Resources

About Us

Quantum Computing Market Size, Share & Trends Analysis by Offering (Hardware, Software, Services/QaaS), Technology Type (Superconducting Qubits), Deployment Model, Application, End User, and Enterprise Size - Global Opportunity Analysis & Industry Forecast (2026-2036)

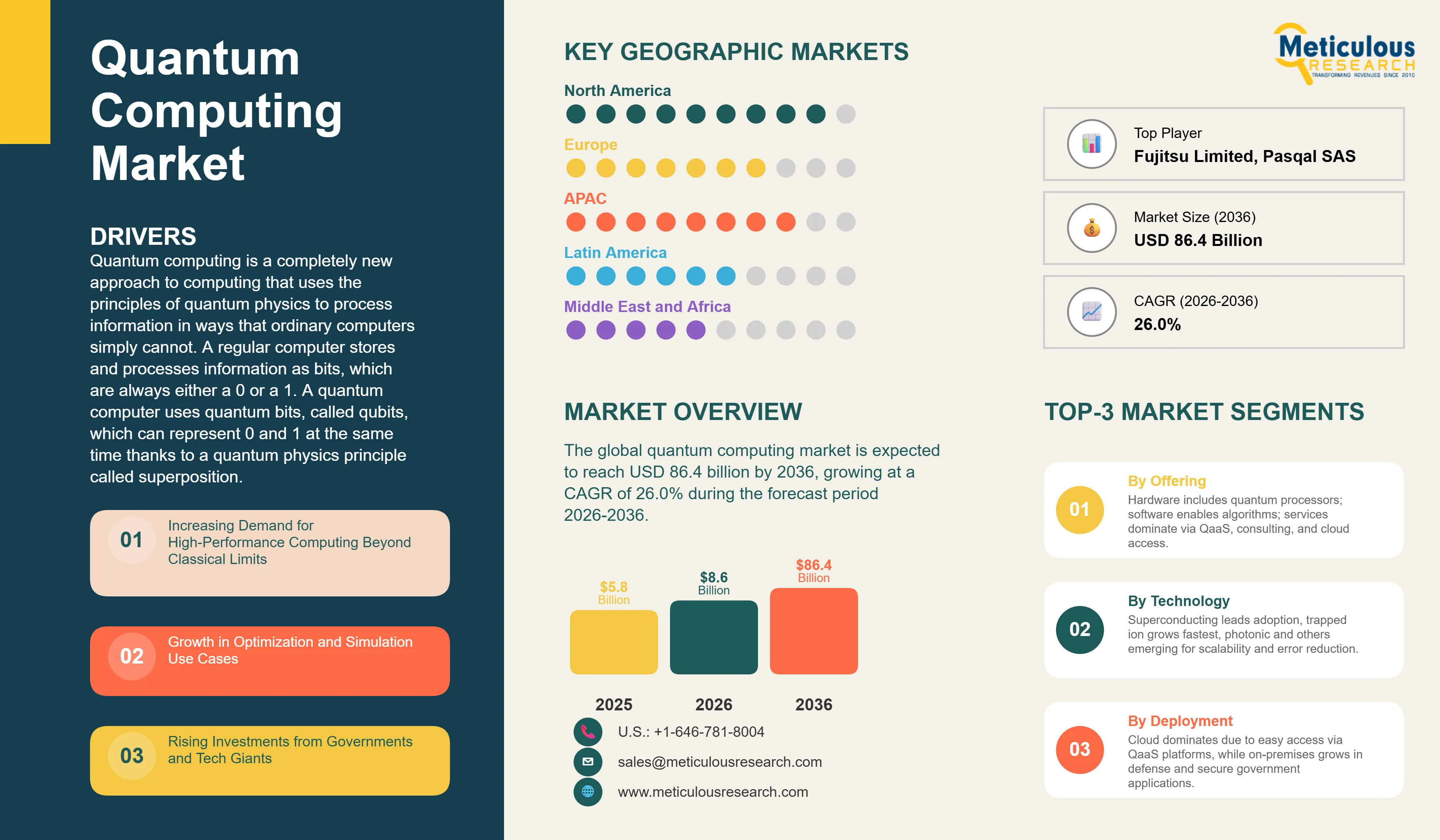

Report ID: MRICT - 1041922 Pages: 280 Apr-2026 Formats*: PDF Category: Information and Communications Technology Delivery: 24 to 72 Hours Download Free Sample ReportThe global quantum computing market was valued at USD 5.8 billion in 2025. This market is expected to reach USD 86.4 billion by 2036 from an estimated USD 8.6 billion in 2026, growing at a CAGR of 26.0% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Quantum computing is a completely new approach to computing that uses the principles of quantum physics to process information in ways that ordinary computers simply cannot. A regular computer stores and processes information as bits, which are always either a 0 or a 1. A quantum computer uses quantum bits, called qubits, which can represent 0 and 1 at the same time thanks to a quantum physics principle called superposition. This means a quantum computer can explore many possible solutions to a problem simultaneously, rather than testing each possibility one at a time the way a conventional computer does. For certain specific types of problems, particularly those involving finding the best answer among an enormous number of options or simulating how molecules and chemicals interact, this approach can solve problems that would take today's most powerful conventional computers millions of years to work through.

The market is growing because organizations in industries like banking, pharmaceutical research, logistics, and cybersecurity are starting to recognize that quantum computing could give them a significant competitive advantage for specific high-value problems they currently cannot solve efficiently. Banks want to use quantum computers to optimize their investment portfolios and detect fraud in ways that account for many more variables simultaneously than current systems can handle. Drug companies want to use quantum simulation to design new medicines by modeling how drug molecules interact with the human body at the atomic level, which is too complex for conventional computers. Logistics companies want to use quantum optimization to find the ideal delivery routes and supply chain configurations across networks so large and complex that current software cannot find truly optimal solutions.

Two significant opportunities are shaping the near-term commercial development of the market. Cloud-based quantum computing services, often called Quantum-as-a-Service, allow businesses to access quantum computing power over the internet from platforms operated by IBM, Google, Amazon, and Microsoft without needing to buy or operate expensive quantum hardware themselves. This dramatically lowers the barrier to experimenting with quantum computing and is the primary commercial revenue generator in the current market. The growing integration of quantum computing with conventional artificial intelligence systems is also a significant opportunity, as hybrid quantum-classical computing approaches that use quantum processing for the most computationally demanding parts of an AI workload and conventional computing for the rest are already showing practical performance advantages for certain types of machine learning problems.