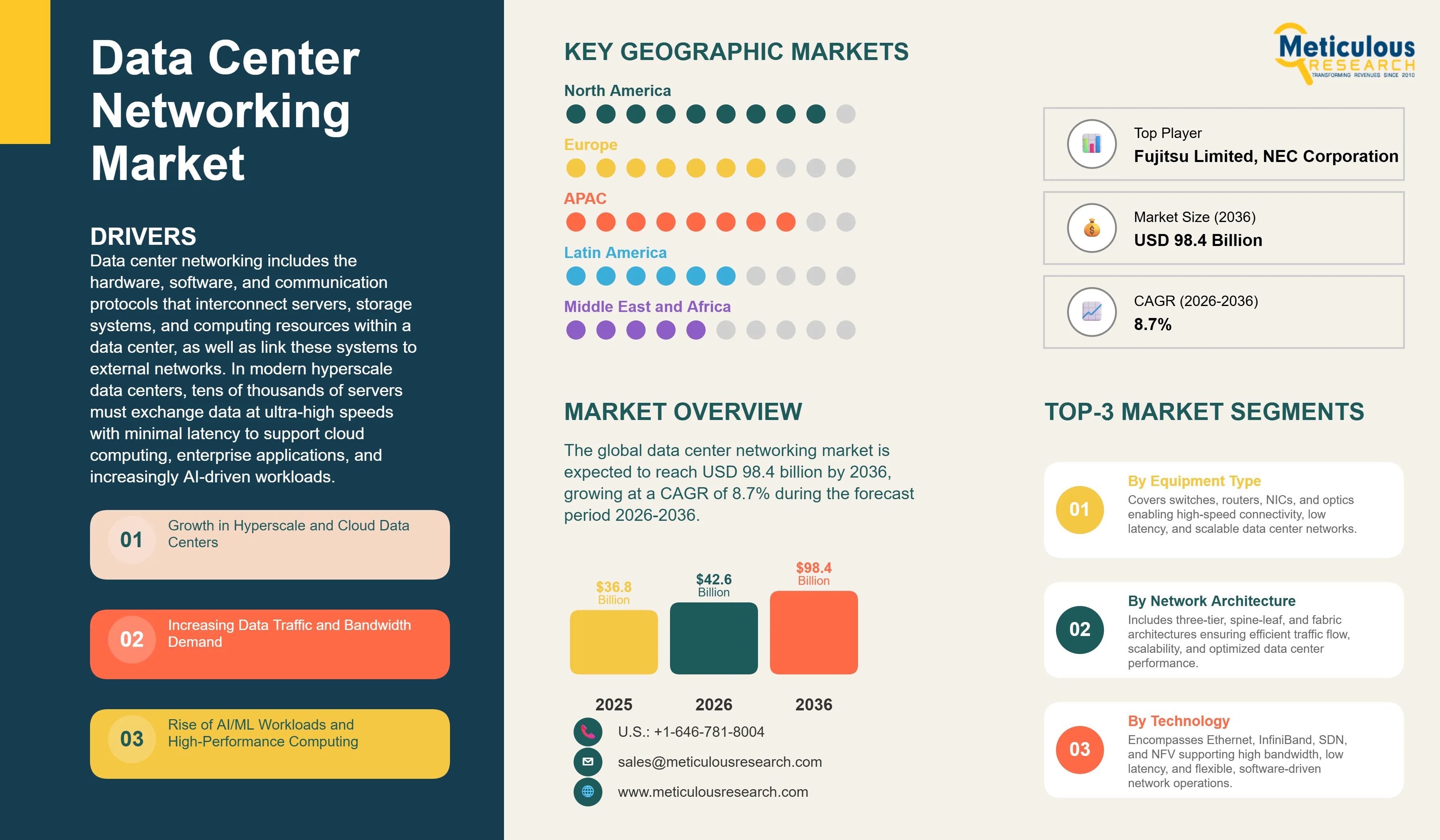

The global data center networking market was valued at USD 36.8 billion in 2025. This market is expected to reach USD 98.4 billion by 2036 from an estimated USD 42.6 billion in 2026, growing at a CAGR of 8.7% during the forecast period 2026-2036. According to Synergy Research Group, the number of hyperscale data centers operated by major cloud providers reached 1,136 globally at the end of 2024, reflecting record-scale expansion over the past several years. The sector added 137 new hyperscale facilities in 2024, and the global hyperscale footprint continues to grow rapidly as AI-driven demand pushes networking and IT infrastructure requirements higher.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Data center networking includes the hardware, software, and communication protocols that interconnect servers, storage systems, and computing resources within a data center, as well as link these systems to external networks. In modern hyperscale data centers, tens of thousands of servers must exchange data at ultra-high speeds with minimal latency to support cloud computing, enterprise applications, and increasingly AI-driven workloads. The network fabric, comprising switches, routers, security systems, and high-speed optical interconnects, forms a performance-critical backbone, directly influencing application speed, scalability, and reliability. As a result, data center networking remains one of the most frequently upgraded layers of IT infrastructure.

The market is experiencing strong and sustained growth, driven by the convergence of cloud expansion and AI workload proliferation. Global data center traffic continues to rise rapidly, fueled by video streaming, cloud services, and data-intensive enterprise applications. More importantly, the surge in artificial intelligence (AI) training and inference workloads since 2023 has introduced a new class of networking demand. AI clusters require thousands of GPUs to operate in parallel, necessitating ultra-high bandwidth, low-latency interconnects. This has significantly accelerated the adoption of advanced networking technologies such as 400G Ethernet and InfiniBand, particularly in AI-optimized data centers.

A major technology transition is currently underway, with hyperscale operators shifting from 100G to 400G Ethernet as the standard interconnect, while early deployments of 800G infrastructure are gaining momentum. Industry analyses (e.g., Dell'Oro Group) indicate that 400G switch deployments have now overtaken 100G in hyperscale environments, marking a key inflection point in the market. This upgrade cycle is expected to continue through the forecast period, as cloud providers and AI infrastructure builders invest in next-generation networking to support increasingly complex, data-intensive workloads.

