Resources

About Us

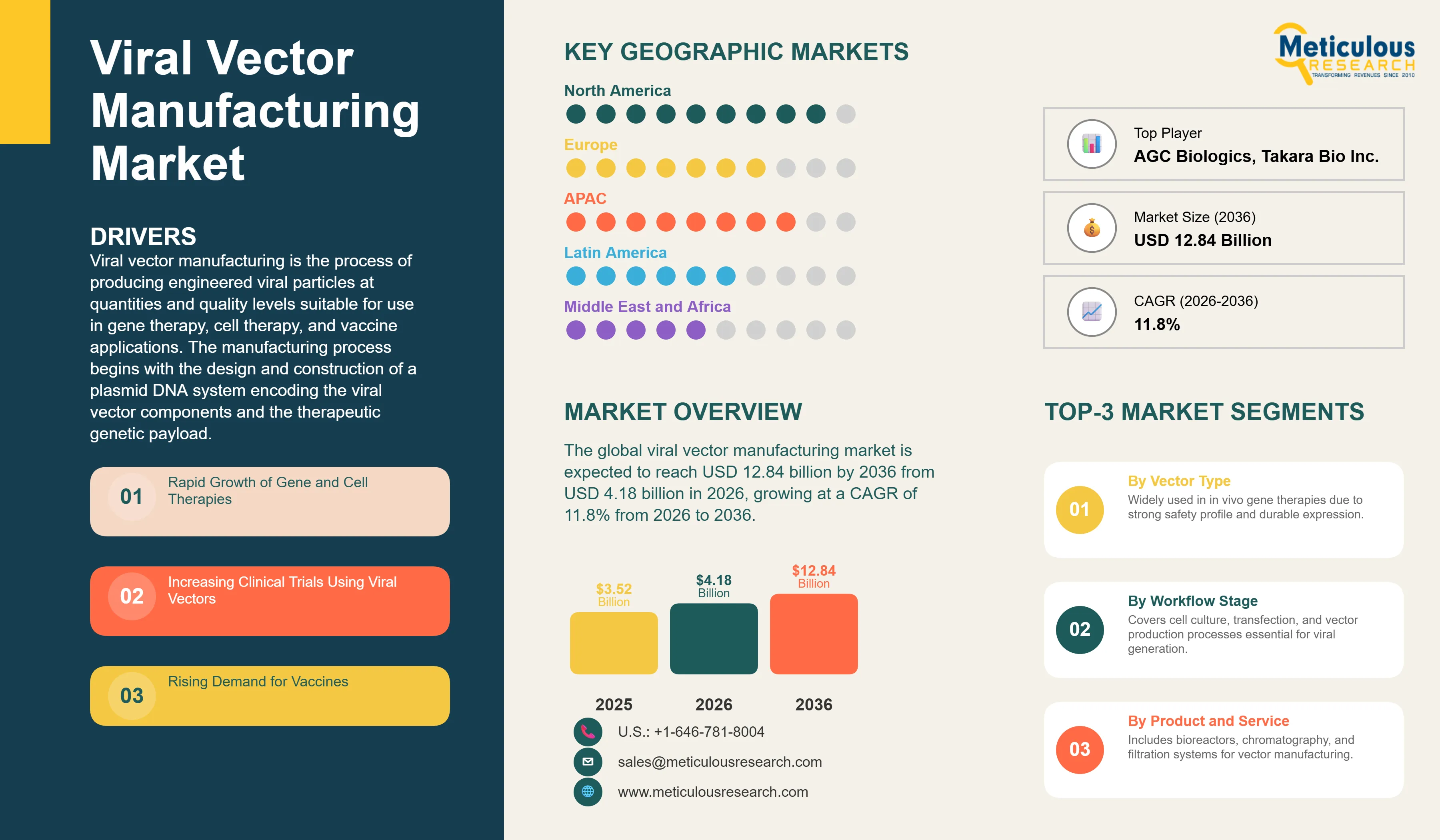

The global viral vector manufacturing market was valued at USD 3.52 billion in 2025. This market is expected to reach USD 12.84 billion by 2036 from USD 4.18 billion in 2026, growing at a CAGR of 11.8% from 2026 to 2036.

The growth of this market is driven by the accelerating clinical and commercial advancement of gene therapies and cell therapies that rely on viral vectors as their primary delivery mechanism. A viral vector is a modified virus, stripped of its disease-causing genes and re-engineered to carry therapeutic genetic material into target cells. Manufacturing these vectors at the purity, potency, and scale required for clinical use and commercial supply is one of the most technically demanding processes in biopharmaceutical production, requiring specialized upstream cell culture systems, complex downstream purification and characterization processes, and highly controlled fill and finish operations under strict GMP conditions.

The market has expanded significantly since the first commercial approvals of viral vector-based gene therapies. According to the U.S. Food and Drug Administration, the agency continues to project approvals of approximately 10–20 cell and gene therapy products annually, reflecting the rapid expansion of advanced biologics pipelines. FDA-approved cell and gene therapy products have increased significantly in recent years, with the total number of approved therapies reaching more than 40 products by 2025, spanning CAR-T therapies, gene therapies for rare diseases, and regenerative medicine products.

Key commercial milestones driving manufacturing demand include Novartis's Zolgensma for spinal muscular atrophy (2019), CSL Behring's Hemgenix for hemophilia B (2022), BioMarin's Roctavian for hemophilia A (2022/2023), and Sarepta's Elevidys for Duchenne muscular dystrophy (2023). According to data from ClinicalTrials.gov cited by multiple industry sources, more than 2,000 gene and cell therapy clinical trials were active globally as of 2024, with each program advancing through phases creating compounding upstream demand for GMP-grade viral vector manufacturing capacity.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Viral vector manufacturing is the process of producing engineered viral particles at quantities and quality levels suitable for use in gene therapy, cell therapy, and vaccine applications. The manufacturing process begins with the design and construction of a plasmid DNA system encoding the viral vector components and the therapeutic genetic payload. This genetic material is then introduced into a producer cell line, typically human embryonic kidney 293 cells for adenovirus and AAV production or human fibrosarcoma HT1080 cells for lentiviral vector production, which generates new viral vector particles during upstream culture. The crude viral harvest is then processed through a series of downstream purification steps including clarification, chromatography, filtration, and concentration to remove cellular debris, host cell proteins, empty capsids, and process-related impurities, yielding a purified vector bulk that is formulated and filled into final containers under sterile conditions.

The major viral vector platforms each have distinct manufacturing characteristics that influence the choice of production system, equipment, and process development approach. Adeno-associated viruses are small, non-enveloped viruses that are produced using transient transfection of producer cells with multiple plasmids or using baculovirus-insect cell production systems. AAV manufacturing is characterized by relatively low volumetric yields compared with other biological products, making upstream intensification and downstream recovery efficiency critically important cost drivers. Lentiviral vectors are enveloped retroviruses that require careful handling due to their sensitivity to physical stress during processing, and their production by transient transfection generates a complex mixture of particles that requires sophisticated downstream purification to achieve the purity levels required for clinical use. Adenoviral vectors, including the ChAdOx platform used in the AstraZeneca COVID-19 vaccine, are produced at relatively high titers in adherent or suspension HEK293 cell cultures and benefit from a more established manufacturing process infrastructure developed through decades of adenovirus-based vaccine production.

The competitive landscape of the viral vector manufacturing market is organized around two primary business models. CDMOs including Lonza, Catalent, Fujifilm Diosynth Biotechnologies, Oxford Biomedica, and WuXi AppTec provide contract manufacturing services to gene and cell therapy developers that outsource some or all of their vector manufacturing needs. These CDMOs have invested heavily in dedicated viral vector manufacturing suites with the specialized equipment, validated processes, and qualified personnel required for GMP production. Technology and equipment providers including Thermo Fisher Scientific, Cytiva (Danaher), Sartorius, and Merck KGaA supply the bioreactors, chromatography systems, filtration devices, cell culture media, and analytical kits that both CDMOs and in-house manufacturing operations use across the upstream and downstream workflow. This two-tier structure means that growth in the viral vector manufacturing market benefits both service providers and technology suppliers.

Shift from Adherent to Suspension Cell Culture Systems

One of the most important manufacturing technology shifts in the viral vector market is the transition from adherent cell culture systems to suspension-based production platforms. Traditional viral vector manufacturing has relied heavily on adherent HEK293 cells grown on surfaces using multi-layer cell stacks, roller bottles, and fixed-bed bioreactors such as the iCELLis system. While effective at smaller scales, these approaches are labor-intensive, challenging to scale, and constrained in terms of volumetric productivity. In contrast, suspension-adapted HEK293 cell lines that can grow efficiently in stirred-tank bioreactors enable more scalable and flexible manufacturing, supporting higher production volumes required for commercial gene therapy applications.

This transition is particularly critical for adeno-associated virus (AAV) manufacturing, where scaling from clinical to commercial production has historically been a major bottleneck. Leading organizations such as Novartis have invested in suspension-based manufacturing capabilities, while contract development and manufacturing organizations including Lonza and Fujifilm Diosynth Biotechnologies are advancing commercially validated suspension processes. The increasing adoption of single-use bioreactor systems further supports this shift by reducing operational complexity, lowering capital requirements, and enabling faster turnaround between production campaigns, thereby accelerating the overall scalability of viral vector manufacturing.

Increasing Outsourcing to CDMOs Driven by Capacity and Expertise Gaps

The outsourcing of viral vector manufacturing to contract development and manufacturing organizations (CDMOs) is accelerating as gene and cell therapy developers recognize the complexity and resource intensity of building in-house capabilities. Establishing a purpose-built GMP viral vector facility requires substantial capital investment, long development timelines, and access to highly specialized technical talent that remains in limited supply globally. For most clinical-stage developers, allocating resources to manufacturing infrastructure diverts focus from core research and clinical development priorities. As a result, partnering with established CDMOs offers a more efficient and flexible pathway to access scalable, compliant manufacturing capacity.

This shift has driven significant capacity expansion across leading CDMOs such as Lonza, Catalent, Fujifilm Diosynth Biotechnologies, Oxford Biomedica, and Samsung Biologics. At the same time, the growing pipeline of cell and gene therapy programs is steadily increasing demand for viral vectors and related manufacturing services, reinforcing the industry’s reliance on outsourced production models.

The CDMO landscape is also becoming more sophisticated and differentiated. While earlier competition focused primarily on GMP compliance and available capacity, leading providers are now distinguishing themselves through advanced platform technologies, proprietary cell lines, optimized upstream and downstream processes, and integrated analytical capabilities. Increasingly, sponsors are seeking end-to-end partners capable of supporting development from early-stage process optimization through clinical supply and commercial-scale manufacturing within a single relationship. CDMOs that can demonstrate a clear and scalable pathway to commercial production for specific vector types are gaining a competitive edge in securing long-term partnerships.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 12.84 Billion |

|

Market Size in 2026 |

USD 4.18 Billion |

|

Market Size in 2025 |

USD 3.52 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 11.8% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Vector Type, Workflow Stage, Product and Service, Manufacturing Scale, Application, End User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Driver: Rapid Growth of Gene and Cell Therapies Advancing Through Clinical Development

The primary driver of the viral vector manufacturing market is the rapid expansion of gene and cell therapy pipelines, alongside the progression of existing programs from early-stage research into late-stage clinical development and commercialization. Viral vector-based gene therapies, particularly those using adeno-associated virus (AAV) platforms, have demonstrated durable therapeutic benefits across multiple disease areas, including hemophilia, spinal muscular atrophy, retinal disorders, and neuromuscular conditions. These clinical successes have established strong proof-of-concept and commercial validation, attracting increased investment and accelerating pipeline growth.

As more programs advance through clinical phases, manufacturing requirements scale significantly, creating sustained demand for high-quality viral vectors and associated production capabilities. The AAV segment remains a central contributor to this demand, given its widespread use in gene therapy development. In parallel, chimeric antigen receptor T-cell (CAR-T) therapies, enabled by lentiviral vectors, have further expanded the need for viral vector manufacturing since the commercial introduction of therapies such as Kymriah and Yescarta.

Overall, the increasing number of gene and cell therapy programs, combined with their progression toward commercialization, is creating a structurally expanding demand for viral vector production. Viral vectors remain a foundational technology across both gene and cell therapy modalities, reinforcing their central role in biopharmaceutical manufacturing and long-term market growth.

Opportunity: Automation and Digital Bioprocessing in Vector Manufacturing

The integration of automation, process analytical technology (PAT), and digital bioprocessing tools represents a significant opportunity to address the cost, scalability, and consistency challenges in viral vector manufacturing. Compared with conventional biopharmaceutical production, viral vector processes remain highly manual and operator-dependent, with critical steps such as cell culture handling, transfection, media exchange, and in-process sampling often performed through complex, labor-intensive workflows. This reliance on manual intervention introduces process variability, which can impact batch consistency, regulatory compliance, and overall manufacturing yield. The adoption of automated bioreactor systems with integrated PAT sensors, along with automated downstream processing solutions, is helping to reduce variability, improve control over critical quality attributes, and enhance overall process robustness.

At the same time, digital bioprocessing platforms are emerging as a transformative layer within manufacturing operations. These systems enable the capture and analysis of large volumes of process data, allowing the application of advanced analytics and machine learning to optimize process parameters, predict outcomes, and accelerate development timelines. Companies such as Cytiva and Sartorius are developing integrated solutions tailored to viral vector workflows, combining automation with data-driven process optimization. As these technologies mature, they are expected to improve manufacturing efficiency, reduce cost of goods, and support the broader scalability of gene and cell therapy production, ultimately enabling greater patient access.

Why Does Adeno-associated Virus Lead the Market?

In 2026, the adeno-associated virus (AAV) segment is expected to account for the largest share of the overall market for viral vector manufacturing. AAV is currently the most commercially advanced viral vector platform, supported by multiple approved gene therapies that continue to drive sustained manufacturing demand, as well as a robust pipeline of late-stage programs approaching commercialization. Therapies such as Luxturna, Zolgensma, Hemgenix, Roctavian, and Elevidys have established strong clinical and commercial precedents for AAV-based treatments. However, AAV manufacturing remains technically challenging, with limitations in production yield and downstream recovery driving ongoing innovation in process optimization. In response to growing demand, major CDMOs and biopharmaceutical companies, including Thermo Fisher Scientific, Lonza, Fujifilm Diosynth Biotechnologies, and Catalent, have made significant investments in dedicated AAV manufacturing infrastructure.

However, the lentiviral vectors segment is expected to witness the fastest growth during the forecast period. This growth is primarily driven by the expansion of cell therapy manufacturing, particularly chimeric antigen receptor T-cell (CAR-T) therapies, which rely on lentiviral vectors for genetic modification of patient or donor-derived T cells. Commercially approved therapies such as Kymriah, Yescarta, Tecartus, Breyanzi, and Carvykti are generating increasing demand for lentiviral vector supply through patient-specific manufacturing processes. In addition, the development of next-generation allogeneic, off-the-shelf cell therapies is creating new requirements for large-scale lentiviral production. Together, these trends position lentiviral vectors as the fastest-growing segment within the viral vector manufacturing market.

How Does Upstream Processing Lead the Market?

In 2026, the upstream processing segment is expected to account for the largest share of the viral vector manufacturing market. Upstream processing includes the core production activities such as cell culture, bioreactor operation, transfection, and the use of specialized media and consumables to generate viral vectors within host cells. This stage represents the most resource-intensive portion of the workflow, both in terms of capital equipment and recurring consumables. As a result, it is the primary focus of process development efforts, with manufacturers continuously working to improve yield, scalability, and consistency. Widely adopted platforms such as single-use bioreactors from Sartorius, Cytiva, and Thermo Fisher Scientific further reinforce the commercial significance of this segment by driving recurring demand for consumables and integrated production systems.

However, the downstream processing segment is expected to witness the fastest growth during the forecast period. Downstream operations, including purification, filtration, and analytical characterization, have historically posed greater technical challenges, particularly for complex vectors such as AAV. The need to separate full viral particles from empty capsids and other impurities requires advanced purification strategies that go beyond conventional biopharmaceutical processes. Innovations such as high-selectivity affinity chromatography, advanced filtration techniques, and enhanced analytical methods are improving process efficiency and product quality. At the same time, increasing regulatory expectations for detailed vector characterization are driving greater investment in downstream capabilities, positioning this segment as a key area of innovation and growth within viral vector manufacturing.

How Do Services Lead the Market?

In 2026, the services segment is expected to account for the largest share of the viral vector manufacturing market. Contract development and manufacturing organizations (CDMOs) play a central role, as most gene and cell therapy developers lack in-house manufacturing capabilities and depend on external partners for critical production activities. These services span the full development lifecycle, including process development, analytical testing, clinical- and commercial-scale GMP manufacturing, and fill-finish operations. Beyond manufacturing capacity, CDMOs provide specialized expertise, regulatory experience, and established quality systems, making them essential partners in managing the complexity and risk associated with gene therapy development. This value-added offering enables service providers to command a premium over basic production costs.

However, the consumables and reagents segment is expected to witness the fastest growth during the forecast period. As manufacturing volumes increase and more therapies advance toward commercialization, demand for single-use consumables and process reagents continues to scale with production activity. Unlike capital equipment, which is utilized across multiple campaigns, consumables must be replaced for each manufacturing run, creating a recurring revenue stream closely tied to output levels. Leading suppliers such as Sartorius, Cytiva, Thermo Fisher Scientific, and Merck KGaA have built business models around this recurring demand, particularly through single-use systems that generate ongoing sales of associated bags, filters, and tubing assemblies.

How Does the Clinical Scale Lead the Market?

In 2026, the clinical segment is expected to account for the largest share of the viral vector manufacturing market. This is driven by the large and active pipeline of gene and cell therapy programs across early and late-stage clinical trials, all of which rely heavily on viral vectors for development. Clinical-stage manufacturing requires full compliance with good manufacturing practice (GMP) standards, even at smaller batch sizes, resulting in high per-unit production costs and significant demand for specialized infrastructure. Contract development and manufacturing organizations such as Oxford Biomedica, Cobra Biologics, and Charles River Laboratories play a key role in supporting this segment by providing dedicated clinical-scale manufacturing capabilities and regulatory expertise.

However, the commercial production segment is expected to witness the fastest growth during the forecast period. As more gene and cell therapy programs progress toward regulatory approval, the demand for large-scale manufacturing capacity is increasing rapidly. Transitioning from clinical to commercial production requires substantial scale-up of bioreactor volumes and process optimization to meet market demand while maintaining product quality and consistency. This shift is particularly significant for widely adopted vector types such as AAV, where manufacturing complexity and yield constraints necessitate further expansion of upstream and downstream capabilities. As a result, the commercialization phase is emerging as a major growth driver, supported by ongoing investments in large-scale GMP manufacturing infrastructure and process innovation.

Why Does Gene Therapy Lead the Application Market?

In 2026, the gene therapy segment is expected to account for the largest share of the viral vector manufacturing market. In vivo gene therapies, particularly those based on adeno-associated virus (AAV) platforms, represent the most commercially advanced application of viral vectors. These therapies have demonstrated strong clinical outcomes across multiple disease areas, including rare genetic and neurological disorders, and continue to drive sustained manufacturing demand. Treatments such as Hemgenix and Zolgensma highlight both the clinical success and the manufacturing intensity of this segment, as high per-patient dosing requirements necessitate large-scale production capabilities even for relatively small patient populations. As a result, gene therapy remains the most demanding application in terms of manufacturing scale and process optimization.

However, the cell therapy segment is expected to witness the fastest growth during the forecast period. This growth is primarily driven by the expanding adoption of chimeric antigen receptor T-cell (CAR-T) therapies, which rely on viral vectors, typically lentiviral, for genetic modification of immune cells. Commercial therapies such as Kymriah and Yescarta continue to generate increasing demand for vector supply through patient-specific manufacturing workflows. At the same time, the development of next-generation allogeneic, off-the-shelf cell therapies is expected to shift manufacturing toward larger-scale production models, further accelerating demand for viral vector capacity. Together, these trends position cell therapy as the fastest-growing application segment within the viral vector manufacturing market.

Why Do CDMOs and CMOs Lead the End User Market?

In 2026, the CDMOs and CMOs segment is expected to hold the largest share of the viral vector manufacturing market. CDMOs are the primary buyers of viral vector manufacturing technology and equipment and the primary providers of manufacturing services to gene and cell therapy developers. The capital and expertise requirements for establishing in-house GMP viral vector manufacturing capability are prohibitive for the majority of gene and cell therapy companies, which are typically smaller biotechnology companies or clinical-stage programs within larger pharmaceutical companies that do not yet have commercial-scale gene therapy manufacturing infrastructure. CDMOs including Lonza, Catalent, Fujifilm Diosynth, Oxford Biomedica, WuXi AppTec, and AGC Biologics have built the specialized facilities, qualified processes, and regulatory track records that gene therapy developers require, and they serve as the primary manufacturing partners for the majority of viral vector programs in clinical development globally.

However, the biopharmaceutical companies segment is expected to witness the fastest growth during the forecast period. As gene and cell therapy programs approach and achieve commercial approval, the innovator biopharmaceutical companies that own these programs are investing in building or expanding in-house manufacturing capacity to reduce long-term supply chain risk, improve cost of goods at commercial scale, and maintain manufacturing control over products that are central to their therapeutic franchise. Novartis has built a dedicated gene therapy manufacturing center in Durham, North Carolina for Zolgensma production. BioMarin has invested in its own AAV manufacturing capability for Roctavian. Bluebird Bio, Sarepta Therapeutics, and Solid Biosciences are among the companies that have invested in in-house lentiviral and AAV vector manufacturing infrastructure. This trend of insourcing at commercial scale will increase the direct equipment and consumable procurement by biopharmaceutical companies relative to CDMOs over the forecast period.

How is North America Maintaining Market Leadership?

In 2026, North America is expected to account for the largest share of the global viral vector manufacturing industry. The United States serves as the primary growth engine, supported by a high concentration of gene and cell therapy development activity and a well-established biopharmaceutical ecosystem. Key innovation hubs such as Boston, San Francisco, Philadelphia, and the Research Triangle host a dense network of biotechnology companies, research institutions, and manufacturing facilities. In addition, major contract development and manufacturing organizations, including Catalent, Lonza, Thermo Fisher Scientific, and WuXi AppTec, have established significant viral vector production capacity in the region, reinforcing North America’s leadership in both clinical and commercial manufacturing.

Asia-Pacific is expected to witness the highest growth rate in the viral vector manufacturing market during the forecast period. This growth is driven by a combination of expanding gene therapy pipelines, supportive regulatory environments, and increasing investment in biomanufacturing infrastructure across the region. Countries such as China, Japan, Singapore, South Korea, and Australia are actively strengthening their capabilities in advanced therapy development and manufacturing, positioning the region as a key emerging hub for viral vector production.

China is leading this growth, supported by a rapidly expanding base of gene and cell therapy programs and strong domestic investment in biotechnology innovation. Local CDMOs such as WuXi AppTec and GenScript Biotech are scaling viral vector manufacturing capacity to serve both domestic and international demand. Singapore has emerged as a regional manufacturing hub, attracting investments from global players including Lonza, Thermo Fisher Scientific, and AGC Biologics, supported by strong government initiatives and its reputation for high-quality GMP-compliant manufacturing. Japan’s regulatory framework, including accelerated pathways for regenerative medicine, is encouraging domestic development and driving demand for local manufacturing capabilities, while South Korea is expanding its ecosystem with companies such as Samsung Biologics entering the viral vector space. Australia is also contributing through public sector investments in GMP-grade manufacturing infrastructure.

Some of the key companies operating in the global viral vector manufacturing market are Thermo Fisher Scientific Inc., Danaher Corporation (Cytiva), Lonza Group AG, Catalent Inc., Samsung Biologics Co. Ltd., Fujifilm Diosynth Biotechnologies, WuXi AppTec Co. Ltd., Oxford Biomedica plc, Sartorius AG, Merck KGaA, Charles River Laboratories International Inc., AGC Biologics, Takara Bio Inc., GenScript Biotech Corporation, and Cobra Biologics.

The global viral vector manufacturing market is expected to grow from USD 4.18 billion in 2026 to USD 12.84 billion by 2036.

The global viral vector manufacturing market is projected to grow at a CAGR of 11.8% from 2026 to 2036.

The adeno-associated virus segment is expected to dominate the overall market in 2026. However, the lentiviral vectors segment is expected to witness the fastest CAGR, driven by the rapid commercial expansion of CAR-T cell therapies and the growing pipeline of allogeneic cell therapy programs that require large-batch lentiviral vector production.

The upstream processing segment is expected to dominate the overall market in 2026. However, the downstream processing segment is expected to witness the fastest CAGR, driven by growing investment in chromatography and filtration solutions for empty-full AAV capsid separation, improved purification yield, and the comprehensive vector characterization required by regulatory agencies for clinical and commercial product submissions.

The gene therapy segment is expected to dominate the overall market in 2026. However, the cell therapy segment is expected to witness the fastest CAGR, driven by the commercial expansion of CAR-T therapies and the anticipated progression of next-generation allogeneic cell therapy programs toward commercial approval during the forecast period.

North America is expected to lead the global market in 2026. However, Asia-Pacific is expected to witness the fastest CAGR, driven by China's rapidly growing gene therapy clinical trial activity and CDMO capacity expansion, Singapore's emergence as a regional biomanufacturing hub, and Japan's accelerated regulatory pathway for regenerative medicines.

The major players are Thermo Fisher Scientific, Cytiva (Danaher), Lonza Group, Catalent, Samsung Biologics, Fujifilm Diosynth Biotechnologies, WuXi AppTec, Oxford Biomedica, Sartorius, Merck KGaA, Charles River Laboratories, AGC Biologics, Takara Bio, GenScript Biotech, and Cobra Biologics.

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Market Ecosystem

1.4 Currency and Limitations

1.4.1 Currency

1.4.2 Limitations

1.5 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation

2.2.1 Secondary Research

2.2.2 Primary Research

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Forecast Modeling

2.4 Data Triangulation

2.5 Assumptions

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Rapid Growth of Gene and Cell Therapies

4.2.1.2 Increasing Clinical Trials Using Viral Vectors

4.2.1.3 Rising Demand for Vaccines

4.2.1.4 Expansion of CDMO and CMO Manufacturing Capacity

4.2.2 Restraints

4.2.2.1 High Manufacturing Costs

4.2.2.2 Complex Production Processes

4.2.2.3 Limited Large-scale Manufacturing Capacity

4.2.3 Opportunities

4.2.3.1 Advancements in Scalable Manufacturing Technologies

4.2.3.2 Growth in Emerging Markets

4.2.3.3 Development of Novel Vector Platforms

4.2.3.4 Automation and Digital Bioprocessing

4.2.4 Challenges

4.2.4.1 Regulatory Complexity

4.2.4.2 Quality Control and Standardization Issues

4.3 Technology and Manufacturing Landscape

4.3.1 Upstream Processing (Cell Culture Systems)

4.3.2 Downstream Processing (Purification and Filtration)

4.3.3 Suspension vs Adherent Cell Culture

4.3.4 Single-use Bioreactors

4.3.5 Continuous Manufacturing

4.3.6 Automation and Digital Bioprocessing

4.4 Viral Vector Manufacturing Ecosystem

4.4.1 Biopharmaceutical Companies

4.4.2 CDMOs and CMOs

4.4.3 Technology and Equipment Providers

4.4.4 Research Institutions

4.4.5 Regulatory Bodies

4.5 Value Chain Analysis

4.5.1 Vector Design and Development

4.5.2 Cell Line Development

4.5.3 Upstream Manufacturing

4.5.4 Downstream Processing

4.5.5 Fill and Finish

4.5.6 Distribution

4.6 Regulatory Landscape

4.6.1 FDA and EMA Guidelines for Viral Vectors

4.6.2 GMP Compliance

4.6.3 Clinical and Commercial Manufacturing Regulations

4.7 Industry Trends

4.7.1 Shift Toward Large-scale Manufacturing

4.7.2 Increasing Outsourcing to CDMOs

4.7.3 Development of Next-generation Vectors

4.7.4 Integration of AI in Bioprocess Optimization

4.8 Cost and Pricing Analysis

4.8.1 Cost by Vector Type

4.8.2 Cost Breakdown by Manufacturing Stage

4.8.3 CDMO Pricing Models

5. Viral Vector Manufacturing Market, by Vector Type

5.1 Introduction

5.2 Adeno-associated Virus (AAV)

5.3 Lentiviral Vectors

5.4 Adenoviral Vectors

5.5 Retroviral Vectors

5.6 Other Viral Vectors

6. Viral Vector Manufacturing Market, by Workflow Stage

6.1 Introduction

6.2 Upstream Processing

6.2.1 Cell Expansion

6.2.2 Vector Production

6.3 Downstream Processing

6.3.1 Purification

6.3.2 Filtration

6.3.3 Concentration

6.4 Fill and Finish

7. Viral Vector Manufacturing Market, by Product and Service

7.1 Introduction

7.2 Instruments and Equipment

7.2.1 Bioreactors

7.2.2 Filtration Systems

7.2.3 Chromatography Systems

7.3 Consumables and Reagents

7.3.1 Cell Culture Media

7.3.2 Kits and Assays

7.3.3 Reagents

7.4 Services

7.4.1 Contract Manufacturing (CDMO and CMO)

7.4.2 Process Development Services

7.4.3 Analytical and QC Services

8. Viral Vector Manufacturing Market, by Manufacturing Scale

8.1 Preclinical

8.2 Clinical (Phase I to III)

8.3 Commercial Production

9. Viral Vector Manufacturing Market, by Application

9.1 Introduction

9.2 Gene Therapy

9.3 Cell Therapy

9.4 Vaccine Production

9.5 Research Applications

10. Viral Vector Manufacturing Market, by End User

10.1 Biopharmaceutical Companies

10.2 CDMOs and CMOs

10.3 Academic and Research Institutes

11. Viral Vector Manufacturing Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Italy

11.3.5 Spain

11.3.6 Netherlands

11.3.7 Sweden

11.3.8 Switzerland

11.3.9 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 Japan

11.4.3 India

11.4.4 South Korea

11.4.5 Australia

11.4.6 Singapore

11.4.7 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Rest of MEA

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Emerging Players

12.5 Market Ranking/Positioning Analysis

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Thermo Fisher Scientific Inc.

13.2 Danaher Corporation (Cytiva)

13.3 Lonza Group AG

13.4 Catalent, Inc.

13.5 Samsung Biologics Co., Ltd.

13.6 Fujifilm Diosynth Biotechnologies

13.7 WuXi AppTec Co., Ltd.

13.8 Oxford Biomedica plc

13.9 Sartorius AG

13.10 Merck KGaA

13.11 Charles River Laboratories International, Inc.

13.12 AGC Biologics

13.13 Takara Bio Inc.

13.14 GenScript Biotech Corporation

13.15 Cobra Biologics

14. Appendix

14.1 Customization Options

14.2 Related Reports

Published Date: Jun-2025

Published Date: Jun-2024

Published Date: Jun-2026

Subscribe to get the latest industry updates