Resources

About Us

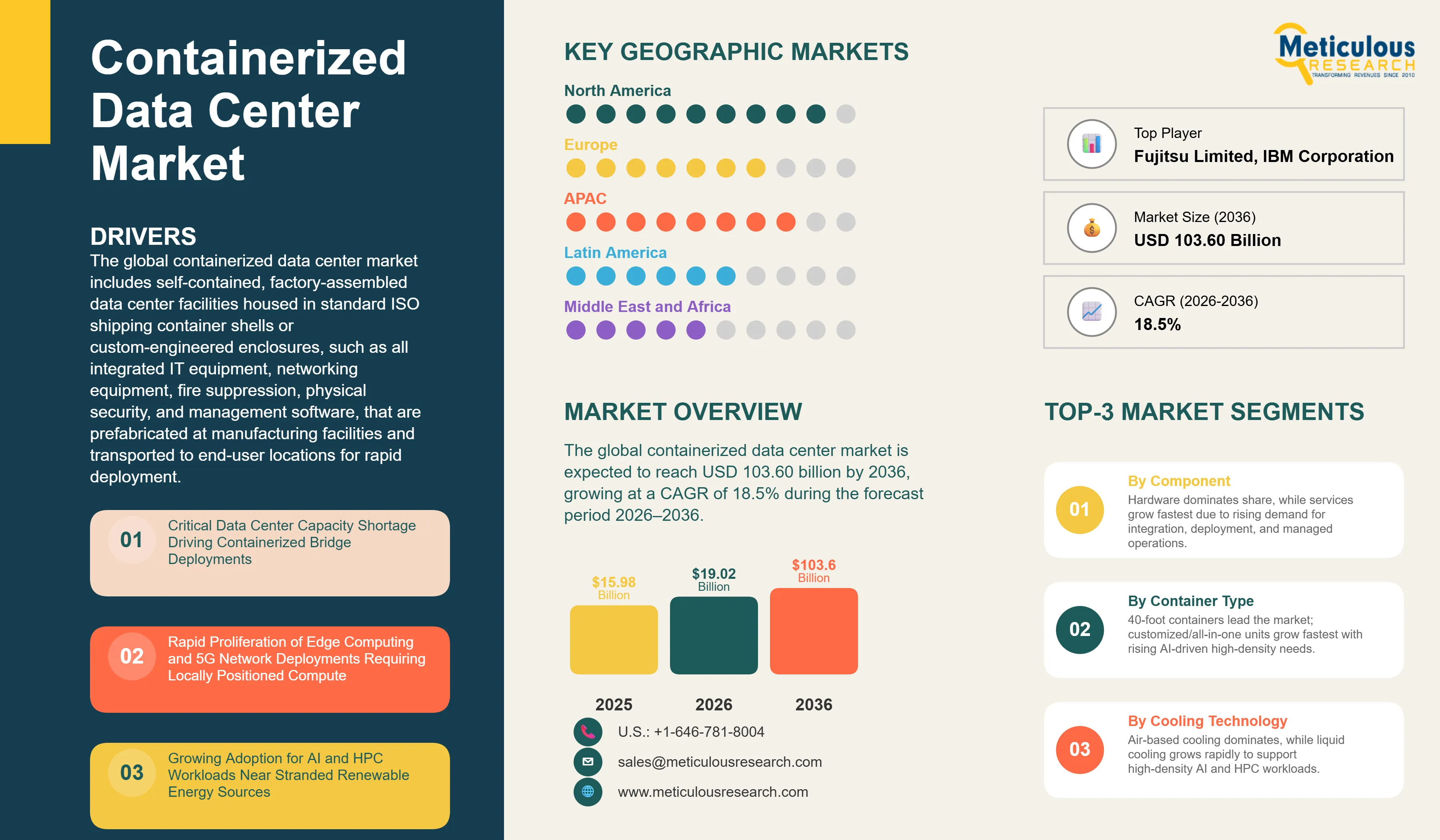

The global containerized data center market was valued at USD 15.98 billion in 2025. This market is expected to reach USD 103.60 billion by 2036 from an estimated USD 19.02 billion in 2026, growing at a CAGR of 18.5% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global containerized data center market includes self-contained, factory-assembled data center facilities housed in standard ISO shipping container shells or custom-engineered enclosures, such as all integrated IT equipment, cooling systems, power infrastructure, networking equipment, fire suppression, physical security, and management software, that are prefabricated at manufacturing facilities and transported to end-user locations for rapid deployment. These solutions serve as complete, standalone data centers that can be operational within 8 to 12 weeks of order placement, compared to 18 to 36 months for equivalent greenfield brick-and-mortar construction, making them critical for organizations facing time-sensitive capacity requirements, land and permitting constraints, remote location deployments, or regulatory data localization mandates.

The growth of the containerized data center market is primarily driven by the shortage of traditional greenfield data center capacity. Multi-year grid interconnection delays and permitting backlogs have constrained new builds, compelling hyperscale operators and cloud providers to deploy containerized modular units as interim or bridge capacity for AI campus expansions. In parallel, the rapid proliferation of edge computing and 5G networks is increasing demand for locally deployable, scalable infrastructure. The adoption of containerized data centers is also rising for AI and HPC workloads in remote locations, particularly near stranded renewable energy sources.

However, the containerized data center market faces certain constraints. Standard containerized configurations typically offer lower rack power density compared to purpose-built facilities, limiting their suitability for ultra-high-density workloads. In addition, integration with existing IT and facility infrastructure can be complex, while premium AI-ready containerized deployments involve relatively high upfront costs, particularly for advanced cooling and power systems.

Despite these challenges, several growth opportunities are emerging in the overall containerized data center market. Governments in emerging markets are increasingly adopting containerized solutions to support sovereign AI cloud deployments and meet data localization requirements. The defense sector also presents a strong opportunity, driven by demand for ruggedized, portable data center solutions. Furthermore, the emergence of White-Space-as-a-Service and leasing models is expanding adoption among mid-sized enterprises by reducing upfront capital investment barriers.

A key trend shaping the containerized data center market is the transition toward liquid-cooled containerized data center configurations. These systems are designed to support next-generation AI GPU workloads with significantly higher rack power densities, enabling containerized solutions to address more advanced and compute-intensive use cases over the forecast period.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 103.6 Billion |

|

Market Size in 2026 |

USD 19.02 Billion |

|

Market Size in 2025 |

USD 15.98 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 18.5% |

|

Dominating Component |

Hardware |

|

Fastest Growing Component |

Services |

|

Dominating Container Type |

40-Foot |

|

Fastest Growing Container Type |

Customized/All-in-One |

|

Dominating Cooling Technology |

Air-Based Cooling |

|

Fastest Growing Cooling Technology |

Liquid-Based Cooling |

|

Dominating Deployment Location |

Core/Campus |

|

Fastest Growing Deployment Location |

Edge/Micro |

|

Dominating End Use |

BFSI |

|

Fastest Growing End Use |

Healthcare |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

AI-Ready Liquid-Cooled Containerized Configurations Becoming a Distinct Product Category

The development of containerized data center formats specifically engineered for AI GPU clusters is creating a distinct and rapidly growing premium product category within the broader containerized data center market. These systems incorporate direct-to-chip cooling capable of managing 60 to 120+ kW rack densities, high-voltage DC power distribution architectures, and NVLink-compatible GPU rack formats.

Huawei’s AI‑optimized FusionModule‑style data‑center solutions, Schneider Electric’s EcoStruxure Modular Data Center architecture for AI, and Vertiv’s prefabricated, AI‑optimized containerized solutions are purpose‑built for NVIDIA Blackwell and future‑generation GPU deployments, commanding significantly higher per‑container pricing than standard configurations and serving as a primary revenue‑growth driver within the containerized‑data‑center hardware segment through the forecast period.

