Resources

About Us

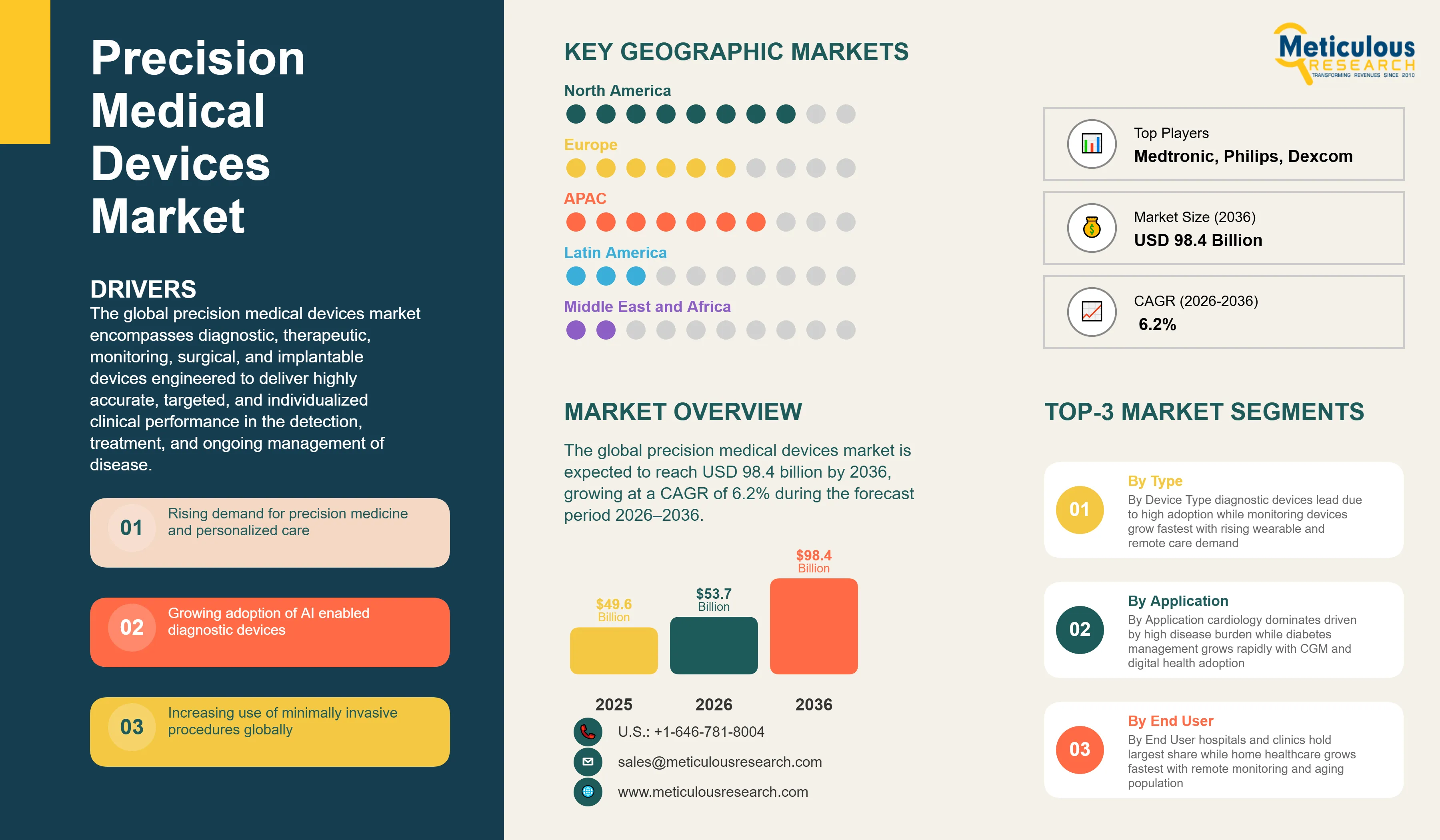

The global precision medical devices market was valued at USD 49.6 billion in 2025. This market is expected to reach USD 98.4 billion by 2036 from an estimated USD 53.7 billion in 2026, growing at a CAGR of 6.2% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global precision medical devices market encompasses diagnostic, therapeutic, monitoring, surgical, and implantable devices engineered to deliver highly accurate, targeted, and individualized clinical performance in the detection, treatment, and ongoing management of disease. Precision medical devices are distinguished from conventional medical equipment by their integration of advanced technologies—including artificial intelligence, robotics, next-generation imaging modalities, biosensors, and additive manufacturing—that enable clinical outcomes defined by sub-millimeter spatial accuracy, real-time physiological data acquisition, patient-specific device customization, and connectivity-enabled clinical decision support. The market serves clinical applications spanning cardiology, oncology, neurology, orthopedics, diabetes management, and respiratory care through end users including hospitals and major medical centers, ambulatory surgical centers, diagnostic laboratories, home healthcare settings, and research institutions.

The growth of the global precision medical devices market is primarily driven by the converging structural forces of the global precision medicine paradigm shift and the accelerating technology integration of artificial intelligence, robotics, and advanced sensors into clinical device platforms. The global adoption of precision medicine—which tailors clinical interventions to individual patient characteristics defined by genomic, proteomic, metabolomic, and physiological data—is fundamentally reshaping requirements for medical devices, demanding diagnostic systems capable of molecular-level disease characterization, monitoring devices providing continuous high-resolution physiological data streams, and therapeutic devices capable of delivering individualized treatment at anatomical precision levels previously unattainable. This clinical imperative is intersecting with technology capabilities—AI algorithms achieving clinical-grade diagnostic accuracy, robotic surgical systems providing sub-millimeter operative precision, and biosensors enabling continuous minimally invasive monitoring—to create a sustained investment wave in precision device development and commercialization.

Two transformative opportunities are defining the market's long-term trajectory. The rapid growth of wearable and remote patient monitoring devices, driven by the post-pandemic expansion of telehealth, the aging of the global population, and the proliferation of smartphone-connected health tracking platforms, is democratizing access to precision physiological monitoring beyond the hospital setting, creating a vast and rapidly expanding consumer and clinical home monitoring market. Simultaneously, the integration of artificial intelligence into diagnostic imaging, pathology, and clinical decision support is creating a new category of AI-enabled precision diagnostic devices that augment clinician accuracy, reduce diagnostic errors, and enable earlier disease detection at a scale and consistency that human interpretation alone cannot achieve, attracting major investment from both established medical device companies and AI-focused healthcare technology entrants.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 98.4 Billion |

|

Market Size in 2026 |

USD 53.7 Billion |

|

Market Size in 2025 |

USD 49.6 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 6.2% |

|

Dominating Device Type |

Diagnostic Devices |

|

Fastest Growing Device Type |

Monitoring Devices |

|

Dominating Technology |

Imaging Technologies |

|

Fastest Growing Technology |

Artificial Intelligence & Machine Learning |

|

Dominating Application |

Cardiology |

|

Fastest Growing Application |

Diabetes Management |

|

Dominating End User |

Hospitals & Clinics |

|

Fastest Growing End User |

Home Healthcare Settings |

|

Dominating Connectivity |

Standalone Devices |

|

Fastest Growing Connectivity |

Connected / IoT-Enabled Devices |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Expansion of AI-Enabled Diagnostic Devices

The integration of artificial intelligence and machine learning algorithms into diagnostic medical devices represents the most transformative technology trend currently reshaping the precision medical devices market, creating a new generation of diagnostic systems that learn from vast clinical datasets to deliver analytical accuracy, pattern recognition, and anomaly detection capabilities that systematically exceed conventional rule-based diagnostic software performance. AI-enabled diagnostic devices are advancing across medical imaging—where deep learning convolutional neural networks analyze CT, MRI, and X-ray images to identify malignant nodules, hemorrhagic strokes, and retinal pathologies with sensitivity and specificity approaching or exceeding subspecialist radiologist performance—pathology, where AI-powered digital slide analysis platforms enable automated cancer grading and biomarker quantification at a throughput and reproducibility unachievable through manual microscopy, and point-of-care diagnostics, where AI algorithms applied to biosensor data streams enable real-time sepsis risk scoring, arrhythmia classification, and hypoglycemia prediction.

The FDA had authorized over 950 AI/ML-enabled medical devices as of early 2025, with the authorization rate accelerating significantly year-over-year as device manufacturers mature their AI validation and regulatory submission processes and the FDA refines its guidance frameworks for AI/ML-based software as a medical device. Major precision medical device companies including Siemens Healthineers, GE HealthCare, Philips, and Roche Diagnostics are making AI the central differentiator of their next-generation diagnostic platform strategies, investing in AI algorithm development, clinical validation, and regulatory clearance pipelines that they expect to define competitive positioning in the diagnostic imaging and laboratory diagnostics markets through the forecast period. The convergence of AI with multimodal clinical data integration represents the advancing frontier of AI-enabled precision diagnostics that leading companies are developing toward commercial deployment.

Rise of Robotic Surgical Systems and Computer-Assisted Intervention

Robotic surgical systems have evolved from their origins as laparoscopic assistance platforms into a comprehensive ecosystem of precision intervention technologies spanning minimally invasive soft tissue surgery, orthopedic implant placement, endovascular intervention, and radiotherapy delivery, collectively representing one of the most capital-intensive and high-growth segments of the precision medical devices market. The da Vinci Surgical System from Intuitive Surgical has demonstrated across more than 10 million cumulative procedures the clinical value proposition of robotic assistance: tremor elimination, enhanced operative visualization through magnified 3D endoscopy, wristed instrument articulation exceeding the range of human wrist motion, and motion scaling enabling surgical maneuvers at precision levels that define new clinical standards for complex procedures including prostatectomy, hysterectomy, and thoracic surgery.

The robotic surgery market is broadening significantly beyond soft tissue laparoscopy into orthopedics, where systems from Stryker (MAKO), Zimmer Biomet (ROSA), and Smith+Nephew (CORI) provide intraoperative bone preparation guidance referenced to patient-specific preoperative CT-derived joint models, enabling total knee and hip replacement implant positioning accuracy within one to two degrees of planned alignment versus five to ten degrees for conventional jig-based techniques. Single-port robotic systems, magnetic-guided endoscopic platforms, and AI-integrated surgical planning tools represent the innovation frontier of robotic surgery that is attracting substantial R&D investment from both established platforms and new market entrants seeking to address the cost and access limitations of current-generation large-footprint robotic systems.

Growth of Continuous and Wearable Monitoring Devices

The transformation of patient physiological monitoring from episodic in-clinic measurement toward continuous, wearable, and home-based data acquisition represents a structural market evolution that is expanding the precision medical devices market beyond its traditional institutional boundaries into a large consumer and community health monitoring segment. Continuous glucose monitoring has become the definitive proof of concept for wearable precision monitoring at scale, with the global CGM market growing from a niche technology for intensive insulin-managed Type 1 diabetes patients toward broad adoption across Type 2 diabetes patients, pre-diabetic individuals, and performance health enthusiasts, driven by the compelling clinical evidence that continuous glucose visibility significantly improves glycemic control outcomes compared with fingerstick point-in-time measurement. Dexcom's G7 and Abbott's FreeStyle Libre platforms have demonstrated that factory-calibrated, smartphone-connected CGM devices can achieve clinical-grade accuracy at consumer-accessible price points with 14-day sensor wear durations, establishing a commercial template that device developers in cardiac, respiratory, and neurological monitoring are actively replicating.

Cardiac monitoring wearables including the Apple Watch's FDA-cleared ECG and irregular rhythm notification capabilities, the AliveCor KardiaMobile device, and ambulatory cardiac patch monitors from iRhythm (Zio) and Philips are establishing a continuous cardiac monitoring market that is capturing the large pool of undiagnosed atrial fibrillation and other arrhythmias that only manifest intermittently and therefore evade detection through conventional periodic Holter monitoring. The integration of SpO2 sensing, respiration rate monitoring, blood pressure estimation, and sleep quality tracking into multi-parameter wearable platforms is advancing toward the vision of a comprehensive continuous vital sign monitoring solution that can flag early deterioration signals before clinical manifestation, with particular value for post-acute care monitoring, chronic disease management, and elderly independent living support.

Growing Adoption of Precision Medicine and Personalized Healthcare

The global paradigm shift from population-averaged disease management toward precision medicine—which uses genomic sequencing, molecular biomarker profiling, and advanced diagnostics to characterize individual disease biology and select treatments optimized for each patient's specific disease subtype—is the foundational structural driver of the precision medical devices market, as the precision medicine model's clinical effectiveness depends fundamentally on devices capable of molecular-level diagnosis, biomarker-guided therapeutic monitoring, and personalized treatment delivery. The cost of whole-genome sequencing has declined from approximately USD 100 million per genome in 2001 to under USD 200 in 2025, enabling the clinical deployment of genomic diagnostics at population scale and driving demand for advanced molecular diagnostic platforms that can process genomic data into clinically actionable treatment guidance. Precision oncology has become the standard of care across multiple cancer types, generating large and growing demand for next-generation sequencing diagnostic platforms, liquid biopsy devices, and companion diagnostic systems from leading companies including Roche Diagnostics, Illumina, and Foundation Medicine.

Increasing Demand for Minimally Invasive Procedures

The sustained global shift in surgical preference from open procedures to minimally invasive approaches—driven by documented clinical benefits including reduced operative blood loss, shorter hospital stays, faster patient recovery, lower infection risk, and improved cosmetic outcomes—is a primary structural demand driver for the precision surgical and interventional device categories. Minimally invasive surgery requires advanced precision instrumentation, including articulating laparoscopic instruments, high-definition endoscopic visualization systems, and energy-based tissue management devices, that deliver operative capability through small access incisions, directly expanding the addressable market for precision surgical devices that enable clinicians to perform complex procedures through anatomically constrained access geometries. The growth of transcatheter cardiac intervention has demonstrated that catheter-based precision devices can address cardiac conditions previously requiring open chest surgery, generating large market opportunities for device developers with precision guidance, imaging, and deployment technologies enabling transcatheter procedural success.

Growth in Wearable and Remote Monitoring Devices

The expansion of wearable and remote patient monitoring into a mainstream clinical and consumer health management modality represents the largest near-term market expansion opportunity in the precision medical devices landscape. The addressable market for clinical remote monitoring extends across the estimated 537 million adults living with diabetes globally who could benefit from continuous glucose monitoring, the more than one billion individuals with hypertension requiring regular blood pressure monitoring, the estimated 37 million people with atrial fibrillation who could benefit from continuous cardiac rhythm monitoring, and the large populations with heart failure, COPD, and sleep apnea requiring ongoing physiological parameter tracking. Healthcare system economics strongly support the expansion of remote monitoring, as home-based continuous monitoring enables earlier intervention before costly acute hospitalization, reduces outpatient visit frequency, and supports value-based care models that reward proactive chronic disease management over reactive acute episode treatment.

Expansion of AI-Enabled Diagnostic Devices

The commercial opportunity created by integrating AI diagnostic algorithms into medical imaging, pathology, and point-of-care diagnostic devices is substantial and still in early stages of realization, as the majority of the global installed base of medical imaging systems and diagnostic laboratory analyzers operates with conventional software that lacks AI-augmented interpretation capabilities. The retrofit and upgrade market for AI software integration into existing imaging platforms and the new system replacement market for AI-native diagnostic devices collectively represent a multi-billion-dollar near-term commercial opportunity for established imaging companies and AI diagnostic software developers alike. In radiology, AI-powered triage algorithms that prioritize worklists by clinical urgency, flag critical findings for immediate clinician notification, and automate measurement and reporting workflows are generating demonstrable efficiency and accuracy improvements in radiology departments globally. The economic value of reducing diagnostic errors which provides a strong payer and health system justification for investment in AI diagnostic tools that independently verify and augment human interpretation.

By Device Type: In 2026, Diagnostic Devices to Dominate

Based on device type, the global precision medical devices market is segmented into diagnostic devices, therapeutic devices, monitoring devices, surgical and interventional devices, implantable devices, and other precision medical devices. In 2026, the diagnostic devices segment is expected to account for the largest share of the global precision medical devices market. The large share of this segment is attributed to the fundamental clinical primacy of accurate diagnosis as the prerequisite for all subsequent therapeutic decision-making, the broad commercial deployment of advanced diagnostic imaging systems across hospital radiology departments and diagnostic imaging centers globally, the rapid growth of molecular and genomic diagnostic platforms enabling precision oncology and infectious disease characterization, and the very high unit value of large-format diagnostic imaging systems that generates substantial market revenue from the global hospital imaging equipment replacement and upgrade cycle. Siemens Healthineers, GE HealthCare, Philips, and Canon Medical represent the leading competitive positions in the advanced diagnostic imaging market.

However, the monitoring devices segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the explosive commercial expansion of continuous glucose monitoring into mainstream diabetes care and prevention markets, the rapid growth of wearable cardiac monitoring platforms for atrial fibrillation detection and remote cardiac care, the expanding adoption of remote patient monitoring systems by health systems and insurers supporting post-acute care and chronic disease management programs, and the proliferation of consumer health monitoring wearables with FDA-cleared clinical measurement capabilities that are extending precision physiological monitoring to hundreds of millions of individuals outside the traditional medical device market.

By Technology: In 2026, Imaging Technologies to Hold the Largest Share

Based on technology, the global precision medical devices market is segmented into artificial intelligence and machine learning, robotics and automation, sensor and biosensor technologies, imaging technologies, and 3D printing and additive manufacturing. In 2026, the imaging technologies segment is expected to account for the largest share of the global precision medical devices market. Advanced medical imaging technology constitutes the largest installed base and highest revenue technology category within precision medical devices, serving as the clinical cornerstone of diagnosis, treatment planning, and therapeutic guidance across all major medical specialties. The continuous innovation cycle in imaging technology, including ultra-high-field 7T MRI, photon-counting CT, contrast-enhanced ultrasound, and spectral CT enabling material decomposition beyond conventional Hounsfield unit characterization, is driving sustained capital equipment replacement investment by healthcare institutions seeking to maintain diagnostic capability at the current clinical standard of care.

However, the artificial intelligence and machine learning segment is projected to register the highest CAGR during the forecast period. This growth is driven by the accelerating FDA authorization of AI/ML-enabled medical devices across diagnostic imaging, pathology, cardiology, and ophthalmology applications, the integration of AI diagnostic software as a standard feature of new diagnostic imaging platform releases by major manufacturers, the growing clinical evidence base demonstrating AI diagnostic accuracy improvements over conventional analysis across high-volume imaging indications including chest X-ray interpretation, diabetic retinopathy screening, and skin lesion classification, and the commercial deployment of AI-powered clinical decision support systems by major health systems seeking to improve diagnostic consistency and operational efficiency.

By Application: In 2026, Cardiology to Hold the Largest Share

Based on application, the global precision medical devices market is segmented into cardiology, oncology, neurology, orthopedics, diabetes management, respiratory care, and others. In 2026, the cardiology segment is expected to account for the largest share of the global precision medical devices market. Cardiology represents the broadest and most diverse application of precision medical devices across the full device type spectrum, encompassing precision diagnostic imaging including cardiac MRI and CT angiography, interventional devices including precision coronary stent delivery systems and transcatheter valve replacement platforms, implantable devices including high-resolution electrophysiology mapping systems, pacemakers, and implantable cardioverter defibrillators, and monitoring devices including wearable cardiac event monitors and implantable loop recorders. The global cardiovascular disease burden provides an immense clinical demand base for precision cardiac devices, and the innovation pipeline across transcatheter intervention, EP ablation, and remote cardiac monitoring is generating sustained new product-driven market growth.

However, the diabetes management segment is projected to register the highest CAGR during the forecast period. This growth is driven by the rapid global expansion of continuous glucose monitoring adoption accelerated by the strong health outcomes evidence supporting CGM over conventional fingerstick monitoring, the advancement of closed-loop automated insulin delivery systems combining CGM with algorithm-controlled insulin pumps into hybrid and fully closed artificial pancreas platforms, the expansion of CGM indications beyond Type 1 diabetes into Type 2 and pre-diabetes monitoring markets that vastly expand the addressable patient population, and the intensifying global diabetes burden projected to reach 783 million people by 2045 according to the International Diabetes Federation.

By End User: In 2026, Hospitals & Clinics to Hold the Largest Share

Based on end user, the global precision medical devices market is segmented into hospitals and clinics, ambulatory surgical centers, diagnostic laboratories, home healthcare settings, and research and academic institutes. In 2026, the hospitals and clinics segment is expected to account for the largest share of the global precision medical devices market. Hospitals and major medical centers represent the primary purchasing, deployment, and utilization environment for the highest-value precision medical device categories, including capital-intensive diagnostic imaging systems, robotic surgical platforms, advanced radiation therapy equipment, and complex interventional cardiology and neurology device suites, that collectively constitute the majority of global precision medical device market revenue. Large academic medical centers and tertiary referral hospitals are typically the first adopters of next-generation precision technologies, providing clinical validation environments that establish the evidence base supporting broader adoption across the hospital market, and their procurement decisions exert strong downstream influence on technology diffusion across the broader healthcare provider landscape.

However, the home healthcare settings segment is projected to register the highest CAGR during the forecast period. This growth is driven by the post-pandemic institutionalization of remote patient monitoring programs by health systems and insurers, the rapid consumer adoption of FDA-cleared wearable health monitoring devices enabling clinical-grade continuous monitoring outside the hospital, the aging global population's preference for home-based care and independent living support enabled by precision monitoring technology, and healthcare system economic incentives favoring lower-cost home monitoring over higher-cost inpatient monitoring for appropriate stable chronic disease patient populations.

By Connectivity: In 2026, Standalone Devices to Hold the Largest Share

Based on connectivity, the global precision medical devices market is segmented into standalone devices, connected and IoT-enabled devices, and cloud-integrated devices. In 2026, the standalone devices segment is expected to account for the largest share of the global precision medical devices market. The large installed base of standalone diagnostic imaging systems, laboratory analyzers, surgical instruments, and implantable devices that operate as self-contained clinical platforms without network connectivity or cloud data integration constitutes the majority of the global precision medical devices installed base by both unit count and revenue value, establishing standalone devices as the structurally dominant connectivity category in the near term. Many of the highest-value precision device categories are implemented as standalone network-isolated clinical systems in many healthcare environments due to cybersecurity concerns, regulatory requirements, and IT infrastructure limitations that constrain the connectivity expansion of existing capital equipment.

However, the connected and IoT-enabled devices segment is projected to register the highest CAGR during the forecast period. This growth is driven by the new product development strategies of all major precision medical device manufacturers increasingly prioritizing connectivity as a core platform feature, the clinical and operational value of real-time device data integration into electronic health record systems and clinical decision support platforms, the expansion of remote monitoring reimbursement by CMS and commercial payers creating economic incentives for healthcare providers to deploy connected monitoring devices, and the proliferation of consumer health IoT wearables that are establishing patient expectations for continuous connected health monitoring that are influencing clinical device adoption.

Precision Medical Devices Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global precision medical devices market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global precision medical devices market. The dominant position of North America in the global precision medical devices market reflects the confluence of the world's highest healthcare expenditure at approximately USD 4.5 trillion annually, the most advanced medical device regulatory and reimbursement ecosystem providing robust commercial pathways for innovative precision technologies, the concentration of the world's leading medical device innovation companies and most productive medical device R&D infrastructure, and the highest market penetration of advanced precision device categories including robotic surgical systems, AI-enabled diagnostic platforms, continuous glucose monitors, and implantable cardiac devices. The U.S. Medicare and Medicaid programs' adoption of reimbursement codes for new precision device categories including CGM, remote patient monitoring, and transcatheter cardiac interventions creates structured commercial markets that incentivize both adoption by healthcare providers and continued investment in precision device innovation by manufacturers. Canada contributes to regional growth through its universal healthcare system's investment in advanced diagnostic imaging and surgical technologies and its productive medical device research ecosystem centered around leading academic medical centers.

However, the Asia-Pacific precision medical devices market is expected to grow at the fastest CAGR during the forecast period. Asia-Pacific's rapid growth is driven by the massive healthcare infrastructure expansion underway across China, India, and Southeast Asia as these economies invest in elevating their healthcare system capabilities to meet the demands of rapidly aging populations and rising chronic disease burdens. China's healthcare reform programs have allocated hundreds of billions of renminbi to hospital construction, medical equipment procurement, and domestic medical device industry development, generating enormous demand for advanced diagnostic imaging, surgical, and monitoring devices while simultaneously supporting the growth of domestic precision device companies including Mindray, United Imaging Healthcare, and Neusoft Medical. Japan and South Korea contribute advanced precision device demand from their highly developed healthcare systems and contribute precision device innovation from their established technology industries, with companies including Canon Medical, Fujifilm Healthcare, and Samsung Medison offering competitive precision imaging platforms to global markets. The rapidly growing middle-income populations of India, Indonesia, Vietnam, and Thailand are driving healthcare investment that is progressively expanding access to precision medical devices beyond the major metropolitan hospital centers that have historically been the primary regional adoption points.

Europe maintains a large and sophisticated precision medical devices market anchored by the continent's advanced healthcare systems, the strong tradition of medical device innovation in Germany, Switzerland, the Netherlands, and Sweden, and the regulatory framework provided by the EU Medical Device Regulation that establishes high clinical evidence standards for device performance and safety. The EU MDR's stringent post-market clinical follow-up requirements are increasing the clinical evidence burden for precision medical devices marketed in Europe but are simultaneously strengthening the value proposition of clinically validated precision technologies that meet the regulation's evidence standards. Germany's hospital sector represents the largest European market for advanced surgical and diagnostic precision devices, and the Swiss medical technology cluster centered around companies including Straumann, Ypsomed, and Medartis contributes significant precision device innovation in dental, drug delivery, and orthopedic implant categories.

The global precision medical devices market is moderately consolidated at the major diagnostic imaging, robotic surgery, and implantable cardiac device segments, with Medtronic, Siemens Healthineers, GE HealthCare, Philips, Abbott, Boston Scientific, and Intuitive Surgical occupying dominant competitive positions in their respective precision device categories. Competition is focused on clinical performance differentiation at the device and platform level, AI and software capability integration, clinical evidence development supporting premium reimbursement positioning, service and connectivity ecosystem development, and geographic market access in high-growth emerging markets. The market is simultaneously experiencing increasing disruption from technology-native entrants—including AI diagnostic software companies, consumer electronics companies with FDA-cleared health monitoring capabilities, and digital health platforms integrating precision monitoring data into clinical care workflows—that are expanding competitive pressure on established device manufacturers from technology adjacencies.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' product portfolios, technology capabilities, clinical evidence bases, geographic market presence, and key strategic developments. Some of the key players operating in the global precision medical devices market include Medtronic plc (Ireland), Siemens Healthineers AG (Germany), GE HealthCare Technologies Inc. (U.S.), Philips Healthcare (Netherlands), Abbott Laboratories (U.S.), Boston Scientific Corporation (U.S.), Stryker Corporation (U.S.), Intuitive Surgical, Inc. (U.S.), Johnson & Johnson MedTech (U.S.), Becton, Dickinson and Company (U.S.), Roche Diagnostics (Switzerland), Dexcom, Inc. (U.S.), Zimmer Biomet Holdings (U.S.), ResMed Inc. (U.S.), and Masimo Corporation (U.S.), among others.

The global precision medical devices market is expected to reach USD 98.4 billion by 2036 from an estimated USD 53.7 billion in 2026, at a CAGR of 6.2% during the forecast period 2026–2036.

In 2026, the diagnostic devices segment is expected to hold the largest share of the global precision medical devices market, driven by the broad clinical deployment of advanced imaging systems, the rapid growth of molecular and genomic diagnostic platforms, and the fundamental clinical requirement for precise diagnosis as the prerequisite for all subsequent therapeutic decision-making.

The monitoring devices segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the explosive commercial expansion of continuous glucose monitoring, the rapid growth of wearable cardiac monitoring platforms, and the broad adoption of remote patient monitoring systems by health systems and insurers supporting chronic disease management and post-acute care programs.

In 2026, the imaging technologies segment is expected to hold the largest share of the global precision medical devices market, reflecting the large installed base and high unit value of advanced medical imaging systems—including AI-enhanced MRI, multi-slice CT, and high-frequency ultrasound—that constitute the clinical backbone of diagnosis and treatment planning across all major medical specialties.

In 2026, the cardiology segment is expected to hold the largest share of the global precision medical devices market, driven by the broad application of precision devices across cardiac diagnosis, intervention, implantation, and monitoring, supported by the immense global cardiovascular disease burden affecting an estimated 520 million people worldwide.

The growth of this market is primarily driven by the global adoption of precision medicine demanding device-level accuracy for molecular diagnosis, biomarker monitoring, and individualized treatment delivery; the increasing preference for minimally invasive procedures requiring advanced precision surgical instrumentation; accelerating technology integration of AI, robotics, and biosensors into clinical device platforms; and the rising global burden of chronic diseases including cardiovascular conditions, diabetes, cancer, and neurological disorders generating large and sustained precision device demand.

Key players are Medtronic plc (Ireland), Siemens Healthineers AG (Germany), GE HealthCare Technologies Inc. (U.S.), Philips Healthcare (Netherlands), Abbott Laboratories (U.S.), Boston Scientific Corporation (U.S.), Stryker Corporation (U.S.), Intuitive Surgical, Inc. (U.S.), Johnson & Johnson MedTech (U.S.), Becton, Dickinson and Company (U.S.), Roche Diagnostics (Switzerland), Dexcom, Inc. (U.S.), Zimmer Biomet Holdings (U.S.), ResMed Inc. (U.S.), and Masimo Corporation (U.S.), among others.

Asia-Pacific is expected to register the highest growth rate in the global precision medical devices market during the forecast period 2026–2036, driven by large-scale healthcare infrastructure investment across China, India, Japan, South Korea, and Southeast Asia, rapidly rising chronic disease burdens generating precision device demand, and the growth of domestic medical device manufacturing capabilities across the region.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Growing Adoption of Precision Medicine and Personalized Healthcare

4.2.1.2 Increasing Demand for Minimally Invasive Procedures

4.2.1.3 Advancements in Imaging, Robotics, and Sensor Technologies

4.2.1.4 Rising Prevalence of Chronic Diseases

4.2.2 Restraints

4.2.2.1 High Cost of Advanced Precision Devices

4.2.2.2 Complex Regulatory Approval Processes

4.2.2.3 Integration Challenges with Healthcare IT Systems

4.2.3 Opportunities

4.2.3.1 Growth in Wearable and Remote Monitoring Devices

4.2.3.2 Expansion of AI-Enabled Diagnostic Devices

4.2.3.3 Increasing Adoption in Emerging Markets

4.2.3.4 Development of Personalized Implantable Devices

4.2.4 Challenges

4.2.4.1 Data Accuracy and Interoperability Issues

4.2.4.2 Cybersecurity Risks in Connected Devices

4.3 Technology Landscape

4.3.1 AI and Machine Learning in Medical Devices

4.3.2 Robotics and Computer-Assisted Surgery

4.3.3 Advanced Imaging Technologies

4.3.4 Biosensors and Wearable Technologies

4.3.5 3D Printing and Personalized Implants

4.5 Value Chain Analysis

4.5.1 Component Suppliers (Sensors, Chips, Materials)

4.5.2 Device Manufacturers

4.5.3 Software & AI Platform Providers

4.5.4 Healthcare Providers

4.5.5 Patients & End Users

4.6 Regulatory and Standards Landscape

4.6.1 FDA Medical Device Regulations

4.6.2 EU MDR and CE Marking

4.6.3 ISO Standards (ISO 13485, IEC 60601)

4.6.4 Data Privacy Regulations (HIPAA, GDPR)

4.7 Porter's Five Forces Analysis

5. Precision Medical Devices Market, by Device Type (Primary Segmentation)

5.1 Introduction

5.2 Diagnostic Devices

5.2.1 Imaging Systems (MRI, CT, Ultrasound)

5.2.2 Molecular & Genomic Diagnostic Devices

5.2.3 Point-of-Care Diagnostic Devices

5.3 Therapeutic Devices

5.3.1 Laser-Based Treatment Devices

5.3.2 Radiation Therapy Devices

5.3.3 Drug Delivery Systems

5.4 Monitoring Devices

5.4.1 Continuous Glucose Monitors (CGM)

5.4.2 Cardiac Monitoring Devices

5.4.3 Remote Patient Monitoring Systems

5.4.4 Wearable Health Devices

5.5 Surgical & Interventional Devices

5.5.1 Robotic Surgical Systems

5.5.2 Image-Guided Surgical Devices

5.5.3 Minimally Invasive Surgical Instruments

5.6 Implantable Devices

5.6.1 Cardiac Implants (Pacemakers, ICDs)

5.6.2 Orthopedic Implants

5.6.3 Neurostimulation Devices

5.6.4 Personalized/3D-Printed Implants

5.7 Other Precision Medical Devices

6. Precision Medical Devices Market, by Technology

6.1 Introduction

6.2 Artificial Intelligence & Machine Learning

6.3 Robotics & Automation

6.4 Sensor & Biosensor Technologies

6.5 Imaging Technologies

6.6 3D Printing & Additive Manufacturing

7. Precision Medical Devices Market, by Application

7.1 Introduction

7.2 Cardiology

7.3 Oncology

7.4 Neurology

7.5 Orthopedics

7.6 Diabetes Management

7.7 Respiratory Care

7.8 Others

8. Precision Medical Devices Market, by End User

8.1 Introduction

8.2 Hospitals & Clinics

8.3 Ambulatory Surgical Centers

8.4 Diagnostic Laboratories

8.5 Home Healthcare Settings

8.6 Research & Academic Institutes

9. Precision Medical Devices Market, by Precision Level (Advanced Segmentation)

9.1 Introduction

9.2 Standard Precision Devices

9.3 High-Precision Devices

9.4 Ultra-Precision / Personalized Devices

10. Precision Medical Devices Market, by Connectivity

10.1 Introduction

10.2 Standalone Devices

10.3 Connected / IoT-Enabled Devices

10.4 Cloud-Integrated Devices

11. Precision Medical Devices Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Italy

11.3.5 Spain

11.3.6 Netherlands

11.3.7 Sweden

11.3.8 Switzerland

11.3.9 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 Japan

11.4.3 India

11.4.4 South Korea

11.4.5 Australia

11.4.6 Singapore

11.4.7 Thailand

11.4.8 Malaysia

11.4.9 Indonesia

11.4.10 Vietnam

11.4.11 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Chile

11.5.5 Colombia

11.5.6 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Turkey

11.6.5 Israel

11.6.6 Rest of Middle East & Africa

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Medtronic plc

13.2 Siemens Healthineers AG

13.3 GE HealthCare Technologies Inc.

13.4 Philips Healthcare

13.5 Abbott Laboratories

13.6 Boston Scientific Corporation

13.7 Stryker Corporation

13.8 Intuitive Surgical, Inc.

13.9 Johnson & Johnson (MedTech)

13.10 Becton, Dickinson and Company (BD)

13.11 Roche Diagnostics

13.12 Dexcom, Inc.

13.13 Zimmer Biomet Holdings

13.14 ResMed Inc.

13.15 Masimo Corporation

14. Appendix

14.1 Additional Customization

14.2 Related Reports

Published Date: Jul-2026

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Feb-2026

Published Date: Feb-2026

Subscribe to get the latest industry updates