Overall, the data center networking market is entering a high-growth phase characterized by rapid bandwidth scaling, shorter technology refresh cycles, and increasing architectural complexity driven by AI and distributed computing demands.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 98.4 Billion |

|

Market Size in 2026 |

USD 42.6 Billion |

|

Market Size in 2025 |

USD 36.8 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 8.7% |

|

Dominating Equipment Type |

Switches |

|

Fastest Growing Equipment Type |

Optical Transceivers and Cables |

|

Dominating Network Architecture |

Spine-Leaf Architecture |

|

Fastest Growing Network Architecture |

Fabric-Based Architecture |

|

Dominating Technology |

Ethernet-Based Networking (100G) |

|

Fastest Growing Technology |

400G/800G Ethernet |

|

Dominating Application |

Cloud Computing |

|

Fastest Growing Application |

AI and Machine Learning Workloads |

|

Dominating End User |

Cloud Service Providers |

|

Fastest Growing End User |

Enterprises |

|

Dominating Data Center Type |

Hyperscale Data Centers |

|

Fastest Growing Data Center Type |

Edge Data Centers |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

AI Infrastructure Buildout Creating an Entirely New Networking Demand Category

The rapid commercial deployment of generative AI applications following the launch of ChatGPT in late 2022 has triggered a data center infrastructure buildout that is without precedent in the industry's history. According to Microsoft's fiscal year 2024 annual report, Microsoft committed to spending around USD 80 billion on data center infrastructure in fiscal year 2025, with a significant portion directed toward AI-optimized compute clusters. Amazon Web Services, Google Cloud, and Meta have made similar large capital expenditure announcements for 2024 and 2025, with AI infrastructure representing a rapidly growing share of total data center capex.

The networking requirements of AI training clusters are fundamentally different from those of conventional cloud computing workloads. Training a large language model requires thousands of GPUs to work in close coordination, exchanging gradient updates across the network thousands of times per second. This requires network latency below one microsecond and bandwidth of 400G or 800G per GPU, creating demand for high-radix switches, low-latency optical interconnects, and specialized AI networking fabrics including NVIDIA's NVLink and NVSwitch technologies and InfiniBand networks. Arista Networks, which has positioned itself as the leading supplier of networking for AI clusters in addition to conventional cloud data centers, reported revenue of approximately USD 7.0 billion in fiscal year 2024, growing over 19.5% year-on-year, with the hyperscale AI networking segment cited as a primary growth driver. This AI networking demand is creating a new high-value market segment that is driving disproportionate revenue growth for networking equipment suppliers.

400G to 800G Transition Accelerating Across Hyperscale Data Centers

The switch port speed transition from 100G to 400G, and the beginning of the transition to 800G, is the largest networking equipment replacement cycle in years and is generating very large procurement volumes across the global hyperscale operator base. According to Dell’Oro Group’s recent data center networking outlook, 400G has become the leading high-speed Ethernet tier in hyperscale data center deployments, with 800G beginning to emerge for the highest-bandwidth AI and hyperscale environments. Each data center networking refresh cycle requires replacement of leaf switches, spine switches, optical transceivers, and associated cabling, generating a multi-year hardware procurement program from each hyperscale customer as they upgrade their facilities.

Broadcom and Marvell are the primary providers of the ASIC switching chips that power high-speed Ethernet switches, and their next-generation chips supporting 51.2 Tbps switch capacity are expected to enable single-chip 800G switches that will further accelerate the transition to higher speeds. Arista, Cisco, and Juniper are the primary switch OEMs incorporating these chips into commercial products, while open networking switches from manufacturers including Edgecore and UfiSpace are gaining adoption among hyperscale operators using open-source network operating systems to reduce vendor dependency. Optical transceiver manufacturers including Coherent, II-VI, and Lumentum are seeing strong demand for 400G QSFP-DD and OSFP transceivers as the installed base of 400G switches grows, with 800G transceivers beginning volume shipments.

Software-Defined Networking Maturing into Mainstream Data Center Operations

Software-defined networking, which separates the network control plane from the data forwarding plane and enables centralized programmable network management, has progressed from a technology concept introduced in academic research around 2008 to a mainstream operational reality at hyperscale data centers. Google's B4 private wide-area network, which Google has publicly described as the world's first software-defined WAN operating at scale, carries more traffic than Google's entire external internet traffic and has demonstrated the operational benefits of SDN at hyperscale. Meta's data center network architecture, described in technical publications, uses SDN-based control to manage its large server and storage interconnect fabrics. Microsoft Azure's network uses SDN principles extensively for virtual network management and traffic engineering.

The commercial SDN market is led by Cisco's Application Centric Infrastructure and its Nexus Dashboard, VMware's NSX (now Broadcom's), and open-source SDN controllers built on the OpenFlow protocol and its successors. According to IDC's 2024 software-defined networking forecast, the SDN market for data centers is growing at approximately 20% annually as enterprises and colocation operators follow the hyperscale lead in deploying SDN for network automation, multi-tenancy management, and network policy enforcement. The combination of SDN with network function virtualization, which replaces physical security appliances and load balancers with software running on standard servers, is enabling data center operators to dramatically reduce the hardware cost and physical footprint of their network services layer while improving the speed of network provisioning and change management.

Rise of AI/ML Workloads and High-Performance Computing

The commercial deployment of generative AI applications at scale has created a step-change in data center networking requirements that is driving an investment cycle unlike any the industry has seen before. According to Goldman Sachs Research, hyperscale (AI-driven) data center capital expenditure has been rising sharply, with total investments reaching over USD 300 billion annually by 2024, and projected to exceed USD 500 billion by 2026 as AI infrastructure build-out accelerates. NVIDIA's data center revenue, which is the primary proxy for AI compute infrastructure investment, reached USD 60.9 billion in fiscal year 2024, growing over 126% year-on-year, and each NVIDIA GPU cluster requires high-performance networking that is a multiplier of the compute spend. According to NVIDIA's own guidance, networking and interconnect infrastructure typically represents 20 to 30% of total AI cluster cost, meaning NVIDIA's data center revenue implies very large networking infrastructure procurement.

Growth in Hyperscale and Cloud Data Centers

According to Synergy Research Group's 2024 tracking data, global hyperscale data center capacity expanded substantially in 2023 and 2024, with Amazon, Microsoft, Google, and Meta collectively accounting for the majority of new hyperscale deployments. The global cloud computing market, which drives hyperscale data center investment, reached approximately USD 680 billion in revenue in 2024 according to Gartner's forecast, and is projected to continue growing at above-average rates through the forecast period. Each new hyperscale data center facility of 50 to 100 megawatts of IT load capacity requires hundreds of millions of dollars of networking equipment including spine and leaf switches, optical interconnects, and security appliances, making hyperscale expansion the primary near-term demand driver for data center networking hardware.

Adoption of 400G/800G Networking Technologies

The transition from 100G to 400G and eventually 800G as the standard data center interconnect speed represents the most significant hardware upgrade cycle in the networking market today and the largest near-term commercial opportunity for equipment and component suppliers. According to Dell'Oro Group's 2024 data, 400G Ethernet switch revenue crossed the 100G revenue line in 2023 and is expected to represent the majority of hyperscale switch procurement through 2025 and 2026. The 800G transition, driven by the networking bandwidth requirements of the largest AI training clusters, is beginning in 2024 and 2025 with early deployments at hyperscale customers. Each port speed transition requires replacement of switches, optical transceivers, and associated cabling, generating procurement programs of hundreds of millions of dollars per hyperscale facility across the global data center operator base.

Network Automation and AI-Based Management

The increasing complexity of large-scale data center networks, which may include hundreds of thousands of switch ports and millions of virtual network connections, is creating strong demand for AI-based network management platforms that can automate configuration, detect anomalies, predict failures, and optimize traffic routing without requiring manual intervention at the individual device level. Cisco's AI-powered Catalyst Center and Nexus Dashboard Insights, Arista's CloudVision platform, and Juniper's Mist AI platform are examples of commercial AI network management products that are gaining traction in enterprise and colocation data center environments. According to Gartner's 2024 Hype Cycle for Networking, AI-driven network operations, referred to as AI Ops for networking, are transitioning from early adoption to mainstream deployment, with a growing number of enterprise customers reporting measurable reductions in network-related incidents and mean time to resolution through AI-based anomaly detection and root cause analysis.

By Equipment Type: In 2026, Switches to Dominate

Based on equipment type, the global market for data center networking is segmented into switches (core, spine, and leaf), routers, network security equipment, load balancers, network interface cards, and optical transceivers and cables. In 2026, the switches segment is expected to account for the largest share of the global data center networking market. Data center switches are the fundamental building blocks of every data center network, required at the leaf layer to connect servers, at the spine layer to interconnect leaf switches, and at the core layer to connect to external networks. The very large volume of switches required to connect the hundreds of thousands of servers in a hyperscale data center, combined with the ongoing transition from 100G to 400G switches that is driving a multi-year replacement cycle, makes switches the dominant equipment category by revenue.

However, the optical transceivers and cables segment is projected to register the highest CAGR during the forecast period. Every 400G or 800G switch port requires a corresponding optical transceiver, and the transition to higher-speed networking is driving very rapid growth in high-speed transceiver demand. Optical transceivers are a consumable infrastructure component that must match every networking speed upgrade, making the transceiver market a leading indicator and proportional beneficiary of each networking technology transition.

By Technology: In 2026, 100G Ethernet to Hold the Largest Share

Based on technology, the global data center networking market is segmented into Ethernet-based networking (25G/50G, 100G, and 400G/800G), InfiniBand networking, software-defined networking, network function virtualization, and others. In 2026, the 100G Ethernet segment is expected to account for the largest share of the global data center networking market. 100G Ethernet is the current predominant interconnect speed across the large installed base of data center switches globally, having been the standard for hyperscale and enterprise data centers for the past five to six years. The large number of data center facilities still operating on 100G infrastructure and the gradual pace at which capacity is upgraded rather than replaced overnight means 100G remains the largest installed base by port count through 2026.

