Resources

About Us

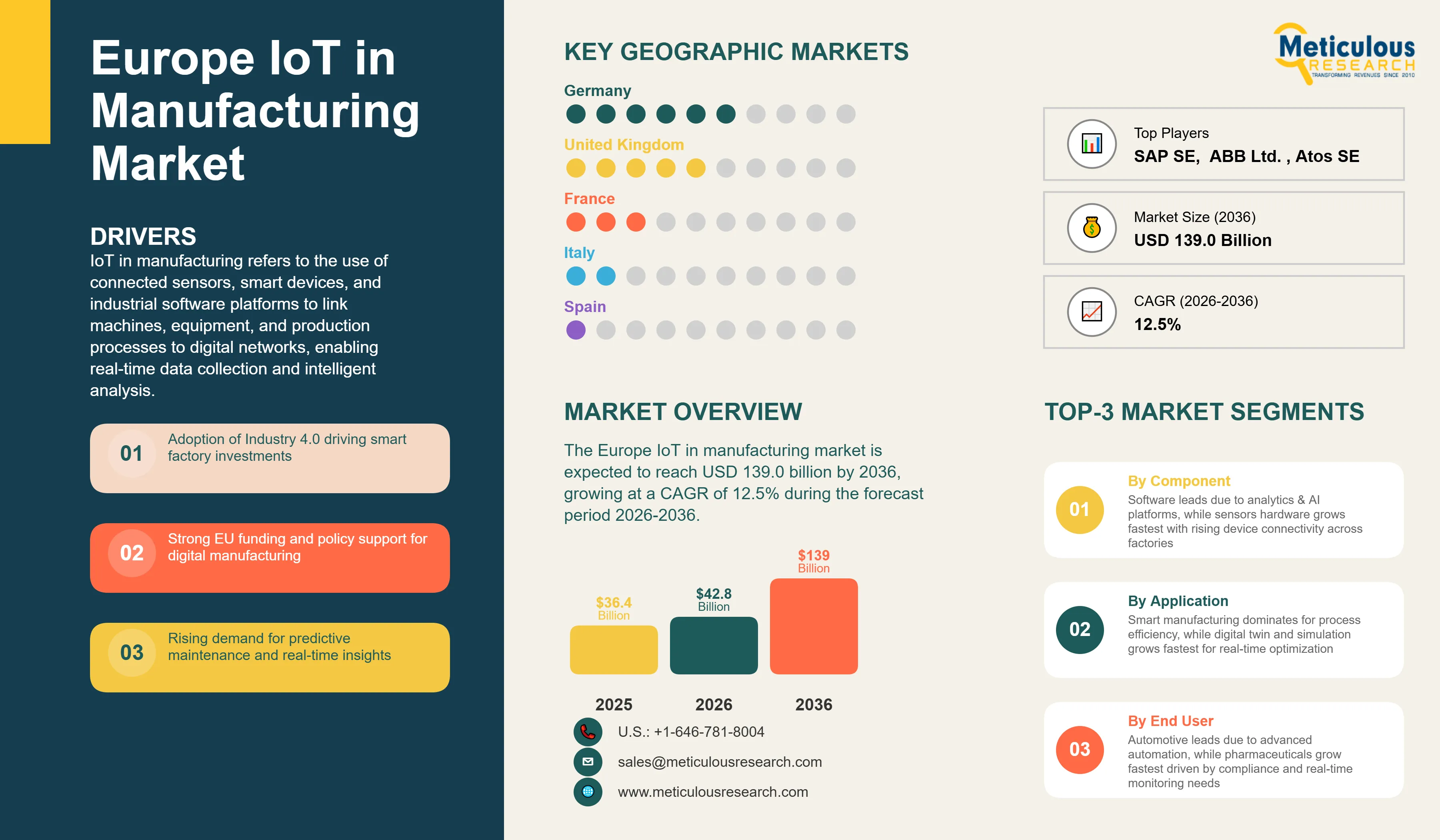

Europe IoT in Manufacturing Market Size, Share & Trends Analysis by Component, Deployment Mode, Application, End-Use Industry, Connectivity Technology, and Country - Opportunity Analysis & Industry Forecast (2026-2036)

Report ID: MRICT - 1041943 Pages: 190 Apr-2026 Formats*: PDF Category: Information and Communications Technology Delivery: 24 to 72 Hours Download Free Sample ReportThe Europe IoT in manufacturing market was valued at USD 36.4 billion in 2025. This market is expected to reach USD 139.0 billion by 2036 from an estimated USD 42.8 billion in 2026, growing at a CAGR of 12.5% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

IoT in manufacturing refers to the use of connected sensors, smart devices, and industrial software platforms to link machines, equipment, and production processes to digital networks, enabling real-time data collection and intelligent analysis. In a connected factory, sensors on machines transmit performance data continuously, software platforms analyze this data to detect inefficiencies and predict failures, and operators receive actionable insights through dashboards and alerts. The result is a manufacturing environment that operates with greater efficiency, lower unplanned downtime, and better quality control than conventional factories.

Europe's IoT in manufacturing market is growing strongly because of the continent's deep industrial base and the strong political and financial commitment behind the Industry 4.0 transformation. The EU's Digital Europe Programme, Horizon Europe research funding, and the European Alliance for Industrial Data, Edge and Cloud are all providing capital and regulatory direction that is accelerating IoT adoption across European factories. Energy costs are a particular motivator: European manufacturers, facing some of the world's highest industrial electricity prices, are using IoT energy monitoring systems to identify and reduce waste in ways that produce rapid and measurable financial returns.

Two key opportunities are defining the next growth phase. The expansion of AI-driven analytics on top of existing IoT sensor infrastructure is transforming basic data collection into genuine intelligence, with platforms from Siemens, SAP, and Bosch now offering AI models that predict machine failures days in advance, optimize production scheduling in real time, and automatically flag quality deviations. At the same time, the enormous and largely untapped SME market across Europe represents the biggest expansion opportunity as cloud-based IoT platforms lower the cost of entry to levels that smaller manufacturers can afford without large upfront infrastructure investment.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 139.0 Billion |

|

Market Size in 2026 |

USD 42.8 Billion |

|

Market Size in 2025 |

USD 36.4 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 12.5% |

|

Dominating Component |

Software |

|

Fastest Growing Component |

Hardware (Sensors) |

|

Dominating Deployment Mode |

Cloud-Based |

|

Fastest Growing Deployment Mode |

Hybrid |

|

Dominating Application |

Smart Manufacturing / Production Management |

|

Fastest Growing Application |

Digital Twin and Simulation |

|

Dominating End-Use Industry |

Automotive Manufacturing |

|

Fastest Growing End-Use Industry |

Pharmaceuticals |

|

Dominating Connectivity Technology |

Wired Connectivity |

|

Fastest Growing Connectivity Technology |

Cellular (4G/5G) |

|

Dominating Enterprise Size |

Large Enterprises |

|

Fastest Growing Enterprise Size |

Small & Medium Enterprises (SMEs) |

|

Dominating Country |

Germany |

|

Fastest Growing Country |

Spain |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Germany's Mittelstand Driving Industrial IoT Adoption at Scale

Germany's uniquely structured industrial economy, dominated by a large number of highly specialized mid-size manufacturers known collectively as the Mittelstand, is one of the most important demand drivers in the European industrial IoT market. These companies, which lead globally in specialized machine tools, automation equipment, and industrial components, are both major adopters of IoT technology for their own production processes and major developers and suppliers of IoT solutions to their customers. Germany is home to the original Industrie 4.0 initiative, launched jointly by the German government and industry associations in 2011, which established the intellectual and policy framework for smart manufacturing that has influenced industrial digitalization programs across Europe and globally.

The practical result is that Germany has the highest IoT in manufacturing adoption rate of any European country, with Siemens, Bosch, KUKA, and ifm electronic among the world's leading industrial IoT technology developers all headquartered there. The German market benefits from a dense ecosystem of solution providers, system integrators with deep manufacturing domain expertise, and a sophisticated industrial customer base that understands and demands advanced IoT capabilities. This ecosystem advantage makes Germany the largest single national market in Europe and a global reference for industrial IoT implementation best practices.

