Resources

About Us

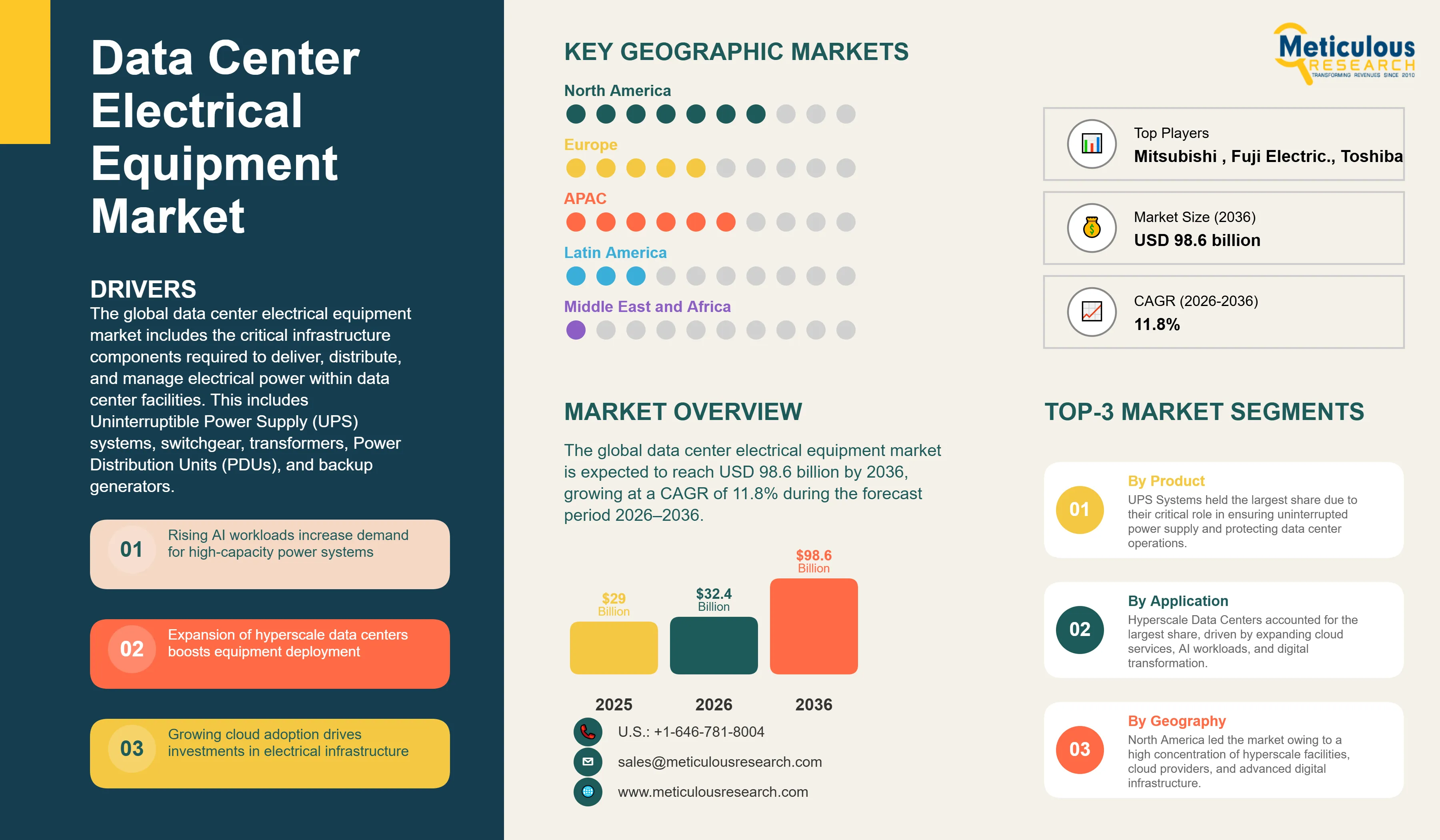

The global data center electrical equipment market was valued at USD 32.4 billion in 2026. This market is expected to reach USD 98.6 billion by 2036, growing at a CAGR of 11.8% during the forecast period 2026–2036.

The global data center electrical equipment market includes the critical infrastructure components required to deliver, distribute, and manage electrical power within data center facilities. This includes Uninterruptible Power Supply (UPS) systems, switchgear, transformers, Power Distribution Units (PDUs), and backup generators. As the backbone of data center reliability, this equipment ensures that IT loads remain powered during utility outages and electrical disturbances. The market is currently undergoing a significant transformation driven by the huge scale of hyperscale data centers and the increasing power density of artificial intelligence (AI) workloads. According to the International Energy Agency (IEA), data centers accounted for approximately 1.5% of global electricity consumption in 2024, a figure that is projected to double by 2030, necessitating a corresponding expansion in electrical infrastructure.

The growth of the overall data center electrical equipment market is primarily fueled by the rapid proliferation of cloud services and the global shift toward digital economies. JLL Research projects that the data center sector will add 97 GW of new capacity between 2025 and 2030, effectively doubling the market's footprint. This expansion is characterized by a shift toward larger, more power-intensive facilities. Bloom Energy reports that by 2030, one in five data center campuses will exceed gigawatt scale, rising to one in three by 2035. At this scale, the complexity of electrical distribution increases exponentially, requiring advanced medium-voltage switchgear and high-capacity UPS systems that can provide millisecond-level response times to power fluctuations.

However, the market faces significant restraints, most notably grid connection delays and supply chain constraints. Utility time-to-power for new data center projects is currently 1.5-2 years longer than what hyperscalers and colocation providers anticipate, creating a bottleneck for market expansion. Additionally, the industry is grappling with extended lead times for critical components like transformers and high-voltage switchgear, which can exceed 50-80 weeks in some regions. Furthermore, the transition to sustainable energy sources requires data center operators to integrate microgrids and on-site renewable generation, adding a layer of complexity to the electrical design and increasing initial capital expenditure by 30-50% compared to traditional grid-only connections.

Despite these challenges, the emergence of smart power technologies and the integration of IoT-enabled electrical equipment present substantial growth opportunities. 'Smart' electrical systems provide real-time data on energy consumption and equipment health, allowing for predictive maintenance and optimized power usage. Geographic expansion in Asia-Pacific, driven by rapid urbanization and government digitalization initiatives in China and India, further supports the market's long-term outlook. The integration of liquid cooling systems also creates a demand for specialized electrical equipment capable of operating in proximity to immersion and direct-to-chip cooling infrastructures.

Click here to: Get Free Sample Pages of this Report

The primary driver for the global data center electrical equipment market is the exponential growth in AI-driven power density. Traditional data center racks typically operate at 5-10kW, but AI and machine learning workloads have pushed this density to 50-100kW per rack. This shift requires a fundamental redesign of the power distribution chain, driving demand for high-capacity Power Distribution Units (PDUs), advanced switchgear, and liquid-cooled UPS systems. S&P Global/451 Research estimates that global power demand from data centers will increase from 860 TWh in 2025 to 1,587 TWh by 2030, a surge largely attributed to the deployment of AI infrastructure.

Another key driver is the proliferation of hyperscale data centers. As organizations migrate their operations to the cloud, major providers like Amazon, Google, and Microsoft are building massive facilities that require robust and redundant electrical systems. These hyperscale facilities often employ 2N or N+1 redundancy configurations, effectively doubling the amount of electrical equipment required per megawatt of IT load. The U.S. Department of Energy (DOE) reports that data center load growth has tripled over the past decade, and this trend is expected to continue as cloud adoption deepens globally.

A major restraint is the increasing delay in grid connections and utility power delivery. As data center power requirements reach the gigawatt scale, existing utility grids often lack the capacity to support new projects without significant upgrades. Bloom Energy reports that utility time-to-power is now 1.5-2 years longer than expected, forcing data center providers to delay the commissioning of new facilities. This bottleneck not only slows market growth but also increases the cost of project financing. Additionally, the rising cost of raw materials such as copper and electrical steel has pushed up the prices of transformers and generators, straining the capital budgets of data center operators.

The integration of sustainable energy and microgrid technologies offers a significant growth opportunity. To meet sustainability goals and mitigate grid reliability issues, data center operators are increasingly investing in on-site renewable generation (solar, wind) and battery energy storage systems (BESS). This creates demand for specialized electrical equipment such as microgrid controllers, bi-directional inverters, and high-capacity energy storage units. Furthermore, the growth of edge computing, where data is processed closer to the end user, creates a market for compact, modular electrical systems designed for smaller, decentralized data center environments.

Supply chain constraints remain a critical challenge for the industry. The lead times for high-voltage switchgear and transformers have reached historic highs, often exceeding 12-18 months. This makes long-term planning difficult for data center developers and can lead to project cancellations or significant cost overruns. Additionally, as electrical equipment becomes more 'smart' and interconnected, cybersecurity risks have emerged as a major concern. Protecting digital electrical infrastructure from grid-level cyber threats requires robust security protocols and continuous monitoring, adding a layer of operational complexity for data center managers.

The data center electrical equipment industry is witnessing a shift from individual data center buildings to massive gigawatt-scale campuses. These campuses function as independent power ecosystems, often featuring their own high-voltage substations and dedicated utility interconnections. Bloom Energy reports that by 2035, one in three data center campuses will reach this scale. This trend significantly increases the demand for high-capacity electrical equipment and specialized engineering services to manage the immense power loads and ensure grid stability.

Environmental regulations and sustainability initiatives are driving a shift away from SF6-insulated switchgear. SF6 is a potent greenhouse gas, and manufacturers are increasingly developing vacuum-based and air-insulated alternatives for medium-voltage applications. This trend is particularly strong in Europe and North America, where data center operators are prioritizing eco-friendly equipment to align with their corporate ESG (Environmental, Social, and Governance) commitments.

Based on product, the market is segmented into UPS Systems, Switchgear, Transformers, Power Distribution Units (PDUs), Generators, and others. In 2026, the UPS systems segment is expected to hold the largest share of the market. UPS systems are the single most critical component for ensuring continuous uptime, as they provide immediate backup power during utility outages and protect sensitive IT equipment from voltage spikes and sags. The shift toward high-efficiency, modular UPS systems that can scale with IT load is a key driver for this segment.

However, the Switchgear and PDU segments are projected to register the highest CAGR during the forecast period. This growth is driven by the increasing complexity of power distribution within high-density data centers. As rack densities increase, more sophisticated switchgear and PDUs are required to manage the higher amperages and provide granular monitoring and control at the rack level.

North America is expected to dominate the global data center electrical equipment market in 2026, primarily due to the high concentration of hyperscale facilities and the presence of major technology companies. The U.S. Congress reports that data center annual energy use reached ~176 TWh in 2023, representing ~4.4% of total U.S. electricity. This huge energy footprint necessitates a vast and continuously growing electrical infrastructure. The key companies operating in the North American market are Schneider Electric SE, ABB Ltd., Siemens Energy AG, Eaton Corporation plc, and GE Vernova.

Asia-Pacific is projected to witness the fastest growth during the forecast period. This is driven by rapid digital transformation, increasing internet penetration, and significant investments in data center infrastructure in China and India. China's state-led 'East-to-West' computing project is a major driver for new power infrastructure in the region. The key companies operating in the Asia-Pacific market are Mitsubishi Electric Corporation, Fuji Electric Co., Ltd., LS ELECTRIC Co., Ltd., CHINT Group, and Toshiba Energy Systems & Solutions Corporation.

The market is projected to reach USD 98.6 billion by 2036, growing at a CAGR of 11.8% from 2026 to 2036.

The UPS systems segment is expected to hold the largest share in 2026, as they are critical for continuous uptime.

The exponential growth in AI-driven power density and the proliferation of hyperscale data centers are the primary drivers.

Asia-Pacific is projected to witness the highest CAGR due to rapid digitalization and infrastructure development in China and India.

It significantly increases the demand for high-capacity electrical equipment and specialized high-voltage substations.

Smart equipment provides real-time energy monitoring, predictive maintenance, and optimized power usage.

PDUs are essential for managing higher amperages and providing granular power monitoring at the rack level.

Challenges include historic high lead times for transformers and switchgear, often exceeding 12-18 months.

It requires the integration of microgrids, on-site renewable generation, and battery energy storage systems.

Leading companies include Schneider Electric SE, ABB Ltd., Siemens Energy AG, Eaton Corporation plc, and Vertiv Holdings Co.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency and Pricing

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research (Manufacturers, Retailers, Nutrition Experts, Consumers)

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Forecast Modeling

2.4. Data Triangulation

2.5. Assumptions

3. Executive Summary

4. Market Insights

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Exponential Growth in AI-Driven Power Density

4.2.1.2. Proliferation of Hyperscale and Colocation Data Centers

4.2.2. Restraints

4.2.2.1. Grid Connection Delays and Utility Power Bottlenecks

4.2.2.2. High Initial Capital Expenditure for Advanced Systems

4.2.3. Opportunities

4.2.3.1. Integration of Sustainable Energy and Microgrid Technologies

4.2.3.2. Growth of Edge Computing and Modular Power Systems

4.2.4. Challenges

4.2.4.1. Supply Chain Constraints and Extended Lead Times

4.2.4.2. Cybersecurity Risks in Digitally-Connected Equipment

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Data Center Electrical Equipment Market Assessment, by Product

5.1. Introduction

5.2. UPS Systems

5.3. Switchgear

5.4. Transformers

5.5. Power Distribution Units (PDUs)

5.6. Generators

5.7. Others

6. Data Center Electrical Equipment Market Assessment, by Voltage Level

6.1. Introduction

6.2. High Voltage

6.3. Medium Voltage

6.4. Low Voltage

7. Data Center Electrical Equipment Market Assessment, by Application

7.1. Introduction

7.2. Hyperscale Data Centers

7.3. Colocation Data Centers

7.4. Enterprise Data Centers

7.5. Edge Data Centers

8. Data Center Electrical Equipment Market Assessment, by Geography

8.1. Introduction

8.2. North America

8.2.1. U.S.

8.2.2. Canada

8.3. Europe

8.3.1. Germany

8.3.2. UK

8.3.3. France

8.3.4. Italy

8.3.5. Spain

8.3.6. Netherlands

8.3.7. Ireland

8.3.8. Rest of Europe

8.4. Asia-Pacific

8.4.1. China

8.4.2. India

8.4.3. Japan

8.4.4. Singapore

8.4.5. Australia

8.4.6. Rest of Asia-Pacific

8.5. Latin America

8.5.1. Brazil

8.5.2. Mexico

8.5.3. Rest of Latin America

8.6. Middle East & Africa

8.6.1. UAE

8.6.2. Saudi Arabia

8.6.3. South Africa

8.6.4. Rest of MEA

9. Competitive Landscape

9.1. Overview

9.2. Key Growth Strategies

9.3. Competitive Benchmarking

9.4. Competitive Dashboard

9.4.1. Market Leaders

9.4.2. Market Differentiators

9.4.3. Vanguards

9.4.4. Emerging Companies

9.5. Market Share Analysis

10. Company Profiles

10.1. Schneider Electric SE

10.2. ABB Ltd.

10.3. Siemens Energy AG

10.4. Eaton Corporation plc

10.5. Mitsubishi Electric Corporation

10.6. Legrand S.A.

10.7. Vertiv Holdings Co.

10.8. Fuji Electric Co., Ltd.

10.9. LS ELECTRIC Co., Ltd.

10.10. GE Vernova

10.11. Rockwell Automation, Inc.

10.12. CHINT Group

10.13. Hyundai Electric & Energy Systems Co., Ltd.

10.14. Toshiba Energy Systems & Solutions Corporation

10.15. Powell Industries, Inc.

10.16. WEG S.A.

10.17. Socomec Group

10.18. Cummins Inc.

10.19. Caterpillar Inc.

10.20. Delta Electronics, Inc.

10.21. Other Players

11. Appendix

Published Date: Jun-2026

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Feb-2026

Subscribe to get the latest industry updates