However, the 400G/800G Ethernet segment is projected to register the highest CAGR during the forecast period, driven by rapidly increasing bandwidth requirements in AI and hyperscale cloud environments. The pace of 400G deployment continues to accelerate across hyperscale data centers, particularly to support AI training clusters, east-west traffic growth, and distributed workloads. At the same time, the transition toward 800G Ethernet is gaining momentum, with leading cloud providers and AI infrastructure operators beginning to deploy next-generation switches and optical modules to overcome the bandwidth limitations of 400G architectures.

By Application: In 2026, Cloud Computing to Hold the Largest Share

Based on application, the global market for data center networking is segmented into cloud computing (public, private, and hybrid), AI and machine learning workloads, big data and analytics, content delivery and streaming, enterprise IT applications, and other applications. In 2026, the cloud computing segment is expected to account for the largest share of the global data center networking market. Cloud computing is the largest and most dominant application driving data center investment globally. According to Gartner's 2024 forecast, worldwide public cloud services revenue reached approximately USD 680 billion in 2024, and the hyperscale cloud operators who run this infrastructure are the world's largest single purchasers of data center networking equipment. Amazon Web Services, Microsoft Azure, and Google Cloud collectively spend tens of billions of dollars on networking infrastructure annually.

However, the AI and machine learning workloads segment is projected to register the highest CAGR during the forecast period. The AI infrastructure buildout of 2023 to 2025 has created a new and very fast-growing demand segment for networking equipment specifically optimized for AI cluster interconnects, characterized by very high bandwidth, very low latency, and the use of both Ethernet and InfiniBand fabrics. According to IDC's 2024 AI infrastructure spending forecast, global spending on AI infrastructure including servers, storage, and networking is expected to grow at approximately 30% annually through 2028, with networking representing a substantial and growing share of total AI cluster cost.

By Data Center Type: In 2026, Hyperscale Data Centers to Hold the Largest Share

Based on data center type, the global data center networking market is segmented into hyperscale data centers, colocation data centers, enterprise data centers, and edge data centers. In 2026, the hyperscale data centers segment is expected to account for the largest share of the global data center networking market. Hyperscale data centers operated by Amazon, Microsoft, Google, Meta, and a small number of other large cloud and internet companies are the world's largest individual purchasers of networking equipment, with a single facility of 100 megawatts or more potentially consuming hundreds of millions of dollars of switches, transceivers, and security equipment. According to Synergy Research Group, hyperscale operators are responsible for a rapidly growing share of global data center capacity expansion, with 1,136 hyperscale sites worldwide at the end of 2024 and a continuing four-year doubling trend in total hyperscale capacity

However, the edge data centers segment is projected to register the highest CAGR during the forecast period. Edge data centers, which are smaller facilities located close to end users to enable low-latency processing of data from IoT devices, mobile users, and streaming applications, are growing rapidly as 5G deployment creates new latency-sensitive application requirements and as content delivery networks expand their point-of-presence footprints.

Data Center Networking Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global data center networking market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global data center networking market. The United States is home to the global headquarters and primary data center operations of Amazon Web Services, Microsoft Azure, Google Cloud, and Meta, which are collectively the world's largest purchasers of data center networking equipment. According to industry reporting, the U.S. is the world’s largest data center market by capacity, and Northern Virginia remains the largest data center cluster globally, with commissioned inventory well above 2.6 GW in 2024 and nearly 5 GW by 2025. The AI infrastructure buildout of 2024 and 2025 has been heavily concentrated in U.S. data center markets, including Northern Virginia, Phoenix, Chicago, and Dallas, driving very large networking equipment procurement. Cisco and Arista are two of the most important North American suppliers in data center networking, reflecting the region’s leadership in high-performance switching and AI-driven infrastructure demand.

However, the Asia-Pacific data center networking market is projected to register the fastest CAGR during the forecast period. The region has emerged as the most dynamic global hub for new data center capacity, supported by strong digital demand, expanding cloud adoption, and supportive regulatory environments. According to insights from JLL, Asia-Pacific recorded the highest year-on-year growth in data center construction activity globally across 2023 and 2025, with major investments concentrated in key hubs such as Singapore, Tokyo, and Sydney, alongside rapidly growing secondary markets including Jakarta, Kuala Lumpur, and Mumbai.

China continues to be a major driver of regional demand, supported by its large domestic internet ecosystem and hyperscale cloud providers such as Alibaba Cloud, Tencent Cloud, ByteDance, and Huawei Cloud. These companies are investing heavily in high-performance data center infrastructure, including advanced networking, largely independent of Western hyperscale ecosystems.

India is emerging as one of the fastest-growing data center markets globally. The country’s capacity is expected to expand significantly in the near term, driven by rapid digitalization, increasing enterprise cloud adoption, and evolving data localization requirements that are encouraging both domestic and global cloud providers to scale local infrastructure. Meanwhile, Singapore continues to serve as a strategic ASEAN data center hub despite land and power constraints, while Australia remains a highly active market with sustained investments in hyperscale and colocation facilities.

The data center networking market is dominated by a small number of large networking technology companies that supply the switching and routing infrastructure for the world's largest data centers, alongside semiconductor companies that develop the ASICs powering high-speed networking equipment and a growing ecosystem of software-defined and open networking companies. Competition is based on switching capacity and latency performance, port speed capability, software platform quality and ecosystem integration, power efficiency, and the ability to supply at the very large volumes that hyperscale data center operators require on tight construction timelines.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, customer relationships, technology roadmaps, and recent strategic developments. Some of the key players operating in the global data center networking market include Cisco Systems Inc. (U.S.), Arista Networks Inc. (U.S.), Juniper Networks Inc./HPE (U.S.), NVIDIA Corporation (U.S.), Hewlett Packard Enterprise (U.S.), Huawei Technologies Co. Ltd. (China), Dell Technologies Inc. (U.S.), Extreme Networks Inc. (U.S.), Broadcom Inc. (U.S.), Lenovo Group Limited (Hong Kong), Fujitsu Limited (Japan), NEC Corporation (Japan), IBM Corporation (U.S.), Nokia Corporation (Finland), and ZTE Corporation (China), among others.

The global market for data center networking is expected to reach USD 98.4 billion by 2036 from an estimated USD 42.6 billion in 2026, at a CAGR of 8.7% during the forecast period 2026-2036.

The AI and machine learning workloads segment is projected to register the highest CAGR during the forecast period 2026-2036.

The market is primarily driven by the AI infrastructure buildout, with NVIDIA reporting over 126% data center revenue growth in fiscal 2024 reflecting unprecedented GPU cluster deployment that requires proportional networking investment, combined with the continued growth of cloud computing, which Gartner projects reached USD 680 billion in 2024, driving ongoing hyperscale data center expansion globally.

Key players are Cisco Systems Inc. (U.S.), Arista Networks Inc. (U.S.), Juniper Networks Inc./HPE (U.S.), NVIDIA Corporation (U.S.), Hewlett Packard Enterprise (U.S.), Huawei Technologies Co. Ltd. (China), Dell Technologies Inc. (U.S.), Extreme Networks Inc. (U.S.), Broadcom Inc. (U.S.), Lenovo Group Limited (Hong Kong), Fujitsu Limited (Japan), NEC Corporation (Japan), IBM Corporation (U.S.), Nokia Corporation (Finland), and ZTE Corporation (China), among others.

Asia-Pacific is expected to register the highest growth rate during the forecast period 2026-2036.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Growth in Hyperscale and Cloud Data Centers

4.2.1.2 Increasing Data Traffic and Bandwidth Demand

4.2.1.3 Rise of AI/ML Workloads and High-Performance Computing

4.2.1.4 Adoption of Software-Defined Networking (SDN)

4.2.2 Restraints

4.2.2.1 High Capital Investment in Network Infrastructure

4.2.2.2 Complexity in Network Management

4.2.2.3 Interoperability Issues

4.2.3 Opportunities

4.2.3.1 Adoption of 400G/800G Networking Technologies

4.2.3.2 Growth in Edge Data Centers

4.2.3.3 Network Automation and AI-Based Management

4.2.3.4 Expansion in Emerging Markets

4.2.4 Challenges

4.2.4.1 Latency and Scalability Issues

4.2.4.2 Network Security Threats

4.3 Technology Landscape

4.3.1 Ethernet Switching Technologies (25G/100G/400G/800G)

4.3.2 Software-Defined Networking (SDN)

4.3.3 Network Function Virtualization (NFV)

4.3.4 Intent-Based Networking

4.3.5 AI-Driven Network Analytics

4.4 Data Center Networking Architecture

4.4.1 Core Layer

4.4.2 Aggregation/Spine Layer

4.4.3 Access/Leaf Layer

4.4.4 Overlay Networks (VXLAN, EVPN)

4.4.5 Control and Management Plane

4.5 Value Chain Analysis

4.5.1 Semiconductor and Chipset Providers

4.5.2 Network Equipment Vendors

4.5.3 System Integrators

4.5.4 Data Center Operators

4.5.5 Cloud Service Providers

4.6 Regulatory and Standards Landscape

4.6.1 Networking Standards (IEEE, IETF)

4.6.2 Data Security and Compliance Regulations

4.6.3 Industry Best Practices

4.7 Porter's Five Forces Analysis

4.8 Investment and Industry Trends

4.8.1 Hyperscale Data Center Expansion

4.8.2 Growth in AI Infrastructure

4.8.3 Mergers and Acquisitions in Networking

5. Data Center Networking Market, by Equipment Type

5.1 Introduction

5.2 Switches

5.2.1 Core Switches

5.2.2 Spine Switches

5.2.3 Leaf Switches

5.3 Routers

5.4 Network Security Equipment

5.4.1 Firewalls

5.4.2 Intrusion Detection/Prevention Systems

5.5 Load Balancers

5.6 Network Interface Cards (NICs)

5.7 Optical Transceivers and Cables

6. Data Center Networking Market, by Network Architecture

6.1 Introduction

6.2 Traditional Three-Tier Architecture

6.3 Spine-Leaf Architecture

6.4 Fabric-Based Architecture

7. Data Center Networking Market, by Technology

7.1 Introduction

7.2 Ethernet-Based Networking

7.2.1 25G/50G Ethernet

7.2.2 100G Ethernet

7.2.3 400G/800G Ethernet

7.3 InfiniBand Networking

7.4 Software-Defined Networking (SDN)

7.5 Network Virtualization (NFV)

7.6 Others

8. Data Center Networking Market, by Application

8.1 Introduction

8.2 Cloud Computing (Largest Segment)

8.2.1 Public Cloud

8.2.2 Private Cloud

8.2.3 Hybrid Cloud

8.3 AI and Machine Learning Workloads

8.4 Big Data and Analytics

8.5 Content Delivery and Streaming

8.6 Enterprise IT Applications

8.7 Other Applications

9. Data Center Networking Market, by End User

9.1 Introduction

9.2 Cloud Service Providers

9.3 Telecom Operators

9.4 Enterprises

9.5 Government and Public Sector

10. Data Center Networking Market, by Data Center Type

10.1 Introduction

10.2 Hyperscale Data Centers

10.3 Colocation Data Centers

10.4 Enterprise Data Centers

10.5 Edge Data Centers

11. Data Center Networking Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Netherlands

11.3.5 Ireland

11.3.6 Sweden

11.3.7 Switzerland

11.3.8 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 India

11.4.3 Japan

11.4.4 South Korea

11.4.5 Singapore

11.4.6 Australia

11.4.7 Indonesia

11.4.8 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Chile

11.5.5 Colombia

11.5.6 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Israel

11.6.5 Turkey

11.6.6 Rest of Middle East & Africa

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Cisco Systems, Inc.

13.2 Arista Networks, Inc.

13.3 Juniper Networks, Inc.

13.4 NVIDIA Corporation

13.5 Hewlett Packard Enterprise (HPE)

13.6 Huawei Technologies Co., Ltd.

13.7 Dell Technologies Inc.

13.8 Extreme Networks, Inc.

13.9 Broadcom Inc.

13.10 Lenovo Group Limited

13.11 Fujitsu Limited

13.12 NEC Corporation

13.13 IBM Corporation

13.14 Nokia Corporation

13.15 ZTE Corporation

14. Appendix

14.1 Additional Customization

14.2 Related Reports

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Jul-2024

Published Date: May-2024

Subscribe to get the latest industry updates