EU Digital Policy Creating Mandatory and Funded Adoption Incentives

The European Union's ambitious digital policy agenda is creating both mandated requirements and substantial financial incentives for IoT adoption in European manufacturing that have no equivalent in other major industrial regions. The EU's European Data Act, which came into force in 2023, establishes a regulatory framework for data sharing from connected industrial devices that creates common rules for how IoT data from manufacturing equipment can be accessed and shared, reducing fragmentation and encouraging investment in IoT connectivity. The EU Cyber Resilience Act is establishing mandatory cybersecurity requirements for IoT devices sold in Europe, raising the security standard baseline across the market.

On the funding side, the EU's Recovery and Resilience Facility allocated hundreds of billions of euros to member state digital transformation programs, a significant portion of which is flowing into smart manufacturing and industrial digitalization projects. Horizon Europe, the EU's research and innovation framework, is funding industrial IoT research consortia that bring together manufacturers, technology providers, and universities across Europe to develop next-generation IIoT solutions. For European manufacturers, this combination of regulatory clarity and funded support is materially reducing the risk and cost of IoT adoption, accelerating the investment case for factory digitalization programs that might otherwise have been deferred.

5G Private Networks Unlocking New Industrial IoT Capabilities

The deployment of private 5G networks within manufacturing facilities is one of the most commercially significant technology trends emerging in the European industrial IoT market, enabling the high bandwidth, ultra-low latency, and massive device density connectivity that the most demanding IoT applications require. Conventional Wi-Fi and wired industrial networks struggle to support the real-time control of large robot fleets, high-resolution video quality inspection at full production line speeds, and the dense sensor networks needed for comprehensive asset monitoring across large factory floors. Private 5G networks, which give manufacturers dedicated spectrum and network slicing capabilities within their own facilities, solve these limitations while adding the flexibility of wireless connectivity.

Ericsson and Nokia, both with major European headquarters, are the world's two leading private 5G network providers for industrial customers and are building significant European market positions in factory 5G deployments. German automakers including BMW and Mercedes-Benz have deployed private 5G networks in their manufacturing facilities and are using them to enable flexible automation, autonomous guided vehicle navigation, and real-time quality control applications. As 5G equipment costs fall and as European spectrum regulators including the German Federal Network Agency have allocated dedicated industrial spectrum bands for private networks, more manufacturing companies across Europe are expected to deploy private 5G as the connectivity backbone for their factory IoT infrastructure.

Adoption of Industry 4.0 Across European Manufacturing

Europe is the birthplace of the Industry 4.0 concept and the region with the deepest political, industrial, and financial commitment to its implementation. Germany's Industrie 4.0 platform, France's Industrie du Futur program, Italy's Piano Nazionale Industria 4.0, Spain's Industria Conectada 4.0, and equivalent programs across all major European manufacturing nations are providing strategic direction and in many cases direct financial support for factory digitalization that is translating into sustained and growing IoT investment across the continent. The European manufacturing sector's very large installed base of precision machinery and sophisticated production systems creates high-value IoT use cases including predictive maintenance, quality traceability, and production optimization where the ROI from IoT investment is demonstrable and significant. European manufacturers are also facing growing competitive pressure from Asian manufacturers who are rapidly adopting automation, creating an urgency to invest in IoT-enabled productivity improvements to maintain competitive advantage in high-quality specialized production where Europe currently leads.

Strong Government Support for Digital Manufacturing (EU Initiatives)

The EU's coordinated digital policy framework provides European manufacturing companies with a uniquely supportive environment for IoT adoption. National recovery programs funded through the EU Recovery and Resilience Facility are directing billions of euros toward manufacturing digitalization across member states, with IoT connectivity and smart factory technology among the priority investment categories. The European Alliance for Industrial Data, Edge and Cloud is creating a pan-European industrial data infrastructure that will enable interoperable data sharing across manufacturing value chains, directly supporting IoT platform adoption. Standards development through the EU's engagement with IEC and ISO on industrial communication protocols is reducing interoperability barriers that previously made large-scale IoT deployments expensive and complex. This multi-layered policy support has no equivalent in the United States or Asia and is a meaningful structural advantage for the European industrial IoT market.

AI-Driven Industrial IoT and Smart Factories

The integration of AI and machine learning with industrial IoT platforms is transforming data collection into genuine operational intelligence, creating the most compelling ROI case for IoT investment that European manufacturers have seen to date. AI models trained on sensor data from production equipment can predict mechanical failures with sufficient advance warning to schedule planned maintenance rather than emergency repairs, reducing unplanned downtime by 30 to 50% in proven deployments. AI vision systems integrated with camera IoT networks can inspect products at full production speed with defect detection accuracy that exceeds human inspection. AI scheduling optimization platforms use real-time IoT production data to dynamically adjust production plans to minimize energy use, reduce changeover time, and maximize throughput. Siemens' Industrial AI suite, SAP's AI-powered manufacturing cloud, and Bosch's IoT AI platform are among the leading European industrial AI products that are driving strong commercial adoption across the automotive, electronics, and pharmaceuticals sectors.

Increasing Adoption in SMEs Across Europe

Europe has a very large population of small and medium-sized manufacturers that have historically been underserved by industrial IoT solutions designed for large enterprise budgets and IT capabilities. This SME market, which includes hundreds of thousands of manufacturing companies across Germany, Italy, France, Spain, and other European countries, represents the largest untapped growth opportunity in the European industrial IoT market. Cloud-based IoT platforms that can be subscribed to on a per-machine monthly basis, IoT sensor kits with plug-and-play connectivity requiring no IT department to deploy, and IoT-as-a-service offerings where technology providers manage the infrastructure are progressively lowering the entry barrier for SME adoption. EU and national programs specifically targeting SME digitalization, including the European Digital Innovation Hubs that provide SMEs with subsidized access to digital technology testing and implementation support, are accelerating SME IoT adoption in ways that pure market forces alone would not achieve.

By Component: In 2026, Software to Dominate

Based on component, the Europe market for IoT in manufacturing is segmented into hardware, software, and services. In 2026, the software segment is expected to account for the largest share of the Europe IoT in manufacturing market. IoT platforms, analytics software, security solutions, and data management applications collectively represent the highest-value component category because they are sold on recurring subscription models that generate ongoing revenue, and because the intelligence delivered by analytics and AI software is where the measurable business value of IoT systems resides. Leading platforms from Siemens (MindSphere), SAP (IoT Business Services), and Bosch (IoT Suite) command premium pricing that gives the software segment the highest per-customer revenue in the European IIoT market.

However, the hardware segment, particularly sensors, is projected to register the highest CAGR during the forecast period. The expansion of IoT connectivity to more machines, more production areas, and more European SME facilities that have not yet deployed sensors is driving rapid growth in sensor procurement. As sensor costs continue falling and as plug-and-play wireless sensor solutions simplify deployment, the total number of connected industrial devices in European factories is expected to grow very rapidly, driving strong hardware segment growth.

By Deployment Mode: In 2026, Cloud-Based to Hold the Largest Share

Based on deployment mode, the Europe market for IoT in manufacturing is segmented into cloud-based, on-premises, and hybrid deployment. In 2026, the cloud-based segment is expected to account for the largest share of the Europe IoT in manufacturing market. Cloud platforms offer the fastest deployment, lowest upfront investment, automatic updates, and the ability to scale connectivity across multiple factory sites without infrastructure duplication. For SMEs and for manufacturers piloting IoT before committing to full-scale deployment, cloud is the natural entry point. GDPR compliance requirements have been addressed by major cloud providers through EU-based data centers and contractual data residency commitments, removing the primary regulatory barrier to cloud adoption in European industrial contexts.

However, the hybrid deployment segment is projected to register the highest CAGR during the forecast period. Large manufacturers with sensitive production data, especially in aerospace, defense, and pharmaceuticals, are increasingly adopting hybrid models where edge computing processes time-sensitive and sensitive data locally while aggregating anonymized analytics in the cloud. This hybrid approach provides the security of on-premises processing with the scalability and analytical power of cloud platforms, making it increasingly the preferred architecture for enterprise-scale European manufacturers.