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 86.4 Billion |

|

Market Size in 2026 |

USD 8.6 Billion |

|

Market Size in 2025 |

USD 5.8 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 26.0% |

|

Dominating Offering |

Services (QaaS) |

|

Fastest Growing Offering |

Hardware |

|

Dominating Technology Type |

Superconducting Qubits |

|

Fastest Growing Technology Type |

Trapped Ion |

|

Dominating Deployment Model |

Cloud-Based Quantum Computing |

|

Fastest Growing Deployment Model |

On-Premises Quantum Systems |

|

Dominating Application |

Simulation and Modeling |

|

Fastest Growing Application |

Machine Learning and AI |

|

Dominating End User |

BFSI |

|

Fastest Growing End User |

Healthcare & Pharmaceuticals |

|

Dominating Enterprise Size |

Large Enterprises |

|

Fastest Growing Enterprise Size |

SMEs |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Cloud Access Making Quantum Computing Available to Businesses Today

The most commercially significant trend in the quantum computing market is the rapid expansion of cloud-based quantum computing services that allow businesses to run quantum algorithms on real quantum hardware over the internet, without the enormous cost and complexity of owning and operating quantum equipment themselves. IBM's Quantum Network provides access to its quantum processors through the cloud to over 400 organizations worldwide including major companies, universities, and research institutions. Amazon Web Services offers quantum computing access through its Braket service supporting hardware from multiple quantum computer manufacturers. Microsoft Azure provides quantum-inspired optimization services and is building toward broader quantum access. Google offers access to its quantum hardware through its Google Quantum AI cloud platform.

The QaaS model is important because it is making quantum computing practically accessible to businesses that want to explore how the technology could benefit their specific problems, years before quantum hardware will be affordable enough for most organizations to own. A pharmaceutical company can run drug discovery simulations on IBM's or Google's quantum hardware for the cost of cloud computing fees, which is far more affordable than building or buying a quantum computer costing tens of millions of dollars. As competition among cloud providers for quantum computing customers intensifies and as quantum hardware becomes more capable, the QaaS market is expected to grow very rapidly, making it the primary revenue driver of the quantum computing market through the forecast period.

IBM and Google Quantum Hardware Progress Establishing Commercial Timelines

The steady progress being made by IBM and Google in improving the capability and reliability of their quantum processors is providing the clearest evidence of when quantum computing is likely to become commercially useful for specific real-world applications, which is driving business planning and investment decisions across the industries that expect to be early quantum computing customers. IBM has mapped out a detailed multi-year roadmap targeting systems with thousands of high-quality qubits, and has been consistently delivering on that roadmap with each annual hardware generation improving both the number of qubits and their quality in terms of error rates and stability. IBM's 2023 announcement of 1,000-plus qubit processors and its progress toward error-corrected quantum computing represent important milestones that the industry takes seriously as indicators of commercial timeline.

Google's 2024 demonstration of its Willow quantum chip, which showed that increasing qubit count actually reduces error rates, solving a fundamental technical challenge that had constrained quantum computing progress, was widely seen as a major step toward fault-tolerant quantum computing. These hardware milestones are translating into more concrete commercial planning by companies in finance, pharmaceuticals, and logistics that are building internal quantum computing expertise and running proof-of-concept workloads on cloud quantum hardware today, so they are ready to extract competitive advantage when the hardware reaches the capability thresholds needed for their specific applications.

Governments Treating Quantum Computing as a National Security Priority

A striking feature of the quantum computing investment landscape is how aggressively governments around the world are funding quantum computing research and development, treating it as a strategic national priority comparable in importance to artificial intelligence. The United States has committed over USD 1.8 billion through the National Quantum Initiative Act and has additional quantum computing investments through DARPA, Department of Energy, and National Science Foundation programs. The European Union launched a EUR 1 billion Quantum Flagship program. China's government has invested an estimated USD 15 billion or more in quantum research and has established the world's largest quantum communication network. The UK, Canada, Germany, Australia, Japan, India, and many other nations have each committed national quantum strategies with significant public investment commitments.

The primary security motivation for this government investment is the recognition that sufficiently powerful quantum computers could break the encryption systems that currently protect banking transactions, government communications, military secrets, and internet privacy globally. Any nation that develops a powerful quantum computer before others could potentially decrypt encrypted communications that its adversaries had thought were permanently secure. This creates an urgent and strategic motivation for governments to lead in quantum computing development while also investing heavily in post-quantum encryption standards that will remain secure even against quantum attacks. The U.S. National Institute of Standards and Technology finalized its first post-quantum cryptography standards in 2024, and financial institutions and government agencies globally are beginning the complex and expensive process of updating their encryption systems, creating a large market for quantum cybersecurity products and consulting services alongside the quantum hardware and software markets.

Increasing Demand for High-Performance Computing Beyond Classical Limits

The fundamental driver of the quantum computing market is the existence of important and commercially valuable problems that conventional computers simply cannot solve efficiently, no matter how powerful they become. These include simulating the quantum mechanical behavior of molecules for drug discovery and materials science, optimizing extremely complex logistics and financial systems across thousands of variables simultaneously, breaking and creating cryptographic codes, and training very large machine learning models. For these specific problem types, quantum computers offer the potential to find solutions in hours or days that would take conventional supercomputers thousands to millions of years to compute. The pharmaceutical industry alone spends over USD 180 billion annually on drug research and development, and being able to accurately simulate how drug candidates interact with disease proteins before costly physical experiments could dramatically reduce the time and cost of bringing new medicines to market. Similarly, the financial services industry manages portfolios worth hundreds of trillions of dollars and faces optimization and risk management problems so complex that truly optimal solutions currently require approximations. The commercial value available to early users of quantum computing for these specific high-value applications is creating strong and sustained demand for quantum computing investment and development.

Rising Investments from Governments and Tech Giants

The combination of very large government funding commitments and the significant quantum computing investment programs of technology giants including IBM, Google, Microsoft, Amazon, and Intel is providing the sustained capital base that quantum computing development requires to progress from research to commercial product. IBM has invested billions of dollars in its quantum computing program over more than a decade and has the most commercially deployed quantum computing infrastructure in the world through its IBM Quantum Network. Google's quantum computing investment through its Google Quantum AI division has produced some of the most technically significant quantum computing milestones, including the Sycamore supremacy demonstration and the Willow chip error reduction breakthrough. Microsoft is pursuing a fundamentally different approach through topological qubits and has committed to making quantum computing available through Azure with its own hardware development program. Amazon's AWS Braket and its investment in IonQ, a trapped ion quantum computing company, reflect its strategy of providing quantum access across multiple hardware technologies. These very large and sustained investments from well-funded institutions are accelerating the timeline to commercially useful quantum computing and creating a growing industry ecosystem of quantum hardware manufacturers, software developers, and application specialists.

Quantum Advantage in Drug Discovery and Materials Science

The most commercially compelling near-term quantum computing opportunity is in molecular simulation for pharmaceutical drug discovery and materials science, where quantum computers can simulate the quantum mechanical behavior of molecules accurately in a way that classical computers cannot. The drug discovery process currently takes an average of 10 to 15 years and costs USD 1 to 3 billion per approved drug, largely because testing candidate drug molecules through biological experiments to determine whether they work is expensive and slow. Quantum computers that can accurately predict how a drug candidate molecule will interact with a disease-related protein in the human body from a computational simulation rather than a physical experiment could eliminate years of costly experimental work from the drug development process, representing enormous commercial value to pharmaceutical companies. Roche, Pfizer, and several other major pharmaceutical companies are already running quantum computing proof-of-concept programs in drug discovery, and as quantum hardware becomes more capable, pharmaceutical companies that have built quantum computing expertise early are expected to gain significant competitive advantages in research productivity.

Growth of Quantum-as-a-Service (QaaS) Platforms

The Quantum-as-a-Service model, which allows businesses to access quantum computing capabilities over the internet without owning quantum hardware, is the most commercially immediate and fastest-growing opportunity in the quantum computing market. By making quantum hardware accessible through standard cloud computing interfaces with pay-per-use pricing starting at a few dollars per quantum processing unit hour, QaaS platforms allow any company or research institution to experiment with quantum computing and develop quantum applications without the prohibitive capital cost of purchasing and operating quantum hardware. This accessibility is creating a rapid growth in the number of organizations exploring quantum computing and developing quantum algorithms, which is building the skills, software tools, and application knowledge base that will accelerate commercial adoption when hardware capability improves. For cloud providers, the QaaS business represents a growing recurring revenue stream that is commercially valuable today even before quantum computers reach the capability levels required for major industry use cases, making it an attractive business to invest in now while the technology is still developing.

By Offering: In 2026, Services to Dominate

Based on offering, the global quantum computing market is segmented into hardware, software, and services. In 2026, the services segment is expected to account for the largest share of the global quantum computing market. The services segment encompasses cloud-based Quantum-as-a-Service access fees, consulting and integration services that help organizations understand and apply quantum computing to their business problems, and training services for quantum computing skills development. QaaS is currently the primary commercial revenue channel for the quantum computing market because it allows IBM, Google, Amazon, and Microsoft to generate immediate and growing revenue from their quantum hardware investments while the hardware is still far from the capability levels needed for most commercial applications. The large established customer base of these cloud providers means that QaaS can be marketed and sold to existing enterprise customers through existing commercial relationships.

However, the hardware segment is projected to register the highest CAGR during the forecast period. As quantum hardware progresses toward the qubit quality and quantity levels required for fault-tolerant quantum computing, the addressable market for complete quantum computing systems purchased and operated on-premises by governments, large enterprises, and national laboratories will grow significantly. Quantum hardware sales to government and defense customers, national laboratories, and eventually large pharmaceutical and financial institutions are expected to drive very rapid hardware revenue growth from the current relatively small base.

By Technology Type: In 2026, Superconducting Qubits to Hold the Largest Share

Based on technology type, the global quantum computing market is segmented into superconducting qubits, trapped ion, quantum annealing, photonic quantum computing, topological quantum computing, and neutral atom quantum computing. In 2026, the superconducting qubits segment is expected to account for the largest share of the global quantum computing market. Superconducting qubit technology, used by IBM, Google, and Rigetti, has the most commercially deployed and accessible quantum computing infrastructure in the world, with the largest number of available quantum processors accessible through cloud platforms and the broadest ecosystem of quantum software tools and developer communities. The very large investment by IBM and Google in superconducting qubit systems over many years has established this as the current dominant technology approach by market presence and available qubit count.

However, the trapped ion segment is projected to register the highest CAGR during the forecast period. Trapped ion quantum computers, which use individual atoms suspended in electromagnetic fields as qubits rather than engineered superconducting circuits, have demonstrated significantly better qubit quality in terms of error rates and coherence times than current superconducting systems, even though they currently have fewer qubits. IonQ, Quantinuum (formerly Honeywell), and Oxford Ionics are leading developers of trapped ion quantum computers, and the superior qubit quality of these systems makes them attractive for applications where accuracy is more important than raw qubit count, particularly in the near-term before error correction makes qubit quality less critical.

By Deployment Model: In 2026, Cloud-Based to Hold the Largest Share

Based on deployment model, the global quantum computing market is segmented into on-premises quantum systems and cloud-based quantum computing. In 2026, the cloud-based quantum computing segment is expected to account for the largest share of the global quantum computing market. Cloud access is the primary way that the vast majority of organizations interact with quantum computing today, and the QaaS platforms of IBM, Amazon, Google, and Microsoft collectively serve hundreds of thousands of users globally. The extremely high cost, specialized infrastructure requirements, and deep technical expertise needed to operate quantum hardware directly makes cloud access the only practical option for the overwhelming majority of quantum computing users and developers today.

However, the on-premises segment is projected to register the highest CAGR during the forecast period. Government agencies, defense organizations, and major national laboratories in the U.S., EU, China, and elsewhere are investing in on-premises quantum systems for classified workloads that cannot be sent to commercial cloud platforms for security reasons, and IBM's and Quantinuum's growing sales of on-premises quantum systems to government customers are establishing this as a growing commercial channel. As quantum hardware improves and prices fall, more organizations will evaluate on-premises deployment for sensitive workloads.

By Application: In 2026, Simulation and Modeling to Hold the Largest Share

Based on application, the global quantum computing market is segmented into optimization problems, simulation and modeling, machine learning and AI, cryptography and cybersecurity, financial services applications, healthcare and life sciences, and other emerging applications. In 2026, the simulation and modeling segment is expected to account for the largest share of the global quantum computing market. Molecular simulation and materials science modeling represent the applications where quantum computing has the most clearly identified potential for genuine quantum advantage over classical computers, and consequently these application areas have attracted the largest number of enterprise quantum computing programs. Pharmaceutical companies, chemical manufacturers, and materials science researchers are the most active users of quantum simulation tools, and the large commercial value of improved drug discovery efficiency ensures strong continued investment in this application area.

However, the machine learning and AI segment is projected to register the highest CAGR during the forecast period. The rapid growth and enormous commercial value of AI applications is creating strong interest in quantum approaches that could accelerate machine learning model training, improve pattern recognition accuracy, or enable new types of AI models that are difficult to train on classical hardware. Quantum machine learning is still an early-stage research field, but the combination of the world's two most highly funded and attention-getting technology categories, quantum computing and AI, is driving rapid research progress and strong commercial interest that is translating into growing investment in quantum machine learning applications.

By End User: In 2026, BFSI to Hold the Largest Share

Based on end user, the global quantum computing market is segmented into BFSI, healthcare and pharmaceuticals, government and defense, IT and telecommunications, energy and utilities, manufacturing, and others. In 2026, the BFSI segment is expected to account for the largest share of the global quantum computing market. Banks, financial services firms, and insurance companies are among the earliest and most active adopters of quantum computing, driven by the very large commercial value of quantum optimization applications for portfolio management, risk analysis, fraud detection, and high-frequency trading systems. JPMorgan Chase, Goldman Sachs, HSBC, and several other major financial institutions have established active quantum computing research programs and are running pilot applications on cloud quantum systems today. The financial services industry also has a strong motivation to invest in post-quantum cryptography as part of its cybersecurity programs, creating additional quantum-related spending.

However, the healthcare and pharmaceuticals segment is projected to register the highest CAGR during the forecast period. As quantum hardware improves and molecular simulation becomes more practically useful, pharmaceutical companies are expected to significantly increase their quantum computing investment. Drug discovery, genomics analysis, and personalized medicine applications that leverage quantum computing are projected to generate enormous commercial value, and the pharmaceutical companies that build quantum computing expertise early are expected to gain significant research productivity advantages that drive competitive investment in the sector.

By Enterprise Size: In 2026, Large Enterprises to Hold the Largest Share

Based on enterprise size, the global quantum computing market is segmented into large enterprises and SMEs. In 2026, the large enterprises segment is expected to account for the largest share of the global quantum computing market. Large enterprises including major banks, pharmaceutical companies, defense contractors, and technology firms have the R&D budgets, specialized technical talent, and long-term strategic vision required to invest in quantum computing when it is still in early commercial stages and when near-term financial returns are uncertain. The IBM Quantum Network, Google's quantum research partnerships, and similar programs are primarily built around large enterprise customers and national institutions that can make multi-year commitments to quantum computing exploration.

However, the SMEs segment is projected to register the highest CAGR during the forecast period. The growth of QaaS platforms with accessible pricing, the development of quantum programming tools that do not require a PhD in physics to use, and the growing availability of quantum application templates and pre-built algorithms for specific business problems are progressively making quantum computing accessible to smaller companies that cannot afford dedicated quantum research teams. As quantum computing moves from exploration to commercial application, SMEs in sectors such as logistics, financial services, and pharmaceuticals will increasingly find that cloud-based quantum optimization and simulation services are within their budget and relevant to their specific business challenges.

Quantum Computing Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global quantum computing market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global quantum computing market. The United States is home to the world's leading quantum computing companies including IBM, Google, Microsoft, Amazon Web Services, IonQ, Rigetti, PsiQuantum, and D-Wave, and the U.S. government has made quantum computing a national priority through the National Quantum Initiative Act with multi-billion-dollar funding commitments through the Department of Energy, National Science Foundation, DARPA, and the National Security Agency. IBM's quantum computing program, headquartered in New York, operates the largest commercially deployed quantum computing infrastructure in the world with dozens of quantum processors accessible through its cloud platform and an expanding network of over 400 partner organizations. Google's quantum AI headquarters in California has produced some of the most important technical milestones in quantum computing history. Canada's strong quantum computing ecosystem, including University of Waterloo's Institute for Quantum Computing and companies including D-Wave and Xanadu, contributes significantly to North America's market leadership. The combination of the world's largest concentration of quantum computing talent, technology companies, and government funding makes North America the clear global market leader.

However, the Asia-Pacific quantum computing market is expected to grow at the fastest CAGR during the forecast period. China has made quantum computing a top national strategic priority and has invested an estimated USD 15 billion or more in quantum research and development, including the construction of the world's largest quantum communication network connecting several cities. Chinese quantum computing companies including Origin Quantum and SpinQ are developing domestic quantum hardware and software capabilities, and Alibaba has invested in quantum computing research through its DAMO Academy. Japan's national quantum strategy has committed significant funding to quantum computing through a national strategy targeting fault-tolerant quantum computing, with Fujitsu and Toshiba as leading domestic quantum developers. South Korea, India, Australia, and Singapore all have active national quantum programs creating growing domestic quantum computing investment and adoption. The strong technology manufacturing capabilities of Asia-Pacific countries also make the region well-positioned to contribute to quantum hardware supply chains as production scales up.

Europe is a strong and actively developing quantum computing market with significant public investment through the EUR 1 billion EU Quantum Flagship program and well-established research centers in Germany, the Netherlands, France, the UK, and Switzerland. European quantum computing companies including IQM in Finland, Alice and Bob in France, and Pasqal in France are developing competitive quantum hardware technologies. The UK's National Quantum Computing Centre and Germany's quantum computing programs represent important centers of European quantum computing development. The strong European industrial base in pharmaceutical research, financial services, and advanced manufacturing provides a large potential customer base for quantum computing services as the technology matures.

The quantum computing market includes large technology companies that have built quantum computing programs as part of their broader computing and cloud platform businesses, pure-play quantum computing companies focused exclusively on quantum hardware and software, and a growing group of software and applications companies building quantum-enabled products for specific industries. Competition is based on qubit quality and quantity, error rates, cloud platform capabilities and accessibility, software developer ecosystem quality, enterprise customer relationships, and the commercial relevance of demonstrated use cases.

IBM leads the commercial quantum computing market with the largest deployed quantum computing infrastructure, the most accessible cloud-based quantum systems through IBM Quantum, and the broadest ecosystem of enterprise customers and research partners through the IBM Quantum Network. Google has produced some of the most technically significant quantum computing milestones and operates a strong quantum computing cloud platform. Microsoft is pursuing quantum computing through its Azure Quantum platform and a differentiated approach using topological qubits through its dedicated research program. Amazon Web Services provides access to quantum hardware from multiple vendors through AWS Braket. IonQ is the leading pure-play public quantum computing company and uses trapped ion technology that delivers high qubit quality. Quantinuum, the combination of Honeywell Quantum Solutions and Cambridge Quantum, is a major player in both hardware and quantum software. D-Wave is a pioneer in quantum annealing technology with the longest commercial quantum computing history. PsiQuantum is pursuing the largest scale silicon photonic quantum computing program, targeting fault-tolerant quantum computing at a scale none of its competitors have yet attempted.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' technology platforms, hardware capabilities, cloud service offerings, customer relationships, geographic presence, and recent strategic developments. Some of the key players operating in the global quantum computing market include IBM Corporation (U.S.), Google LLC (U.S.), Microsoft Corporation (U.S.), Amazon Web Services Inc. (U.S.), D-Wave Systems Inc. (Canada), IonQ Inc. (U.S.), Rigetti Computing Inc. (U.S.), Honeywell International Inc./Quantinuum (U.S./UK), Intel Corporation (U.S.), Fujitsu Limited (Japan), Toshiba Corporation (Japan), Alibaba Group Holding Limited (China), PsiQuantum Corp. (U.S.), Xanadu Quantum Technologies Inc. (Canada), and Pasqal SAS (France), among others.

The global quantum computing market is expected to reach USD 86.4 billion by 2036 from an estimated USD 8.6 billion in 2026, at a CAGR of 26.0% during the forecast period 2026-2036.

In 2026, the services segment is expected to hold the largest share of the global quantum computing market, driven by cloud-based Quantum-as-a-Service platforms from IBM, Google, Amazon, and Microsoft being the primary commercial channel through which organizations access quantum computing today.

The hardware segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the growing procurement of on-premises quantum systems by government agencies, national laboratories, and large enterprises as hardware capability improves and prices become more accessible.

In 2026, the simulation and modeling segment is expected to hold the largest share of the global quantum computing market, driven by molecular simulation for drug discovery and materials science representing the application category with the clearest near-term potential for genuine quantum advantage.

In 2026, the BFSI segment is expected to hold the largest share of the global quantum computing market, driven by financial institutions being among the earliest and most active enterprise adopters of quantum computing for portfolio optimization, risk analysis, fraud detection, and cybersecurity applications.

The market is primarily driven by the existence of commercially important problems in drug discovery, financial optimization, and cryptography that conventional computers cannot solve efficiently and that quantum computers can address, and by the very large and sustained investment programs of technology giants including IBM, Google, Microsoft, and Amazon alongside significant government funding from the U.S., EU, China, and other nations treating quantum computing as a strategic national priority.

Key players are IBM Corporation (U.S.), Google LLC (U.S.), Microsoft Corporation (U.S.), Amazon Web Services Inc. (U.S.), D-Wave Systems Inc. (Canada), IonQ Inc. (U.S.), Rigetti Computing Inc. (U.S.), Honeywell International Inc./Quantinuum (U.S./UK), Intel Corporation (U.S.), Fujitsu Limited (Japan), Toshiba Corporation (Japan), Alibaba Group Holding Limited (China), PsiQuantum Corp. (U.S.), Xanadu Quantum Technologies Inc. (Canada), and Pasqal SAS (France), among others.

Asia-Pacific is expected to register the highest growth rate in the global quantum computing market during the forecast period 2026-2036, driven by China's very large national quantum investment program, Japan's national quantum strategy, and the growing quantum computing programs of South Korea, India, Australia, and Singapore.

Published Date: Feb-2026

Published Date: Feb-2026

Published Date: Feb-2026

Published Date: Aug-2025

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates