Resources

About Us

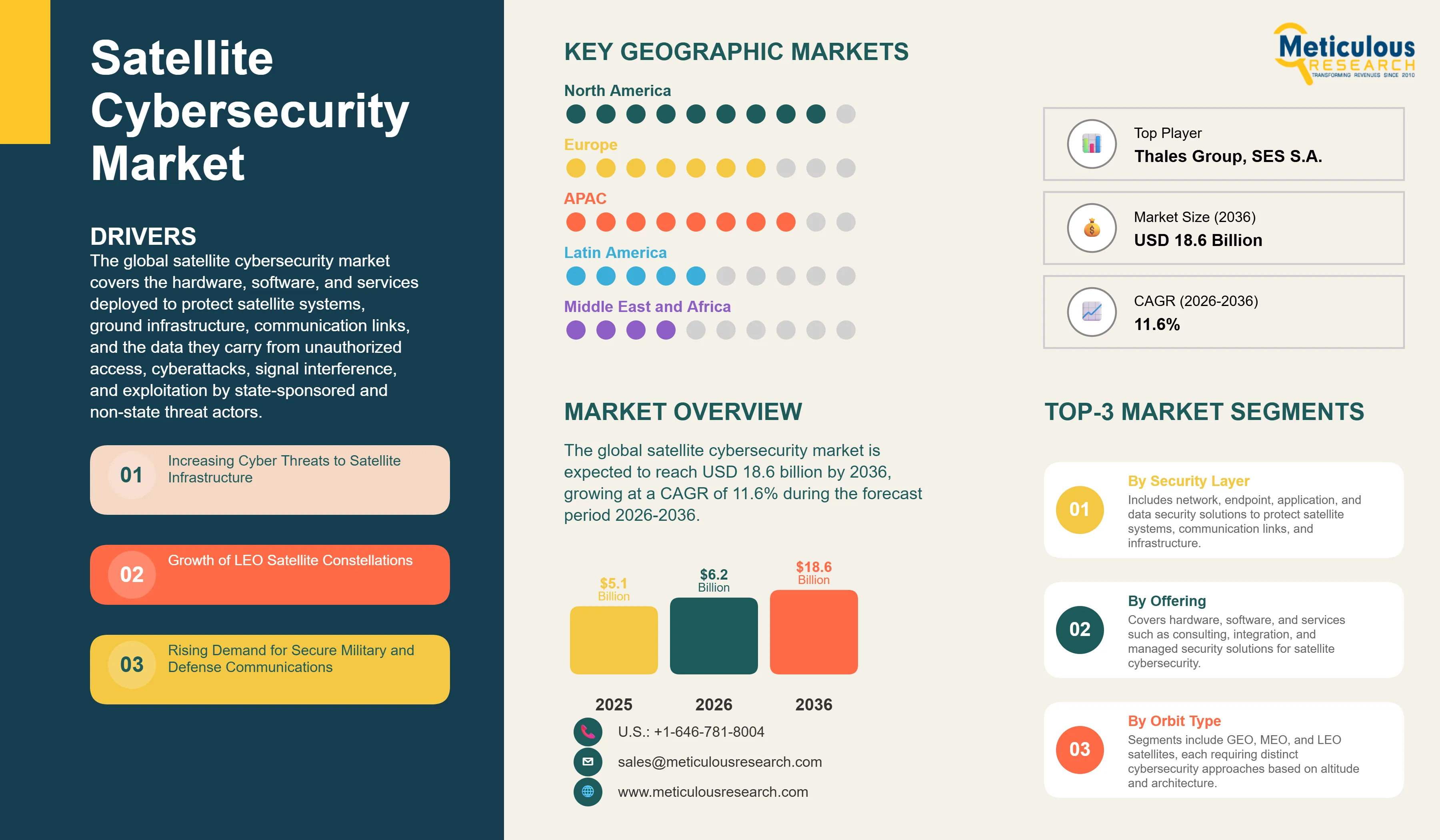

Satellite Cybersecurity Market Size, Share & Trends Analysis by Security Layer, Offering, Orbit Type, End User, Deployment Model, and Threat Type - Global Opportunity Analysis & Industry Forecast (2026-2036)

Report ID: MRAD - 1041905 Pages: 265 Apr-2026 Formats*: PDF Category: Aerospace and Defense Delivery: 24 to 72 Hours Download Free Sample ReportThe global satellite cybersecurity market was valued at USD 5.1 billion in 2025. This market is expected to reach USD 18.6 billion by 2036 from an estimated USD 6.2 billion in 2026, growing at a CAGR of 11.6% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global satellite cybersecurity market covers the hardware, software, and services deployed to protect satellite systems, ground infrastructure, communication links, and the data they carry from unauthorized access, cyberattacks, signal interference, and exploitation by state-sponsored and non-state threat actors. This encompasses network security solutions including firewalls and intrusion detection systems adapted for satellite network architectures, endpoint security for satellite payloads and ground station terminals, application and mission software security, encryption and data integrity protection for uplink and downlink communications, identity and access management for satellite command and control systems, and the managed security services and consulting programs that support satellite operators in assessing, implementing, and maintaining cybersecurity postures across the increasingly complex attack surfaces of modern satellite systems.

The growth of the global satellite cybersecurity market is primarily driven by the dramatically escalating cyber threat environment targeting satellite infrastructure, demonstrated by high-profile incidents including the February 2022 cyberattack on Viasat's KA-SAT network that disrupted satellite internet services across Ukraine and Europe at the outset of the Russia-Ukraine conflict, which established satellite communications infrastructure as a primary target of state-sponsored offensive cyber operations and catalyzed emergency security investment across commercial and government satellite operators globally. The extraordinary growth of low earth orbit satellite constellations, with SpaceX's Starlink network exceeding 6,000 operational satellites, Amazon's Kuiper constellation in initial deployment, and multiple OneWeb and similar programs expanding the orbital satellite population by an order of magnitude, is creating an unprecedented expansion of the satellite attack surface that demands proportional expansion of cybersecurity coverage across thousands of connected satellite endpoints.

Two significant opportunities are shaping the market's long-term trajectory. The development and adoption of zero-trust security architectures specifically engineered for space system environments represents the most strategically important near-term security framework opportunity, as the traditional perimeter-based security model is fundamentally inadequate for distributed satellite constellations with thousands of autonomous nodes, multiple ground stations across different security jurisdictions, and extensive third-party service integration that creates complex trust boundary management challenges requiring zero-trust principles of continuous verification and least-privilege access. The integration of AI and machine learning-based threat detection platforms capable of processing the large volumes of telemetry, command and control traffic, and communication metadata generated by large satellite constellations in real time to detect anomalous behavior patterns indicative of cyber intrusion or signal manipulation represents a transformative capability upgrade over signature-based detection approaches that cannot keep pace with the novelty and sophistication of state-sponsored satellite cyberattack techniques.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 18.6 Billion |

|

Market Size in 2026 |

USD 6.2 Billion |

|

Market Size in 2025 |

USD 5.1 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 11.6% |

|

Dominating Security Layer |

Network Security |

|

Fastest Growing Security Layer |

Data Security |

|

Dominating Offering |

Services |

|

Fastest Growing Offering |

Software |

|

Dominating Orbit Type |

Geostationary Orbit (GEO) |

|

Fastest Growing Orbit Type |

Low Earth Orbit (LEO) |

|

Dominating Application |

Military & Defense |

|

Fastest Growing Application |

Commercial Communications |

|

Dominating End User |

Government and Defense Agencies |

|

Fastest Growing End User |

Commercial Satellite Operators |

|

Dominating Deployment Model |

On-Premises |

|

Fastest Growing Deployment Model |

Cloud-Based |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Nation-State Cyber Threats Elevating Satellite Security to Strategic Priority

The demonstrated willingness and capability of nation-state actors to conduct offensive cyber operations targeting satellite communications infrastructure has fundamentally elevated satellite cybersecurity from a technical risk management concern to a strategic national security priority that is driving emergency and sustained investment from both government defense programs and commercial satellite operators. The Viasat KA-SAT attack of February 2022, attributed by the U.S., EU, and UK governments to Russian military intelligence, demonstrated that commercial satellite internet infrastructure is within the established target set for state-sponsored cyber offensive operations and that successful attacks can achieve strategic military effects by disrupting communications for both military and civilian users across entire regions. The Russian military's persistent use of GPS jamming and spoofing operations across conflict zones and adjacent civilian airspace, documented extensively in the Baltic Sea region and Black Sea, illustrates the operational integration of satellite signal manipulation into modern hybrid warfare doctrine.

The strategic cyber threat environment has directly driven very large government-funded satellite cybersecurity investment programs. The U.S. Space Force's establishment of dedicated space cybersecurity mission areas, the European Union's Space Program Agency's security requirements for Galileo and Copernicus infrastructure, and NATO's space domain integration into alliance cyber defense responsibilities are collectively creating large institutional demand for satellite cybersecurity solutions at the most demanding government security classification levels. Commercial satellite operators that serve government and defense customers face cascading requirements to demonstrate compliance with government cybersecurity standards including NIST SP 800-53 and the U.S. Space Policy Directive-5 Cybersecurity Principles for Space Systems as conditions of government service contracts, creating commercially mandatory cybersecurity investment incentives beyond purely defensive motivations.

LEO Constellation Expansion Driving New Security Architecture Requirements

The extraordinary expansion of low earth orbit satellite constellations from a handful of large GEO satellites to thousands of small satellites operated by SpaceX, Amazon, OneWeb, and multiple government programs is fundamentally reshaping the satellite cybersecurity market by creating security architecture challenges that have no precedent in the traditional GEO satellite security framework. A LEO mega-constellation like Starlink requires cybersecurity coverage across more than 6,000 individual satellite nodes, hundreds of ground station terminals, complex inter-satellite link networks, and millions of user terminals connected through the same infrastructure, creating a vastly larger attack surface than any previous satellite system and requiring security monitoring and response capabilities of a scale and speed that manual security operations cannot support.

The security architecture challenges of LEO constellations are driving demand for automation-heavy, software-defined security platforms that can scale across thousands of satellite endpoints, apply consistent security policies through software-defined networking and centralized policy management, and detect anomalous behavior patterns across the entire constellation through AI-powered analytics of telemetry and communication metadata. The relatively constrained computing resources of small LEO satellites compared with large GEO spacecraft creates a specific engineering challenge for onboard security implementations that must balance security processing requirements against the power and compute budgets of mass-produced small satellites, driving innovation in lightweight cryptography, hardware security module design, and resource-efficient intrusion detection algorithms optimized for the satellite embedded computing environment.

AI-Powered Threat Detection and Automated Response Emerging as Standard

The integration of artificial intelligence and machine learning into satellite cybersecurity monitoring, threat detection, and incident response platforms is transitioning from a premium capability feature to an operational necessity as the volume of security-relevant events generated by large satellite constellations and their ground infrastructure exceeds the capacity of human security analyst teams to process and triage through manual review. AI threat detection platforms trained on satellite system telemetry, command and control traffic patterns, and communication anomaly datasets can identify the subtle behavioral deviations indicative of unauthorized access, command injection, jamming precursor activity, and software compromise in satellite systems with detection speed and sensitivity that signature-based and threshold-based detection approaches cannot match against sophisticated adversary techniques.

Northrop Grumman's Mission Resilience product suite, Lockheed Martin's cyber intelligence integration for space systems, Thales Group's satellite cybersecurity monitoring platforms, and specialist providers including Kratos Defense and Viasat are all incorporating AI analytics capabilities into their satellite security solution portfolios in response to customer demand for continuous and automated threat monitoring across complex satellite network environments. The machine learning model development for satellite-specific threat detection is an emerging competitive differentiation area where the quality and breadth of training datasets derived from operational satellite system telemetry represent a significant and defensible competitive advantage for security providers with established satellite operator customer relationships that enable ongoing operational data access.

Increasing Cyber Threats to Satellite Infrastructure

The rapidly escalating volume, sophistication, and strategic impact of cyberattacks targeting satellite infrastructure is the primary driver of the global satellite cybersecurity market, as documented high-profile incidents are converting satellite cybersecurity investment from a discretionary risk management activity into a strategically mandatory capability for all satellite operators serving government, defense, or critical infrastructure-dependent customer bases. Beyond the Viasat KA-SAT attack, the documented activities of Chinese state-sponsored threat groups including APT40 and Volt Typhoon against satellite communication and ground station infrastructure, the North Korean Lazarus Group's targeting of satellite communication service providers for financial and intelligence collection purposes, and the proliferation of commercially available cyber tools enabling lower-sophistication actors to attempt satellite jamming and signal spoofing operations collectively demonstrate that the threat environment targeting satellite systems has expanded from a narrow government-to-government concern to a broad and diverse threat landscape requiring comprehensive multi-layer defensive capabilities from every satellite operator.

Growth of LEO Satellite Constellations

The deployment of LEO mega-constellations by SpaceX, Amazon, OneWeb, and government programs including the U.S. Space Development Agency's Transport Layer is expanding the total satellite attack surface by an order of magnitude relative to the traditional GEO satellite infrastructure base, generating proportional growth in satellite cybersecurity solution requirements across network monitoring, endpoint protection, communication link security, and identity and access management categories. SpaceX's Starlink constellation, which has exceeded 6,000 operational satellites and is authorized for up to 42,000 total satellites, requires cybersecurity coverage infrastructure of a scale and complexity that represents a fundamentally new market category requiring purpose-built security solutions rather than adaptations of terrestrial or GEO satellite security approaches. The rapid adoption of Starlink by military and emergency services users globally, including the Ukrainian military's use of Starlink terminals for tactical communications, is embedding LEO satellite connectivity into critical defense and emergency management functions that intensify the security requirements and create mandatory security investment drivers for constellation operators serving these customer segments.

Development of Zero-Trust Architectures for Space Systems

The adaptation and implementation of zero-trust security architecture principles specifically engineered for the unique operational and technical characteristics of space systems represents the highest-priority security framework opportunity in the satellite cybersecurity market, as the scale and distributed nature of LEO constellations, the diversity of ground station operators and partner organizations accessing satellite networks, and the demonstrated capability of nation-state adversaries to compromise individual nodes within complex satellite networks collectively make the traditional perimeter-based security model untenable for modern satellite infrastructure. Zero-trust principles requiring continuous authentication and authorization of all users, devices, and processes regardless of network location, combined with microsegmentation of satellite network access to the minimum required for each user role and the automated detection and quarantine of anomalous access behaviors, provide a security architecture fundamentally more resilient to the insider threat, supply chain compromise, and lateral movement attack techniques that characterize advanced persistent threat operations against satellite systems. The U.S. Department of Defense's mandated zero-trust implementation deadline and the Space Force's specific zero-trust guidance for space system cyber resilience are creating policy-driven adoption requirements that are translating the zero-trust opportunity into funded procurement programs for government-connected satellite operators.

Integration with AI-Based Threat Detection

The development and deployment of AI and machine learning-based threat detection platforms specifically trained and optimized for satellite system security monitoring represents a large and growing commercial opportunity for security providers capable of delivering the continuous and automated threat detection capabilities that large-scale satellite constellations require but that human-staffed security operations centers cannot provide at the speed and scale necessary for effective response. AI security platforms that can correlate anomalous telemetry patterns across thousands of satellite nodes, identify the behavioral signatures of command injection attempts against satellite control systems, detect GPS spoofing signal characteristics in navigation satellite monitoring data, and flag the network traffic anomalies associated with unauthorized uplink access to satellite payloads provide a qualitative improvement in threat detection capability that satellite operators are actively seeking as they confront the documented sophistication of nation-state adversaries operating against their infrastructure. The commercial value of satellite-specific AI security is high, as the consequences of undetected compromise in military, navigation, or critical communications satellite systems can be strategically significant, creating willingness to pay premium pricing for detection capabilities with demonstrably superior performance against known satellite attack methodologies.

By Security Layer: In 2026, Network Security to Dominate

Based on security layer, the global satellite cybersecurity market is segmented into network security, endpoint security, application security, data security, identity and access management, and other security solutions. In 2026, the network security segment is expected to account for the largest share of the global satellite cybersecurity market. The large share of this segment is attributed to network security representing the foundational and most broadly deployed security layer across satellite infrastructure, encompassing firewall and intrusion detection and prevention systems deployed at ground station network boundaries, secure communication network architecture implementations for satellite command and control links, and the network monitoring and security analytics platforms that provide visibility across the distributed network infrastructure connecting satellites, ground stations, control centers, and user terminals. The commercial satellite operator community's initial and largest security investment concentration has historically been in network perimeter security, establishing this as the highest-revenue security layer category.

However, the data security segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the escalating regulatory and contractual requirements for encryption of satellite communications carrying sensitive government, defense, and enterprise data, the demonstrated threat of satellite communication interception by state-sponsored intelligence collection programs, and the EU General Data Protection Regulation and equivalent data protection frameworks creating compliance obligations for data-in-transit protection on satellite links carrying personal data of EU residents.

By Offering: In 2026, Services to Hold the Largest Share

Based on offering, the global satellite cybersecurity market is segmented into hardware, software, and services (consulting, integration, and managed security services). In 2026, the services segment is expected to account for the largest share of the global satellite cybersecurity market. The dominance of services reflects the complexity of satellite cybersecurity implementation, which requires specialized expertise in both space system engineering and cybersecurity that is rare in the industry and typically must be supplied through consulting and system integration services rather than purely product procurement. The managed security services category, encompassing outsourced 24/7 security monitoring and incident response for satellite operators who lack the specialized satellite security expertise and staffing to operate security operations centers internally, is growing rapidly as the threat environment intensifies and the expertise gap in satellite-specific security knowledge widens.

However, the software segment is projected to register the highest CAGR during the forecast period, driven by the rapid adoption of AI-powered security analytics platforms, zero-trust policy management software, satellite-specific intrusion detection systems, and cloud-based security orchestration platforms that are displacing hardware-centric security approaches and enabling more scalable and flexible security architectures for large LEO constellations.

By Orbit Type: In 2026, GEO to Hold the Largest Share

Based on orbit type, the global satellite cybersecurity market is segmented into low earth orbit, medium earth orbit, and geostationary orbit. In 2026, the GEO segment is expected to account for the largest share of the global satellite cybersecurity market. The dominance of GEO reflects the large installed base of high-value GEO communication, broadcast, and government satellites that carry critical communications and intelligence data and have been the primary focus of satellite cybersecurity investment programs since the segment's establishment, with the per-satellite cybersecurity investment in GEO spacecraft being very high given their strategic value and multi-decade operational lifetimes. The government and military GEO communications satellites operated by national defense agencies, including the U.S. Advanced Extremely High Frequency and Wideband Global SATCOM programs, represent the highest-security and highest-investment satellite cybersecurity applications globally.

However, the LEO segment is projected to register the highest CAGR during the forecast period. This growth is driven by the extraordinary expansion of LEO satellite constellations requiring cybersecurity coverage at unprecedented scale, the demonstrated targeting of LEO infrastructure by state-sponsored adversaries, and the progressive integration of LEO satellite connectivity into military and critical infrastructure applications that elevate the security requirements and investment priority for LEO system protection.

By Application: In 2026, Military & Defense to Hold the Largest Share

Based on application, the global satellite cybersecurity market is segmented into military and defense, commercial communications, earth observation, navigation (GNSS), and scientific and research missions. In 2026, the military and defense segment is expected to account for the largest share of the global satellite cybersecurity market. Military and defense satellite applications generate the highest per-satellite and per-program cybersecurity investment of any application category, driven by the strategic consequences of successful cyberattacks on military communications and intelligence satellite systems, the classified security standards and requirements imposed on military satellite programs, and the large and growing defense budget allocations to satellite cybersecurity across the United States, NATO allies, and major national defense establishments globally. The U.S. Space Force's dedicated space cybersecurity program, the UK Space Command's satellite security investments, and France's defence spatiale cyber program represent the largest individual national defense satellite security programs.

However, the commercial communications segment is projected to register the highest CAGR during the forecast period. This growth is driven by the Viasat attack's demonstration that commercial satellite communications infrastructure is a legitimate target of state-sponsored cyberattack, the rapid expansion of LEO commercial communications constellations creating new large-scale cybersecurity requirements, and the progressive integration of commercial satellite communications into critical infrastructure and emergency services functions that elevate their security requirements toward near-government levels.

By End User: In 2026, Government and Defense Agencies to Hold the Largest Share

Based on end user, the global satellite cybersecurity market is segmented into government and defense agencies, commercial satellite operators, space agencies, and enterprises. In 2026, the government and defense agencies segment is expected to account for the largest share of the global satellite cybersecurity market. Government and defense customers represent the primary and highest-spending satellite cybersecurity customer category, generating the majority of market revenue through large-scale classified security programs for military satellite systems, national intelligence satellite infrastructure, and government communication networks that mandate the most stringent and highest-cost security implementations available. The U.S. Department of Defense's space cybersecurity budget, allocated through the Space Force, National Reconnaissance Office, and Defense Information Systems Agency programs, collectively represents the single largest national satellite cybersecurity procurement program globally.

However, the commercial satellite operators segment is projected to register the highest CAGR during the forecast period. This growth is driven by the Viasat attack-catalyzed emergency security investment at commercial operators globally, the regulatory and contractual pressure on commercial operators serving government customers to demonstrate compliance with government security standards, and the rapid expansion of commercial LEO constellations generating new large-scale security program requirements at SpaceX Starlink, Amazon Kuiper, OneWeb, and emerging commercial constellation operators.

By Deployment Model: In 2026, On-Premises to Hold the Largest Share

Based on deployment model, the global satellite cybersecurity market is segmented into on-premises, cloud-based, and hybrid deployment. In 2026, the on-premises segment is expected to account for the largest share of the global satellite cybersecurity market. On-premises security deployment dominates the military and government satellite cybersecurity market where classified operations, air-gap requirements, and national security data sovereignty considerations mandate security infrastructure under direct government physical and logical control that precludes the use of commercial cloud platforms for sensitive security monitoring and response functions. The substantial installed base of on-premises security infrastructure at established GEO satellite operator ground stations and government satellite control facilities reinforces the segment's near-term market dominance.

However, the cloud-based segment is projected to register the highest CAGR during the forecast period. This growth is driven by the growing commercial satellite operator adoption of cloud-based security analytics and managed security services platforms for their unclassified security monitoring functions, the scalability advantages of cloud-based security platforms for monitoring large LEO constellations across geographically distributed ground station networks, and the emergence of sovereign cloud deployments that address government data sovereignty requirements while providing the scalability and managed service benefits of cloud delivery models.

Satellite Cybersecurity Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global satellite cybersecurity market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global satellite cybersecurity market. The largest share of this region is mainly due to the United States' dominant position as both the world's largest operator of military and government satellite systems and the home of the majority of leading commercial satellite operators and satellite cybersecurity solution providers. The U.S. Space Force's establishment as a dedicated military branch with a specific satellite cybersecurity mission, the Space Policy Directive-5 cybersecurity framework mandating security standards for all U.S. government space systems, and the large classified cybersecurity budgets of the National Reconnaissance Office, National Geospatial-Intelligence Agency, and other U.S. space intelligence programs collectively generate the largest single-country satellite cybersecurity procurement market globally. The concentration of leading satellite cybersecurity solution providers including Northrop Grumman, Lockheed Martin, Raytheon Technologies, L3Harris, Boeing, Kratos Defense, and Viasat in the United States reinforces North America's dual role as both the largest demand market and the primary supply base for satellite cybersecurity technology globally.

However, the Asia-Pacific satellite cybersecurity market is expected to grow at the fastest CAGR during the forecast period. The region's rapid growth is driven by China's very large and growing military satellite program, encompassing reconnaissance, navigation, and communications satellites that generate substantial domestic satellite security investment within the Chinese defense establishment, alongside the expansion of Chinese commercial satellite operators including GalaxySpace and CAS Space whose LEO constellation programs are creating new commercial satellite security requirements. India's ISRO and newly privatized commercial space sector including Agnikul, Skyroot Aerospace, and OneSpace are generating growing satellite cybersecurity investment as India's space program expands its strategic ambitions and commercial space industry develops. Japan's JAXA and Japan's Self-Defense Force satellite programs, South Korea's Korea Aerospace Research Institute satellite programs, and Australia's growing space industry participation collectively contribute to the region's expanding satellite cybersecurity market.

Europe represents a well-developed and growing satellite cybersecurity market anchored by the large defense satellite programs of France, Germany, the United Kingdom, and Italy, the European Space Agency's security requirements for Galileo navigation and Copernicus earth observation infrastructure, and the established cybersecurity capabilities of European defense contractors including Airbus Defence and Space, Thales Group, and Leonardo. The European Union Space Programme Agency's mandatory security requirements for Galileo and GOVSATCOM programs, combined with the EU's National Security Directives and the European Union Agency for Cybersecurity's satellite security guidance, are creating a comprehensive policy and regulatory framework supporting European satellite cybersecurity market development. Israel's advanced satellite intelligence and space security programs represent a disproportionately important Middle East and Africa market contribution given its technical sophistication and defense export capabilities in satellite security domains.

The global satellite cybersecurity market is moderately concentrated among large defense and aerospace contractors with established classified security clearances and space system expertise, alongside specialist cybersecurity companies with developed satellite-specific security capabilities and commercial satellite operators with vertically integrated security operations. Competition is focused on security clearance levels, satellite-specific technical expertise, track record in delivering classified space security programs, AI and automation capabilities, and the breadth of security solutions spanning space, ground, and communication link security layers.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' solution portfolios, security clearance capabilities, geographic presence, and key strategic developments. Some of the key players operating in the global satellite cybersecurity market include Airbus Defence and Space (France), Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.), Thales Group (France), Raytheon Technologies Corporation (U.S.), Boeing Company (U.S.), L3Harris Technologies Inc. (U.S.), Leonardo S.p.A. (Italy), Honeywell International Inc. (U.S.), Cisco Systems Inc. (U.S.), IBM Corporation (U.S.), Kratos Defense & Security Solutions Inc. (U.S.), Viasat Inc. (U.S.), SES S.A. (Luxembourg), and Eutelsat Communications S.A. (France), among others.

The global satellite cybersecurity market is expected to reach USD 18.6 billion by 2036 from an estimated USD 6.2 billion in 2026, at a CAGR of 11.6% during the forecast period 2026-2036.

In 2026, the network security segment is expected to hold the largest share of the global satellite cybersecurity market, reflecting network perimeter security's position as the foundational and most broadly deployed security layer across satellite infrastructure globally.

The data security segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by escalating regulatory and contractual requirements for encryption of satellite communications, demonstrated threats from state-sponsored intelligence collection against satellite links, and data protection compliance obligations for satellite networks carrying personal data.

In 2026, the GEO segment is expected to hold the largest share of the global satellite cybersecurity market, reflecting the large installed base of high-value GEO military and commercial satellites that have historically been the primary focus of satellite security investment.

In 2026, the military and defense segment is expected to hold the largest share of the global satellite cybersecurity market, driven by the strategic consequences of satellite cyberattacks on military communications and intelligence systems generating the highest per-program security investment of any application category.

The growth of this market is primarily driven by the demonstrated escalation of nation-state cyber offensive operations targeting satellite infrastructure, exemplified by the Viasat KA-SAT attack, compelling emergency and sustained security investment across government and commercial satellite operators globally, and the extraordinary expansion of LEO satellite constellations by SpaceX, Amazon, and others creating an unprecedented new attack surface at scale requiring purpose-built cybersecurity solutions.

Key players are Airbus Defence and Space (France), Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.), Thales Group (France), Raytheon Technologies Corporation (U.S.), Boeing Company (U.S.), L3Harris Technologies Inc. (U.S.), Leonardo S.p.A. (Italy), Honeywell International Inc. (U.S.), Cisco Systems Inc. (U.S.), IBM Corporation (U.S.), Kratos Defense & Security Solutions Inc. (U.S.), Viasat Inc. (U.S.), SES S.A. (Luxembourg), and Eutelsat Communications S.A. (France), among others.

Asia-Pacific is expected to register the highest growth rate in the global satellite cybersecurity market during the forecast period 2026-2036, driven by China's large military satellite program, India's expanding space sector, Japan and South Korea's growing defense satellite investments, and the rapid commercialization of satellite services across the region generating new security requirements.

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Apr-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates