Resources

About Us

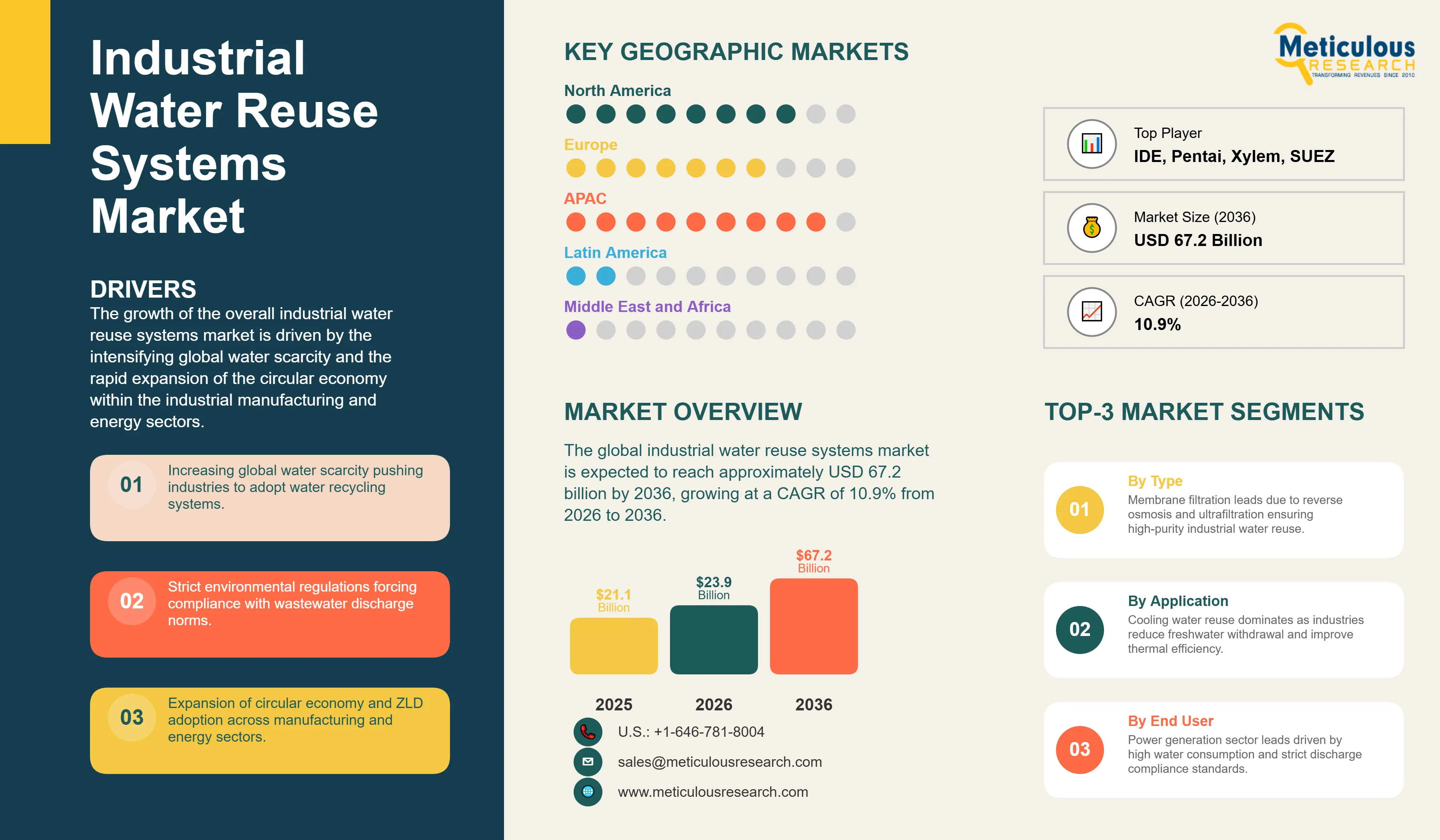

The global industrial water reuse systems market was valued at USD 21.1 billion in 2025. The market is expected to reach approximately USD 67.2 billion by 2036 from USD 23.9 billion in 2026, growing at a CAGR of 10.9% from 2026 to 2036. The growth of the overall industrial water reuse systems market is driven by the intensifying global water scarcity and the rapid expansion of the circular economy within the industrial manufacturing and energy sectors. As manufacturers seek to integrate more sustainable water management into their production lifecycles and address stringent environmental regulations, advanced digital reuse systems have become essential for maintaining compliance and operational durability of the global industrial value chain. The rapid expansion of the membrane infrastructure and the increasing need for high-performance water purification systems like ZLD (Zero Liquid Discharge) and AI-integrated treatment registries continue to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Industrial water reuse systems are critical digital and mechanical setups used to provide lifecycle traceability for water resources while allowing for material recovery and sustainability reporting throughout the industrial operational lifespan. These systems include filtration platforms, integrated sensors, and auditing services, which are designed to withstand supply chain complexities and fit into diverse manufacturing regimens. The market is defined by high-efficiency technologies such as reverse osmosis and IoT-enabled digital twins, which significantly enhance water integrity and signal performance in circular economy applications. These systems are indispensable for manufacturers seeking to optimize their internal resource architecture and meet aggressive carbon and water footprint reduction targets.

The market includes a diverse range of solutions, ranging from simple filtration platforms for basic compliance to complex multilayer recycling systems for high-performance resource management and zero liquid discharge optimization. These systems are increasingly integrated with advanced components such as real-time health monitoring and automated chemical accounting to provide services such as predictive maintenance and improved recovery efficiency. The ability to provide stable, high-precision results while minimizing resource leakage has made advanced water reuse systems the technology of choice for industries where regulatory efficiency and reliability are paramount.

The global industrial sector is pushing hard to modernize production capabilities, aiming to meet net-zero targets and personalized sustainability goals. This drive has increased the adoption of high-density data concentrations, with advanced molecular defense techniques helping to stabilize production yields for ultra-fine chemical processes. At the same time, the rapid growth in the food & beverage and pharmaceutical markets is increasing the need for high-reliability, clinically-proven purification solutions.

Proliferation of AI-Enabled Treatment and Molecular Defense

Manufacturers across the water industry are rapidly shifting to science-optimized reuse, moving well beyond traditional chemical-based documentation toward high-speed, low-friction digital setups. Veolia’s latest AI-driven platforms deliver significantly higher water rejuvenation for aging industrial fleets, while Xylem’s recent installations have slashed visible data gaps in resource audits. The real game-changer comes with “smart” reuse systems featuring integrated molecular defense capabilities that maintain peak performance even in environmentally noisy regulatory environments. These advancements make high-precision reuse practical and cost-effective for everyone from small-scale factories to global petrochemical giants chasing aesthetic excellence and lower system footprint.

Innovation in Modular and Ultra-Thin Filtration Systems

Innovation in modular and ultra-thin filtration systems is rapidly driving the industrial water reuse market, as treatment devices become more compact and multi-functional. Equipment suppliers are now designing units that combine the structural integrity of traditional treatment plants with the versatility of containerized reuse in a single assembly, saving valuable hardware space and simplifying plant logistics. These systems often involve advanced encapsulation and time-release data technology capable of handling ultra-fine performance metrics without compromising data strength or clinical reliability.

At the same time, growing focus on sustainable energy is pushing manufacturers to develop water reuse solutions tailored to circular economy principles. These systems help reduce resource waste through optimized recovery processes and the use of biodegradable digital substrates. By combining high-density resource delivery with robust environmental performance, these new designs support both technological advancement and corporate sustainability, strengthening the resilience of the broader industrial value chain.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 67.2 Billion |

|

Market Size in 2026 |

USD 23.9 Billion |

|

Market Size in 2025 |

USD 21.5 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 10.9% |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Technology, Application, End-use Industry, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Regulatory Mandates and Rise of Circular Economy

A key driver of the industrial water reuse systems market is the rapid movement of the global industrial industry toward science-backed, highly functional sustainability. Global consumer demand for sleek product designs, effective recycling results, and health-monitoring production has created significant incentives for the adoption of water reuse systems. The trend toward “clean” technology and the integration of water into daily wellness patches drive manufacturers toward scalable solutions that reuse systems can uniquely provide. It is estimated that as consumer adoption of circular economy routines rises and diagnostic tools become more decentralized through 2036, the need for robust, effective reuse increases significantly; therefore, technology and targeted services, with their ability to ensure high-density resource delivery, are considered a crucial enabler of modern industrial design strategies.

Opportunity: Gigafactory Expansion and Zero Liquid Discharge Optimization

The rapid growth of the gigafactory market and zero liquid discharge (ZLD) technologies provides great opportunities for the industrial water reuse systems market. Indeed, the global surge in battery and chemical production has created a compelling demand for systems that can replace traditional discharge disposal and integrate seamlessly into digital asset models. These applications require high reliability, resource transparency, and the ability to handle high-volume manufacturing environments, all attributes that are met with advanced digital solutions. The ZLD market is set to expand significantly through 2036, with water reuse systems poised for an expanding share as manufacturers seek to maximize consumer loyalty and minimize resource waste. Furthermore, the increasing demand for AI-driven health analysis and virtual try-on tools for recycled water is stimulating demand for modular reuse solutions that provide high-speed results and design flexibility.

Why Do Membrane Filtration Systems Lead the Market?

The membrane filtration segment accounts for a significant portion of the overall industrial water reuse systems market in 2026. This is mainly attributed to the versatile use of this technology in supporting daily industrial mobility and complex resource protection within extremely diverse environments, such as in urban centers and high-altitude regions. These systems offer the most comprehensive way to ensure water integrity across diverse high-frequency applications. The reverse osmosis and ultrafiltration sectors alone consume a large share of water reuse system production, with major projects in Asia-Pacific and North America demonstrating the technology’s capability to handle high-density resource requirements. However, the biological treatment and AOP segments are expected to grow at a rapid CAGR during the forecast period, driven by the growing need for robust treatment in next-generation chemistries, clinical procedures, and luxury industrial systems.

How Does the Cooling Water Segment Dominate?

Based on application, the cooling water reuse segment holds the largest share of the overall market in 2026. This is primarily due to the massive volume of thermal energy production and the rigorous performance standards required for modern industrial systems. Current large-scale manufacturing plants are increasingly specifying high-density reuse integrations to ensure compliance with global performance standards and consumer expectations for faster, visible sustainability results.

The process water reuse segment is expected to witness the fastest growth during the forecast period. The shift toward high-purity industrial cycles and the complexity of decentralized resource suites are pushing the requirement for advanced reuse systems that can handle varied load types and mechanical stresses while ensuring absolute reliability for safety-critical industrial systems.

How is Asia-Pacific Maintaining Dominance in the Global Industrial Water Reuse Systems Market?

Asia-Pacific holds the largest share of the global industrial water reuse systems market in 2026. The largest share of this region is primarily attributed to the massive industrial push and the presence of the world’s most advanced manufacturing hubs, particularly in China, India, and Japan. China alone accounts for a significant portion of global water reuse system production, with its position as a leading exporter of high-end industrial technology driving sustained growth. The presence of leading manufacturers like Kurita and a well-developed digital supply chain provides a robust market for both standard and high-density reuse solutions.

Which Factors Support North America and Europe Market Growth?

North America and Europe together account for a substantial share of the global industrial water reuse systems market. The growth of these markets is mainly driven by the need for technological modernization in the chemical, pharmaceutical, and luxury electronics sectors. The demand for advanced reuse systems in North America is mainly due to its large-scale R&D projects and the presence of innovators like Xylem and Evoqua.

In Europe, the leadership in circular economy innovation and the push for resource safety innovation are driving the adoption of high-reliability water reuse systems. Countries like Germany, France, and the UK are at the forefront, with significant focus on integrating smart reuse solutions into daily production routines and advanced treatment to ensure the highest levels of performance and reliability.

How are Latin America and Middle East & Africa Expanding?

Latin America is witnessing significant expansion in the industrial water reuse systems market, driven by the region’s emergence as a critical hub for sustainable mining and agricultural exports. Countries like Brazil, Mexico, and Chile are increasingly adopting digital reuse to meet international environmental standards and ensure the “green” credentials of their exports. The presence of global mining giants and a growing focus on the lithium and mineral value chain provide a fertile ground for AI-based reuse solutions.

In the Middle East & Africa, the market is fueled by the rapid development of desalination-alternative infrastructure and the establishment of new industrial cities, particularly in Saudi Arabia and the UAE. These nations are integrating advanced digital reuse into their smart city and sustainable energy initiatives to ensure long-term asset performance. Additionally, the focus on ZLD systems in regions like South Africa and Egypt is driving the adoption of high-reliability reuse systems to ensure ethical sourcing and compliance with global supply chain regulations.

The companies such as Veolia Water Technologies, SUEZ, Xylem Inc., and Evoqua Water Technologies lead the global industrial water reuse systems market with a comprehensive range of software and auditing solutions, particularly for large-scale industrial and high-speed energy applications. Meanwhile, players including DuPont Water Solutions, Pentair plc, and Aquatech International focus on specialized enterprise-grade and high-density formulations targeting the professional and regulatory sectors. Emerging manufacturers and integrated players such as Kurita Water Industries, IDE Technologies, and Bio-Microbics are strengthening the market through innovations in digital twin technology and modular reuse platforms.

The global industrial water reuse systems market is expected to grow from USD 23.9 billion in 2026 to USD 67.2 billion by 2036.

The global industrial water reuse systems market is projected to grow at a CAGR of 10.9% from 2026 to 2036.

Membrane filtration systems are expected to dominate the market in 2026 due to their superior ability to support high-purity process water and cooling. However, biological treatment and AOP are projected to be the fastest-growing segments owing to their increasing adoption in next-generation industrial systems where high treatment delivery is required.

AI and ZLD are transforming the industrial water reuse landscape by demanding higher resource integrity, lower verification friction, and improved lifecycle repair. These technologies drive the adoption of advanced materials like digital twins and predictive analytics, enabling industrial manufacturers to support the complex formulations and high-frequency requirements of next-generation industrial products.

Asia-Pacific holds the largest share of the global industrial water reuse systems market in 2026. The largest share of this region is primarily attributed to the massive industrial push and the presence of the world’s most advanced manufacturing hubs in China, India, and Japan. North America and Europe together account for a substantial share, driven by high-end applications in chemical and power sectors.

The leading companies include Veolia Water Technologies, SUEZ, Xylem Inc., Evoqua Water Technologies, and DuPont Water Solutions.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Research Methodology

1.4. Assumptions & Limitations

2. Executive Summary

3. Market Overview

3.1. Introduction

3.2. Market Dynamics

3.2.1. Drivers

3.2.2. Restraints

3.2.3. Opportunities

3.2.4. Challenges

3.3. Impact of AI and ZLD Regulations on Industrial Water Reuse

3.4. Value Chain Analysis

4. Global Industrial Water Reuse Systems Market, by Technology

4.1. Introduction

4.2. Membrane Filtration

4.2.1. Reverse Osmosis (RO)

4.2.2. Ultrafiltration (UF)

4.2.3. Nanofiltration (NF)

4.2.4. Microfiltration (MF)

4.3. Biological Treatment

4.3.1. Membrane Bioreactor (MBR)

4.3.2. Moving Bed Biofilm Reactor (MBBR)

4.4. Chemical Treatment & Disinfection

4.4.1. Ozonation

4.4.2. UV Disinfection

4.5. Evaporation & Crystallization (Zero Liquid Discharge)

4.6. Advanced Oxidation Processes (AOP)

4.7. Others

5. Global Industrial Water Reuse Systems Market, by Application

5.1. Introduction

5.2. Cooling Water Reuse

5.3. Boiler Feed Water Reuse

5.4. Process Water Reuse

5.5. Wash Water Reuse

5.6. Others

6. Global Industrial Water Reuse Systems Market, by End-use Industry

6.1. Introduction

6.2. Power Generation

6.3. Oil & Gas

6.4. Food & Beverage

6.5. Chemical & Petrochemical

6.6. Pharmaceutical

6.7. Textile & Apparel

6.8. Pulp & Paper

6.9. Others

7. Global Industrial Water Reuse Systems Market, by Region

7.1. Introduction

7.2. North America

7.2.1. U.S.

7.2.2. Canada

7.3. Europe

7.3.1. Germany

7.3.2. France

7.3.3. U.K.

7.3.4. Italy

7.3.5. Spain

7.3.6. Netherlands

7.3.7. Rest of Europe

7.4. Asia-Pacific

7.4.1. China

7.4.2. Japan

7.4.3. South Korea

7.4.4. India

7.4.5. Australia

7.4.6. Rest of Asia-Pacific

7.5. Latin America

7.5.1. Brazil

7.5.2. Mexico

7.5.3. Argentina

7.5.4. Chile

7.5.5. Colombia

7.5.6. Rest of Latin America

7.6. Middle East & Africa

7.6.1. Saudi Arabia

7.6.2. UAE

7.6.3. Qatar

7.6.4. South Africa

7.6.5. Egypt

7.6.6. Nigeria

7.6.7. Rest of Middle East & Africa

8. Competitive Landscape

8.1. Overview

8.2. Key Growth Strategies

8.3. Competitive Benchmarking

8.4. Competitive Dashboard

8.4.1. Industry Leaders

8.4.2. Market Differentiators

8.4.3. Vanguards

8.4.4. Emerging Companies

8.5. Market Ranking/Positioning Analysis of Key Players, 2025

9. Company Profiles (Manufacturers & Providers)

9.1. Veolia Water Technologies

9.2. SUEZ

9.3. Xylem Inc.

9.4. Evoqua Water Technologies

9.5. DuPont Water Solutions

9.6. Pentair plc

9.7. Aquatech International LLC

9.8. Kurita Water Industries Ltd.

9.9. IDE Technologies

9.10. Bio-Microbics, Inc.

9.11. Koch Separation Solutions

9.12. Samco Technologies, Inc.

10. Appendix

10.1. Questionnaire

10.2. Related Reports

Published Date: Mar-2026

Subscribe to get the latest industry updates