Containerized Deployments as Permanent Strategy for Cryptocurrency Mining Facility Conversion

The repurposing of decommissioned cryptocurrency mining facilities in the U.S. into AI compute campuses has emerged as a growing application of containerized data center infrastructure. These sites, characterized by high power density, low building-to-land ratios, and established grid interconnections, are being retrofitted with containerized AI clusters that can be deployed rapidly and at scale within existing electrical capacity, often without significant new construction.

This trend is generating strong demand for containerized AI deployments at facilities previously operated by companies such as Riot Platforms, Inc., Core Scientific, Inc., and Marathon Digital Holdings, Inc. It represents a structural shift in which stranded energy infrastructure assets are being repurposed into high-value AI compute capacity.

Sovereign AI Containerized Deployments in Emerging Markets

The combination of data localization requirements, limited large-scale greenfield data center construction expertise, and the urgency to deploy domestic AI computing capacity is driving governments in emerging markets, particularly across the Middle East, Africa, and Southeast Asia, to adopt containerized data center solutions as a key enabler of sovereign AI cloud infrastructure, rather than relying solely on traditional purpose-built campuses.

Initiatives such as Saudi Arabia HUMAIN AI, the United Arab Emirates AI infrastructure programs, and India IndiaAI Mission are incorporating modular and containerized deployments as part of their rapid AI capacity expansion strategies. These solutions enable significantly faster deployment, typically within 6 to 12 months, compared to the 3–5 year timelines required for conventional data center construction.

By Component: In 2026, the Hardware Segment to Dominate the Global Containerized Data Center Market

Based on component, the global containerized data center market is segmented into hardware, software, and services.

In 2026, the hardware segment is expected to account for the largest share of the global containerized data center market. The large share of this segment is attributed to the capital-intensive nature of containerized data center procurement, in which IT equipment, cooling systems, and power infrastructure represent the majority of total system value.

IT equipment, such as servers, storage, and networking hardware, constitutes the highest-value hardware sub-segment, followed by cooling systems, which are the rapidly evolving hardware component as liquid cooling integration into containerized formats accelerates.

However, the services segment is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing technical complexity of AI-ready containerized data center deployments, which require specialized expertise for liquid cooling commissioning, high-voltage DC power configuration, and NVIDIA Corporation GPU cluster integration.

In addition, the rising adoption of managed services models is further driving the growth of the overall services market, as vendors increasingly operate and maintain containerized infrastructure on behalf of end users that lack in-house technical capabilities.

By Container Type: In 2026, the 40-Foot Segment to Account for the Largest Share

Based on container type, the global containerized data center market is segmented into 20-foot, 40-foot, and customized/all-in-one containers.

In 2026, the 40-foot segment is expected to account for the largest share of the global containerized data center market. This dominance is attributed to its optimal balance of capacity, transportability, and total cost of ownership, enabling deployment across a wide range of use cases.

A 40-foot container provides sufficient internal volume to accommodate approximately 8 to 20 standard server racks along with integrated cooling and power systems, while remaining within standard ISO shipping dimensions that allow efficient transportation via road networks globally.

However, the customized/all-in-one segment is poised to register the highest CAGR during the forecast period. This growth is driven by the increasing demand for bespoke containerized configurations engineered specifically for AI GPU clusters, which require advanced thermal management, high-capacity power distribution, and specialized structural designs that exceed the capabilities of standard 40-foot ISO container formats.

These customized solutions are designed to support high-density AI workloads and are typically priced at a premium, reflecting their higher level of engineering complexity and application-specific optimization.

By Cooling Technology: In 2026, the Air-Based Cooling Segment to Hold the Largest Share

Based on cooling technology, the global containerized data center market is segmented into air-based cooling and liquid-based cooling (direct-to-chip, immersion, rear-door heat exchangers).

In 2026, the air-based cooling segment is expected to account for the largest share of the global containerized data center market. This dominance reflects the large installed base of air-cooled containerized units deployed for conventional server workloads, as well as the lower upfront cost and operational simplicity associated with air-based systems.

However, the liquid-based cooling segment is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing deployment of AI GPU clusters in containerized environments, which require advanced cooling solutions to manage rack densities exceeding 60 kW, levels that are beyond the effective thermal limits of air-based systems in enclosed container configurations.

By Deployment Location: In 2026, the Core/Campus Segment to Hold the Largest Share

Based on deployment location, the global containerized data center market is segmented into core/campus, edge/micro, and remote and off-grid deployments.

In 2026, the core/campus segment is expected to account for the largest share of the global containerized data center market. This is driven by large-scale deployment of containerized AI clusters at hyperscale campuses as bridge capacity, as well as their use for overflow capacity during the construction of permanent facilities.

However, the edge/micro segment is projected to register the highest CAGR during the forecast period. This growth is driven by the proliferation of 5G-enabled edge computing, smart city infrastructure, and autonomous vehicle ecosystems that require locally distributed and rapidly deployable containerized compute capacity.

By End Use: In 2026, the BFSI Segment to Account for the Largest Share

Based on end use, the global containerized data center market is segmented into IT and telecom, BFSI, government and defense, healthcare, retail and e-commerce, energy and utilities, media and entertainment, and other end uses.

In 2026, the BFSI segment is expected to account for the largest share of the global containerized data center market. This is driven by the extensive use of containerized solutions by the financial services industry for branch-level compute, disaster recovery, and regulatory data residency compliance across geographically distributed operations.

The need for Tier 3 and Tier 4 equivalent reliability in compact, rapidly deployable formats, combined with strong physical security and environmental monitoring capabilities, positions BFSI as the leading end-use segment by revenue.

However, the healthcare segment is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing deployment of AI-enabled diagnostic and clinical decision support applications at hospitals and clinics, which require locally deployed compute infrastructure to meet data sovereignty requirements.

Additionally, the growing use of containerized data centers in remote healthcare settings and the rising adoption of AI-based medical imaging and genomics analysis are further accelerating demand for edge-based compute capacity near clinical data sources.

Based on geography, the global containerized data center market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global containerized data center market. This dominance is driven by the high concentration of hyperscale operators deploying containerized units as bridge capacity for AI campus expansions, as well as the leading role of U.S.-based cloud providers in driving procurement. The region is also witnessing increasing conversion of decommissioned cryptocurrency mining facilities into containerized AI compute sites, driven by strong growth in AI server deployments and the need to address multi-year grid interconnection backlogs.

However, the Asia Pacific containerized data center market is expected to grow at the highest CAGR from 2026 to 2036. This growth is driven by large-scale digital infrastructure expansion across China, India, Japan, Singapore, and Southeast Asia, along with aggressive 5G network densification programs that are accelerating demand for edge-based containerized deployments.

In addition, data localization policies, mainly in India, are driving sovereign cloud adoption through modular solutions, while China continues to invest in distributed containerized AI compute campuses. India’s data center capacity is projected to expand significantly through 2030, with containerized solutions capturing an increasing share of new capacity due to faster deployment timelines and lower permitting complexity compared to traditional greenfield construction.

The global containerized data center market is moderately consolidated, with competition centered on deployment speed, thermal‑management capability for high‑density AI workloads, cooling‑technology integration, geographic supply‑chain reach, and the ability to deliver customized configurations meeting sovereign or defense‑specific security requirements.

Huawei is a leading provider in the segment through its FusionModule series, which has gained widespread deployment in China and several emerging markets. Schneider Electric and Vertiv compete primarily on AI‑ready modular infrastructure with advanced cooling integration and DCIM software capabilities, targeting hyperscale and AI‑optimized campus deployments. IBM, Cisco, Dell Technologies, and Hewlett Packard Enterprise offer containerized or modular data center solutions integrated with their broader IT infrastructure portfolios, appealing to enterprises and cloud‑adjacent customers.

The report offers a competitive analysis based on an extensive assessment of the leading players’ product portfolios, geographic presence, and key growth strategies adopted in the few years. Some of the key players operating in the global containerized data center market are Huawei Technologies Co., Ltd. (China), IBM Corporation (U.S.), Cisco Systems, Inc. (U.S.), Schneider Electric SE (France), Dell Technologies Inc. (U.S.), Hewlett Packard Enterprise Company (U.S.), Vertiv Holdings Co. (U.S.), ZTE Corporation (China), Eaton Corporation plc (Ireland), Rittal GmbH & Co. KG (Germany), Fujitsu Limited (Japan), Delta Electronics, Inc. (Taiwan), BladeRoom Group Limited (U.K.), Nat Systems (U.S.), and Flexnode (Sweden) among others.

The global containerized data center market is expected to reach USD 103.6 billion by 2036 from an estimated USD 19.02 billion in 2026, at a CAGR of 18.5% during the forecast period 2026–2036.

In 2026, the hardware segment is expected to hold the largest share of the global containerized data center market.

The services segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the growing technical complexity of AI-ready containerized deployments.

In 2026, the 40-foot containers segment is expected to hold the largest share of the global containerized data center market.

The liquid-based cooling segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by AI GPU cluster deployments requiring direct-to-chip and immersion cooling in containerized formats.

The growth of this market is driven by the critical shortage of traditional data center capacity causing hyperscale operators to deploy containerized bridge capacity, the rapid proliferation of edge computing and 5G deployments, and the growing adoption for AI workloads near stranded renewable energy.

Key players are Huawei Technologies Co., Ltd. (China), IBM Corporation (U.S.), Cisco Systems, Inc. (U.S.), Schneider Electric SE (France), Dell Technologies Inc. (U.S.), Hewlett Packard Enterprise Company (U.S.), Vertiv Holdings Co. (U.S.), ZTE Corporation (China), Eaton Corporation plc (Ireland), Rittal GmbH & Co. KG (Germany), Fujitsu Limited (Japan), Delta Electronics, Inc. (Taiwan), BladeRoom Group Limited (U.K.), Nat Systems (U.S.), and Flexnode (Sweden).

Asia Pacific is expected to register the highest growth rate in the global containerized data center market during the forecast period 2026–2036.

1. Introduction

1.1. Market Definition and Scope

1.2. Currency & Limitations

1.3. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection Methods

2.3. Market Estimation and Forecast Methodology

2.4. Assumptions and Limitations

3. Executive Summary

3.1. Market Overview

3.2. Market Analysis by Component

3.3. Market Analysis by Container Type

3.4. Market Analysis by Cooling Technology

3.5. Market Analysis by Deployment Location

3.6. Market Analysis by Organization Size

3.7. Market Analysis by End Use

3.8. Market Analysis by Geography

4. Market Dynamics

4.1. Overview

4.2. Drivers

4.2.1. Critical Data Center Capacity Shortage Driving Containerized Bridge Deployments

4.2.2. Rapid Proliferation of Edge Computing and 5G Network Deployments Requiring Locally Positioned Compute

4.2.3. Growing Adoption for AI and HPC Workloads Near Stranded Renewable Energy Sources

4.2.4. Data Localization Regulations and Sovereign Cloud Requirements Driving Portable Containerized Deployments

4.3. Restraints

4.3.1. Limited Rack Power Density of Standard Configurations Compared to Purpose-Built Fixed Facilities

4.3.2. Integration Complexity with Existing Enterprise IT Infrastructure During Containerized Deployments

4.4. Opportunities

4.4.1. Sovereign AI Cloud Deployment in Emerging Markets with Data Localization Requirements

4.4.2. Military and Government Defense Applications for Ruggedized Containerized Deployments

4.4.3. White-Space-as-a-Service and Leasing Models Expanding Containerized Market to Mid-Tier Organizations

4.5. Challenges

4.5.1. Cooling and Power Density Challenges for Next-Generation AI GPU Workloads in Standard Container Formats

4.5.2. Lack of Industry Standardization Across Component Interfaces Increasing Integration Cost and Complexity

4.6. Porter’s Five Forces Analysis

5. Containerized Data Center Market, by Component

5.1. Overview

5.2. Hardware

5.2.1. IT Equipment (Servers, Storage, Networking)

5.2.2. Cooling Systems

5.2.3. Power Systems (UPS, PDU, Generators)

5.2.4. Racks and Enclosures

5.3. Software

5.3.1. DCIM Software

5.3.2. Energy Management Software

5.4. Services

5.4.1. Design and Consulting Services

5.4.2. Installation and Deployment Services

5.4.3. Managed Services and Operations

6. Containerized Data Center Market, by Container Type

6.1. Overview

6.2. 20-Foot Containers

6.3. 40-Foot Containers

6.4. Customized/All-in-One Containers

7. Containerized Data Center Market, by Cooling Technology

7.1. Overview

7.2. Air-Based Cooling

7.3. Liquid-Based Cooling

7.3.1. Direct-to-Chip Cooling

7.3.2. Immersion Cooling

7.3.3. Rear-Door Heat Exchangers

8. Containerized Data Center Market, by Deployment Location

8.1. Overview

8.2. Core/Campus

8.3. Edge/Micro

8.4. Remote & Off-Grid

9. Containerized Data Center Market, by Organization Size

9.1. Overview

9.2. Large Enterprises

9.3. Small & Medium Enterprises

10. Containerized Data Center Market, by End Use

10.1. Overview

10.2. IT & Telecom

10.3. BFSI

10.4. Government & Defense

10.5. Healthcare

10.6. Retail & E-Commerce

10.7. Energy & Utilities

10.8. Media & Entertainment

10.9. Other End Uses

11. Containerized Data Center Market, by Geography

11.1. Overview

11.2. North America

11.2.1. U.S.

11.2.2. Canada

11.3. Europe

11.3.1. Germany

11.3.2. U.K.

11.3.3. France

11.3.4. Spain

11.3.5. Italy

11.3.6. Netherlands

11.3.7. Ireland

11.3.8. Rest of Europe

11.4. Asia Pacific

11.4.1. China

11.4.2. Japan

11.4.3. India

11.4.4. Singapore

11.4.5. South Korea

11.4.6. Australia

11.4.7. Rest of Asia Pacific

11.5. Latin America

11.5.1. Brazil

11.5.2. Mexico

11.5.3. Rest of Latin America

11.6. Middle East and Africa

11.6.1. UAE

11.6.2. Saudi Arabia

11.6.3. South Africa

11.6.4. Rest of MEA

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Share Analysis (2025)

13. Company Profiles

13.1. Huawei Technologies Co., Ltd.

13.2. International Business Machines Corporation

13.3. Cisco Systems, Inc.

13.4. Schneider Electric SE

13.5. Dell Technologies Inc.

13.6. Hewlett Packard Enterprise Company

13.7. Vertiv Holdings Co.

13.8. ZTE Corporation

13.9. Eaton Corporation plc

13.10. Rittal GmbH & Co. KG

13.11. Fujitsu Limited

13.12. Delta Electronics, Inc.

13.13. BladeRoom Group Limited

13.14. Super Micro Computer, Inc.

13.15. Canovate Group

13.16. Others

14. Appendix

14.1. Questionnaire

14.2. Available Customization Options

14.3. Related Reports

Published Date: Jun-2026

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Feb-2026

Subscribe to get the latest industry updates