Resources

About Us

Plastic Upcycling Technology Market by Technology (Chemical Recycling -- Pyrolysis, Gasification), Plastic Type (PET, HDPE), Output Product, End-Use Industry (Packaging, Textiles & Apparel, Automotive) - Global Forecast to 2036

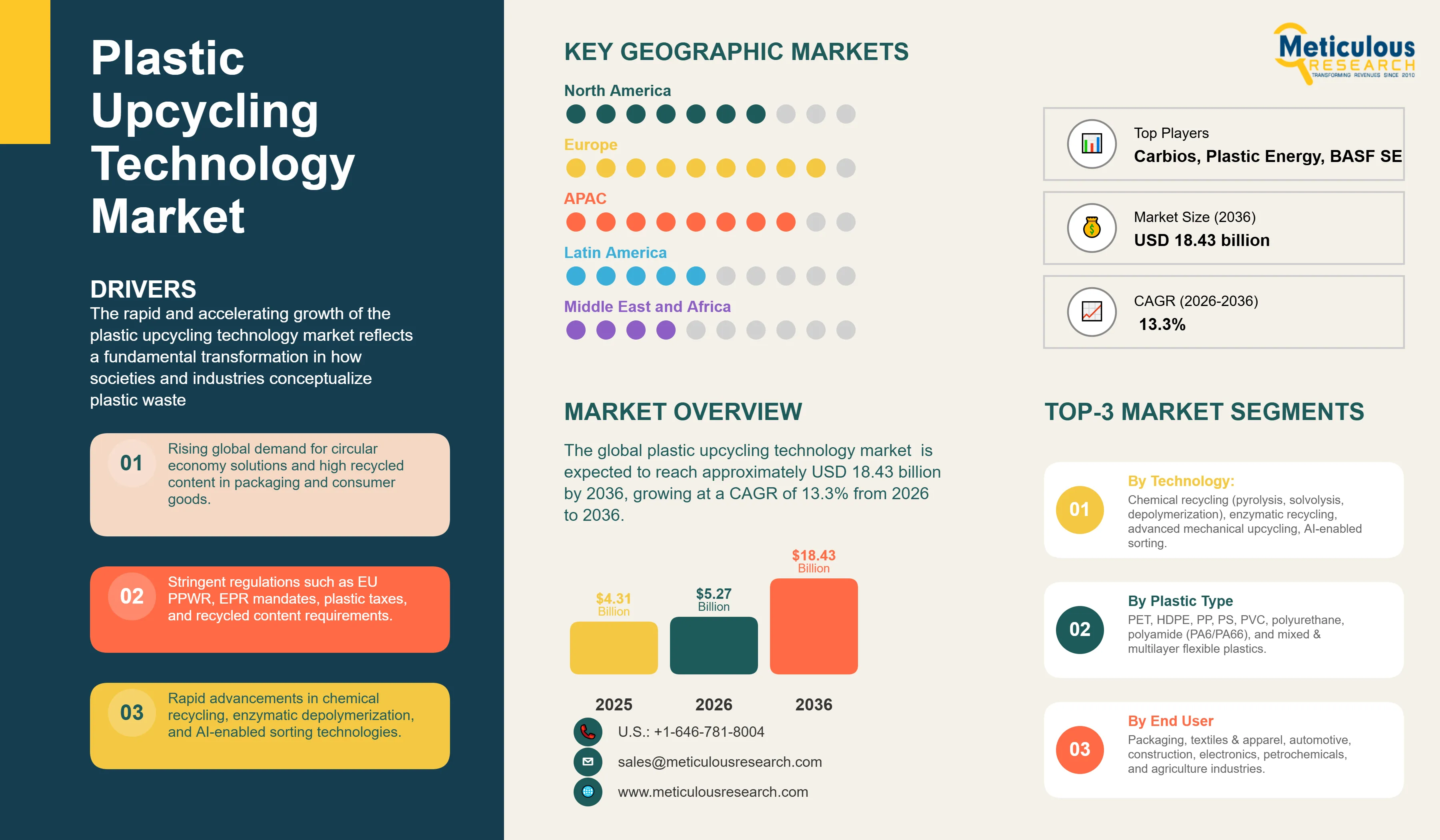

Report ID: MRCHM - 1041836 Pages: 292 Mar-2026 Formats*: PDF Category: Chemicals and Materials Delivery: 24 to 72 Hours Download Free Sample ReportThe global plastic upcycling technology market was valued at USD 4.31 billion in 2025. The market is expected to reach approximately USD 18.43 billion by 2036 from USD 5.27 billion in 2026, growing at a CAGR of 13.3% from 2026 to 2036. The rapid and accelerating growth of the plastic upcycling technology market reflects a fundamental transformation in how societies and industries conceptualize plastic waste — shifting from a linear model of produce-use-discard toward circular economy frameworks that recover maximum material value from post-consumer and post-industrial plastic streams through technologies that convert waste plastics into feedstocks, monomers, fuels, and high-value materials equal to or exceeding the quality of virgin petroleum-derived equivalents. Plastic upcycling transcends conventional mechanical recycling by targeting quality retention or enhancement — producing outputs with comparable or superior properties to the original material rather than the property-degraded downcycled products that traditional mechanical recycling generates from contaminated or mixed plastic streams. The scale of the opportunity is staggering: of the approximately 400 million metric tonnes of plastic produced globally each year, less than 10% is effectively recycled, with the remainder entering landfill, incineration, or the natural environment — representing both an enormous environmental liability and an equally enormous feedstock opportunity for upcycling technologies that can economically convert this waste stream into valuable materials and chemicals. The convergence of regulatory mandates requiring recycled content in plastic products, brand owner commitments to circularity targets, and the commercial maturation of advanced chemical recycling, enzymatic degradation, and AI-powered sorting technologies is creating the structural conditions for plastic upcycling to scale from niche pilot operations toward industrial-scale infrastructure capable of meaningful impact on global plastic waste flows.

Click here to: Get Free Sample Pages of this Report