By Application: In 2026, Smart Manufacturing to Hold the Largest Share

Based on application, the Europe IoT in manufacturing market is segmented into predictive maintenance, smart manufacturing and production management, supply chain and logistics management, energy management, remote monitoring and control, and digital twin and simulation. In 2026, the smart manufacturing and production management segment is expected to account for the largest share of the Europe IoT in manufacturing market. Process optimization and quality management applications directly improve production output quality and volume, which are the metrics most directly tied to manufacturer profitability. The very broad applicability of production management IoT across every manufacturing sector and production type makes this the largest application by revenue.

However, the digital twin and simulation segment is projected to register the highest CAGR during the forecast period. Digital twin technology, which creates real-time virtual replicas of physical production systems that can be used for simulation, testing, and optimization without interrupting actual production, is moving rapidly from research and pilot deployments into mainstream commercial adoption. Dassault Systemes, Siemens, and Hexagon, all with strong European headquarters, are the world's leading digital twin solution providers and are driving strong commercial growth of this application across European automotive, aerospace, and industrial machinery sectors.

By End-Use Industry: In 2026, Automotive Manufacturing to Hold the Largest Share

Based on end-use industry, the Europe IoT in manufacturing market is segmented into automotive manufacturing, aerospace and defense, electronics and semiconductor, food and beverage, pharmaceuticals, chemicals, machinery and heavy equipment, and others. In 2026, the automotive manufacturing segment is expected to account for the largest share of the Europe IoT in manufacturing market. European automotive manufacturing, dominated by German OEMs and their extensive European supply chains, has been at the forefront of IoT adoption for over a decade through connected production lines, quality traceability systems, and predictive maintenance platforms. The shift to electric vehicle manufacturing, which requires new production processes for battery assembly, electronics integration, and software-defined vehicle features, is driving significant new IoT investment as manufacturers build and retrofit facilities for EV production.

However, the pharmaceuticals segment is projected to register the highest CAGR during the forecast period. European pharma manufacturers face intensifying regulatory pressure for data integrity, batch traceability, and continuous process verification from the EMA and equivalent authorities, all of which are most efficiently addressed through IoT-enabled real-time monitoring and digital documentation. The growing adoption of continuous manufacturing processes in pharma, which require real-time IoT monitoring to ensure consistent drug quality, is driving accelerating IoT investment in this sector.

Europe IoT in Manufacturing Market by Country: Germany Leading, Spain Fastest Growing

The Europe IoT in manufacturing market is analyzed across Germany, the United Kingdom, France, Italy, Spain, the Netherlands, Sweden, Switzerland, and the Rest of Europe.

Germany is expected to account for the largest share of the Europe IoT in manufacturing market in 2026. Germany's dominance reflects its position as Europe's largest and most technically sophisticated manufacturing economy, the home of Industrie 4.0, and the headquarters of the world's leading industrial IoT technology providers including Siemens, Bosch, SAP, and KUKA. German manufacturers, ranging from the global automotive OEMs in Bavaria and Baden-Wurttemberg to the precision engineering Mittelstand companies of North Rhine-Westphalia, are among the world's most active and sophisticated industrial IoT adopters. Germany's Federal Ministry for Economic Affairs and Climate Action has consistently supported industrial digitalization through funding programs, regulatory frameworks, and the Plattform Industrie 4.0 ecosystem that brings technology providers and manufacturers together to drive adoption. The very high value-added per employee in German manufacturing creates a strong financial return from IoT investments that improve productivity and quality, and the country's dense network of IoT technology developers, Fraunhofer Institute research centers, and industrial system integrators provides the ecosystem depth needed to support complex IIoT implementations at scale.

The United Kingdom is the second-largest IoT in manufacturing market in Europe, with a strong industrial base in aerospace, automotive, life sciences, and advanced engineering that generates significant demand for connected factory solutions. UK government programs including Made Smarter and the High Value Manufacturing Catapult are actively supporting IoT adoption across UK manufacturing. France's strong industrial base in aerospace, automotive, and defense, combined with Dassault Systemes as a world-leading digital manufacturing software company, makes it a significant and growing IoT in manufacturing market. Italy's manufacturing sector, particularly its highly specialized machinery, fashion, and food processing industries, is investing in IoT connectivity as part of the Piano Nazionale Industria 4.0 program, which offers generous tax incentives for digital manufacturing investment. Sweden, despite its smaller size, has a highly advanced manufacturing technology sector and is home to Hexagon AB, Ericsson, and Atlas Copco, making it an important market and innovation hub. Spain is expected to register the highest growth rate among European countries through the forecast period, driven by Spain's Recovery, Transformation and Resilience Plan directing significant EU funds toward manufacturing digitalization, a growing and dynamic manufacturing sector including automotive, machinery, and food processing, and a starting point of lower IoT penetration that creates more room for rapid growth than more mature markets.

The Europe IoT in manufacturing market is dominated by large European industrial technology and software companies that combine deep manufacturing domain expertise with IIoT platform capabilities, alongside telecommunications companies providing the connectivity infrastructure, IT services companies supporting system integration, and specialist industrial IoT software providers. Europe's strong position in this market reflects the concentration of the world's leading industrial automation, enterprise software, and manufacturing technology companies in Germany, France, Sweden, and Switzerland.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' IoT platform capabilities, customer segments, geographic presence, and recent strategic developments. Some of the key players operating in the Europe IoT in manufacturing market include Siemens AG (Germany), Bosch GmbH (Germany), SAP SE (Germany), ABB Ltd. (Switzerland), Schneider Electric SE (France), Ericsson AB (Sweden), Nokia Corporation (Finland), KUKA AG (Germany), ifm electronic GmbH (Germany), Software AG (Germany), Atos SE (France), Capgemini SE (France), Orange Business Services (France), Hexagon AB (Sweden), and Dassault Systemes SE (France), among others.

The Europe IoT in manufacturing market is expected to reach USD 139.0 billion by 2036 from an estimated USD 42.8 billion in 2026, at a CAGR of 12.5% during the forecast period 2026-2036.

In 2026, the software segment is expected to hold the largest share of the Europe IoT in manufacturing market, driven by IoT platforms and analytics software from Siemens, SAP, and Bosch commanding premium recurring subscription revenues that make software the highest-value component category.

The hardware segment, particularly sensors, is expected to register the highest CAGR during the forecast period 2026-2036, driven by the rapid expansion of IoT connectivity to previously unconnected machines across both large enterprises and the large SME population across Europe.

In 2026, the smart manufacturing and production management segment is expected to hold the largest share of the Europe IoT in manufacturing market, reflecting process optimization and quality management being the applications with the most direct impact on manufacturer profitability and therefore the highest adoption priority across all manufacturing sectors.

Germany is expected to dominate the Europe IoT in manufacturing market in 2026, driven by its position as Europe's largest manufacturing economy, the home of Industrie 4.0, and the headquarters of the world's leading industrial IoT technology providers including Siemens, Bosch, SAP, and KUKA.

The market is primarily driven by the deep and politically supported Industry 4.0 transformation across European manufacturing, including direct EU and national government funding programs and regulatory frameworks that are materially accelerating IoT adoption, combined with the competitive pressure on European manufacturers to improve productivity and quality through connected factory intelligence.

Key players are Siemens AG (Germany), Bosch GmbH (Germany), SAP SE (Germany), ABB Ltd. (Switzerland), Schneider Electric SE (France), Ericsson AB (Sweden), Nokia Corporation (Finland), KUKA AG (Germany), ifm electronic GmbH (Germany), Software AG (Germany), Atos SE (France), Capgemini SE (France), Orange Business Services (France), Hexagon AB (Sweden), and Dassault Systemes SE (France), among others.

Spain is expected to register the highest growth rate in the Europe IoT in manufacturing market during the forecast period 2026-2036, driven by significant EU Recovery and Resilience Facility funding directed toward manufacturing digitalization, a growing automotive and machinery manufacturing sector, and a lower current IoT penetration that provides more room for rapid adoption relative to more mature markets.

Published Date: Jan-2025

Published Date: Sep-2024

Published Date: Oct-2022

Published Date: Jul-2022

Published Date: Jun-2019

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates