Resources

About Us

Research Antibodies and Reagents Market by Product (Antibodies, Reagents), Technology (ELISA, Flow Cytometry, Immunofluorescence, Western Blot, Immunohistochemistry, Immunoprecipitation, Multiplex Immunosorbent Assay), Application, End User, and Geography — Global Opportunity Analysis and Industry Forecast (2024–2031)

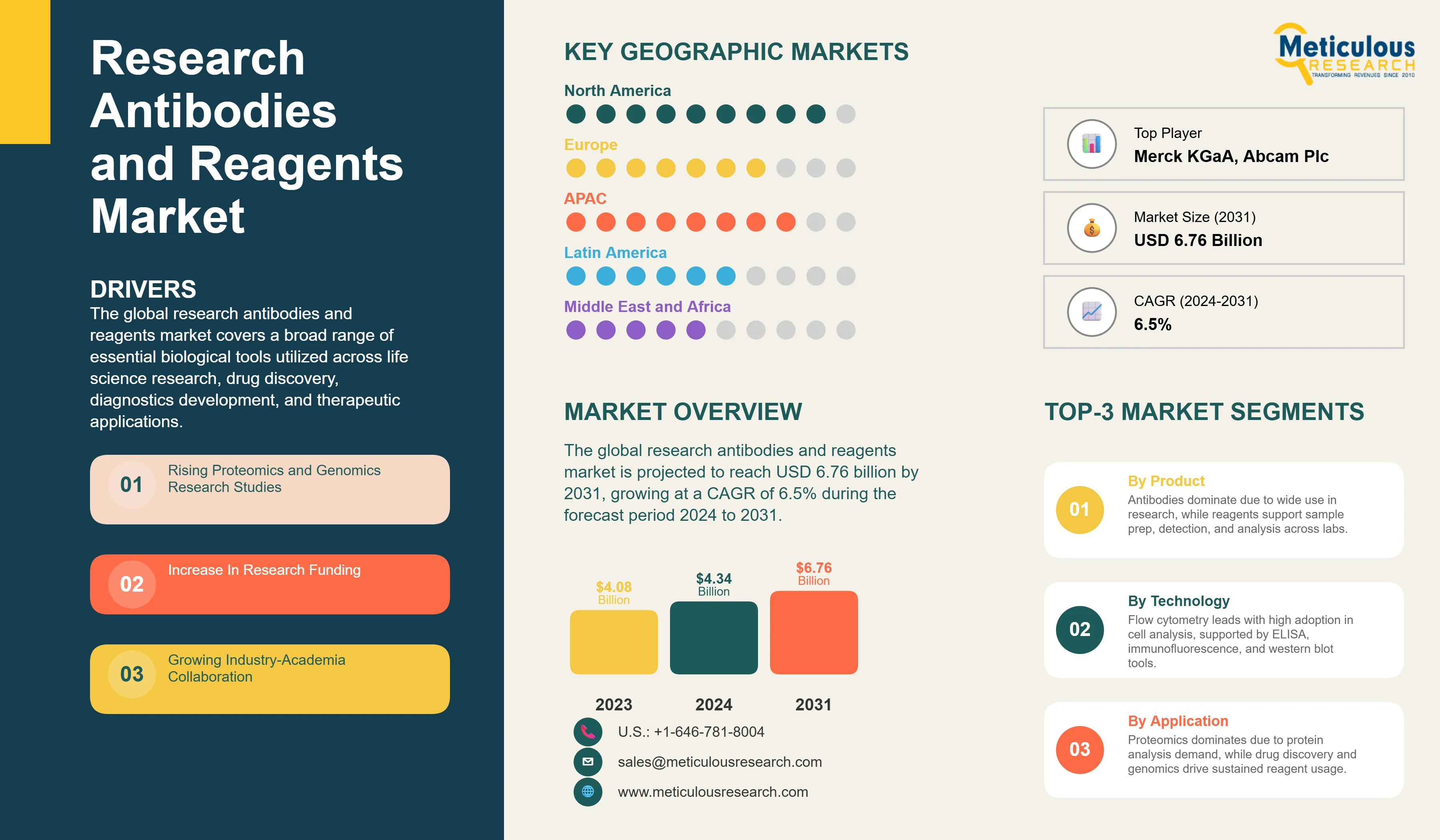

Report ID: MRHC - 104356 Pages: 285 Apr-2026 Formats*: PDF Category: Healthcare Delivery: 2 to 4 Hours Download Free Sample ReportThe global research antibodies and reagents market was valued at USD 4.34 billion in 2024 and is projected to reach USD 6.76 billion by 2031, growing at a CAGR of 6.5% during the forecast period 2024 to 2031.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global research antibodies and reagents market covers a broad range of essential biological tools utilized across life science research, drug discovery, diagnostics development, and therapeutic applications. The product portfolio includes primary and secondary antibodies, monoclonal antibodies, polyclonal antibodies, recombinant antibodies, immunoassay reagents, western blotting reagents, flow cytometry reagents, immunohistochemistry reagents, and other specialized biochemical compounds that allow researchers to detect, quantify, and analyze specific proteins, antigens, and biological molecules.

Research antibodies serve as foundational components across a variety of established laboratory techniques including enzyme linked immunosorbent assay, immunofluorescence, immunoprecipitation, and protein purification, and they continue to support fundamental research across genomics, proteomics, cell biology, immunology, and neuroscience. The market spans applications ranging from basic research and translational medicine to biomarker discovery, target validation, and the development of novel diagnostics and therapeutics, collectively making these biological tools indispensable to advancing both scientific knowledge and medical innovation.

The growth of the overall market for research antibodies and reagents is primarily driven by the rapid expansion of proteomics and genomics research, supported by technological advancements such as next generation sequencing and high throughput analytical techniques. These developments have significantly increased the demand for highly specific and reliable antibodies across applications such as biomarker discovery, drug development, and precision medicine. Rising global R&D funding from government bodies as well as pharmaceutical and biotechnology companies has further strengthened research infrastructure and accelerated innovation across this sector.

Increasing industry academia collaborations are also enhancing access to advanced technologies, novel drug targets, and specialized expertise, while improving the commercialization of research outcomes. Additionally, the growing pipeline of biopharmaceuticals, including complex antibody based therapeutics, is increasing the consumption of research reagents across all stages of drug discovery and development.

However, market growth is partially constrained by the high cost and long development timelines associated with antibody discovery and validation, along with persistent challenges related to the quality, reproducibility, and stability of research antibodies. On the other hand, expanding applications of antibodies in clinical research, biomarker identification, and personalized medicine particularly in oncology, immunology, and cell and gene therapy are creating substantial growth opportunities for market participants.

Major trends shaping this industry include the ongoing shift toward recombinant antibodies, the emergence of multiomics workflows, and the adoption of artificial intelligence driven antibody discovery platforms. These trends are expected to improve research efficiency, enhance reliability, and sustain long term growth within the global research antibodies and reagents market.

Shift Toward Recombinant Antibodies Improving Reproducibility and Standardization Across Research Settings

One of the most significant transitions shaping the research antibodies and reagents market is the progressive shift from conventional polyclonal and animal derived monoclonal antibodies toward recombinant antibodies. Recombinant antibodies are prepared using defined genetic sequences, which ensures batch to batch consistency and eliminates the variability that has historically been a major challenge in research reproducibility. This transition is gaining momentum across pharmaceutical companies, contract research organizations, and academic institutes that require high specificity and reliable performance across repeated experimental cycles.

The increasing publication of studies highlighting the reproducibility crisis in life sciences research has further accelerated the adoption of recombinant antibody formats, as research institutions and funding bodies are placing greater emphasis on validated and standardized reagent use. Leading market participants are responding by expanding their recombinant antibody portfolios and investing in platform technologies that enable faster and more scalable production of these products.

This trend is expected to reshape the competitive landscape of the global research antibodies and reagents market over the coming years, with recombinant formats progressively capturing a larger share of both primary and secondary antibody applications.

Artificial Intelligence Driven Antibody Discovery Accelerating Development Timelines and Expanding Target Space

The integration of artificial intelligence and machine learning into antibody discovery workflows is emerging as a transformative trend with the potential to significantly compress development timelines, reduce costs, and expand the range of druggable and researchable protein targets. AI based computational platforms are being applied to predict antibody binding affinities, optimize sequence designs, and identify novel epitopes that would be difficult to target through conventional immunization based approaches.

Pharmaceutical and biotechnology companies are increasingly partnering with AI focused biotechnology firms to integrate these capabilities into their antibody discovery pipelines, creating synergies between computational biology and experimental validation workflows. This convergence is also driving demand for highly specialized research reagents that support the wet laboratory validation of computationally generated antibody candidates, creating downstream opportunities across multiple product segments within the research antibodies and reagents market.

The long term impact of AI integration is expected to extend beyond discovery efficiency, influencing how antibodies are characterized, validated, and deployed in both research and translational medicine contexts.

Multiomics Workflows Driving Demand for Multiplexed and High Parameter Antibody Based Reagents

The growing adoption of multiomics approaches that combine proteomic, genomic, transcriptomic, and metabolomic data is creating new demand for antibody based reagents capable of simultaneously measuring large numbers of analytes from limited biological samples. Technologies such as high parameter spectral flow cytometry, mass cytometry, and multiplexed immunohistochemistry are enabling researchers to generate far richer biological datasets from individual experiments, fundamentally changing how antibodies and associated reagents are used in both discovery and translational research.

This trend is particularly impactful in oncology, immunology, and cell and gene therapy research, where understanding complex biological interactions across multiple molecular layers is essential for advancing therapeutic development. The demand for validated antibody panels, specialized buffers, staining reagents, and detection chemistries compatible with multiplexed workflows is rising substantially, providing a strong commercial growth vector for suppliers operating across the research antibodies and reagents value chain.

|

Parameters |

Details |

|

Market Size by 2031 |

USD 6.76 Billion |

|

Market Size in 2024 |

USD 4.34 Billion |

|

Revenue Growth Rate (2024 to 2031) |

CAGR of 6.5% |

|

Dominating Product |

Antibodies |

|

Fastest Growing Technology |

Flow Cytometry |

|

Dominating Technology |

Flow Cytometry |

|

Dominating Application |

Proteomics |

|

Dominating End User |

Pharmaceutical & Biotechnology Companies |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2024 |

|

Forecast Period |

2024 to 2031 |

By Product: In 2024, the Antibodies Segment to Dominate the Global Research Antibodies and Reagents Market

Based on product, the global research antibodies and reagents market is segmented into antibodies and reagents. The antibodies segment is further sub-segmented by type into primary antibodies and secondary antibodies; by production into monoclonal antibodies, polyclonal antibodies, and recombinant antibodies; by source into mouse, rabbit, and other sources; and by research area into oncology, infectious diseases, cardiology, immunology, neurology, stem cell research, and other research areas.

In 2024, the antibodies segment accounted for the largest share of the global research antibodies and reagents market. The large share of this segment reflects the growing application of antibodies in medicine and biomedical research for the purposes of diagnosis, drug development, and disease treatment. The increasing volume of proteomics and genomics based research programs, rising R&D funding across the public and private sectors, and the growing need for disease specific biomarkers are collectively expanding the utilization of research antibodies across a broad range of experimental platforms.

The reagents segment, which includes sample preparation reagents such as media and serum, stains and dyes, probes, buffers, and solvents, as well as antibody production reagents including enzymes and proteins, continues to serve as a critical enabling category across virtually all research antibody workflows. Growing laboratory throughput requirements and the expansion of multiomics workflows are expected to support consistent demand growth within the reagents segment throughout the forecast period.

By Technology: In 2024, the Flow Cytometry Segment to Hold the Largest Share

Based on technology, the global research antibodies and reagents market is segmented into flow cytometry, immunofluorescence, enzyme linked immunosorbent assay, multiplex immunosorbent assay, western blot, immunohistochemistry, immunoprecipitation, and other technologies.

In 2024, the flow cytometry segment accounted for the largest share of the global research antibodies and reagents market. The largest share of this segment is primarily attributed to increasing research activities in proteomics and cell based research conducted by universities and by pharmaceutical and biotechnology companies. The availability of a wide range of antibody specific fluorescent tags and the rapid adoption of high parameter spectral flow cytometry platforms are further contributing to the expansion of this segment. As more research institutions invest in next generation cytometry instrumentation, demand for highly specific, validated antibody panels and associated reagents compatible with these platforms continues to grow at an accelerated pace.

By Application: In 2024, the Proteomics Segment to Hold the Largest Share

Based on application, the global research antibodies and reagents market is segmented into proteomics, drug discovery and development, and genomics.

In 2024, the proteomics segment accounted for the largest share of the global research antibodies and reagents market. The large share of this segment is driven by the rising uptake of research antibodies within the significantly expanding global proteomics research landscape. The upsurge in proteomic research activity is attributed to the rising need for designing more effective drugs through protein based disease profiling, growing demand for personalized and protein therapeutics, and increasing public and private sector spending on proteomic research programs.

Drug discovery and development represent another important application segment, driven by the high consumption of research antibodies and reagents across target identification, lead validation, preclinical characterization, and biomarker development workflows. The expanding biopharmaceutical pipeline, particularly for complex antibody based therapies in oncology and immunology, continues to generate substantial and sustained demand for specialized research reagents throughout the development cycle.

Geographical Analysis

Based on geography, the global research antibodies and reagents market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

In 2024, North America accounted for the largest share of the global research antibodies and reagents. The leading position of North America is primarily attributed to the well established healthcare system in the region, higher acceptance of advanced research technologies, rising prevalence of non communicable diseases, increasing drug discovery programs and related growth in pharmaceutical research and development, rising focus on proteomics and genomics research, higher research funding from both government and industry sources, and the presence of a large number of key players operating in this market.

However, the Asia Pacific research antibodies and reagents market is projected to grow at the fastest rate during the forecast period. The rapid growth of this region is driven by rapidly developing economies, a large and growing population base, strong investment from government and non government bodies in the life sciences sector, and various technological advancements being implemented across research institutions in the region. China, India, and other emerging Asian markets are increasingly becoming important growth hubs due to rising healthcare investments, expanding research infrastructure, and an increasing burden of chronic and infectious diseases that is stimulating broader biomedical research activity.

The competitive environment within the global research antibodies and reagents market is shaped by continuous product innovation, strategic collaborations, geographic expansion, and the increasing importance of antibody validation and reproducibility standards. Leading companies are actively investing in expanding their antibody portfolios, strengthening their manufacturing capabilities, and pursuing partnerships and acquisitions to broaden their technological and commercial reach.

Thermo Fisher Scientific and Merck KGaA maintain leadership positions through their comprehensive and diversified product portfolios spanning primary and secondary antibodies, immunoassay reagents, and sample preparation chemistries that cater to virtually every research application. F. Hoffmann-La Roche AG, Agilent Technologies, and Becton Dickinson and Company also hold prominent positions, supported by their strong presence across flow cytometry, immunohistochemistry, and proteomics research segments.

Bio-Techne Corporation, Bio-Rad Laboratories, BioLegend, GenScript Biotech Corporation, Abcam (now a Danaher Company), Cell Signaling Technology, Santa Cruz Biotechnology, and OriGene Technologies are among the other key participants driving innovation and competitive activity across specialized product categories and end user segments.

The key strategies followed by most companies in the research antibodies and reagents market include partnerships, agreements and collaborations; product launches and enhancements; geographic expansions; and mergers and acquisitions, all aimed at strengthening market presence and accelerating the delivery of validated, high performance biological tools to the global research community.

Some of the key players operating in the global research antibodies and reagents market include Thermo Fisher Scientific Inc. (U.S.), Merck KGaA (Germany), F. Hoffmann-La Roche AG (Switzerland), Agilent Technologies, Inc. (U.S.), Becton Dickinson and Company (U.S.), PerkinElmer, Inc. (U.S.), GenScript Biotech Corporation (China), Bio-Techne Corporation (U.S.), Bio-Rad Laboratories, Inc. (U.S.), Santa Cruz Biotechnology, Inc. (U.S.), BioLegend, Inc. (U.S.), Abcam Plc (U.K.), OriGene Technologies, Inc. (U.S.), and Cell Signaling Technology, Inc. (U.S.), among others.

The global research antibodies and reagents market is expected to reach USD 6.76 billion by 2031 from USD 4.34 billion in 2024, growing at a CAGR of 6.5% during the forecast period 2024 to 2031.

In 2024, the antibodies segment is expected to hold the largest share of the global research antibodies and reagents market, driven by widespread application across biomedical research, drug discovery, diagnostics, and disease treatment programs.

In 2024, the flow cytometry segment is expected to hold the largest share of the global research antibodies and reagents market, supported by rising proteomics and cell based research and rapid adoption of high parameter spectral flow cytometry platforms.

In 2024, the proteomics segment is expected to hold the largest share of the global research antibodies and reagents market, driven by growing demand for protein based disease profiling and rising investment in proteomic research programs.

What are the major factors driving the growth of the global research antibodies and reagents market?

The growth of this market is primarily driven by the rapid expansion of proteomics and genomics research, rising R&D investments from pharmaceutical and biotechnology companies, increasing industry academia collaborations, and a growing biopharmaceutical pipeline that requires high volumes of research antibodies and reagents across all stages of drug discovery and development.

Key players operating in the research antibodies and reagents market include Thermo Fisher Scientific Inc. (U.S.), Merck KGaA (Germany), F. Hoffmann-La Roche AG (Switzerland), Agilent Technologies, Inc. (U.S.), Becton Dickinson and Company (U.S.), PerkinElmer, Inc. (U.S.), GenScript Biotech Corporation (China), Bio-Techne Corporation (U.S.), Bio-Rad Laboratories, Inc. (U.S.), Santa Cruz Biotechnology, Inc. (U.S.), BioLegend, Inc. (U.S.), Abcam Plc (U.K.), OriGene Technologies, Inc. (U.S.), and Cell Signaling Technology, Inc. (U.S.).

Asia Pacific is expected to register the highest growth rate in the global research antibodies and reagents market during the forecast period 2024 to 2031.

Published Date: Jan-2025

Published Date: Aug-2024

Published Date: Jul-2024

Published Date: Jun-2024

Published Date: Jul-2022

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates