Resources

About Us

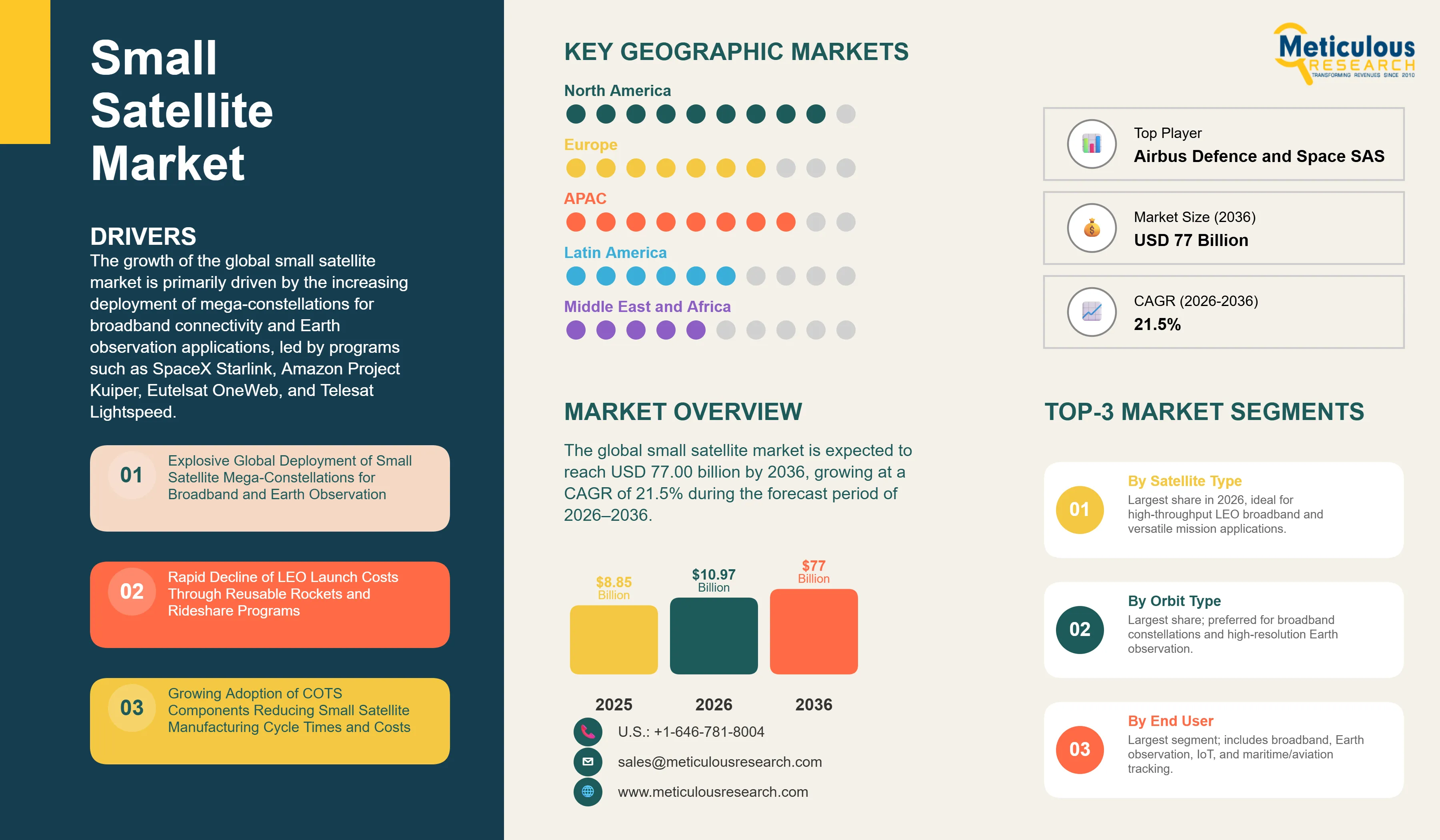

The global small satellite market was valued at USD 8.85 billion in 2025. This market is expected to reach USD 77.00 billion by 2036 from an estimated USD 10.97 billion in 2026, growing at a CAGR of 21.5% during the forecast period of 2026–2036.

The growth of the global small satellite market is primarily driven by the increasing deployment of mega-constellations for broadband connectivity and Earth observation applications, led by programs such as SpaceX Starlink, Amazon Project Kuiper, Eutelsat OneWeb, and Telesat Lightspeed. In addition, the significant reduction in launch costs enabled by reusable launch vehicle technologies and rideshare missions has made large-scale deployment of small satellites increasingly economically viable. The growing adoption of commercial off-the-shelf (COTS) components is further driving market growth by substantially reducing manufacturing cycle times and lowering per-unit production costs.

However, the relatively shorter operational lifespan of small satellites compared with conventional large satellites, typically 5–7 years versus more than 15 years, results in higher replacement and replenishment costs over the mission lifecycle. Furthermore, increasing congestion across low Earth orbit (LEO) orbital shells is elevating collision risks and adding to regulatory and space traffic management complexities. Supply chain constraints related to specialized components, mainly radiation-hardened electronics, advanced sensors, and propulsion hardware, also remain key restraints to market growth.

The increasing deployment of LEO-based infrastructure to complement 5G and next-generation communication networks, growing government and defense procurement of proliferated satellite architectures for resilient surveillance, intelligence, and secure communications, and the growing use of satellite-derived data across agriculture, maritime monitoring, logistics, and climate intelligence applications are expected to create significant growth opportunities for market players. Moreover, the continued miniaturization of satellite bus platforms, enabling compact and cost-efficient spacecraft to perform missions that previously required significantly larger satellites, is emerging as a major trend shaping the evolution of this market.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Mega-Constellation Manufacturing at Industrial Scale Transforming Satellite Production Economics

The deployment of satellite mega-constellations at industrial scale is transforming small satellite manufacturing from a project-based, artisanal industry into a high-volume, assembly-line manufacturing sector with economics more analogous to commercial aviation than traditional spacecraft production. SpaceX's Starlink manufacturing facility in Redmond, Washington, produces approximately 70+ satellites per week, a throughput that exceeds the total annual production of most national space agencies, using automotive-inspired production line techniques, COTS components, and aggressive supplier integration.

This manufacturing scale is significantly reducing per-unit satellite production costs, driving supply chain standardization, and fostering the emergence of a new class of small satellite component and subsystem suppliers capable of delivering thousands of units annually. In addition, the constellation manufacturing paradigm is enabling new business models, including satellite-as-a-service, data-as-a-service, and connectivity-as-a-service, which are attracting substantial venture capital and strategic investments across the global space ecosystem.

Proliferated Defense Satellite Architectures Driving Government Small Satellite Procurement

The growing adoption of proliferated low‑Earth orbit (LEO) satellite architectures by defense agencies is creating a substantial and rapidly growing government procurement market for small satellites. Under this architecture, surveillance, secure communications, and missile‑warning capabilities are distributed across dozens to hundreds of smaller satellites, rather than being concentrated in a limited number of large, high‑value, strategically vulnerable spacecraft.

A key example is the U.S. Space Development Agency’s (SDA) Proliferated Warfighter Space Architecture (PWSA), which includes the Transport Layer and Tracking Layer constellations designed to provide low‑latency military communications, resilient data relay, and missile warning and tracking capabilities. The SDA has already awarded contracts for more than 430 satellites across multiple tranches, with cumulative contract values reaching several billion dollars. Recent awards include multiple multi‑billion‑dollar multi‑vendor contracts for Tranche 3 Tracking Layer satellites supplied by primes such as Lockheed Martin Corporation, Northrop Grumman Corporation, L3Harris Technologies, Inc., and Rocket Lab USA, Inc., reflecting a shift toward large‑scale, tranche‑based small‑satellite procurement.

In addition, manufacturers such as York Space Systems LLC and Terran Orbital Corporation continue to benefit from recurring tranche‑based procurement programs for advanced tactical communications and missile‑defense applications. Beyond the U.S., defense agencies in the U.K., Australia, France, Japan, and other allied nations are increasingly pursuing similar proliferated‑architecture strategies to strengthen space resilience and reduce single‑point mission vulnerabilities. This trend is broadening the defense small‑satellite procurement market beyond its historical U.S.‑centric concentration and is expected to remain a major driver of market growth over the forecast period.

AI and Onboard Processing Enabling Autonomous Small Satellite Operations

The integration of artificial intelligence and onboard processing into small satellite platforms, enabling autonomous anomaly detection, intelligent downlink scheduling, on‑orbit image processing, and adaptive mission planning with minimal reliance on continuous ground‑station contact, is expanding the mission capability envelope of small satellites and creating new commercial opportunities for satellite‑derived intelligence products.

Planet Labs’ Pelican constellation, for example, embeds advanced onboard AI and edge‑processing capabilities to support functions such as automated cloud detection and tasking optimization, thereby maximizing the collection of scientifically useful imagery per orbit. These onboard processing capabilities are particularly valuable for high‑volume constellations where the ground segment cannot practically manage every satellite contact, enabling the constellation to operate with a high degree of autonomy and significantly reducing operational cost per satellite.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 77.00 Billion |

|

Market Size in 2026 |

USD 10.97 Billion |

|

Market Size in 2025 |

USD 8.85 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 21.5% |

|

Dominating Satellite Type |

Minisatellites |

|

Fastest Growing Satellite Type |

Nanosatellites/CubeSats |

|

Dominating Subsystem |

Payloads & Structures |

|

Fastest Growing Subsystem |

Propulsion Systems |

|

Dominating Orbit |

Low Earth Orbit (LEO) |

|

Dominating Application |

Communication |

|

Fastest Growing Application |

Earth Observation & Remote Sensing |

|

Dominating End User |

Commercial |

|

Fastest Growing End User |

Government & Defense |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

By Satellite Type: In 2026, the Minisatellites Segment to Dominate the Global Small Satellite Market

Based on satellite type, the global small satellite market is segmented into minisatellites (100–1,000 kg), microsatellites (10–100 kg), nanosatellites (1–10 kg), and CubeSats.

In 2026, the minisatellites segment is expected to account for the largest market share of the global small satellite market. The large share of this segment is attributed to the deployment of minisatellite-class platforms as the preferred configuration for high-throughput LEO broadband constellation nodes, where the higher mass envelope enables larger solar arrays for electric propulsion, more powerful communication payloads for high-capacity throughput, and longer operational lifespans that reduce replacement cadence costs.

Starlink V2 Mini satellites at approximately 800 kg, OneWeb satellites at approximately 150 kg, and Telesat Lightspeed microsatellite nodes weighing in the 700–750 kg range all fall within the small‑satellite class, with OneWeb squarely in the minisatellite range and Starlink V2 Mini and Telesat Lightspeed at the upper‑end of the small‑satellite or lower‑medium‑satellite mass band. This positioning reflects their role as high‑capacity, high‑throughput communication platforms, for which average per‑unit revenue is typically among the highest in the commercial satellite market.

However, the nanosatellites and CubeSats segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the rapid growth in CubeSat deployment volumes across commercial Earth observation, IoT connectivity, technology demonstration, and academic missions; the regulatory mandate for end-of-life deorbit capability expanding the propulsion-equipped CubeSat addressable market; and the proliferation of standardized 3U, 6U, and 12U CubeSat platforms that enable rapid, low-cost mission deployment for a growing global base of commercial and academic operators.

By Subsystem: In 2026, the Payloads & Structures Segment to Hold the Largest Share

Based on subsystem, the global small satellite market is segmented into payloads and structures, propulsion systems, power systems, communication subsystems, attitude determination and control systems, thermal control systems, and command and data handling.

In 2026, the payloads and structures segment is expected to account for the largest share of the global small satellite market. The large share of this segment is attributed to the dominant revenue contribution of mission-specific payload equipment, including imaging sensors, communication transponders, scientific instruments, and radar systems, that constitute the highest-value content per satellite and determine the commercial mission utility and revenue-generating capability of each deployment. Advances in miniaturized sensor technology, software-defined radio, and on-orbit processing have significantly improved payload performance per unit mass, enabling smaller satellites to perform missions previously requiring much larger platforms.

However, the propulsion systems segment is projected to register the highest CAGR during the forecast period. The strong growth of this segment is driven by the U.S. FCC’s five‑year deorbit rule and equivalent international regulations mandating propulsion capability across satellite classes that previously flew without it, the growing adoption of electric propulsion for low‑Earth orbit (LEO) constellation station‑keeping, and the increasing deployment of multi‑mode propulsion systems that combine chemical and electric technologies for mission‑specific optimization.

By Orbit Type: In 2026, Low Earth Orbit to Account for the Largest Share

Based on orbit type, the global small satellite market is segmented into low Earth orbit (LEO), medium Earth orbit (MEO), and geostationary Earth orbit (GEO). In 2026, the LEO segment is expected to account for the largest share of the global small satellite market, reflecting the dominant role of LEO mega‑constellation deployments for broadband connectivity, Earth observation, and defense surveillance, as the primary driver of small satellite manufacturing volume. LEO’s advantage in launch cost, low‑latency communication performance, and suitability for high‑revisit Earth observation makes it the optimal orbit class for the vast majority of small satellite applications.

By Application: In 2026, the Communication Segment to Hold the Largest Share

Based on application, the global small satellite market is segmented into communication, Earth observation and remote sensing, navigation, scientific research and technology demonstration, military intelligence and surveillance, IoT and M2M connectivity, and other applications. In 2026, the communication segment is expected to account for the largest share of the global small satellite market. This dominance reflects the huge procurement volumes generated by low Earth orbit (LEO) broadband constellation deployments—SpaceX Starlink, Amazon Kuiper, OneWeb/Eutelsat, and Telesat Lightspeed—each requiring hundreds to thousands of communication satellite platforms to achieve global coverage. The commercial segment is expected to record the highest CAGR in the satellite market, driven by rising demand for high‑speed internet in underserved regions and the development of large‑scale LEO satellite constellations.

However, the Earth observation and remote sensing segment is projected to register the highest CAGR during the forecast period. The rapid growth of this segment is driven by the expanding commercial Earth observation data market, with operators such as Planet Labs, ICEYE, Satellogic, BlackSky, and numerous specialized firms deploying increasingly capable imaging and synthetic aperture radar (SAR) constellations, and by growing government investment in enhanced Earth observation capability for climate monitoring, disaster management, agricultural surveillance, and military intelligence applications, which small satellites uniquely support through high revisit frequency and global coverage.

By End User: In 2026, the Commercial Segment to Hold the Largest Share

Based on end user, the global small satellite market is segmented into commercial, government and defense, and academic and research. In 2026, the commercial segment is expected to account for the largest share of the global small satellite market, reflecting the dominant role of private commercial operators as both the largest satellite deployers by volume and the primary drivers of small satellite manufacturing innovation. The commercial segment includes broadband connectivity operators, Earth observation data companies, IoT connectivity platform providers, maritime and aviation tracking services, and the broad ecosystem of data analytics companies that derive revenue from satellite‑collected information.

However, the government and defense segment is projected to register the highest CAGR during the forecast period. The rapid growth of this segment is driven by increasing national investment in proliferated low Earth orbit (LEO) satellite architectures for defense surveillance, strategic communications, and missile warning, with the U.S. Space Development Agency’s Transport Layer and Tracking Layer programs representing billions of dollars of committed small satellite procurement, and by growing investment in national commercial space programs across Europe, Japan, India, Australia, and the Middle East, creating sustained government demand that complements commercial constellation activity.

Based on geography, the global small satellite market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of around 40–45% of the global small satellite market, driven by the concentration of commercial small satellite operators such as SpaceX, Amazon, Rocket Lab, Planet Labs, Maxar, L3Harris, Northrop Grumman, and York Space Systems, along with hundreds of smaller firms, the most advanced small satellite manufacturing ecosystem globally, and the largest government and defense satellite procurement market through NASA, the U.S. Space Force, and the National Reconnaissance Office.

However, the Asia Pacific small satellite market is expected to grow at the fastest CAGR from 2026 to 2036. This growth is driven by China’s aggressive domestic small satellite constellation buildout, including the government‑backed Guowang 13,000‑satellite constellation and commercial constellations from GalaxySpace, Commsat, and LandSpace, India’s liberalized space policy enabling rapid private‑sector growth following the establishment of IN‑SPACe, Japan’s expanding commercial space program anchored by iQPS and Synspective, and South Korea’s growing national and commercial satellite deployment programs.

The global small satellite market is characterized by a diversified and evolving competitive landscape, including established aerospace and defense primes that develop small satellite platforms alongside large satellite programs, dedicated New‑Space manufacturers, vertically integrated operators offering spacecraft manufacturing and launch capabilities, as well as specialized subsystem, payload, and platform suppliers.

Space Exploration Technologies Corp. (SpaceX) remains one of the most influential companies in the global space market in terms of deployment scale and manufacturing throughput, driven by its Starlink constellation and a production rate of around 70 Starlink satellites per week at its Redmond factory, equivalent to more than 3,600 units per year. Rocket Lab USA, Inc. maintains a strong foothold across spacecraft manufacturing, launch services, and integrated space systems through its Electron launch vehicle and Photon satellite platform, which provides a standardized bus with power, propulsion, and communications subsystems for a range of low‑Earth orbit, lunar, and deep‑space missions. Surrey Satellite Technology Limited, widely recognized as a pioneer of the modern small‑satellite industry, continues to hold a robust presence across government, defense, and commercial missions, delivering turnkey small‑satellite platforms and subsystems for Earth‑observation, science, and communications applications, including a £40‑million contract with the UK Ministry of Defence for the Juno satellite program.

In addition, growing investments in low‑Earth orbit (LEO) constellations, sovereign space programs, defense‑led resilience initiatives, and Earth observation networks are driving competition among both established manufacturers and emerging platform providers. The market is also witnessing increased demand for modular satellite buses, rapid deployment capabilities, and application‑specific payload integration, further strengthening competition across the value chain.

The report provides a detailed competitive assessment of key players based on their product portfolios, regional presence, manufacturing capabilities, strategic developments, partnerships, contracts, and major growth initiatives undertaken over the last few years. Some of the key players operating in the global small satellite market include Space Exploration Technologies Corp. (U.S.), Airbus Defence and Space SAS (France), The Boeing Company (U.S.), Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.), Rocket Lab USA, Inc. (U.S.), Surrey Satellite Technology Limited (U.K.), Thales Alenia Space SAS (France/Italy), OHB SE (Germany), L3Harris Technologies, Inc. (U.S.), York Space Systems LLC (U.S.), China Aerospace Science and Technology Corporation (China), ICEYE Oy (Finland), and Terran Orbital Corporation (U.S.). Other notable manufacturers and platform providers include Maxar Technologies Inc., BlackSky Technology Inc., Spire Global, Inc., GomSpace Group AB, AAC Clyde Space AB, Blue Canyon Technologies, Inc., Kongsberg NanoAvionics, and LeoStella LLC., among others.

The global small satellite market is expected to reach USD 77.00 billion by 2036 from an estimated USD 10.97 billion in 2026, at a CAGR of 21.5% during the forecast period 2026–2036.

In 2026, the minisatellites segment is expected to hold the largest share of the global small satellite market, driven by their dominant role as the preferred platform for high-throughput LEO broadband constellation nodes.

The nanosatellites and CubeSats segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by explosive deployment volume growth, regulatory deorbit mandates, and proliferating commercial and academic applications.

In 2026, the payloads and structures segment is expected to hold the largest share of the global small satellite market.

In 2026, the communication segment is expected to hold the largest share of the global small satellite market.

The growth of this market is primarily driven by the increasing global deployment of small satellite mega-constellations for broadband connectivity and Earth observation, the rapid decline of launch costs through reusable rocket technology and rideshare programs, and the growing adoption of COTS components reducing manufacturing cycle times and costs.

Key players operating in the global small satellite market include Space Exploration Technologies Corp. (U.S.), Airbus Defence and Space SAS (France), The Boeing Company (U.S.), Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.), Rocket Lab USA, Inc. (U.S.), Surrey Satellite Technology Limited (U.K.), Thales Alenia Space SAS (France/Italy), OHB SE (Germany), L3Harris Technologies, Inc. (U.S.), York Space Systems LLC (U.S.), China Aerospace Science and Technology Corporation (China), ICEYE Oy (Finland), Terran Orbital Corporation (U.S.), MDA Space Ltd. (Canada), Blue Canyon Technologies, Inc. (U.S.), Kongsberg NanoAvionics (Lithuania), AAC Clyde Space AB (Sweden), and GomSpace Group AB (Denmark).

Asia Pacific is expected to register the highest growth rate in the global small satellite market during the forecast period 2026–2036.

1 Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2 Research Methodology

2.1 Research Approach

2.2 Data Collection and Validation

2.2.1 Secondary Research

2.2.2 Primary Research and Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Country and Region Level Analysis

2.3 Market Assessment

2.3.1 Market Size Estimation

2.3.2 Bottom Up Approach

2.3.3 Top Down Approach

2.3.4 Growth Forecast

2.4 Assumptions for the Study

3 Executive Summary

3.1 Market Overview

3.2 Market Analysis by Satellite Type

3.3 Market Analysis by Subsystem

3.4 Market Analysis by Orbit Type

3.5 Market Analysis by Application

3.6 Market Analysis by End User

3.7 Market Analysis by Geography

4 Market Dynamics

4.1 Overview

4.2 Drivers

4.2.1 Explosive Global Deployment of Small Satellite Mega-Constellations for Broadband and Earth Observation

4.2.2 Rapid Decline of LEO Launch Costs Through Reusable Rockets and Rideshare Programs

4.2.3 Growing Adoption of COTS Components Reducing Small Satellite Manufacturing Cycle Times and Costs

4.2.4 Accelerating Government and Defense Procurement of Proliferated Small Satellite Architectures

4.3 Restraints

4.3.1 Limited Operational Lifespan of Small Satellites Compared to Conventional Large Satellites

4.3.2 Increasing Congestion of LEO Orbital Shells Creating Collision Risk and Regulatory Complexity

4.4 Opportunities

4.4.1 5G Complementary LEO Connectivity Infrastructure Expanding Small Satellite Addressable Market

4.4.2 Expanding Commercial Applications of Small Satellite Data in Agriculture, Maritime, and Climate Monitoring

4.4.3 In-Orbit Servicing and Active Debris Removal Creating New Mission Categories for Advanced Small Satellites

4.5 Challenges

4.5.1 Supply Chain Constraints for Radiation-Hardened Electronics and Specialized Satellite Components

4.5.2 Radio Frequency Spectrum and Orbital Slot Congestion Complicating Constellation Licensing

4.6 Porter’s Five Forces Analysis

5 Small Satellite Market, by Platform Type

5.1 Overview

5.2 Minisatellites (100–1,000 kg)

5.3 Microsatellites (10–100 kg)

5.4 Nanosatellites (1–10 kg)

5.5 CubeSat Platforms

5.5.1 1U–3U

5.5.2 6U–12U

5.5.3 27U and Above

6 Small Satellite Market, by Subsystem

6.1 Overview

6.2 Payload Systems

6.3 Structural & Mechanical Systems

6.4 Satellite Bus / Platform Structure

6.5 Propulsion Systems

6.6 Power Systems (Solar Panels, Batteries & Power Management Units)

6.7 Communication & RF Subsystems

6.8 Attitude Determination and Control Systems (ADCS)

6.9 Thermal Management Systems

6.10 Command, Data Handling & On-board Computing

7 Small Satellite Market, by Orbit Type

7.1 Overview

7.2 Low Earth Orbit (LEO)

7.3 Medium Earth Orbit (MEO)

7.4 Geostationary Earth Orbit (GEO)

7.5 Highly Elliptical Orbit (HEO)

8 Small Satellite Market, by Application

8.1 Overview

8.2 Communication

8.3 Earth Observation & Remote Sensing

8.4 Navigation

8.5 Scientific Research & Technology Demonstration

8.6 Defense, Intelligence & Surveillance

8.7 IoT & M2M Connectivity

8.8 Other Applications

9 Small Satellite Market, by End User

9.1 Overview

9.2 Commercial

9.3 Government & Defense

9.4 Academic & Research

10 Small Satellite Market, by Geography

10.1 Overview

10.2 North America

10.2.1 U.S.

10.2.2 Canada

10.3 Europe

10.3.1 U.K.

10.3.2 France

10.3.3 Germany

10.3.4 Italy

10.3.5 Spain

10.3.6 Russia

10.3.7 Netherlands

10.3.8 Rest of Europe

10.4 Asia Pacific

10.4.1 China

10.4.2 India

10.4.3 Japan

10.4.4 South Korea

10.4.5 Australia

10.4.6 Singapore

10.4.7 New Zealand

10.4.8 Rest of Asia Pacific

10.5 Latin America

10.5.1 Brazil

10.5.2 Mexico

10.5.3 Argentina

10.5.4 Chile

10.5.5 Rest of Latin America

10.6 Middle East and Africa

10.6.1 Israel

10.6.2 UAE

10.6.3 Saudi Arabia

10.6.4 South Africa

10.6.5 Rest of Middle East and Africa

11 Competitive Landscape

11.1 Overview

11.2 Key Growth Strategies

11.3 Competitive Benchmarking

11.4 Competitive Dashboard

11.4.1 Industry Leaders

11.4.2 Market Differentiators

11.4.3 Vanguards

11.4.4 Emerging Companies

11.5 Market Share/Ranking Analysis (2025)

12 Company Profiles

12.1 Space Exploration Technologies Corp. (SpaceX)

12.2 Airbus Defence and Space SAS

12.3 The Boeing Company

12.4 Lockheed Martin Corporation

12.5 Northrop Grumman Corporation

12.6 Rocket Lab USA, Inc.

12.7 Surrey Satellite Technology Limited (SSTL)

12.8 Thales Alenia Space SAS

12.9 OHB SE

12.10 L3Harris Technologies, Inc.

12.11 York Space Systems LLC

12.12 China Aerospace Science and Technology Corporation (CASC)

12.13 ICEYE Oy

12.14 Terran Orbital Corporation

12.15 Maxar Space LLC

12.16 MDA Space Ltd.

12.17 Blue Canyon Technologies, Inc.

12.18 Kongsberg NanoAvionics UAB

12.19 AAC Clyde Space AB

12.20 GomSpace Group AB

12.21 Others

13 Appendix

13.1 Questionnaire

13.2 Available Customization Options

13.3 Related Reports

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Feb-2026

Subscribe to get the latest industry updates