Resources

About Us

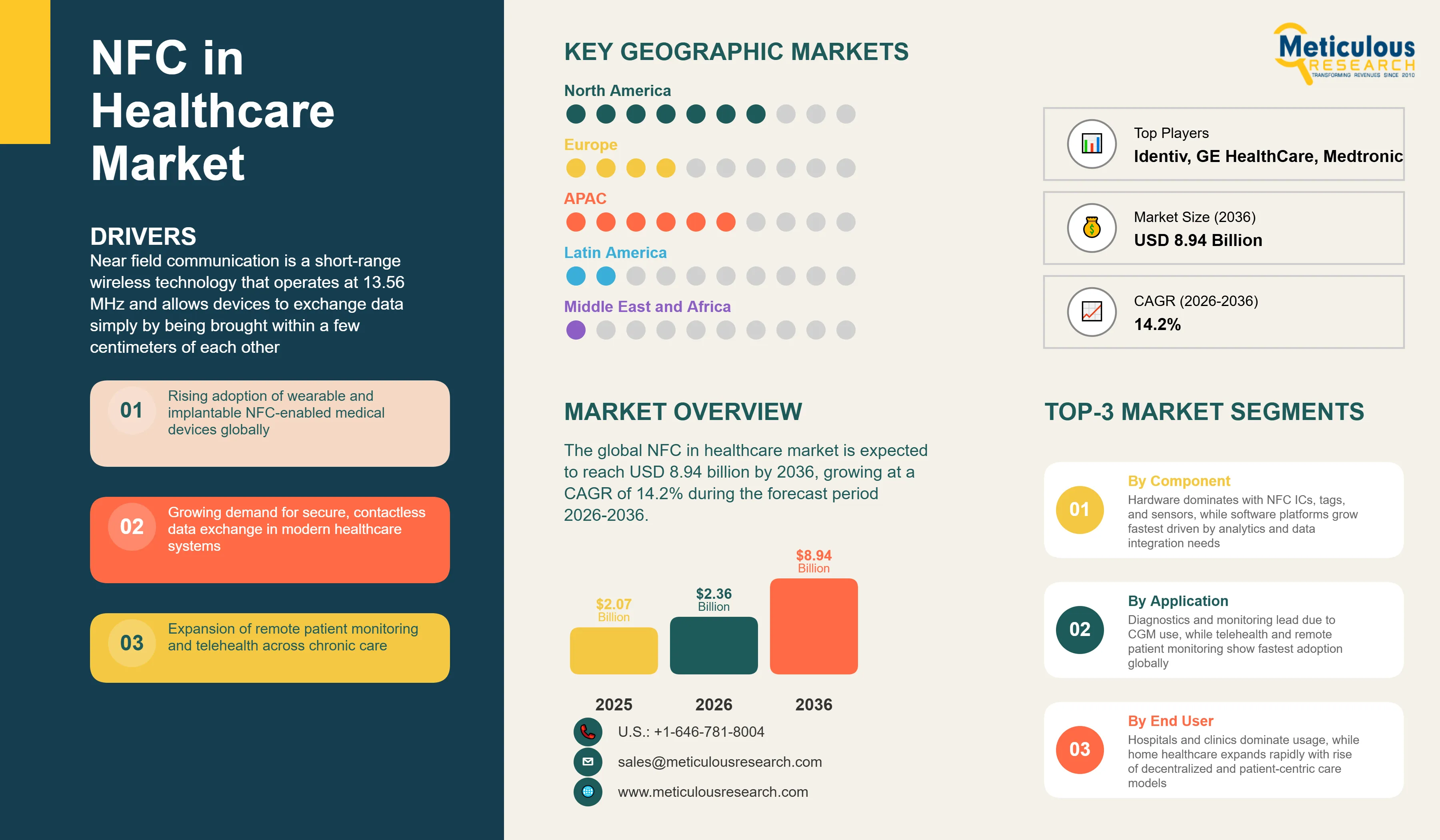

The global NFC in healthcare market was valued at USD 2.07 billion in 2025. This market is expected to reach USD 8.94 billion by 2036 from an estimated USD 2.36 billion in 2026, growing at a CAGR of 14.2% during the forecast period 2026-2036. Near field communication technology, which enables two-way wireless data exchange over distances of a few centimeters, is transforming how patient data is collected, how medical devices communicate, and how medications are tracked in healthcare settings where contactless, secure, and battery-independent data transmission has compelling operational and clinical advantages.

Click here to: Get Free Sample Pages of this Report

Near field communication is a short-range wireless technology that operates at 13.56 MHz and allows devices to exchange data simply by being brought within a few centimeters of each other. In healthcare, NFC enables a wide range of applications, from a nurse tapping a smartphone against a patient wristband to retrieve medical records, to a continuous glucose monitor patch transmitting blood sugar readings to a smartphone without needing a battery in the patch itself. Passive NFC tags can be powered entirely by the electromagnetic field from a reader device, making them suitable for small disposable medical sensors, smart medication packaging, and patient identification bands that require no onboard power. Active NFC systems in medical devices enable two-way communication with smartphones and hospital IT systems, creating a seamless data bridge between the patient and the electronic health record.

The market is growing because healthcare is experiencing a broad shift toward digitization, decentralization, and continuous monitoring that NFC's specific properties are well-suited to enable. The COVID-19 pandemic demonstrated the value of contactless interaction in clinical settings, and the operational advantages of NFC over alternatives including Bluetooth in terms of zero pairing requirement, instant data transfer, and passive operation have sustained clinical adoption well beyond the pandemic period. According to the International Diabetes Federation's Diabetes Atlas 2025, approximately 11.1% of adults worldwide are living with diabetes, and the continuous glucose monitoring market serving this population is one of the most commercially active adoption channels for NFC-enabled medical sensors.

Two growth opportunities are defining the technology's next phase. Abbott's FreeStyle Libre continuous glucose monitoring system, which uses NFC to transmit glucose readings from a wearable sensor to a smartphone or dedicated reader, reported global FreeStyle Libre sales of approximately USD 1.8 billion in Q4 2024 according to Abbott's 2025 financial results, making it the world's largest single NFC-enabled healthcare product and a powerful proof-of-concept for the commercial potential of NFC in continuous health monitoring. The second opportunity is NFC-enabled implantable biosensors, where research programs at multiple academic and commercial organizations are developing subcutaneous sensors for continuous biomarker monitoring that communicate data wirelessly through the skin to an external reader, removing the need for any transcutaneous connections or battery replacement.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 8.94 Billion |

|

Market Size in 2026 |

USD 2.36 Billion |

|

Market Size in 2025 |

USD 2.07 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 14.2% |

|

Dominating Component |

Hardware (NFC ICs and Chipsets) |

|

Fastest Growing Component |

Software (Data Analytics Platforms) |

|

Dominating Device Type |

Wearable Devices |

|

Fastest Growing Device Type |

Implantable Devices |

|

Dominating Sensor Type |

Biosensors |

|

Fastest Growing Sensor Type |

Chemical Sensors (Glucose Monitoring) |

|

Dominating Application |

Diagnostics & Monitoring |

|

Fastest Growing Application |

Remote Patient Monitoring & Telehealth |

|

Dominating End User |

Hospitals and Clinics |

|

Fastest Growing End User |

Home Healthcare |

|

Dominating Deployment Mode |

Cloud-Based Systems |

|

Fastest Growing Deployment Mode |

Cloud-Based Systems |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Abbott FreeStyle Libre Demonstrating the Commercial Scale of NFC Health Monitoring

The commercial success of Abbott's FreeStyle Libre continuous glucose monitoring system is the most important single reference point for the commercial potential of NFC in healthcare, demonstrating that consumers and clinicians will enthusiastically adopt NFC-based health monitoring when the product delivers genuinely better experience and outcomes than the alternatives it replaces. The FreeStyle Libre sensor is worn on the upper arm for up to 14 days and reads glucose continuously using a small biosensor in contact with interstitial fluid, transmitting readings to a smartphone running the LibreLink app or a dedicated reader via NFC with a simple one-second scan. According to Abbott's 2025 Annual Report, the FreeStyle Libre franchise generated approximately USD 1.8 billion in revenues in Q 4 2024, representing approximately 16% of Abbott's total revenues, and is one of the company's fastest-growing product lines.

The Libre's success has proven several commercially important points about NFC in healthcare: consumers are willing to wear a sensor continuously when it replaces painful finger-prick testing; NFC data transfer is sufficiently fast, reliable, and user-friendly for frequent clinical use; and the integration of NFC-enabled sensor data with smartphone apps and cloud platforms creates genuine clinical value by enabling continuous trend monitoring rather than point-in-time measurements. These lessons from the CGM market are directly informing the development of NFC-enabled sensors for other biomarkers including blood pressure, cardiac rhythms, and metabolic parameters, expanding the addressable market for NFC healthcare technology well beyond glucose monitoring.

Smart Medical Packaging Using NFC for Medicine Authentication and Patient Safety

The pharmaceutical industry is increasingly deploying NFC tags in medication packaging for multiple functions including counterfeit authentication, smart adherence monitoring, cold chain tracking, and direct patient information access. A patient who taps an NFC-equipped medication box with their smartphone can instantly retrieve dosing instructions in their language, confirm the medication is authentic, check the expiration date, and log the administration time in a connected medication management app. In clinical settings, NFC-tagged unit-dose packaging can support bedside verification of the right drug for the right patient with a simple tap, helping reduce medication administration errors. WHO has identified medication errors as a major cause of preventable harm worldwide.

NXP Semiconductors, a world leader in NFC semiconductor solutions, has specifically targeted the pharmaceutical and healthcare packaging market with its NFC tag product lines, reporting growing demand from pharmaceutical companies deploying NFC for track-and-trace and patient engagement applications. According to NXP's 2025 investor communications, healthcare and pharmaceutical applications represent a growing segment of its NFC IC shipments, driven by both regulatory pressure to improve medication safety and by pharmaceutical companies' desire to build direct digital connections with patients and healthcare providers through smart packaging. The EU's Falsified Medicines Directive, which requires serialization and authentication of prescription medicines, is creating a policy driver for digital authentication technologies in pharmaceutical packaging that NFC is well-positioned to address.

Smartphone NFC Penetration Creating a Universal Healthcare Reader Platform

One of the most commercially important infrastructure developments for NFC in healthcare is the near-universal availability of NFC readers in modern smartphones, which means that the reader hardware for NFC-based healthcare applications is already in the pocket of most patients and healthcare workers without any additional device investment. According to Omdia smartphone preliminary shipment report, global smartphone shipments were about 1.22 billion units in 2024, and NFC adoption continues to expand as more consumers use smartphones or smartwatches for contactless payments.

This ubiquity of NFC reader capability fundamentally changes the economics of NFC healthcare applications. A hospital deploying NFC patient wristbands for identification does not need to invest in dedicated readers at every point of care because nurses' and physicians' existing smartphones already have NFC capability. A pharmaceutical company deploying NFC smart packaging does not need to provide patients with a dedicated reader device because the patients' existing smartphones can read the tags. This infrastructure leverage dramatically reduces the total cost of NFC healthcare deployment compared with proprietary wireless systems and is one of the primary reasons for NFC's growing adoption advantage over competing short-range wireless technologies in consumer-facing healthcare applications.

Growth of Wearable and Implantable Medical Devices

The wearable medical device market is one of the most rapidly growing segments of the broader medical technology industry, and NFC is increasingly the preferred wireless connectivity protocol for wearable health sensors because of its battery-independent passive operation and its zero-pairing instant data transfer characteristics. Abbott's FreeStyle Libre, reporting approximately USD 1.8 billion in Q 4 2024 revenues per its 2025 Annual Report, is the commercial anchor of the NFC wearable medical device market and the proof point that NFC-connected biosensors can achieve mass-market consumer adoption at the billion-dollar scale.

Expansion of Remote Patient Monitoring & Telehealth

The telehealth and remote patient monitoring market expanded substantially during the COVID-19 pandemic and has retained a substantially larger patient and provider base than existed before 2020. According to the American Hospital Association's 2025 data, telehealth utilization in the U.S. remained at levels many times higher than pre-pandemic baselines, with chronic disease management and post-acute care representing the highest-volume telehealth use cases. NFC-enabled devices are well-positioned for remote monitoring because they combine continuous sensor operation in the patient's home with a simple smartphone tap to upload accumulated data to the clinical team's patient monitoring platform, requiring no technical expertise from the patient and generating structured data that integrates directly with electronic health record systems. The International Diabetes Federation's 2025 Diabetes Atlas projecting over 600 million diabetes patients globally by 2045 indicates the long-term scale of the chronic disease monitoring market that NFC-enabled remote monitoring is increasingly serving.

NFC-Based Biosensors and Smart Patches

NFC-based smart patches and biosensors represent one of the most commercially compelling near-term growth opportunities in the healthcare NFC market, combining the proven NFC connectivity platform with new generations of flexible, skin-conformable biosensor electronics that can monitor an expanding range of biomarkers continuously and non-invasively. Research groups at MIT, EPFL, and several commercial companies are developing NFC-powered patches that can simultaneously monitor glucose, lactate, pH, sweat electrolytes, and skin temperature, transmitting this multi-parameter data to a smartphone with a single tap. The commercial pathway from research to clinical product is becoming shorter as flexible electronics manufacturing, biochemical sensor fabrication, and NFC IC integration are all maturing simultaneously. Companies including Gentag and Grapheal have disclosed commercial NFC biosensor patch development programs targeting wound monitoring, glucose monitoring, and general wellness applications, indicating the growing commercial pipeline in this segment.

Smartphone-Based Diagnostics

The combination of NFC-enabled point-of-care diagnostic cartridges with smartphone reader platforms is creating a new category of distributed diagnostics that can deliver laboratory-quality test results outside the laboratory without requiring dedicated reader instruments. An NFC diagnostic test cartridge performs the biochemical assay autonomously after sample application and then communicates the quantitative result to the user's smartphone via NFC when tapped, which transmits the result to the patient's healthcare provider via the cloud. This architecture eliminates the need for a dedicated benchtop reader, reducing the capital cost of point-of-care testing deployment significantly and enabling deployment in pharmacy, home, and community settings where a traditional reader instrument would be impractical. The COVID-19 pandemic's rapid expansion of home diagnostic testing demonstrated consumer willingness to perform self-tests, and the NFC smartphone platform is well-positioned to extend this direct-to-consumer diagnostic model to a broader range of biomarkers in the coming years.

By Component: In 2026, Hardware to Hold the Largest Share

Based on component, the global NFC in healthcare market is segmented into hardware (NFC ICs and chipsets, NFC tags and readers, sensor-integrated NFC modules, antennas and flexible electronics), software (NFC communication software, data analytics platforms, security and encryption software), and services (integration and deployment, maintenance and support, data management services). In 2026, the hardware segment is expected to account for the largest share of the global NFC in healthcare market. NFC semiconductor ICs, tags, and sensor-integrated modules are the physical enablers of every NFC healthcare application and represent the largest procurement category by value, anchored by the large volumes of NFC chipsets consumed by the continuous glucose monitoring and wearable biosensor markets. NXP Semiconductors and STMicroelectronics are the world's leading NFC IC suppliers and serve both consumer NFC and healthcare-specific NFC applications.

However, the software segment, particularly data analytics platforms, is projected to register the highest CAGR during the forecast period. As NFC-enabled health sensor deployments scale up and generate large volumes of continuous physiological data, the value of analytics platforms that can process, visualize, and generate clinical insights from this data is growing rapidly. Healthcare providers and digital health companies are increasingly adopting subscription analytics platforms that convert raw NFC sensor data into actionable clinical guidance, creating a high-margin recurring revenue software stream that is growing faster than the underlying hardware market.

By Device Type: In 2026, Wearable Devices to Hold the Largest Share

Based on device type, the global NFC in healthcare market is segmented into wearable devices (smart patches and smartwatches/fitness bands), implantable devices (biosensors and drug delivery systems), handheld diagnostic devices, and smart medical packaging. In 2026, the wearable devices segment is expected to account for the largest share of the global NFC in healthcare market. The continuous glucose monitoring market anchored by Abbott's FreeStyle Libre, which uses NFC-enabled skin-worn sensor patches, drives the majority of NFC wearable medical device revenue and provides the commercial scale reference for this segment. The broader wearable biosensor market is rapidly adding additional parameters to NFC-connected wearable platforms, expanding the total addressable market beyond glucose monitoring.

However, the implantable devices segment is projected to register the highest CAGR during the forecast period. NFC-enabled implantable biosensors that can transmit data from beneath the skin to an external reader without transcutaneous connections represent a significant clinical improvement over current implantable sensor approaches and are attracting growing research and commercial investment. Medtronic's work on NFC-enabled implantable cardiac monitors and several academic and startup programs developing NFC-powered subcutaneous biosensors represent the leading edge of this segment's commercial development.

By Application: In 2026, Diagnostics and Monitoring to Hold the Largest Share

Based on application, the global NFC in healthcare market is segmented into diagnostics and monitoring (point-of-care diagnostics and chronic disease monitoring), patient identification and tracking, medication management, remote patient monitoring and telehealth, and asset and inventory management. In 2026, the diagnostics and monitoring segment is expected to account for the largest share of the global NFC in healthcare market. Continuous glucose monitoring and other NFC-enabled biosensor applications for chronic disease monitoring generate the highest total NFC healthcare revenue, driven by the very large and growing diabetes patient population and the premium pricing of CGM systems relative to traditional monitoring approaches. The point-of-care diagnostics subcategory is also growing rapidly as NFC-connected test cartridges reduce the infrastructure requirements for bedside and home-based testing.

However, the remote patient monitoring and telehealth segment is projected to register the highest CAGR during the forecast period. The sustained high levels of telehealth utilization, combined with the growing clinical evidence that continuous remote monitoring improves outcomes in chronic disease management, is driving healthcare providers and payers to invest in NFC-enabled RPM programs. The International Diabetes Federation's 2025 Diabetes Atlas projecting global diabetes prevalence reaching over 853 million by 2050 represents the long-term patient population growth that will sustain remote monitoring demand.

NFC in Healthcare Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global NFC in healthcare market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global NFC in healthcare market. The United States has the world's most advanced digital health ecosystem, the highest per-capita healthcare spending, and the largest domestic commercial deployment of NFC-enabled continuous glucose monitors anchored by Abbott's FreeStyle Libre and Dexcom's competing CGM systems. The U.S. FDA's digital health policy framework, which has developed specific regulatory pathways for software as a medical device and NFC-enabled diagnostics, provides regulatory clarity that enables faster product commercialization than most other markets. The U.S. Centers for Medicare and Medicaid Services has expanded reimbursement coverage for CGM devices in recent years, according to the American Diabetes Association's 2025 Standards of Medical Care, making continuous NFC-enabled glucose monitoring financially accessible to a broader population of Medicare beneficiaries. The very large U.S. diabetes population, the American Hospital Association's data showing sustained high telehealth adoption, and the presence of leading NFC semiconductor companies including NXP, Texas Instruments, and Analog Devices collectively make North America the dominant regional market.

However, the Asia-Pacific NFC in healthcare market is expected to grow at the fastest CAGR during the forecast period. The region contains the two largest national diabetes populations globally: the International Diabetes Federation's 2025 Atlas identifies China at approximately 148 million and India at approximately 90 million adult patients, creating enormous demand for affordable continuous monitoring solutions. China's digital health transformation, accelerated by government investment in healthcare digitalization and the very high smartphone penetration that provides the NFC reader infrastructure for patient-facing applications, is creating rapid adoption of digital health technologies including NFC-enabled wearables. Japan's aging population, with over 29% of residents aged 65 and above according to Japan's Statistics Bureau 2025 data, creates growing demand for remote monitoring solutions that NFC-enabled wearables are well-positioned to serve. South Korea's advanced digital health infrastructure, high NFC-capable smartphone penetration, and sophisticated health technology industry including Samsung's semiconductor and healthcare businesses, and Singapore's position as Asia's most advanced digital health hub, add to the region's growth momentum.

The NFC in healthcare market is served by semiconductor companies that provide the NFC IC and chipset foundation for all applications, medical device companies that integrate NFC into clinical products, digital health platform companies that build the software and analytics layer, and specialist identification and tracking technology companies serving hospital operations. Competition is based on NFC IC performance specifications including read range, data transfer speed, and power consumption, the degree of medical-grade compliance and biocompatibility of device-integrated NFC systems, software platform capabilities for data management and clinical analytics, and the strength of healthcare channel and regulatory approval relationships.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, healthcare customer relationships, geographic presence, and recent strategic developments. Some of the key players operating in the global NFC in healthcare market include NXP Semiconductors N.V. (Netherlands), STMicroelectronics N.V. (Switzerland/France), Infineon Technologies AG (Germany), Analog Devices Inc. (U.S.), Texas Instruments Incorporated (U.S.), Medtronic plc (Ireland), Abbott Laboratories (U.S.), Philips Healthcare (Netherlands), GE HealthCare (U.S.), Siemens Healthineers AG (Germany), Sony Semiconductor Solutions Corporation (Japan), ams-OSRAM AG (Austria), Identiv Inc. (U.S.), HID Global Corporation (U.S.), Silicon Craft Technology PLC (Thailand), Zebra Technologies Corporation (U.S.), and many others.

The global NFC in healthcare market is expected to reach USD 8.94 billion by 2036 from an estimated USD 2.36 billion in 2026, at a CAGR of 14.2% during the forecast period 2026-2036.

In 2026, the hardware segment is expected to hold the largest share of the global NFC in healthcare market, driven by NFC ICs, chipsets, and sensor-integrated modules being the physical foundation of every NFC healthcare application and representing the highest procurement value across the continuous glucose monitoring and wearable biosensor markets.

The software segment, particularly data analytics platforms, is projected to register the highest CAGR during the forecast period, driven by the growing need to extract actionable clinical insights from the large volumes of continuous physiological data generated by NFC-enabled health sensors deployed at scale.

In 2026, the diagnostics and monitoring segment is expected to hold the largest share of the global NFC in healthcare market, anchored by continuous glucose monitoring and other NFC-enabled biosensor applications for chronic disease monitoring that generate the highest recurring revenue per patient of any NFC healthcare application.

The home healthcare segment is projected to register the highest CAGR during the forecast period, driven by the sustained expansion of remote patient monitoring and the growing clinical and payer preference for managing chronic diseases in home settings using NFC-enabled wearable sensors that transmit data to care teams digitally.

The market is primarily driven by the rapid commercial success of NFC-enabled continuous glucose monitoring, most notably Abbott's FreeStyle Libre franchise, which has demonstrated the patient and clinical acceptance of NFC-based continuous health monitoring at commercial scale, combined with the near-universal availability of NFC readers in modern smartphones that eliminates the need for dedicated reader hardware in patient-facing applications.

Key players are NXP Semiconductors N.V. (Netherlands), STMicroelectronics N.V. (Switzerland/France), Infineon Technologies AG (Germany), Analog Devices Inc. (U.S.), Texas Instruments Incorporated (U.S.), Medtronic plc (Ireland), Abbott Laboratories (U.S.), Philips Healthcare (Netherlands), GE HealthCare (U.S.), Siemens Healthineers AG (Germany), Sony Semiconductor Solutions Corporation (Japan), ams-OSRAM AG (Austria), Identiv Inc. (U.S.), HID Global Corporation (U.S.), Silicon Craft Technology PLC (Thailand), and Zebra Technologies Corporation (U.S.), among others.

Asia-Pacific is expected to register the highest growth rate in the global NFC in healthcare market during the forecast period 2026-2036, driven by the very large and growing diabetes patient populations in China and India, rapidly expanding digital health infrastructure and smartphone NFC penetration, and government-driven healthcare digitalization programs across Japan, South Korea, and Singapore.

1. Introduction

1.1. Market Definition

1.2. Scope

1.3. Market Ecosystem

1.4. Currency and Limitations

1.4.1. Currency

1.4.2. Limitations

1.5. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research & Validation

2.2.2.1. Primary Interviews (OEMs, Hospitals, Sensor Developers)

2.2.2.2. Country-Level Analysis Approach

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Growth of Wearable and Implantable Medical Devices

4.2.1.2. Increasing Demand for Contactless and Secure Data Exchange

4.2.1.3. Expansion of Remote Patient Monitoring & Telehealth

4.2.1.4. Rising Adoption of Smart Diagnostics and Point-of-Care Testing

4.2.2. Restraints

4.2.2.1. Limited Communication Range

4.2.2.2. Integration Complexity with Medical Systems

4.2.2.3. Regulatory Approval Challenges

4.2.3. Opportunities

4.2.3.1. NFC-Based Biosensors and Smart Patches

4.2.3.2. Growth in Implantable and Flexible Electronics

4.2.3.3. Smartphone-Based Diagnostics

4.2.3.4. Smart Drug Delivery Systems

4.2.4. Challenges

4.2.4.1. Data Privacy and Security Compliance

4.2.4.2. Power Constraints in Passive NFC Devices

4.3. Technology Landscape

4.3.1. NFC Chipsets and Tags

4.3.2. NFC Sensor Interfaces (Analog Front-End Integration)

4.3.3. Passive vs Active NFC Systems

4.3.4. Flexible & Biocompatible Electronics

4.3.5. Integration with IoT and Mobile Platforms

4.4. NFC Healthcare Architecture (System View)

4.4.1. NFC Sensors (Physical, Chemical, Biosensors)

4.4.2. NFC Tag/Reader Interface

4.4.3. Mobile Devices (Smartphones/Tablets)

4.4.4. Cloud & Healthcare IT Systems (EHR/EMR)

4.4.5. AI & Analytics Platforms

4.5. Value Chain Analysis

4.5.1. Semiconductor & NFC Chip Providers

4.5.2. Sensor & Medical Device Manufacturers

4.5.3. System Integrators

4.5.4. Healthcare Providers

4.5.5. Digital Health Platforms

4.6. Regulatory and Standards Landscape

4.6.1. Medical Device Regulations (FDA, CE)

4.6.2. Data Privacy (HIPAA, GDPR)

4.6.3. Wireless Communication Standards

4.7. Industry Trends

4.7.1. Growth of Wearable Biosensors

4.7.2. Rise of Decentralized Healthcare

4.7.3. Integration with AI Diagnostics

4.7.4. Smart Hospitals and Digital Health Ecosystems

4.8. Cost and Pricing Analysis

4.8.1. Cost of NFC Modules and Sensors

4.8.2. Integration Costs in Medical Devices

4.8.3. Pricing Models (Device + Platform)

5. NFC in Healthcare Market, by Component

5.1. Introduction

5.2. Hardware

5.2.1. NFC ICs and Chipsets

5.2.2. NFC Tags and Readers

5.2.3. Sensor-Integrated NFC Modules

5.2.4. Antennas and Flexible Electronics

5.3. Software

5.3.1. NFC Communication Software

5.3.2. Data Analytics Platforms

5.3.3. Security & Encryption Software

5.4. Services

5.4.1. Integration and Deployment

5.4.2. Maintenance and Support

5.4.3. Data Management Services

6. NFC in Healthcare Market, by Device Type

6.1. Introduction

6.2. Wearable Devices

6.2.1. Smart Patches

6.2.2. Smartwatches & Fitness Bands

6.3. Implantable Devices

6.3.1. Biosensors

6.3.2. Drug Delivery Systems

6.4. Handheld Diagnostic Devices

6.5. Smart Medical Packaging

7. NFC in Healthcare Market, by Sensor Type

7.1. Introduction

7.2. Physical Sensors

7.2.1. Temperature Sensors

7.2.2. Pressure Sensors

7.3. Chemical Sensors

7.3.1. Glucose Monitoring

7.3.2. Electrolyte Detection

7.4. Biosensors

7.4.1. Heart Rate Monitoring

7.4.2. Biomarker Detection

7.5. Multi-Parameter Sensors

8. NFC in Healthcare Market, by Application

8.1. Introduction

8.2. Diagnostics & Monitoring

8.2.1. Point-of-Care Diagnostics

8.2.2. Chronic Disease Monitoring

8.3. Patient Identification & Tracking

8.4. Medication Management

8.5. Remote Patient Monitoring & Telehealth

8.6. Asset & Inventory Management

9. NFC in Healthcare Market, by End User

9.1. Hospitals and Clinics

9.2. Diagnostic Laboratories

9.3. Home Healthcare

9.4. Pharmaceutical Companies

9.5. Research Institutes

10. NFC in Healthcare Market, by Deployment Mode

10.1. On-Premise Systems

10.2. Cloud-Based Systems

11. NFC in Healthcare Market, by Geography

11.1. Introduction

11.2. North America

11.2.1. U.S.

11.2.2. Canada

11.3. Europe

11.3.1. Germany

11.3.2. United Kingdom

11.3.3. France

11.3.4. Italy

11.3.5. Spain

11.3.6. Netherlands

11.3.7. Sweden

11.3.8. Switzerland

11.3.9. Rest of Europe

11.4. Asia-Pacific

11.4.1. China

11.4.2. Japan

11.4.3. South Korea

11.4.4. India

11.4.5. Australia

11.4.6. Singapore

11.4.7. Thailand

11.4.8. Vietnam

11.4.9. Indonesia

11.4.10. Rest of Asia-Pacific

11.5. Latin America

11.5.1. Brazil

11.5.2. Mexico

11.5.3. Argentina

11.5.4. Chile

11.5.5. Colombia

11.5.6. Rest of Latin America

11.6. Middle East & Africa

11.6.1. UAE

11.6.2. Saudi Arabia

11.6.3. South Africa

11.6.4. Israel

11.6.5. Turkey

11.6.6. Rest of Middle East & Africa

12. Competitive Landscape

12.1. Overview

12.2. Key Growth Strategies

12.3. Competitive Benchmarking

12.4. Competitive Dashboard

12.4.1. Industry Leaders

12.4.2. Market Differentiators

12.4.3. Vanguards

12.4.4. Emerging Companies

12.5. Market Ranking/Positioning Analysis, 2025

13. Company Profiles

(Business Overview, Financials, Product Portfolio, Strategic Developments, SWOT)

13.1. NXP Semiconductors N.V.

13.2. STMicroelectronics N.V.

13.3. Infineon Technologies AG

13.4. Analog Devices, Inc.

13.5. Texas Instruments Incorporated

13.6. Medtronic plc

13.7. Abbott Laboratories

13.8. Philips Healthcare

13.9. GE HealthCare

13.10. Siemens Healthineers AG

13.11. Sony Semiconductor Solutions Corporation

13.12. ams-OSRAM AG

13.13. Identiv, Inc.

13.14. HID Global Corporation

13.15. Silicon Craft Technology PLC

13.16. Zebra Technologies Corporation

13.17. Other Companies

14. Appendix

14.1. Additional Customization

14.2. Related Reports

Published Date: Feb-2026

Published Date: Jan-2025

Published Date: Aug-2024

Subscribe to get the latest industry updates