Resources

About Us

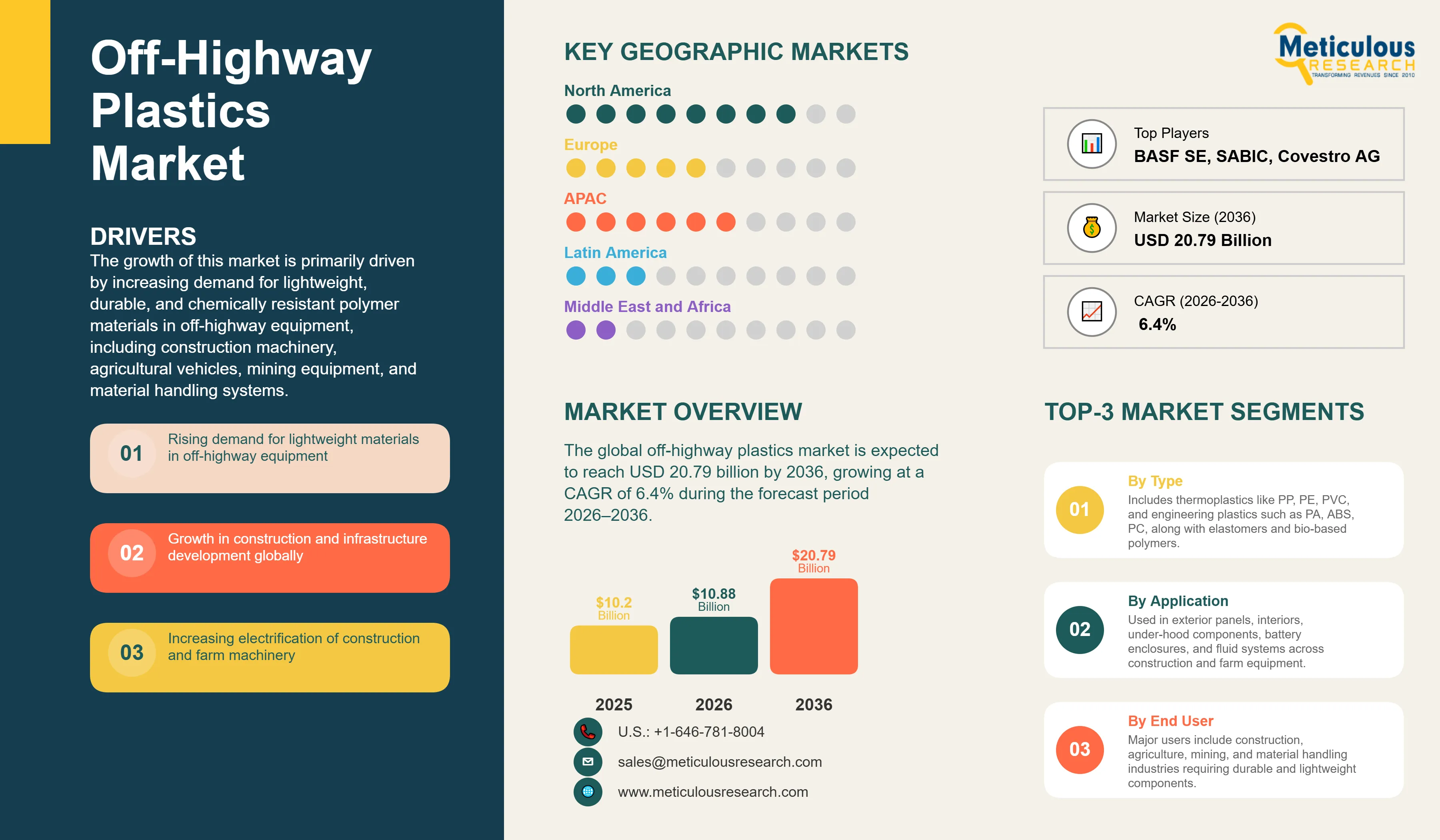

The global off-highway plastics market was valued at USD 10.2 billion in 2025. This market is expected to reach USD 20.79 billion by 2036 from an estimated USD 10.88 billion in 2026, growing at a CAGR of 6.4% during the forecast period 2026–2036.

The growth of this market is primarily driven by increasing demand for lightweight, durable, and chemically resistant polymer materials in off-highway equipment, including construction machinery, agricultural vehicles, mining equipment, and material handling systems. Plastics are increasingly replacing conventional metals to reduce equipment weight, enhance fuel efficiency, lower lifecycle maintenance costs, and support compliance with evolving emissions and sustainability regulations.

Click here to: Get Free Sample Pages of this Report

The global off-highway plastics market comprises a wide range of polymer materials, such as commodity thermoplastics such as polypropylene (PP), polyethylene (PE), and polyvinyl chloride (PVC); engineering thermoplastics such as polyamide (PA), polycarbonate (PC), acrylonitrile butadiene styrene (ABS), and polyoxymethylene (POM); thermoplastic elastomers (TPE); and bio-based polymers. These materials are processed through injection molding, extrusion, blow molding, compression molding, and additive manufacturing to produce structural and functional components for off-highway vehicles.

Off-highway equipment includes construction machinery (e.g., excavators, wheel loaders, bulldozers, motor graders, and concrete mixers), agricultural machinery (e.g., tractors, combine harvesters, sprayers, and seeding equipment), mining equipment (e.g., haul trucks, drilling systems, and continuous miners), and material handling equipment (e.g., forklifts, reach stackers, telehandlers, and automated guided vehicles).

Within these applications, plastics perform critical roles across exterior components (fenders, hoods, and side panels), interior cabin systems (dashboards, instrument panels, door trims, and seating structures), under-hood applications (fluid reservoirs, cooling system components, air intake ducts, and cable management systems), and semi-structural housings (including battery enclosures in electric equipment, hydraulic system components, and gearbox covers).

The increasing electrification of off-highway equipment is a major growth driver, as battery-electric and hybrid machinery require higher volumes of high-performance plastics for applications such as battery enclosures, high-voltage cable insulation and conduits, thermal management systems, and select structural components compared to internal combustion engine (ICE)-based platforms.

In addition, the expanding global infrastructure investment pipeline, mainly across Asia-Pacific, the Middle East, and North America, is driving demand for construction equipment, while the growing emphasis on food security and precision agriculture is driving the expansion of agricultural equipment fleets and increasing plastic content per machine in advanced farming systems.

However, market growth is restrained by volatility in petrochemical feedstock prices, which impacts polymer production costs, and increasing regulatory pressure around plastic waste management, recycling, and end-of-life disposal in industrial applications.

Key opportunities include the rising adoption of bio-based and recycled-content engineering plastics aligned with OEM sustainability commitments and regulatory frameworks such as the European End-of-Life Vehicles Directive; the increasing use of additive manufacturing (3D printing) for rapid prototyping and low-volume, customized components; and advancements in glass fiber- and carbon fiber-reinforced polymer composites enabling partial substitution of metals in semi-structural and structural applications.

Furthermore, the ongoing transition from conventional diesel-powered equipment toward battery-electric and, to a lesser extent, hydrogen fuel cell-based platforms is a major trend driving material selection and design requirements across the global off-highway plastics market.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 20.79 Billion |

|

Market Size in 2026 |

USD 10.88 Billion |

|

Market Size in 2025 |

USD 10.2 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 6.4% |

|

Dominating Material Type |

Polypropylene (PP) |

|

Fastest Growing Material Type |

Bio-based Plastics |

|

Dominating Process Type |

Injection Molding |

|

Fastest Growing Process Type |

Additive Manufacturing / 3D Printing |

|

Dominating End User |

Construction |

|

Fastest Growing End User |

Agriculture |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Electrification of Off-Highway Equipment Driving Fundamental Material Specification Shift

The increasing electrification of construction, agricultural, and material handling equipment is a key trend transforming material requirements across the off-highway plastics market. Battery-electric platforms necessitate advanced engineering plastics with performance characteristics beyond those required in conventional internal combustion engine (ICE) equipment. These include high-temperature polyamide and specialty polycarbonate grades for battery enclosures and thermal management systems, capable of maintaining structural integrity at elevated operating temperatures (typically ~80–150°C) while ensuring electrical insulation for high-voltage applications.

In addition, glass fiber-reinforced polypropylene and polyamide are increasingly utilized in lightweight structural components and battery support structures, enabling partial substitution of metal parts with significant weight reduction benefits. Thermoplastic elastomers are also gaining traction in high-voltage cable insulation and sealing applications, where durability, flexibility, and compliance with stringent electrical safety standards are critical.

Leading OEM initiatives, including electric equipment programs from Volvo Construction Equipment, Caterpillar, and CNH Industrial, are driving the adoption of these advanced materials at scale. Furthermore, stringent emissions regulations, such as the European Union Stage V standards and comparable frameworks in North America and Japan, are strengthening the transition toward electrified and low-emission powertrains, thereby driving demand for high-performance polymer materials in off-highway applications.

Metal Replacement and Weight Reduction Driving Engineering Polymer Adoption

The ongoing shift toward metal-to-plastic substitution in off-highway equipment, driven by the dual imperatives of weight reduction for improved fuel efficiency and emissions compliance, and cost optimization through part consolidation and design flexibility, is driving the addressable market for engineering polymers across structural and semi-structural applications traditionally dominated by steel and aluminum.

Glass fiber-reinforced polypropylene (typically ~20–40% GF content in commercial applications) is increasingly displacing metals in medium load-bearing components such as brackets, seat structures, and access panels, enabling weight reductions in the range of ~15–30% while maintaining required mechanical performance. Long glass fiber-reinforced thermoplastics (LGF-PP and LGF-PA) are gaining traction in semi-structural applications, including cab floor modules and underbody shielding systems, due to their enhanced stiffness-to-weight ratio and impact resistance.

Polyoxymethylene (POM/acetal) is widely used as a substitute for machined metals in precision components such as gears, bearing cages, and valve systems, where high dimensional stability, low friction, and wear resistance are critical. Additionally, polyamide materials, mainly PA66 and high-temperature variants, are increasingly replacing metals in fluid handling and under-hood applications, such as oil pans, coolant reservoirs, and hydraulic system components operating under elevated temperatures and chemically demanding conditions.

Bio-based and Recycled-Content Plastics Responding to OEM Sustainability Mandates

The increasing adoption of bio-based and recycled-content engineering plastics in off-highway equipment is driven by OEM sustainability commitments, including alignment with Science Based Targets initiative (SBTi) frameworks, Scope 3 emissions reduction programs, and circular economy principles, alongside tightening regulatory expectations around material sustainability in Europe and North America.

Bio-based polyamides are gaining traction in applications such as fluid handling systems, cable management, and select housings, where they offer comparable performance to fossil-based counterparts while enabling measurable reductions in product carbon footprint. Materials such as castor oil-derived polyamides and bio-attributed engineering plastics are increasingly incorporated into OEM material specifications, mainly in applications where lifecycle emissions are a key procurement criterion.

In parallel, post-consumer recycled (PCR) and post-industrial recycled (PIR) polypropylene and polyethylene are witnessing growing adoption in non-structural and semi-structural components, including exterior panels, flooring systems, and interior cabin elements. Advancements in compounding technologies are enabling higher recycled content (typically ~20–50%) while maintaining the required mechanical and durability performance for industrial applications.

Regulatory developments act as an important catalyst, although current frameworks such as the European End-of-Life Vehicles (ELV) Directive primarily apply to passenger vehicles and light-duty commercial vehicles, with limited direct applicability to off-highway equipment. However, ongoing policy discussions and broader EU sustainability initiatives, such as circular economy action plans and construction-related material regulations, are expected to indirectly influence material selection in off-highway applications.

As a result, bio-based and recycled-content plastics are emerging as key drivers of OEM sustainability strategies, supporting both regulatory alignment and voluntary carbon reduction targets across the off-highway equipment value chain.

By Material Type: In 2026, Polypropylene to Dominate the Global Off-Highway Plastics Market

Based on material type, the global off-highway plastics market is segmented into polypropylene (PP), polyvinyl chloride (PVC), polyethylene (PE), polyamide (PA), acrylonitrile butadiene styrene (ABS), polycarbonate (PC), polyoxymethylene (POM), thermoplastic elastomers (TPE), and bio-based plastics.

In 2026, polypropylene is expected to account for the largest market share. This dominance is attributed to its well-balanced property profile, making it suitable for a wide range of off-highway applications. It offers strong impact resistance, fatigue performance, and chemical resistance, enabling reliable operation under exposure to fuels, lubricants, moisture, dust, and variable temperature conditions typical of construction, agricultural, and mining environments. Its low density supports weight reduction compared to metal alternatives, while its excellent processability enables the production of complex and large components such as exterior panels, fenders, engine covers, battery housings, and interior trims.

Additionally, polypropylene can be reinforced with glass fibers, mineral fillers, and elastomers to enhance mechanical strength and stiffness for semi-structural applications.

Polypropylene also provides adequate electrical insulation properties for cable management and battery-related applications in electrified equipment. Furthermore, its cost competitiveness and well-established global supply chain support widespread adoption across OEM tiers.

However, the bio-based plastics market is poised to grow at the fastest CAGR during the forecast period. This growth is driven by increasing OEM focus on sustainability, rising incorporation of bio-based or bio-attributed materials in component specifications, improving cost dynamics with scale, and the expanding availability of high-performance bio-based engineering polymers that meet the mechanical and thermal requirements of off-highway applications.

By Process Type: In 2026, Injection Molding to Hold the Largest Share

The global off-highway plastics market is segmented by process type into injection molding, extrusion, compression molding, blow molding, additive manufacturing/3D printing, and others.

In 2026, injection molding is projected to command the largest share due to its established dominance in high-volume manufacturing of intricate precision components such as dashboards, fenders, engine covers, structural housings, and cab interiors for off-highway equipment. This process excels in delivering tight tolerances, superior surface finishes, design versatility for complex geometries with integrated features, and compatibility with high-performance engineering polymers and reinforced compounds essential for rugged applications.

Recent innovations like multi-cavity tooling, gas-assisted injection, and automated systems have boosted production speeds and material efficiency, enabling manufacturers to meet demanding mechanical, thermal, and chemical resistance requirements in harsh off-highway environments. These capabilities solidify injection molding's position for structural and functional parts where reliability under extreme conditions is non-negotiable.

Meanwhile, the off-highway plastics market for additive manufacturing/3D printing is poised for the highest CAGR over the 2026–2036 forecast period. Its rapid growth stems from expanding roles in tooling, fixtures, and low-volume custom replacements for legacy equipment, leveraging processes like selective laser sintering (SLS) and fused deposition modeling (FDM) with advanced filaments such as PA12, PEEK, and PETG.

By End User: In 2026, Construction to Hold the Largest Share

The global off-highway plastics market is segmented by end user into construction, agriculture, mining, and material handling.

In 2026, the construction segment is expected to account for the largest market share, driven by the extensive global fleet of equipment, including excavators, wheel loaders, motor graders, concrete mixers, and earthmoving machinery, driven by ongoing infrastructure investments across major economies.

Plastics are widely utilized across construction equipment in operator cabins (dashboards, instrument panels, door trims), exterior components (engine covers, hoods, and side panels), hydraulic systems (reservoirs, hoses, and manifolds), and increasingly in electrified subsystems such as battery enclosures and cable management. Large-scale infrastructure initiatives, such as public investment programs in North America, Asia-Pacific, and the Middle East, continue to support high equipment production volumes, thereby driving consistent demand for polymer components that enable durability, corrosion resistance, and weight reduction.

However, the off-highway plastics market for the agriculture segment is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing adoption of precision agriculture technologies, including GPS-guided systems, autonomous machinery, and sensor-based crop monitoring, all of which require advanced plastic housings and enclosures for electronic components.

Additionally, rising global food demand, expanding farm mechanization in emerging markets, and the gradual electrification of agricultural equipment are contributing to higher plastic content per machine, driving the transition toward lighter, more efficient, and technologically advanced farming systems.

The global off-highway plastics market is segmented geographically into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. In 2026, North America is expected to account for the largest share, primarily driven by the U.S., which is one of the largest national markets for off-highway equipment across construction, agriculture, and mining.

The growth of the off-highway plastics market in North America is further supported by the strong presence of leading OEMs, including Caterpillar, John Deere, CNH Industrial, and Komatsu, which drive consistent demand for high-performance polymer components.

Additionally, large-scale infrastructure investments, mainly under the U.S. Infrastructure Investment and Jobs Act, are supporting equipment demand for applications such as transportation, utilities, and logistics. Stringent emissions regulations for non-road diesel engines are also driving the transition toward electrified and low-emission equipment platforms, thereby increasing demand for advanced plastics in battery systems, electrical insulation, and lightweight structural components.

However, the Asia-Pacific off-highway plastics market is poised to grow at the highest CAGR during the forecast period. This growth is driven by China’s position as the largest market for construction equipment and a key global manufacturing hub, along with significant infrastructure development initiatives across India, Southeast Asia, and other emerging economies. Programs focused on transportation infrastructure, urban development, energy, and agricultural modernization are fueling demand for construction and agricultural machinery.

Furthermore, rapid urbanization, population growth, and increasing mechanization in agriculture are contributing to rising demand for off-highway equipment across the region. This, in turn, is driving the adoption of lightweight, durable, and cost-effective plastic components to enhance equipment efficiency, performance, and lifecycle durability.

The competitive landscape of the global off-highway plastics market is characterized by continuous material innovation, increasing focus on lightweighting and electrification requirements, and rising investments in sustainable polymers, including bio-based and recycled-content materials.

Key players are prioritizing strategic collaborations with OEMs, expanding production and compounding capacities in high-growth regions, and developing application-specific formulations to enhance performance and meet evolving regulatory requirements.

Some of the key players operating in the global off-highway plastics market are BASF SE, SABIC, Covestro AG, LyondellBasell Industries N.V., Dow Inc., Evonik Industries AG, DuPont de Nemours, Inc., Borealis AG, Arkema S.A., LANXESS AG, Solvay, DSM Engineering Materials, Celanese Corporation, Mitsubishi Chemical Corporation, and ExxonMobil Corporation, among others.

The global off-highway plastics market is expected to reach USD 20.79 billion by 2036 from an estimated USD 10.88 billion in 2026, at a CAGR of 6.4% during the forecast period 2026–2036.

In 2026, polypropylene (PP) is expected to hold the largest market share of the global off-highway plastics market, driven by its superior balance of impact resistance, chemical stability, lightweight properties, and cost-effectiveness across construction, agriculture, mining, and material handling applications.

Bio-based plastics are expected to register the highest CAGR during the forecast period 2026–2036, driven by accelerating OEM sustainability mandates, regulatory requirements for renewable content, and improving price competitiveness of bio-based engineering polymer grades.

In 2026, injection molding is expected to hold the largest market share, driven by its dominance in high-volume production of complex precision plastic components for off-highway equipment with tight tolerances and excellent surface finish.

In 2026, the construction segment is expected to hold the largest market share of the global off-highway plastics market, driven by sustained global infrastructure investment and the large construction equipment fleet requiring diverse plastic components.

The growth of this market is primarily driven by rising demand for lightweight durable plastics in off-highway equipment replacing metals for weight reduction and emission compliance, accelerating electrification of construction and agricultural equipment requiring high-performance engineering polymers for battery systems, and expanding global infrastructure and agricultural investment sustaining equipment demand.

Key players are BASF SE (Germany), SABIC (Saudi Arabia), Covestro AG (Germany), LyondellBasell Industries N.V. (Netherlands), Dow Inc. (U.S.), Evonik Industries AG (Germany), DuPont de Nemours, Inc. (U.S.), Borealis AG (Austria), Arkema S.A. (France), LANXESS AG (Germany), Solvay S.A. (Belgium), DSM Engineering Materials (Netherlands), Celanese Corporation (U.S.), Mitsubishi Chemical Corporation (Japan), and ExxonMobil Chemical Company (U.S.).

Asia Pacific is expected to register the highest growth rate in the global off-highway plastics market during the forecast period 2026–2036, driven by massive infrastructure development, expanding agricultural mechanization, and the region's role as the primary global manufacturing hub for off-highway equipment and polymer components.

1. Introduction

1.1 Market Definition and Scope

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

3.1 Market Overview

3.2 Market Analysis by Material Type

3.3 Market Analysis by Process Type

3.4 Market Analysis by End User

3.5 Market Analysis by Geography

4. Market Dynamics

4.1 Overview

4.2 Drivers

4.2.1 Rising Demand for Lightweight Durable Plastics Replacing Metals in Off-Highway Equipment for Weight Reduction and Fuel Efficiency

4.2.2 Accelerating Electrification of Construction, Agricultural, and Mining Equipment Requiring High-Performance Engineering Polymers

4.2.3 Expanding Global Infrastructure Investment and Agricultural Mechanization Driving Off-Highway Equipment Demand

4.2.4 Stringent Emissions Regulations (Stage V, EPA Tier 4 Final) Driving Material Innovation and Lightweighting

4.3 Restraints

4.3.1 Volatility of Petrochemical Feedstock Prices Affecting Polymer Production Costs and OEM Procurement Budgets

4.3.2 Growing Regulatory Pressure to Reduce End-of-Life Plastic Waste from Industrial Equipment and Vehicles

4.4 Opportunities

4.4.1 Bio-based and Recycled-Content Plastics Responding to OEM Sustainability Mandates and Circular Economy Regulations

4.4.2 Advanced Glass-Fiber and Carbon-Fiber Reinforced Polymer Compounds Enabling Structural Metal Replacement in Load-Bearing Components

4.4.3 Additive Manufacturing for Custom and Low-Volume Off-Highway Replacement Part Production and Rapid Prototyping

4.5 Challenges

4.5.1 Harsh Operating Environments of Mining and Construction Applications Demanding Extreme Durability and Chemical Resistance Standards

4.5.2 Long Equipment Lifecycles and Extended Qualification Timelines for New Material Adoption in Safety-Critical Off-Highway Components

4.6 Porter’s Five Forces Analysis

5. Off-Highway Plastics Market, by Material Type

5.1 Overview

5.2 Polypropylene (PP)

5.2.1 Homopolymer PP

5.2.2 Copolymer PP

5.2.3 Glass-Fiber Reinforced PP

5.3 Polyvinyl Chloride (PVC)

5.4 Polyethylene (PE)

5.4.1 HDPE

5.4.2 UHMWPE

5.5 Polyamide (PA)

5.5.1 PA6

5.5.2 PA66

5.5.3 High-Temperature PA (PA46, PPA)

5.6 Acrylonitrile Butadiene Styrene (ABS)

5.7 Polycarbonate (PC)

5.8 Polyoxymethylene (POM)

5.9 Thermoplastic Elastomer (TPE)

5.10 Bio-based Plastics

5.10.1 Bio-based PA (Bio-PA12, Bio-PA11)

5.10.2 Bio-based PE (Bio-PE)

5.10.3 Bio-based PP (Bio-PP)

6. Off-Highway Plastics Market, by Process Type

6.1 Overview

6.2 Injection Molding

6.3 Extrusion

6.4 Compression Molding

6.5 Blow Molding

6.6 Additive Manufacturing / 3D Printing

6.7 Other Process Types

7. Off-Highway Plastics Market, by End User

7.1 Overview

7.2 Construction

7.2.1 Excavators

7.2.2 Wheel Loaders & Bulldozers

7.2.3 Motor Graders & Compactors

7.2.4 Concrete & Road Machinery

7.3 Agriculture

7.3.1 Tractors

7.3.2 Combine Harvesters

7.3.3 Sprayers & Seeding Equipment

7.4 Mining

7.4.1 Haul Trucks

7.4.2 Drilling & Blasting Equipment

7.4.3 Continuous Miners & Roof Bolters

7.5 Material Handling

7.5.1 Forklifts & Reach Stackers

7.5.2 Telehandlers

7.5.3 Automated Guided Vehicles (AGVs)

8. Off-Highway Plastics Market, by Geography

8.1 Overview

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.3 Europe

8.3.1 Germany

8.3.2 U.K.

8.3.3 France

8.3.4 Sweden

8.3.5 Italy

8.3.6 Spain

8.3.7 Rest of Europe

8.4 Asia Pacific

8.4.1 China

8.4.2 India

8.4.3 Japan

8.4.4 South Korea

8.4.5 Indonesia

8.4.6 Rest of Asia Pacific

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Argentina

8.5.4 Rest of Latin America

8.6 Middle East and Africa

8.6.1 South Africa

8.6.2 Saudi Arabia

8.6.3 Rest of Middle East and Africa

9. Competitive Landscape

9.1 Overview

9.2 Key Growth Strategies

9.3 Competitive Benchmarking

9.4 Competitive Dashboard

9.4.1 Industry Leaders

9.4.2 Market Differentiators

9.4.3 Vanguards

9.4.4 Emerging Companies

9.5 Market Share Analysis (2025)

10. Company Profiles

10.1 BASF SE

10.2 SABIC

10.3 Covestro AG

10.4 LyondellBasell Industries N.V.

10.5 Dow Inc.

10.6 Evonik Industries AG

10.7 DuPont de Nemours, Inc.

10.8 Borealis AG

10.9 Arkema S.A.

10.10 LANXESS AG

10.11 Solvay S.A.

10.12 DSM Engineering Materials (part of Envalior)

10.13 Celanese Corporation

10.14 Mitsubishi Chemical Corporation

10.15 ExxonMobil Corporation

10.16 Röchling Group (Germany)

10.17 Trelleborg AB (Sweden)

10.18 Mack Molding Co. (US)

10.19 Others

11. Appendix

11.1 Questionnaire

11.2 Available Customization Options

11.3 Related Reports

Published Date: Mar-2026

Published Date: Dec-2025

Published Date: Sep-2024

Published Date: May-2024

Published Date: Jan-2024

Subscribe to get the latest industry updates