Resources

About Us

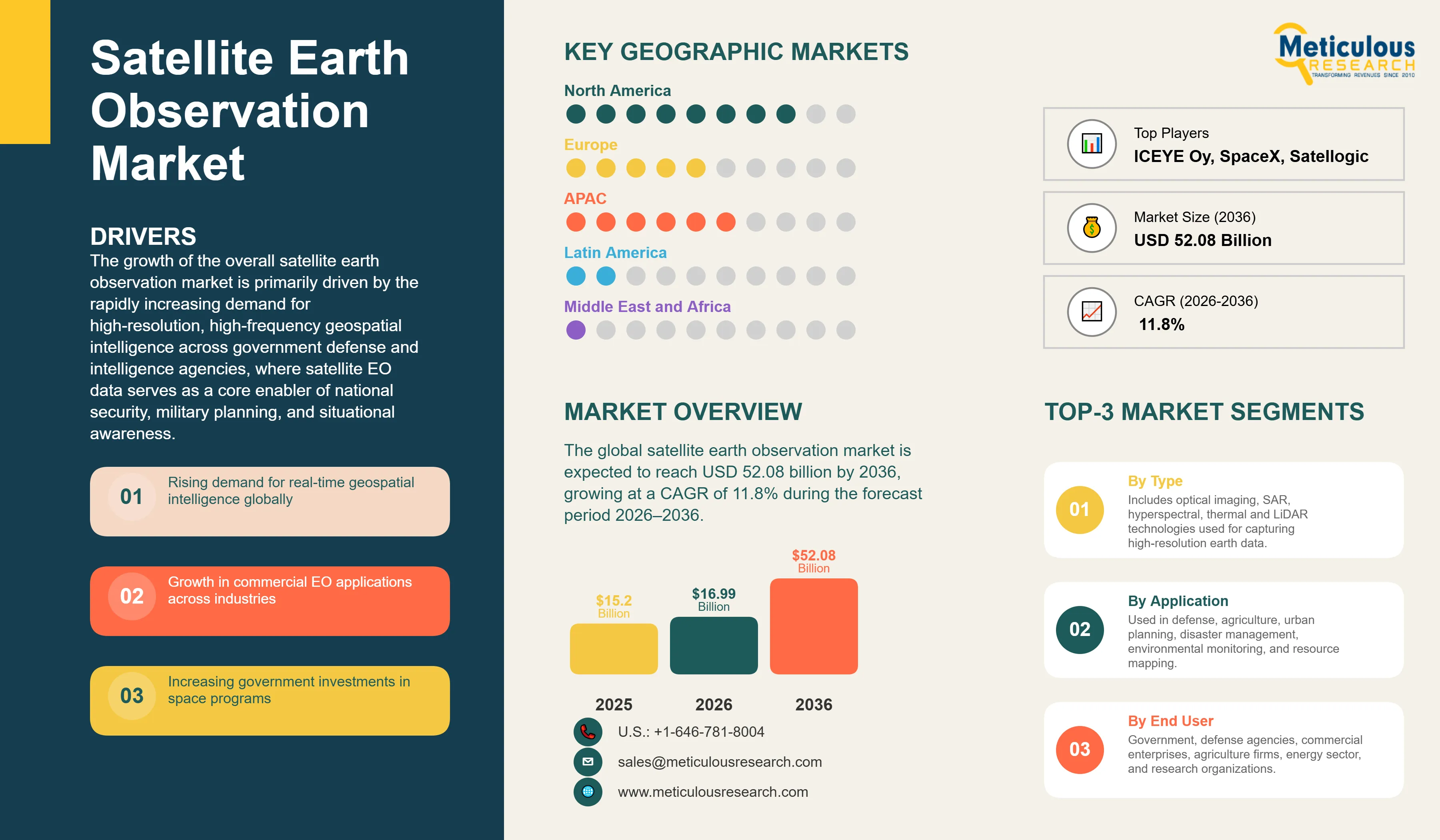

The global satellite earth observation market was valued at USD 15.20 billion in 2025. This market is expected to reach USD 52.08 billion by 2036 from an estimated USD 16.99 billion in 2026, growing at a CAGR of 11.8% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global satellite earth observation (EO) market comprises the integrated ecosystem of satellite systems, data products, and analytical services that enable continuous monitoring and analysis of the Earth’s surface, atmosphere, and oceans.

The market spans the full value chain, including satellite hardware (spacecraft, optical and radar payloads, and ground infrastructure), EO data products (panchromatic, multispectral, hyperspectral, SAR, and thermal infrared imagery), and value-added services such as geospatial analytics, AI-driven insights, and customized intelligence solutions delivered to government, defense, commercial, and research end users.

Key application areas include defense and intelligence, precision agriculture, urban planning, environmental monitoring, maritime surveillance, disaster management, energy and resource management, and ESG compliance.

The growth of the overall satellite earth observation market is primarily driven by the rapidly increasing demand for high-resolution, high-frequency geospatial intelligence across government defense and intelligence agencies, where satellite EO data serves as a core enabler of national security, military planning, and situational awareness. In parallel, growing commercial adoption across agriculture, insurance, energy, infrastructure, and logistics sectors, supported by declining cost per image from small satellite constellations and the proliferation of cloud-based data platforms, is significantly broadening market accessibility.

Additionally, the rising need for continuous global environmental monitoring, driven by climate change, biodiversity tracking, carbon accounting, and disaster management, is further driving demand for satellite-based observation capabilities.

However, the growth of this market is restrained by the high capital requirements associated with satellite development, launch, and ground infrastructure, along with increasing concerns around orbital congestion and space debris in low Earth orbit (LEO). Furthermore, the availability of free and open-access data from government programs such as NASA, ESA Copernicus, and ISRO limits pricing power for commercial providers in baseline imagery segments.

Key opportunities lie in the advancement of hyperspectral imaging technologies enabling detection of chemical and biological signatures for applications such as precision agriculture, environmental monitoring, and resource exploration; the growing integration of artificial intelligence and machine learning for automated analytics and real-time intelligence generation; and the rising demand for satellite-verified data to support ESG reporting and sustainability compliance.

Furthermore, the emergence of Very Low Earth Orbit (VLEO) constellations, enabling higher revisit frequency and near-continuous monitoring capabilities, is a major trend shaping the evolution of the global satellite earth observation market.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 52.08 Billion |

|

Market Size in 2026 |

USD 16.99 Billion |

|

Market Size in 2025 |

USD 15.20 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 11.8% |

|

Dominating Technology |

Optical Imaging |

|

Fastest Growing Technology |

Synthetic Aperture Radar (SAR) |

|

Dominating Orbit |

Low Earth Orbit (LEO) |

|

Fastest Growing Orbit |

Geostationary Earth Orbit (GEO) |

|

Dominating Payload Type |

Imaging (Optical / Multi-Spectral) |

|

Fastest Growing Payload Type |

EO/IR (Electro-Optical / Infrared) |

|

Dominating Application |

Infrastructure & Urban Planning |

|

Fastest Growing Application |

Disaster Management & Response |

|

Dominating End-Use |

Defense & Intelligence |

|

Fastest Growing End-Use |

Agriculture & Environmental Monitoring |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

AI-Driven Geospatial Intelligence Transforming Raw Imagery into Real-Time Decision Support

The integration of artificial intelligence (AI) and machine learning (ML) into satellite earth observation (EO) data pipelines is a key trend transforming the market from a raw imagery supply model to a high-value geospatial intelligence services ecosystem. Competitive differentiation is increasingly defined by the speed, accuracy, and actionability of AI-driven insights rather than satellite hardware capabilities alone.

Leading operators are embedding AI directly into their processing workflows to enable automated, large-scale analytics. Maxar Technologies, Inc. has integrated AI-enabled capabilities such as change detection, object classification, and damage assessment across its high-resolution imagery platforms, significantly reducing analysis time and enhancing operational decision-making. BlackSky Technology, Inc. is advancing AI-native architectures through its next-generation satellite systems designed for high-frequency monitoring and real-time analytics applications, including dynamic mapping and situational awareness.

In parallel, specialized analytics firms are driving this shift by developing application-specific AI platforms. Companies such as EOS Data Analytics are delivering advanced solutions for precision agriculture, combining satellite imagery with crop classification, yield prediction, and field-level monitoring. Emerging players, including Satellogic Inc., are exploring AI-driven data interaction models to simplify the use of high-resolution imagery and enable rapid application development across industries.

This evolution is enabling the emergence of subscription-based analytics models with higher customer stickiness and recurring revenue streams, gradually replacing transactional imagery sales.

As EO data becomes increasingly integrated into operational workflows across defense, agriculture, infrastructure monitoring, and supply chain intelligence, AI-driven geospatial insights are becoming central to value creation in the satellite earth observation market.

SAR Constellation Proliferation Enabling All-Weather Real-Time Monitoring

The rapid expansion of commercial Synthetic Aperture Radar (SAR) satellite constellations, capable of penetrating cloud cover, operating in complete darkness, and detecting surface deformation with high sensitivity, is significantly broadening the applicability of satellite earth observation beyond the limitations of optical, weather-dependent imaging systems. This capability is particularly critical for mission-critical applications requiring continuous monitoring, including maritime surveillance, disaster response, and infrastructure assessment.

Leading operators are scaling SAR constellations to deliver high-revisit, all-weather imaging. ICEYE Oy has expanded its constellation to enhance coverage for applications such as flood monitoring and maritime domain awareness, while Capella Space Corp. continues to strengthen its position in defense-focused intelligence through high-resolution SAR data and government partnerships. These developments indicate SAR’s growing importance in both commercial and defense segments.

SAR satellites are accounting for an increasing share of new EO satellite deployments, reflecting rising investments from both public and private stakeholders in radar-based imaging technologies. The ability to generate reliable, high-frequency data irrespective of atmospheric conditions is driving adoption across sectors where optical limitations previously constrained use cases.

Furthermore, the integration of SAR and optical data is emerging as a key value driver, combining the weather independence and structural sensitivity of SAR with the visual interpretability of optical imagery. This multi-sensor data fusion approach is enabling advanced analytics and premium applications, including flood risk modeling, infrastructure health monitoring, and precision agriculture, thereby enhancing the overall value proposition of satellite earth observation services.

Hyperspectral and Specialized Sensor Payloads Opening High-Margin New Vertical Markets

The commercialization of hyperspectral imaging satellites, capable of capturing hundreds of contiguous spectral bands compared to conventional multispectral systems, is enabling a new class of satellite EO applications based on precise chemical and material identification. This capability allows for surface fingerprinting of minerals, vegetation health, pollutants, and other environmental indicators, significantly reducing reliance on ground-based surveys and laboratory analysis.

Emerging players such as Pixxel Space Technologies Pvt. Ltd. are advancing high-resolution hyperspectral constellations targeting applications in mineral exploration, precision agriculture, environmental monitoring, and carbon assessment. These systems enable detection of subtle spectral variations, supporting use cases such as nutrient mapping, soil analysis, and pollution tracking with a level of granularity not achievable with traditional optical imaging.

In parallel, GHGSat Inc. is pioneering satellite-based greenhouse gas monitoring, offering high-resolution detection of methane and carbon dioxide emissions at the point-source level. This capability is increasingly critical for regulatory compliance, emissions accountability, and carbon market verification, particularly as ESG reporting requirements and climate disclosure frameworks continue to expand globally.

These specialized sensor payloads are enabling the development of high-value, application-specific verticals within the EO market. Compared to standard multispectral imagery, hyperspectral and emissions-monitoring data command premium pricing due to their unique analytical capabilities and direct applicability in revenue-generating use cases. As demand grows across industries such as mining, agriculture, and environmental compliance, hyperspectral and specialized EO solutions are expected to represent a rapidly expanding, high-margin segment of the global satellite earth observation market.

By Technology: In 2026, Optical Imaging to Dominate the Global Satellite EO Market

Based on technology, the global satellite earth observation market is segmented into optical imaging (multispectral, hyperspectral, panchromatic, and thermal infrared), synthetic aperture radar (SAR), and other technologies (LiDAR and passive microwave).

In 2026, the optical imaging segment is expected to account for the largest share of the market. The dominance of this segment is primarily attributed to the ability of optical satellites to deliver high-resolution, visually intuitive imagery that is easily interpretable by both human analysts and AI-based systems. Optical data, mainly RGB and multispectral imagery, integrates seamlessly with GIS platforms and analytics workflows, making it suitable for a wide range of applications, including urban planning, agriculture monitoring, infrastructure inspection, and disaster assessment. Leading operators such as Maxar Technologies, Inc. (WorldView Legion), Planet Labs PBC (SuperDove constellation), and Airbus Defence and Space (Pléiades Neo) continue to expand high-resolution optical imaging capabilities, supporting strong commercial and government demand.

Within optical imaging, the hyperspectral sub-segment is expected to register the fastest growth, driven by its ability to capture detailed spectral signatures for advanced applications such as mineral identification, precision agriculture, and environmental monitoring.

However, the SAR segment is projected to witness the highest growth during the forecast period. This growth is driven by SAR’s ability to capture imagery independent of weather conditions and lighting, making it critical for applications such as maritime surveillance, disaster monitoring, infrastructure assessment, and defense intelligence. Additionally, advanced techniques such as interferometric SAR (InSAR) enable detection of minute surface deformations, supporting use cases in infrastructure risk monitoring, geohazard detection, and resource management that cannot be effectively addressed through optical imaging alone.

By Orbit: In 2026, LEO to Hold the Largest Market Share

Based on orbit, the global satellite earth observation market is segmented into low Earth orbit (LEO: <600 km and 600–1,200 km), medium Earth orbit (MEO), and geostationary Earth orbit (GEO).

In 2026, LEO is expected to account for the largest market share, with the sub-600 km segment alone contributing a significant portion of total EO deployments. This dominance is driven by LEO satellites’ ability to deliver high spatial resolution, frequent revisit rates, and lower deployment costs, making them the preferred orbit for commercial earth observation missions. Satellites operating in the 300–600 km range can achieve sub-meter resolution with relatively small payloads, enabling cost-efficient constellation models.

The rapid expansion of commercial small satellite constellations, driven by the availability of cost-effective rideshare launch services from players such as SpaceX, has further accelerated LEO adoption across both commercial and government segments.

In contrast, MEO plays a relatively limited role in EO applications due to its trade-off between coverage and resolution, and is primarily utilized for navigation systems rather than high-resolution imaging.

However, the GEO segment is expected to register steady growth during the forecast period. GEO satellites provide continuous, fixed-area coverage, making them particularly suitable for applications such as weather monitoring, environmental observation, and persistent regional surveillance.

While GEO systems typically offer lower spatial resolution compared to LEO, ongoing advancements in sensor technologies are improving imaging capabilities, enhancing their relevance for applications where continuous temporal coverage is more critical than high spatial detail.

Overall, the market is expected to remain LEO-centric, with GEO complementing LEO constellations in applications requiring persistent monitoring and broad-area coverage.

By Application: In 2026, Infrastructure & Urban Planning to Hold the Largest Share

Based on application, the global satellite earth observation market is segmented into infrastructure & urban planning, disaster management, environmental monitoring, surveillance & security, precision agriculture, maritime monitoring, energy & natural resource management, and others.

In 2026, the infrastructure & urban planning segment is expected to account for the largest share of the overall satellite earth observation market. This dominance is driven by the increasing use of satellite imagery for urban expansion planning, transportation network development, smart city initiatives, and large-scale infrastructure monitoring.

The EO data is extensively utilized by governments and private stakeholders for construction progress tracking, asset monitoring, land-use mapping, and post-event infrastructure assessment. The integration of satellite data with GIS platforms, digital twins, and urban analytics systems is further enhancing its role in long-term planning and real-time decision-making across infrastructure projects.

However, the disaster management segment is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing frequency and severity of climate-related events, including floods, wildfires, hurricanes, and earthquakes, which are driving demand for real-time monitoring, early warning systems, and rapid damage assessment.

Satellite EO plays a critical role in disaster response by enabling large-area damage assessment, population displacement tracking, and coordination of emergency operations.

Additionally, the growing adoption of EO data in the insurance sector for catastrophe modeling, risk assessment, and claims verification is further strengthening demand in disaster-related applications.

North America is expected to account for the largest share of the global satellite earth observation market in 2026, driven by strong government-backed programs and a highly developed commercial ecosystem. The U.S. market is characterized by strong regional leadership driven by long-standing civil and defense initiatives led by agencies such as NASA, NOAA, USGS, and NGA, supporting continuous demand for EO data across environmental monitoring, weather forecasting, and geospatial intelligence applications.

In parallel, the presence of leading commercial players, such as Maxar Technologies, Inc., Planet Labs PBC, BlackSky Technology, Inc., Capella Space Corp., Spire Global, Inc., and Satellogic Inc., ensures strong commercial adoption across defense, intelligence, and enterprise applications. The ongoing procurement from defense and intelligence agencies, along with increasing integration of commercial EO data into government workflows, continues to drive the growth of the satellite earth observation market in the region.

The Asia-Pacific satellite earth observation market is poised to grow at the fastest CAGR during the forecast period, driven by expanding national space programs, increasing private sector participation, and rising demand for EO applications across agriculture, urban planning, and maritime monitoring. China leads regional growth through large-scale government-backed missions and the expansion of commercial constellations, while India is strengthening its capabilities through ISRO-led programs and growing private sector initiatives.

Japan and South Korea are advancing through established satellite programs and emerging SAR-focused companies, while Southeast Asian countries are increasingly adopting EO solutions for resource management and disaster monitoring. Overall, strategic focus on space sovereignty, combined with growing application demand and investments in next-generation satellite technologies, is driving the growth of the satellite earth observation market in Asia-Pacific.

The global satellite earth observation market is moderately consolidated at the imagery and data level, with the top players accounting for a significant share of total revenue, while a large number of emerging companies and specialized operators compete across niche applications such as hyperspectral imaging, SAR analytics, and climate monitoring. The market is characterized by a mix of vertically integrated operators (satellite + data + analytics) and downstream analytics-focused firms.

Maxar Technologies, Inc. holds a leading position in the commercial EO segment, driven by its high-resolution WorldView constellation (including WorldView Legion) and strong presence in defense, intelligence, and geospatial analytics. Planet Labs PBC operates one of the largest commercial satellite constellations, enabling high-frequency, subscription-based imagery that has significantly improved temporal resolution and accessibility of EO data.

ICEYE Oy and Capella Space Corp. are key players in the commercial SAR segment, offering all-weather, day-and-night imaging capabilities, particularly for defense and monitoring applications. Airbus Defence and Space remains a major European provider through its Pléiades Neo and SPOT satellite programs, serving both government and commercial customers.

BlackSky Technology, Inc., Spire Global, Inc., and Satellogic Inc. are expanding their presence through differentiated constellations and analytics platforms targeting near-real-time intelligence and industry-specific use cases. Emerging players such as Pixxel Space Technologies Pvt. Ltd. and GHGSat Inc. are focusing on high-growth niches, including hyperspectral imaging and greenhouse gas monitoring.

Upstream and integrated players such as L3Harris Technologies, Inc., Thales Alenia Space, Northrop Grumman Corporation, Leonardo S.p.A., and Surrey Satellite Technology Ltd. contribute through satellite manufacturing, payload development, and integrated EO systems. Additionally, SpaceX is increasingly relevant through its Starshield program and launch capabilities supporting EO constellation deployment.

The competitive landscape is further shaped by increasing investments in constellation expansion, vertical integration across data and analytics layers, and growing demand from defense, climate monitoring, and commercial intelligence applications.

Some of the key players operating in the global satellite earth observation market are Maxar Technologies, Inc., Planet Labs PBC, Airbus Defence and Space, ICEYE Oy, Capella Space Corp., BlackSky Technology, Inc., Spire Global, Inc., Satellogic Inc., L3Harris Technologies, Inc., Thales Alenia Space, Pixxel Space Technologies Pvt. Ltd., ImageSat International N.V., GHGSat Inc., Satrec Initiative Co., Ltd., Surrey Satellite Technology Ltd., SpaceX, Northrop Grumman Corporation, Orbital Insight, and Leonardo S.p.A..

The global satellite earth observation market was valued at USD 15.20 billion in 2025. This market is expected to reach USD 52.08 billion by 2036 from an estimated USD 16.99 billion in 2026, growing at a CAGR of 11.8% during the forecast period 2026–2036.

The global satellite earth observation market is expected to reach USD 52.08 billion by 2036 from an estimated USD 16.99 billion in 2026, at a CAGR of 11.8% during the forecast period 2026–2036.

In 2026, optical imaging is expected to hold the largest market share, driven by its broad application base and established integration with GIS workflows and analytics platforms globally.

SAR (Synthetic Aperture Radar) is expected to register the highest CAGR during the forecast period, driven by its all-weather, day-and-night imaging capability that is indispensable for maritime surveillance, flood monitoring, and defense intelligence applications.

LEO (Low Earth Orbit) is expected to hold the largest market share, with below 600 km LEO alone accounting for around 50-55% share in 2025, driven by small satellite constellation deployments that provide high resolution and frequent revisit at commercially viable cost points.

Disaster management is expected to register the highest CAGR during the forecast period, driven by increasing frequency of climate-related disasters creating surging demand for real-time satellite monitoring, early warning, and post-disaster damage assessment.

The growth is primarily driven by accelerating demand for geospatial intelligence across defense, commercial, and environmental applications; falling launch and satellite manufacturing costs enabling commercial constellation deployment at scale; and the integration of AI and ML with satellite data creating actionable real-time intelligence from automated image analysis.

Key players operating in the global satellite earth observation market include Maxar Technologies, Inc. (U.S.), Planet Labs PBC (U.S.), Airbus Defence and Space (France), ICEYE Oy (Finland), Capella Space Corp. (U.S.), BlackSky Technology, Inc. (U.S.), Spire Global, Inc. (U.S.), Satellogic Inc. (Argentina/U.S.), L3Harris Technologies, Inc. (U.S.), Thales Alenia Space (France/Italy), Pixxel Space Technologies Pvt. Ltd. (India), ImageSat International N.V. (Israel), GHGSat Inc. (Canada), Satrec Initiative Co., Ltd. (South Korea), Surrey Satellite Technology Ltd. (U.K.), SpaceX (U.S.), Northrop Grumman Corporation (U.S.), Orbital Insight (U.S.), and Leonardo S.p.A. (Italy).

Asia Pacific is expected to register the highest growth rate during the forecast period 2026–2036, driven by China's commercial EO expansion, India's growing satellite program and private EO consortium, Japan's commercial SAR development, and South Korea's Satrec Initiative.

1. Introduction

1.1 Market Definition and Scope

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

3.1 Market Overview

3.2 Market Analysis by Technology

3.3 Market Analysis by Component

3.4 Market Analysis by Orbit

3.5 Market Analysis by Payload Type

3.6 Market Analysis by Application

3.7 Market Analysis by End-Use

3.8 Market Analysis by Geography

4. Market Dynamics

4.1 Overview

4.2 Drivers

4.2.1 Growing Demand for High-Resolution, High-Frequency Geospatial Intelligence Across Government Defense and Commercial Applications

4.2.2 Falling Satellite Manufacturing and Launch Costs Enabling Commercial Small Satellite Constellation Deployment at Scale

4.2.3 Accelerating Climate Change-Driven Demand for Continuous Global Environmental Monitoring and Disaster Early Warning

4.2.4 ESG Reporting Mandates Requiring Satellite-Verified Environmental Metrics for Corporate Sustainability Compliance

4.3 Restraints

4.3.1 High Capital Investment Requirements for Satellite Constellation Development, Launch, and Ground Segment Infrastructure

4.3.2 Competition from Open-Source Government Satellite Programs Limiting Commercial Per-Scene Pricing Power

4.4 Opportunities

4.4.1 Hyperspectral Imaging Enabling High-Margin Precision Agriculture, Mineral Exploration, and Environmental Compliance Services

4.4.2 AI and ML Integration Creating Subscription-Based Geospatial Intelligence Revenue Models with Switching Costs

4.4.3 VLEO Constellation Deployment Enabling Sub-Daily Revisit Times for Near-Continuous Real-Time Monitoring Services

4.5 Challenges

4.5.1 Orbital Debris and Space Congestion Creating Collision Risk and Regulatory Complexity for New Constellation Deployments

4.5.2 Data Volume Management and Downlink Bandwidth Constraints for Processing Full-Constellation Daily Imagery at Scale

4.6 Porter’s Five Forces Analysis

5. Satellite EO Market, by Technology

5.1 Overview

5.2 Optical Imaging

5.2.1 Panchromatic

5.2.2 Multispectral

5.2.3 Hyperspectral

5.2.4 Thermal Infrared (TIR)

5.3 Synthetic Aperture Radar (SAR)

5.3.1 Stripmap SAR

5.3.2 ScanSAR

5.3.3 Spotlight SAR

5.3.4 Interferometric SAR (InSAR)

5.4 Other Technologies

5.4.1 LiDAR

5.4.2 Passive Microwave

6. Satellite EO Market, by Component

6.1 Overview

6.2 Hardware

6.2.1 Satellites (Bus & Payload)

6.2.2 Ground Stations & Terminals

6.2.3 Launch Vehicles

6.3 Software

6.3.1 Image Processing & Analytics Platforms

6.3.2 GIS & Mapping Platforms

6.3.3 AI/ML-Based Geospatial Intelligence

6.4 Data & Services

6.4.1 Raw Imagery Data (Tasked & Archive)

6.4.2 Value-Added Data Products (Mosaics, Change Detection, Analytics)

6.4.3 Managed EO Services

7. Satellite EO Market, by Orbit

7.1 Overview

7.2 Low Earth Orbit (LEO)

7.2.1 Very Low Earth Orbit (VLEO, < 400 km)

7.2.2 LEO 400–600 km

7.2.3 LEO 600–1,200 km

7.3 Medium Earth Orbit (MEO)

7.4 Geostationary Earth Orbit (GEO)

8. Satellite EO Market, by Payload Type

8.1 Overview

8.2 Imaging (Optical / Multispectral)

8.3 EO/IR (Electro-Optical / Infrared)

8.4 Communication

8.5 Navigation

9. Satellite EO Market, by Application

9.1 Overview

9.2 Infrastructure & Urban Planning

9.3 Disaster Management & Response

9.4 Environmental Monitoring

9.5 Surveillance & Security

9.6 Precision Agriculture

9.7 Maritime Monitoring

9.8 Energy & Natural Resource Management

9.9 Other Applications

10. Global Satellite EO Market, by End-Use

10.1 Overview

10.2 Government & Defense

10.2.1 Defense & Intelligence Agencies

10.2.2 Civil Government (Environmental, Agriculture, Infrastructure Ministries)

10.2.3 Emergency Management

10.3 Commercial

10.3.1 Insurance & Reinsurance

10.3.2 Agriculture & Food

10.3.3 Energy & Utilities

10.3.4 Real Estate & Construction

10.3.5 Logistics & Transportation

10.4 Research & Academic

11. Satellite EO Market, by Geography

11.1 Overview

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 U.K.

11.3.2 Germany

11.3.3 France

11.3.4 Italy

11.3.5 Spain

11.3.6 Finland

11.3.7 Luxembourg

11.3.8 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 India

11.4.3 Japan

11.4.4 South Korea

11.4.5 Singapore

11.4.6 Australia

11.4.7 Indonesia

11.4.8 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Argentina

11.5.3 Mexico

11.5.4 Chile

11.5.5 Rest of Latin America

11.6 Middle East & Africa

11.6.1 Saudi Arabia

11.6.2 UAE

11.6.3 Israel

11.6.4 South Africa

11.6.5 Rest of Middle East & Africa

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Share/Ranking Analysis (2025)

13. Company Profiles

13.1 Maxar Technologies, Inc.

13.2 Planet Labs PBC

13.3 Airbus Defence and Space

13.4 ICEYE Oy

13.5 Capella Space Corp.

13.6 BlackSky Technology, Inc.

13.7 Spire Global, Inc.

13.8 Satellogic Inc.

13.9 L3Harris Technologies, Inc.

13.10 Thales Alenia Space

13.11 Pixxel Space Technologies Pvt. Ltd.

13.12 ImageSat International N.V.

13.13 GHGSat Inc.

13.14 Satrec Initiative Co., Ltd.

13.15 Surrey Satellite Technology Ltd.

13.16 SpaceX

13.17 Northrop Grumman Corporation

13.18 Orbital Insight

13.19 Leonardo S.p.A.

13.20 Others

14. Appendix

14.1 Questionnaire

14.2 Available Customization Options

14.3 Related Reports

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Feb-2026

Subscribe to get the latest industry updates