Plastic upcycling encompasses a spectrum of technologies and processes that convert post-consumer and post-industrial plastic waste into products of equal or greater value than the original material, fundamentally distinguishing itself from conventional mechanical recycling which typically produces lower-quality downcycled outputs with degraded mechanical and aesthetic properties unsuitable for demanding applications including food contact packaging. The upcycling technology landscape is organized around three primary technological approaches: chemical recycling converts plastics back into their constituent monomers or into hydrocarbon feedstocks through thermal, catalytic, or chemical processes; enhanced mechanical recycling applies advanced sorting, decontamination, and compatibilization technologies to produce high-quality recycled polymers meeting demanding specifications; and biological upcycling employs engineered enzymes and microorganisms to depolymerize specific plastic types into recoverable monomers or higher-value biochemicals.

Chemical recycling represents the most technically diverse and fastest-growing segment of plastic upcycling technology, encompassing multiple distinct process routes addressing different plastic types and target outputs. Pyrolysis -- thermal decomposition of plastic waste in the absence of oxygen at temperatures of 400-600 degrees Celsius -- converts mixed polyolefins and polystyrene into pyrolysis oil, a hydrocarbon mixture usable as chemical plant feedstock or as fuel, alongside syngas and char by-products. Gasification converts plastic waste at higher temperatures (700-1200 degrees Celsius) into synthesis gas (carbon monoxide and hydrogen) that can be used for chemical synthesis, power generation, or hydrogen production. Solvolysis processes -- including glycolysis, hydrolysis, methanolysis, and aminolysis -- depolymerize specific condensation polymers including PET and polyurethanes using solvent or reactive agents to recover purified monomers including BHET (bis(2-hydroxyethyl) terephthalate), TPA (terephthalic acid), and EG (ethylene glycol) that can be repolymerized into virgin-equivalent materials. Enzymatic depolymerization using engineered PETase and related enzymes -- most notably Carbios's patented thermophilic enzyme technology -- enables selective depolymerization of PET plastics at moderate temperatures with high selectivity for the target polymer, enabling processing of mixed and contaminated PET streams that chemical processes require pre-sorted feedstock to handle economically.

The commercial landscape of plastic upcycling technology is rapidly evolving from early-stage pilot facilities toward industrial-scale operations, with significant investment from both specialized upcycling technology developers and major petrochemical companies seeking to meet regulatory recycled content mandates and brand owner procurement commitments. SABIC, LyondellBasell, Dow, BASF, and Ineos have all announced substantial investments in pyrolysis-based chemical recycling capacity, integrating upcycled plastic feedstock into existing cracker and polymer production infrastructure. Specialized chemical recycling companies including Plastic Energy, Renewlogy, Pyrowave, Plastic2Fuel, and Neste's plastic waste refinery operations are developing proprietary pyrolysis technologies with differentiated catalyst systems and process optimization. PET depolymerization specialists including Carbios, Loop Industries, gr3n, Rematpet, and Ioniqa Technologies are commercializing enzymatic and solvolysis PET recycling at increasing scale, with Carbios's first industrial facility in France targeting 50,000 tonnes per year PET processing capacity. Brand owners including Unilever, Nestle, PepsiCo, L'Oreal, and Danone have committed to specific recycled content targets in plastic packaging that are creating contractual demand for upcycled plastic outputs, providing the revenue certainty enabling upcycling infrastructure investment at commercial scale.

Enzymatic Depolymerization Achieving Commercial Breakthrough for PET Upcycling

Enzymatic depolymerization of PET plastic -- using engineered thermostable PETase enzymes to selectively cleave ester bonds throughout the PET polymer chain, releasing terephthalic acid (TPA) and ethylene glycol (EG) monomers of virgin-equivalent purity -- has achieved commercial-scale breakthrough after more than a decade of laboratory and pilot development, representing the most significant innovation in plastic recycling science since mechanical bottle-to-bottle recycling was established in the 1990s. Carbios, the French biochemical company that developed the most advanced thermophilic enzyme variant in partnership with researchers from INSA Toulouse, demonstrated 90% depolymerization of post-consumer PET waste within 10 hours using its leaf-branch compost cutinase (LCCICCG) enzyme at 72 degrees Celsius -- enabling economically viable industrial depolymerization at temperature conditions far below conventional chemical glycolysis or methanolysis processes and with superior selectivity enabling processing of contaminated PET waste streams including colored bottles, opaque trays, and PET fabrics. Carbios signed licensing agreements with major PET producers including Indorama Ventures, Zhink Group, Far Eastern New Century, and Neo Group to deploy the technology at industrial scale globally, with Indorama -- the world's largest PET producer -- committed to integrating enzymatic recycling into its global production network representing over 12 million tonnes per year of PET processing capacity. The commercial significance extends beyond PET: the successful commercialization of PETase has catalyzed enzyme engineering efforts targeting other plastic polymers including polyurethanes (using cutinases and lipases targeting ester bonds in ester-based PU), polylactic acid, and potentially polyolefins through novel oxidative enzyme systems, suggesting that biological depolymerization may progressively extend to additional plastic types as enzyme engineering advances.

AI-Powered Sorting and Pre-Processing Enabling Economic Feedstock Quality for Chemical Recycling

The economic viability of advanced plastic upcycling technologies -- particularly chemical recycling processes that require well-characterized, minimally contaminated feedstock to achieve consistent product quality and process efficiency -- depends critically on the upstream sorting and pre-processing infrastructure that separates mixed post-consumer plastic waste into discrete polymer streams and removes food residues, labels, closures, and other contaminants. AI-powered near-infrared and hyperspectral imaging sorting systems capable of identifying plastic polymer types, colors, and contamination levels at conveyor belt speeds of 3-6 meters per second with over 95% accuracy -- provided by companies including AMP Robotics, Machinex, TOMRA, Steinert, and Sesotec -- are transforming the economics of plastic waste sorting by enabling automated processing of mixed plastic streams with labor cost advantages over manual sorting and quality advantages over earlier generation single-wavelength NIR sorting systems. AMP Robotics' robotic sorting systems combining computer vision, AI classification trained on billions of material images, and robotic picking arms operating at 80+ picks per minute are being deployed at Material Recovery Facilities in the United States and Europe, enabling economic recovery of plastic streams previously discarded as residual due to marginal economics at manual sorting labor rates. Digital watermarking technology -- pioneered by HolyGrail 2.0, a consortium including over 130 consumer goods companies and recyclers using cryptographic watermarks printed into packaging that NIR sorting systems can read -- enables automatic sorting of packaging to brand, grade, and recycled content level, creating the feedstock quality differentiation that premium upcycling processes require. The integration of AI sorting data with chemical recycling plant operations through digital twins and feedstock management systems enables upcycling facilities to optimize blend compositions for target pyrolysis oil or monomer outputs, improving process efficiency and output quality in ways that manual feedstock characterization cannot achieve.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 18.43 Billion |

|

Market Size in 2026 |

USD 5.27 Billion |

|

Market Size in 2025 |

USD 4.31 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 13.3% |

|

Dominating Region |

Europe |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Technology, Plastic Type, Output Product, End-Use Industry, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Extended Producer Responsibility Regulations and Recycled Content Mandates

The primary regulatory driver of plastic upcycling market growth is the global proliferation of extended producer responsibility frameworks and mandatory recycled content requirements that are creating legally enforceable obligations for plastic producers, brand owners, and retailers to source specified proportions of recycled plastic content -- directly generating contracted demand for upcycled plastic outputs that justifies the capital investment in upcycling infrastructure. The European Union's Packaging and Packaging Waste Regulation -- adopted in final form in 2024 -- mandates minimum recycled content percentages in plastic packaging ranging from 10% for contact-sensitive packaging to 35% for PET beverage bottles by 2030 and 65% for all plastic packaging by 2040, creating a multi-million tonne annual demand for high-quality recycled plastic that only advanced chemical recycling and enhanced mechanical upcycling can supply in sufficient volume and quality. The UK Plastic Packaging Tax -- imposing GBP 210.82 per tonne on plastic packaging containing less than 30% recycled content -- has created direct financial incentives for brands to source recycled plastic, with revenues earmarked to support recycling infrastructure investment. California's SB 343 and AB 793 mandate minimum recycled content in single-use plastic bottles and packaging, establishing the most stringent state-level requirements in the United States and creating pressure for similar federal legislation. Brand owner voluntary commitments -- with Unilever targeting 25% recycled plastic content across packaging by 2025, PepsiCo committing to 50% recycled content in primary plastic packaging by 2030, and L'Oreal targeting 50% recycled or bio-sourced plastic in all plastic packaging by 2030 -- translate regulatory pressure into procurement commitments that provide revenue visibility for upcycling capacity investment.

Opportunity: Plastic Waste-to-Circular Feedstock for Petrochemical Industry Decarbonization

The strategic opportunity for plastic upcycling technologies to serve as the circular feedstock pathway for the global petrochemical industry's decarbonization commitments represents the largest long-term market expansion potential in the sector, with major petrochemical companies including SABIC, LyondellBasell, Dow, BASF, Borealis, and Ineos actively integrating upcycled plastic streams into existing cracker and polymer production infrastructure as a mechanism for reducing Scope 3 emissions while meeting recycled content obligations. The circular feedstock pathway -- where pyrolysis oil from mixed plastic waste is co-processed in existing steam crackers alongside naphtha to produce ethylene and propylene that are subsequently polymerized into certified circular polymers carrying mass balance chain-of-custody certification -- enables major polymer producers to offer circular product lines without constructing dedicated recycling infrastructure. SABIC's TRUCIRCLE circular polymers, LyondellBasell's Circulen products, and Dow's recycled content product lines are commercially available circular polymer grades produced via mass balance accounting from pyrolysis oil co-processing, creating a scalable pathway for chemical recycling integration into conventional petrochemical production. The International Energy Agency estimates that achieving global plastic recycling rates of 50% by 2050 -- compared to current rates below 10% -- would reduce the petrochemical industry's oil demand by approximately 200 million tonnes per year and CO2 emissions by 1.5 billion tonnes annually, representing a decarbonization contribution equivalent to eliminating the entire aviation industry's emissions. This macro-scale opportunity is driving national government investment in plastic waste collection and sorting infrastructure as the feedstock supply chain prerequisite for large-scale chemical recycling, with the EU's Circular Economy Action Plan, China's 14th Five-Year Plan plastic recycling targets, and US EPA's National Recycling Strategy collectively mobilizing public investment that complements private capital in building the integrated plastic waste-to-feedstock value chains that industrial-scale upcycling requires.

Why Does Chemical Recycling Lead the Technology Market?

Chemical recycling technologies command approximately 48-52% of total plastic upcycling technology market revenue in 2026, reflecting the technology class's unique capability to process the widest range of plastic waste types -- including mixed, contaminated, multilayer, and flexible plastic packaging that mechanical recycling cannot economically handle -- while producing outputs including virgin-equivalent monomers and chemical plant feedstocks that command substantial price premiums over downcycled mechanical recycling outputs. Pyrolysis-based chemical recycling represents the most commercially mature and widely deployed chemical recycling technology, with multiple commercial-scale facilities operational in Europe and North America processing mixed plastic waste streams into pyrolysis oil for co-processing in steam crackers or for use as refinery feedstock. The pyrolysis technology landscape encompasses continuous and batch process configurations from suppliers including Plastic Energy (TACOIL technology), Quantafuel, Pyrowave, Renewlogy, Encina, Brightmark Energy, and Mura Technology (HydroPRS supercritical water process), each with differentiated process conditions, catalyst systems, and target output specifications. Depolymerization technologies targeting specific condensation polymers -- Carbios for PET enzymatic recycling, Eastman's Polyester Renewal Technology for PET and PA, Loop Industries' catalytic depolymerization, and Ioniqa's magnetic catalyst-based glycolysis -- produce high-purity monomers that can be repolymerized into certified virgin-equivalent materials carrying International Sustainability and Carbon Certification (ISCC+) and similar chain-of-custody certifications that enable brand owners to make verified recycled content claims. Mechanical upcycling technologies -- incorporating advanced sorting, decontamination including supercritical CO2 extraction and solid-state vacuum stripping, compatibilization with reactive extrusion additives, and property-enhancing additives -- are progressively narrowing the quality gap between mechanically recycled and virgin polymers, enabling premium applications including food contact packaging and automotive components that previously required virgin material specifications.

Why Does PET Lead the Plastic Upcycling Market?

PET (polyethylene terephthalate) commands approximately 30-34% of plastic upcycling technology market revenue in 2026, reflecting the most developed and commercially mature upcycling ecosystem of any plastic polymer type, encompassing both well-established mechanical bottle-to-bottle recycling infrastructure and the most advanced chemical depolymerization technologies reaching commercial scale in this period. The PET upcycling advantage stems from PET's widespread use in beverage bottles and food packaging where deposit return schemes and kerbside collection programs have established high-quality feedstock collection rates of 30-70% in leading markets, providing the volume and quality of post-consumer PET necessary to support industrial-scale upcycling operations. Chemical depolymerization of PET -- whether through enzymatic (Carbios), methanolysis (Aquafil, Worn Again), glycolysis (multiple operators), or hydrolysis routes -- produces TPA and EG monomers of virgin-equivalent purity suitable for repolymerization into food-contact grade rPET meeting the demanding quality specifications of Coca-Cola, PepsiCo, Danone, and Nestle Waters' commitments to 50-100% recycled content in PET beverage bottles by 2025-2030. HDPE and PP represent the second and third-largest plastic type upcycling segments, serving applications including recycled content rigid packaging, agricultural film processing, and automotive parts where mechanical upcycling with enhanced decontamination and compatibilization produces materials meeting the elevated performance specifications demanded by automotive OEMs and premium packaging applications. Mixed and multilayer plastic packaging -- representing the most challenging and currently least-recovered plastic waste stream -- is the highest-growth upcycling technology target, as chemical recycling via pyrolysis provides the only economically viable pathway for converting multi-layer food packaging films, pouches, and composite packaging into recoverable value.

How Do Recycled Monomers and Feedstocks Lead by Value?

Recycled monomers and chemical feedstocks -- produced by depolymerization of condensation polymers including PET, polyurethanes, polyamides, and polycarbonates to recover their constituent chemical building blocks -- command the highest value per tonne of any plastic upcycling output, with virgin-equivalent TPA, EG, caprolactam, and diols produced by chemical recycling achieving price parity with petrochemical-derived equivalents while qualifying for significant price premiums from brand owners seeking certified circular content for sustainability commitments. Virgin-equivalent rTPA from PET depolymerization commands prices comparable to petro-TPA in commodity markets while accessing premium pricing of 10-30% above commodity in sustainability-certified channels where brand owners compete for limited available supply to meet recycled content targets. Pyrolysis oil from mixed plastic waste pyrolysis -- trading at discounts of 10-30% to fossil naphtha in commodity channels but qualifying for substantial premiums as certified circular feedstock in mass balance accounting frameworks adopted by major polymer producers -- represents the largest volume output product category by processed tonnage, with the price differential reflecting residual specification differences including higher olefin content and chlorine levels requiring management in co-processing applications. High-value polymer outputs from mechanical upcycling -- including food-grade recycled PET pellets, engineering-grade recycled PC/ABS for electronics, and recycled nylon 6 and 6,6 from carpet and fishing net processing -- represent significant value-per-tonne output categories where quality certifications, chain-of-custody documentation, and application-specific performance testing create defensible price premiums over commodity recycled pellets in demanding end-use applications.

Why Does Packaging Lead the End-Use Market?

The packaging end-use industry commands approximately 42-46% of plastic upcycling technology market revenue in 2026, reflecting packaging's position as both the largest consumer of plastic globally -- representing approximately 40% of total plastic production -- and the most advanced adopter of upcycled plastic content under regulatory recycled content mandates and brand owner sustainability commitments. The packaging application's upcycled content adoption is driven by the specific and legally binding nature of recycled content requirements -- the EU Packaging Regulation's mandatory minimum recycled content percentages, California AB 793's bottle recycled content mandates, and equivalent requirements across multiple national jurisdictions -- that create non-discretionary procurement demand for upcycled plastics in food and beverage packaging, personal care packaging, household product containers, and industrial packaging. Major packaging converters including Amcor, Berry Global, Sealed Air, Alpla, and Huhtamaki have established substantial recycled content plastic procurement programs and in some cases direct investments in chemical recycling infrastructure to secure supply of high-quality recycled materials meeting their customers' sustainability specifications. The textiles and apparel end-use segment represents the second-largest and fastest-growing application for upcycled plastics, driven by the fashion industry's adoption of rPET fiber from recycled plastic bottles for polyester fabric production -- with brands including Patagonia, H&M, Nike, and Adidas sourcing substantial proportions of polyester fiber from recycled PET -- and emerging chemical recycling-to-fiber pathways converting mixed plastic waste and even worn polyester garments into virgin-equivalent PET fiber bypassing the quality degradation of mechanical textile recycling. The automotive end-use segment is a growing and technically demanding market for upcycled plastics, with automotive OEMs including BMW, Mercedes-Benz, Volkswagen, and Toyota setting ambitious recycled content targets for interior, underhood, and body component applications that mechanical and chemical upcycling technologies must supply with consistent quality and traceability documentation.

How is Europe Maintaining Market Leadership?

Europe holds approximately 36-40% of the global plastic upcycling technology market in 2026, driven by the world's most comprehensive and stringent plastic waste regulatory framework -- the EU Packaging and Packaging Waste Regulation, Single-Use Plastics Directive, Extended Producer Responsibility harmonization, and the European Green Deal's circular economy targets -- that collectively create the strongest regulatory pull for plastic upcycling capacity investment of any global region. The European chemical recycling landscape has attracted the largest concentration of advanced upcycling facility investments globally: Plastic Energy operates commercial pyrolysis facilities in Spain and the UK; Mura Technology is developing a supercritical water pyrolysis plant in Teesside, UK; Carbios is commissioning its first industrial PET enzymatic recycling plant in France in partnership with Indorama Ventures; Renewlysis is developing a chemical recycling facility in the Netherlands; and BASF's ChemCycling program is co-processing pyrolysis oil at Ludwigshafen. Germany's Kreislaufwirtschaftsgesetz (circular economy legislation), France's AGEC law mandating recycled content in plastic products, and the Netherlands' national plastic pact have created national-level regulatory environments that reinforce EU-wide requirements and maintain Europe's leading position in upcycling technology deployment. The UK post-Brexit has maintained alignment with EU plastic waste standards while developing its own Plastic Packaging Tax, Extended Producer Responsibility reform, and planned Deposit Return Scheme that collectively create a comparable regulatory environment to EU member states for upcycling investment purposes.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific demonstrates the highest regional growth rate at approximately 16-18% CAGR, driven by China's post-National Sword domestic recycling infrastructure buildout, Japan and South Korea's advanced technology development programs, and the rapidly increasing awareness and regulatory response to plastic waste accumulation across Southeast Asian coastal nations. China's National Sword policy of 2018 -- banning imports of most plastic waste and raising quality standards for domestic recycling -- triggered a transformation of China's plastic recycling industry from import-dependent processing toward domestic collection, sorting, and upcycling infrastructure investment, with government-supported industrial parks dedicated to plastic recycling and chemical recovery operations being developed in multiple provinces. China's 14th Five-Year Plan explicitly targets increasing plastic waste recycling rates and developing domestic chemical recycling capacity, with state-owned enterprises and private companies including Sinopec, CNOOC, and specialized recyclers investing in pyrolysis and depolymerization capacity. Japan's commitment to plastic resource circulation -- articulated in the Plastic Resource Circulation Act of 2022 requiring businesses to reduce single-use plastic use and expand recycled content -- is driving domestic upcycling technology development, with companies including Teijin (PET chemical recycling), Toray (nylon recycling), and Toyota Tsusho (mixed plastic chemical recycling) developing and deploying domestic upcycling solutions. South Korea's K-REUSE, K-RECYCLE, and Extended Producer Responsibility programs are among the most ambitious in Asia, with recycling rate targets and recycled content requirements creating demand for domestic upcycling capacity serviced by Korean conglomerates including SK Geocentric (formerly SK Global Chemical) which has committed substantial investment in chemical recycling facility development targeting pyrolysis oil production for petrochemical co-processing.

The global plastic upcycling technology market encompasses technology developers, industrial operators, petrochemical integrators, and AI-powered sorting platform companies spanning the full value chain from waste collection through processed output. In chemical recycling technology, Plastic Energy (TACOIL pyrolysis), Mura Technology (HydroPRS), Renewlogy, Brightmark Energy, and Quantafuel are leading pyrolysis operators. PET depolymerization specialists include Carbios (enzymatic, industrial scale), Loop Industries (catalytic depolymerization), Eastman Chemical (Polyester Renewal Technology), Ioniqa Technologies (magnetic catalyst glycolysis), and gr3n (alkaline hydrolysis). Major petrochemical companies integrating chemical recycling include SABIC (TRUCIRCLE), LyondellBasell (Circulen), Dow (recycled content polyethylene), BASF (ChemCycling), Ineos (Project Plastic Road), and Borealis (ReOil). In AI-powered sorting and pre-processing, AMP Robotics, TOMRA Sorting, Steinert, Machinex, and Sesotec provide the automated sorting infrastructure enabling feedstock quality for chemical recycling. Mechanical upcycling technology leaders include Starlinger, Erema Group, Gneuss, and Krones for advanced mechanical recycling equipment with decontamination and compatibilization capability. Biological upcycling companies beyond Carbios include Novamont and Total Energies' bioplastics joint ventures exploring enzyme-enhanced biodegradation pathways. Waste management companies including Veolia, Suez, Biffa, and DSM Venturing provide feedstock supply chain infrastructure and investment capital to the sector.

The global plastic upcycling technology market is expected to grow from USD 5.27 billion in 2026 to USD 18.43 billion by 2036.

The global plastic upcycling technology market is projected to grow at a CAGR of 13.3% from 2026 to 2036.

Chemical recycling dominates representing approximately 48-52% of revenue through pyrolysis, gasification, solvolysis, and depolymerization technologies capable of processing contaminated and mixed plastic streams. Enzymatic depolymerization demonstrates the fastest growth driven by Carbios's commercial breakthrough for PET upcycling enabling virgin-equivalent monomer recovery from post-consumer packaging at industrial scale.

Engineered thermostable PETase enzymes -- particularly Carbios's leaf-branch compost cutinase variant achieving 90% PET depolymerization within 10 hours at 72 degrees Celsius -- enable selective depolymerization of contaminated and mixed PET waste into virgin-equivalent TPA and EG monomers, with Carbios licensing the technology to major PET producers including Indorama Ventures representing 12 million tonnes per year of global PET production capacity.

Europe leads with approximately 36-40% of global market driven by the world's most comprehensive plastic waste regulatory framework including the EU Packaging and Packaging Waste Regulation's mandatory recycled content requirements and the highest concentration of operational advanced chemical recycling facilities. Asia-Pacific demonstrates the fastest growth at 16-18% CAGR driven by China's post-National Sword domestic infrastructure buildout, Japan's Plastic Resource Circulation Act, and South Korea's SK Geocentric chemical recycling investment.

The leading companies include Plastic Energy, Mura Technology, Carbios, Loop Industries, Eastman Chemical, Ioniqa Technologies, SABIC, LyondellBasell, Dow, BASF, Borealis, AMP Robotics, TOMRA, Erema Group, and Starlinger -- spanning pyrolysis operators, PET depolymerization specialists, petrochemical integrators, AI sorting platform providers, and mechanical upcycling equipment manufacturers.

Published Date: Apr-2026

Published Date: Dec-2025

Published Date: May-2024

Published Date: Aug-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates