Resources

About Us

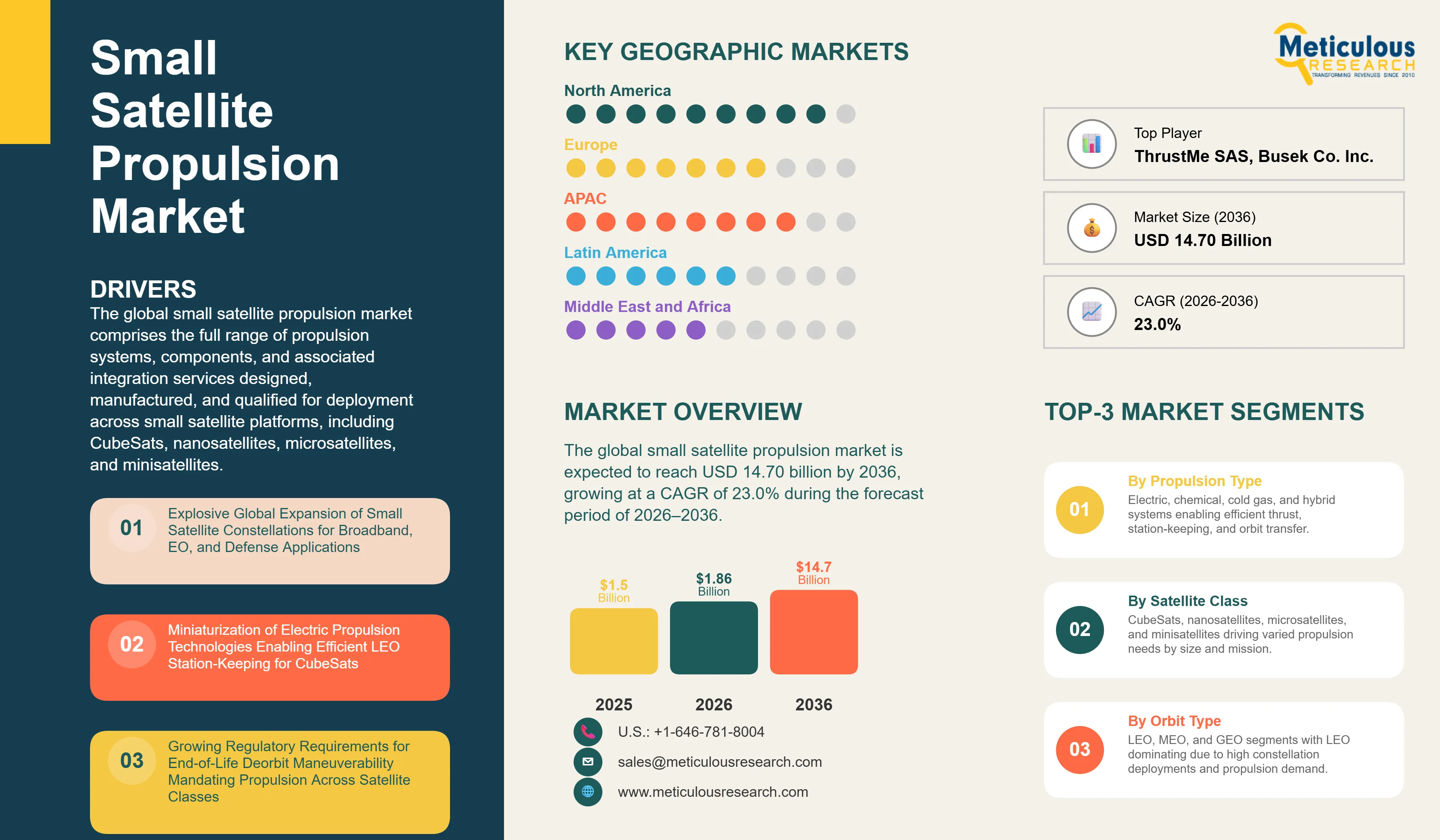

The global small satellite propulsion market was valued at USD 1.50 billion in 2025. This market is expected to reach USD 14.70 billion by 2036 from an estimated USD 1.86 billion in 2026, growing at a CAGR of 23.0% during the forecast period of 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global small satellite propulsion market comprises the full range of propulsion systems, components, and associated integration services designed, manufactured, and qualified for deployment across small satellite platforms, including CubeSats, nanosatellites, microsatellites, and minisatellites. The market includes electric propulsion systems, such as Hall-effect thrusters, ion thrusters, electrospray thrusters, and pulsed plasma thrusters; chemical propulsion systems, including monopropellant, bipropellant, and green propellant solutions; cold gas propulsion systems; and emerging hybrid propulsion architectures.

These systems support mission-critical functions, including orbit raising from launch vehicle insertion to the designated operational orbit, station-keeping to counter atmospheric drag and solar radiation pressure, collision avoidance and conjunction management, precision attitude control, orbital transfer, and end-of-life deorbit maneuvering, which is increasingly being mandated under global space debris mitigation and orbital sustainability regulations.

The growth of the global small satellite propulsion market is primarily driven by the rapid expansion of satellite constellations for broadband connectivity, Earth observation, and national security applications, which is significantly increasing propulsion system procurement volumes.

In addition, the continued miniaturization of electric propulsion technologies is enabling efficient station-keeping, orbit-raising, collision avoidance, and end-of-life deorbiting for CubeSats, nanosatellites, and microsatellites at commercially viable cost points. The growing emphasis on regulatory compliance and orbital sustainability, particularly requirements related to controlled deorbiting and space debris mitigation, is further driving the adoption of propulsion systems across satellite classes that previously operated without dedicated propulsion capability.

However, the high development and qualification costs associated with next-generation propulsion technologies for compact satellite platforms, the technical complexity of integrating propulsion systems within stringent volume, mass, and power constraints, and supply chain limitations related to specialty propellants, precision valves, micro-thrusters, and advanced materials restrain market growth.

The increasing transition toward green propulsion systems, replacing conventional hydrazine-based monopropellants with environmentally compliant alternatives such as AF-M315E and LMP-103S, the growing adoption of multi-mode propulsion architectures that combine chemical and electric propulsion for greater mission flexibility, and the expansion of in-orbit servicing, orbital transfer, and active debris removal applications are expected to create significant growth opportunities for market players.

Furthermore, the declining cost of LEO access through rideshare and reusable launch programs, which is enabling larger and more frequent constellation deployments, is a major trend shaping the growth of this market.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 14.70 Billion |

|

Market Size in 2026 |

USD 1.86 Billion |

|

Market Size in 2025 |

USD 1.50 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 23.0% |

|

Dominating Propulsion Type |

Electric Propulsion |

|

Fastest Growing Propulsion Type |

Hybrid Propulsion |

|

Dominating Satellite Class |

Microsatellites |

|

Fastest Growing Satellite Class |

CubeSats |

|

Dominating Orbit Type |

Low Earth Orbit (LEO) |

|

Dominating Application |

Communication |

|

Fastest Growing Application |

Earth Observation |

|

Dominating End User |

Commercial |

|

Fastest Growing End User |

Government & Defense |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Green Propellant Transition Replacing Hydrazine Across Small Satellite Propulsion Systems

The transition from hydrazine-based monopropellant systems to environmentally compliant green propellant alternatives, including AF-M315E (ASCENT) developed by L3Harris Technologies, Inc. / Aerojet Rocketdyne heritage programs, LMP-103S (HPGP) developed by ECAPS (now part of Bradford Space heritage), and nitrous oxide-based formulations, represents one of the most significant technology trends in small satellite chemical propulsion.

While hydrazine has historically offered well-established performance and extensive flight heritage, it poses substantial operational and regulatory challenges due to its toxicity and carcinogenicity, requiring specialized hazardous-material handling infrastructure at launch and integration facilities and facing increasing regulatory scrutiny across multiple jurisdictions. Green propellant systems offer approximately 12–15% higher specific impulse, along with significantly higher volumetric efficiency, while materially reducing ground handling complexity and associated fueling costs.

NASA’s Green Propellant Infusion Mission (GPIM) successfully validated AF-M315E in orbit, establishing its technical and commercial viability for next-generation satellite propulsion applications. In parallel, commercial and government small satellite operators are increasingly evaluating and adopting green propulsion solutions to improve performance, simplify launch-site operations, and align with evolving environmental and safety regulations.

Iodine and Xenon-Alternative Propellants Addressing Electric Propulsion Supply Chain Constraints

The growing adoption of alternative propellants for electric propulsion systems, mainly iodine as a substitute for xenon in Hall-effect and ion thruster applications, is helping address one of the key supply chain constraints in the small satellite propulsion market. Xenon is produced in limited quantities as a byproduct of industrial air-separation processes and remains subject to significant price volatility and potential supply shortages as electric propulsion deployment scales with mega-constellation programs and proliferated LEO architectures.

Iodine-based propulsion has emerged as a commercially viable alternative, offering higher storage density and eliminating the need for high-pressure propellant tanks that typically increase volume, mass, and integration complexity in compact satellite platforms. ThrustMe has successfully demonstrated an iodine-propelled electric thruster in orbit, with the propellant stored in solid form at room temperature, thereby enabling more efficient integration within highly constrained CubeSat and nanosatellite form factors.

In addition, alternative propellant technologies such as ionic liquid electrospray thrusters and krypton-based radio-frequency propulsion systems are further diversifying the propulsion ecosystem. These innovations are expanding electric propulsion accessibility across the full range of small satellite classes while reducing dependence on conventional noble gas supply chains and lowering total propulsion system costs.

End-of-Life Deorbit Regulations Creating Mandatory Propulsion Market Across Previously Unpropelled Satellites

The increasingly stringent global regulatory environment for orbital debris mitigation is creating a substantial new mandatory demand category for small satellite propulsion systems. Satellite classes that historically operated without onboard propulsion, particularly CubeSats and nanosatellites, are now increasingly required to demonstrate end-of-life disposal capability within defined regulatory timelines following mission completion.

A key regulatory milestone is the U.S. Federal Communications Commission’s (FCC) adoption of the five-year post-mission disposal rule for satellites operating in or passing through low Earth orbit (LEO) below 2,000 km, which replaced the earlier 25-year guideline and became effective for applicable missions from 2024 onward. In parallel, global debris mitigation frameworks, including ITU-aligned and national orbital sustainability guidelines, are progressively moving toward shorter post-mission disposal timelines.

These regulatory requirements are driving the addressable propulsion market by effectively converting previously unpropelled satellite segments into mandatory propulsion procurement opportunities. This trend is driving demand for miniaturized cold-gas, electrospray, water-based, and low-power electric propulsion systems designed for CubeSat and nanosatellite platforms.

As a result, regulatory compliance is emerging as a major driver of propulsion system adoption across the small satellite ecosystem.

By Propulsion Type: In 2026, the Electric Propulsion Segment to Dominate the Global Small Satellite Propulsion Market

Based on propulsion type, the global small satellite propulsion market is segmented into electric propulsion (Hall-effect thrusters, ion thrusters, electrospray/FEEP thrusters, pulsed plasma thrusters), chemical propulsion (monopropellant, bipropellant, green propellant), cold gas propulsion, and hybrid propulsion.

In 2026, the electric propulsion segment is expected to account for the largest share of around 55–60% of the global small satellite propulsion market. The large share of this segment is attributed to the dominant adoption of Hall‑effect and ion‑thruster systems by commercial LEO constellation operators, for whom electric propulsion’s superior specific impulse of 1,500–3,000 seconds, versus 200–300 seconds for chemical alternatives, translates directly into reduced propellant mass, lower launch cost, extended mission lifetime, and improved orbital‑slot management capability. SpaceX’s Starlink V2 satellites, Amazon Kuiper, and OneWeb constellation satellites all use electric propulsion for station‑keeping and collision avoidance, creating massive and sustained procurement volumes.

However, the hybrid propulsion segment is projected to register the highest CAGR during the forecast period. The rapid growth of this segment is driven by the growing adoption of multi‑mode propulsion architectures that combine high‑thrust chemical systems for rapid orbit‑raising following rideshare launches with high‑efficiency electric systems for station‑keeping throughout operational life, enabling satellite operators to optimize both deployment timeline and in‑service propellant efficiency within a single propulsion platform.

By Satellite Class: In 2026, the Microsatellites Segment to Hold the Largest Share

Based on satellite class, the global small satellite propulsion market is segmented into CubeSats (1U, 3U, 6U, 12U), nanosatellites (1–10 kg, 10–50 kg), microsatellites (50–200 kg), and minisatellites (200–1,000 kg).

In 2026, the microsatellites segment is expected to account for the largest share of the global small satellite propulsion market by revenue. This is primarily attributed to the significantly higher per-unit value of propulsion systems deployed in microsatellite platforms, which typically include advanced electric propulsion packages, such as Hall-effect thrusters, ion thrusters, and integrated propulsion modules, compared with lower-cost cold-gas and micro-propulsion systems used in CubeSats. In addition, microsatellites continue to be the preferred platform for high-capacity LEO communication, Earth observation, and defense constellation nodes, thereby driving substantial propulsion system procurement volumes.

However, the CubeSats segment is projected to register the highest CAGR during the forecast period. The rapid growth of this segment is primarily driven by the sharp increase in CubeSat deployment volumes across commercial, academic, and defense applications, the growing regulatory requirement for end-of-life deorbit capability in previously unpropelled missions, and the continued miniaturization of electrospray, iodine-based ion thrusters, cold-gas systems, and other compact propulsion technologies into 1U- and 3U-compatible form factors. These developments are making propulsion systems increasingly commercially accessible to the full spectrum of CubeSat operators, including universities, emerging space startups, and defense technology demonstrator programs.

By Orbit Type: In 2026, Low Earth Orbit to Account for the Largest Share

Based on orbit type, the global small satellite propulsion market is segmented into low earth orbit, medium earth orbit, and geostationary earth orbit. In 2026, the LEO segment is expected to account for the largest share of the global small satellite propulsion market, indicating the dominant role of LEO constellation deployments in driving small satellite propulsion procurement volumes. LEO satellites experience atmospheric drag that requires continuous station‑keeping thrust, creating ongoing propulsion demand throughout the operational lifetime rather than a one‑time orbit‑raising requirement, and the collision‑avoidance maneuvering requirements of increasingly congested LEO orbital shells represent a growing propulsion duty cycle per satellite.

By Application: In 2026, the Communication Segment to Hold the Largest Share

Based on application, the global small satellite propulsion market is segmented into communication, earth observation and remote sensing, navigation, scientific research, technology demonstration, and other applications. In 2026, the communication segment is expected to account for the largest share of the global small satellite propulsion market. The leading share of this segment is primarily attributed to the large-scale deployment of LEO broadband communication constellations, including Space Exploration Technologies Corp. Starlink, Amazon Project Kuiper, Eutelsat OneWeb, and Telesat Lightspeed, which continue to represent the primary volume driver for propulsion system procurement. These mega-constellation programs collectively comprise thousands of propulsion-equipped satellites and are expected to generate substantial propulsion hardware demand throughout the forecast period.

However, the earth observation and remote sensing segment is projected to register the highest CAGR during the forecast period. The strong growth of this segment is primarily driven by the growing deployment of Earth observation constellations by Planet Labs PBC, ICEYE Oy, Satellogic Inc., BlackSky Technology Inc., and various government-sponsored space programs. These deployments require advanced propulsion systems for precise orbit maintenance, orbital plane adjustments, rapid retasking, station-keeping, and collision avoidance in increasingly congested observation orbital shells, thereby driving robust market growth in this segment.

By End User: In 2026, the Commercial Segment to Hold the Largest Share

Based on end user, the global small satellite propulsion market is segmented into commercial, government and defense, and academic and research. In 2026, the commercial segment is expected to account for the largest share of the global small satellite propulsion market. The segment’s leading share is primarily attributed to the dominant role of commercial LEO constellation operators as the largest volume procurers of small satellite propulsion hardware globally. This segment includes broadband connectivity operators, Earth observation and geospatial data companies, maritime and aviation tracking service providers, and IoT connectivity platform providers, all of which are deploying propulsion-equipped small satellites at unprecedented commercial scale.

However, the government and defense segment is projected to register the highest CAGR during the forecast period. The robust growth of this segment is driven by accelerating national investments in proliferated LEO satellite architectures for defense surveillance, secure strategic communications, missile warning, and space situational awareness applications, all of which require highly maneuverable, propulsion-equipped small satellites to support responsive space operations. In addition, increasing investments in in-orbit servicing, orbital transfer, and active debris removal missions are expected to further drive demand for advanced small satellite propulsion systems in this segment.

Based on geography, the global small satellite propulsion market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of the global small satellite propulsion market. The region’s dominant position is primarily supported by the high concentration of small satellite operators, constellation developers, and launch-service providers, including Space Exploration Technologies Corp., Amazon, Planet Labs PBC, and a large ecosystem of emerging commercial space companies.

In addition, the presence of leading propulsion technology providers, such as L3Harris Technologies, Inc. / Aerojet Rocketdyne heritage programs, Moog Inc., Busek Co. Inc., and Phase Four, Inc., combined with strong procurement from NASA, the U.S. Space Force, DARPA, and the National Reconnaissance Office, continues to support regional market leadership. Furthermore, the U.S. FCC’s five-year post-mission disposal mandate is driving additional regulatory-led propulsion demand across the domestic commercial satellite ecosystem, sustaining North America’s leading share through the forecast period.

However, the Asia Pacific small satellite propulsion market is projected to register the highest CAGR during the forecast period. The strong growth of this region is primarily driven by China’s accelerated domestic small satellite constellation buildout, including the Guowang and other national broadband and Earth observation programs, India’s liberalized space policy framework that is enabling rapid private-sector participation, and Japan and South Korea’s expanding investments in national and commercial LEO satellite initiatives.

In addition, the emergence of indigenous propulsion technology companies, such as Bellatrix Aerospace in India, is strengthening regional manufacturing capabilities and reducing reliance on foreign supply chains. These concurrent national and commercial initiatives are expected to drive the fastest regional growth in the Asia Pacific small satellite propulsion market between 2026 and 2036.

The global small satellite propulsion market is characterized by a dual-tier competitive structure, comprising an established tier of aerospace and defense prime contractors and specialist propulsion technology companies serving the microsatellite and minisatellite segments, alongside a rapidly expanding new-space tier of startups and scale-up companies targeting CubeSat and nanosatellite platforms with miniaturized, commercially accessible propulsion solutions.

L3Harris Technologies, Inc. (Aerojet Rocketdyne heritage) maintains a strong position in green monopropellant propulsion systems through its ASCENT (AF-M315E) program and advanced Hall-effect thruster product portfolio. Moog Inc. competes across both chemical and electric propulsion technologies, supported by extensive flight heritage across government, defense, and commercial space programs. Busek Co. Inc. remains a leading specialist in Hall-effect, ion, and electrospray thrusters for small satellite applications, with strong program experience across NASA and U.S. defense initiatives. Bradford Space AB continues to hold a strong position in high-performance green propulsion solutions.

At the same time, emerging new-space propulsion companies, such as ThrustMe SAS (France), Phase Four, Inc. (U.S.), ENPULSION GmbH (Austria), and propulsion platforms supported by Rocket Lab USA, Inc.’s Sinclair Interplanetary heritage, are gaining increasing commercial market share through highly miniaturized, cost-efficient propulsion solutions designed for CubeSat and constellation deployments.

The report provides a detailed competitive assessment of leading market participants based on their product portfolios, regional presence, technological capabilities, strategic developments, partnerships, contracts, and key growth initiatives undertaken over the last few years.

Some of the key players operating in the global small satellite propulsion market include L3Harris Technologies, Inc. (U.S.), Moog Inc. (U.S.), Busek Co. Inc. (U.S.), Bradford Space AB (Sweden), Thales Alenia Space SAS (France), Northrop Grumman Corporation (U.S.), Rocket Lab USA, Inc. (U.S.), ThrustMe SAS (France), Phase Four, Inc. (U.S.), ENPULSION GmbH (Austria), Bellatrix Aerospace Pvt. Ltd. (India), GomSpace Group AB (Denmark), Dawn Aerospace Holdings Limited (New Zealand/Netherlands), Applied Ion Systems, Inc. (U.S.), and Momentus Inc. (U.S.).

The global small satellite propulsion market is expected to reach USD 14.70 billion by 2036 from an estimated USD 1.86 billion in 2026, at a CAGR of 23.0% during the forecast period 2026–2036.

In 2026, the electric propulsion segment is expected to hold the largest share of approximately 55–60% of the global small satellite propulsion market, driven by Hall-effect and ion thruster adoption for LEO constellation station-keeping.

The hybrid propulsion segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by growing adoption of multi-mode systems combining chemical and electric propulsion for mission flexibility.

In 2026, the microsatellites segment is expected to hold the largest share of the global small satellite propulsion market by revenue.

The CubeSats segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by explosive deployment volume growth, deorbit regulation mandates, and miniaturized propulsion accessibility.

The growth of this market is primarily driven by the explosive expansion of small satellite constellations for broadband connectivity, Earth observation, and national security applications; the accelerating miniaturization of electric propulsion for CubeSats and nanosatellites; and growing regulatory requirements for deorbit maneuverability mandating propulsion across previously unpropelled satellite classes.

Key players operating in the global small satellite propulsion market include L3Harris Technologies, Inc. (Aerojet Rocketdyne heritage) (U.S.), Moog Inc. (U.S.), Busek Co. Inc. (U.S.), Bradford Space AB (ECAPS heritage) (Sweden), Thales Alenia Space SAS (France), Northrop Grumman Corporation (U.S.), Rocket Lab USA, Inc. (U.S.), ThrustMe SAS (France), Phase Four, Inc. (U.S.), ENPULSION GmbH (Austria), Bellatrix Aerospace Pvt. Ltd. (India), GomSpace Group AB (Denmark), Dawn Aerospace Holdings Limited (New Zealand/Netherlands), Applied Ion Systems, Inc. (U.S.), and Momentus Inc. (U.S.).

Asia Pacific is expected to register the highest growth rate in the global small satellite propulsion market during the forecast period 2026–2036.

1 Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2 Research Methodology

2.1 Research Approach

2.2 Data Collection and Validation

2.2.1 Secondary Research

2.2.2 Primary Research and Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Country and Region Level Analysis

2.3 Market Assessment

2.3.1 Market Size Estimation

2.3.2 Bottom Up Approach

2.3.3 Top Down Approach

2.3.4 Growth Forecast

2.4 Assumptions for the Study

3 Executive Summary

3.1 Market Overview

3.2 Market Analysis by Propulsion Type

3.3 Market Analysis by Satellite Class

3.4 Market Analysis by Orbit Type

3.5 Market Analysis by Application

3.6 Market Analysis by End User

3.7 Market Analysis by Geography

4 Market Dynamics

4.1 Overview

4.2 Drivers

4.2.1 Explosive Global Expansion of Small Satellite Constellations for Broadband, EO, and Defense Applications

4.2.2 Miniaturization of Electric Propulsion Technologies Enabling Efficient LEO Station-Keeping for CubeSats

4.2.3 Growing Regulatory Requirements for End-of-Life Deorbit Maneuverability Mandating Propulsion Across Satellite Classes

4.2.4 Declining LEO Launch Costs Through Rideshare Programs Expanding Economically Viable Constellation Scale

4.3 Restraints

4.3.1 High Development Cost and Limited Flight Heritage of Novel Propulsion Technologies for CubeSat Form Factors

4.3.2 Technical Complexity of Integrating Propulsion Within Volume and Mass Constraints of Small Satellites

4.4 Opportunities

4.4.1 Green Propellant Transition Replacing Hydrazine Across Small Satellite Chemical Propulsion Systems

4.4.2 Iodine and Alternative Propellants Addressing Electric Propulsion Xenon Supply Chain Constraints

4.4.3 In-Orbit Servicing and Active Debris Removal Creating New Advanced Propulsion Demand Categories

4.5 Challenges

4.5.1 Supply Chain Constraints for Specialty Materials Including Xenon and High-Purity Propellant Feedstocks

4.5.2 Export Control Regulations Restricting International Collaboration on Advanced Propulsion Technologies

4.6 Porter’s Five Forces Analysis

5 Small Satellite Propulsion Market, by Propulsion Type

5.1 Overview

5.2 Electric Propulsion

5.2.1 Hall-Effect Thrusters

5.2.2 Ion Thrusters

5.2.3 Electrospray / FEEP Thrusters

5.2.4 Pulsed Plasma Thrusters

5.3 Chemical Propulsion

5.3.1 Monopropellant Systems

5.3.2 Bipropellant Systems

5.3.3 Green Propellant Systems

5.4 Cold Gas Propulsion

5.5 Hybrid Propulsion

6 Small Satellite Propulsion Market, by Satellite Class

6.1 Overview

6.2 CubeSats

6.2.1 1U

6.2.2 3U

6.2.3 6U

6.2.4 12U and Above

6.3 Nanosatellites

6.3.1 1–10 kg

6.3.2 10–50 kg

6.4 Microsatellites (50–200 kg)

6.5 Minisatellites (200–1,000 kg)

7 Small Satellite Propulsion Market, by Orbit Type

7.1 Overview

7.2 Low Earth Orbit (LEO)

7.3 Medium Earth Orbit (MEO)

7.4 Geostationary Earth Orbit (GEO)

8 Small Satellite Propulsion Market, by Application

8.1 Overview

8.2 Communication

8.3 Earth Observation & Remote Sensing

8.4 Navigation

8.5 Scientific Research

8.6 Technology Demonstration

8.7 Other Applications

9 Small Satellite Propulsion Market, by End User

9.1 Overview

9.2 Commercial

9.3 Government & Defense

9.4 Academic & Research

10 Small Satellite Propulsion Market, by Geography

10.1 Overview

10.2 North America

10.2.1 U.S.

10.2.2 Canada

10.3 Europe

10.3.1 U.K.

10.3.2 France

10.3.3 Germany

10.3.4 Italy

10.3.5 Sweden

10.3.6 Finland

10.3.7 Netherlands

10.3.8 Rest of Europe

10.4 Asia Pacific

10.4.1 China

10.4.2 India

10.4.3 Japan

10.4.4 South Korea

10.4.5 Australia

10.4.6 Singapore

10.4.7 Rest of Asia Pacific

10.5 Latin America

10.5.1 Brazil

10.5.2 Mexico

10.5.3 Argentina

10.5.4 Chile

10.5.5 Rest of Latin America

10.6 Middle East and Africa

10.6.1 Israel

10.6.2 UAE

10.6.3 Saudi Arabia

10.6.4 South Africa

10.6.5 Rest of Middle East and Africa

11 Competitive Landscape

11.1 Introduction

11.2 Key Growth Strategies

11.2.1 Market Differentiators

11.2.2 Strategic Alliances and Partnerships

11.3 Competitive Benchmarking

11.4 Competitive Dashboard

11.4.1 Industry Leaders

11.4.2 Market Differentiators

11.4.3 Vanguards

11.4.4 Emerging Companies

11.5 Market Ranking and Positioning of Key Players

12 Company Profiles

12.1 L3Harris Technologies, Inc. (Aerojet Rocketdyne heritage)

12.2 Moog Inc.

12.3 Busek Co. Inc.

12.4 Bradford Space AB (ECAPS heritage)

12.5 Thales Alenia Space SAS

12.6 Northrop Grumman Corporation

12.7 Rocket Lab USA, Inc.

12.8 ThrustMe SAS

12.9 Phase Four, Inc.

12.10 ENPULSION GmbH

12.11 Bellatrix Aerospace Pvt. Ltd.

12.12 GomSpace Group AB

12.13 Dawn Aerospace Holdings Limited

12.14 Applied Ion Systems, Inc.

12.15 Momentus Inc.

12.16 Others

13 Appendix

13.1 Questionnaire

13.2 Available Customization Options

13.3 Related Reports

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Feb-2026

Subscribe to get the latest industry updates