Resources

About Us

Data Center Microgrid Market Size, Share & Trends Analysis by Power Source (Natural Gas & Diesel Generators, Battery Energy Storage Systems, Fuel Cells), Component (Microgrid Controllers, Inverters, Switchgear, Software), Application, and Geography — Global Opportunity Analysis and Industry Forecast (2026–2036)

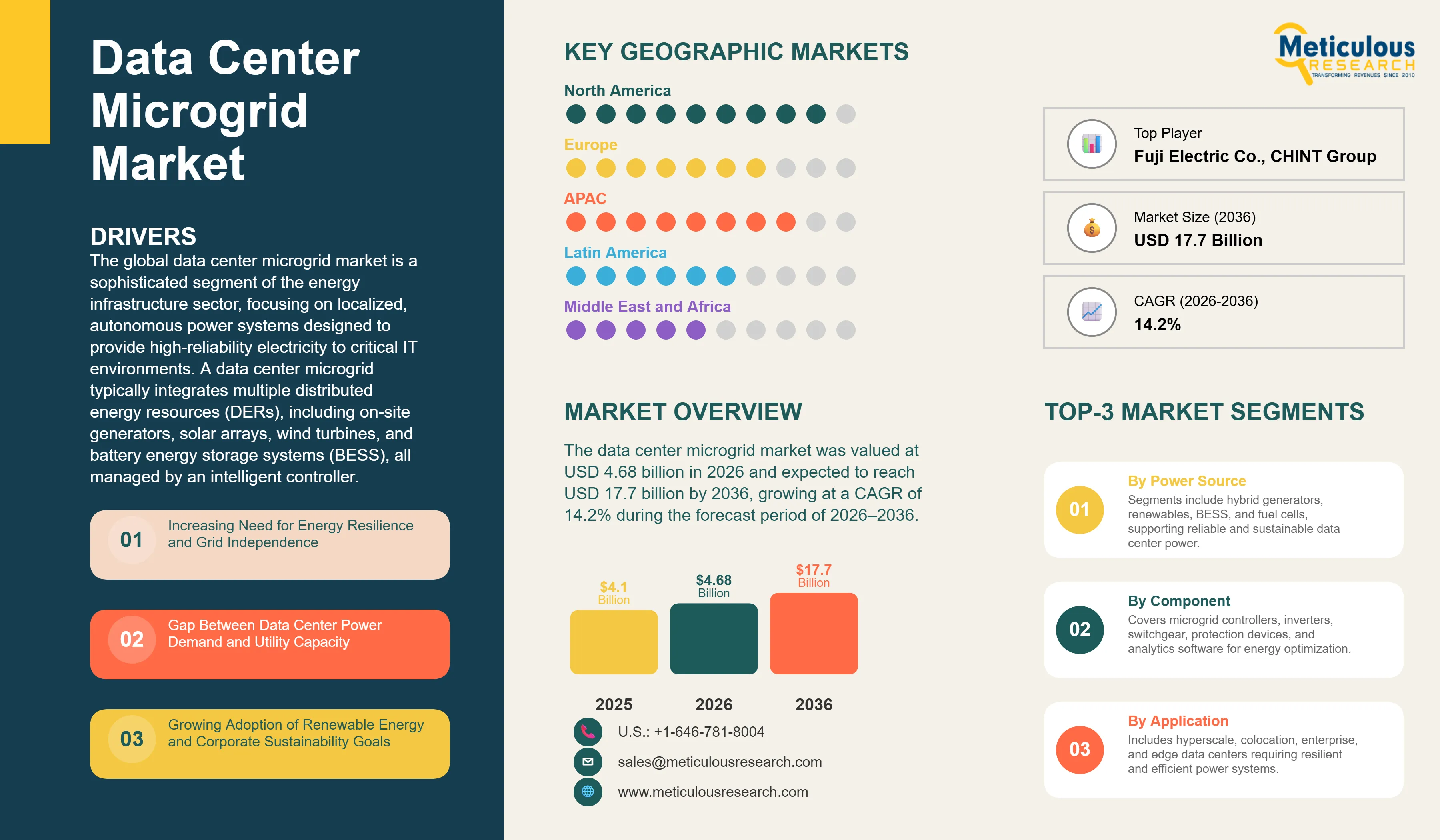

Report ID: MRSE - 1042002 Pages: 256 Jun-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global data center microgrid market was valued at USD 4.68 billion in 2026. This market is expected to reach USD 17.7 billion by 2036, growing at a CAGR of 14.2% during the forecast period of 2026–2036.

The global data center microgrid market is a sophisticated segment of the energy infrastructure sector, focusing on localized, autonomous power systems designed to provide high-reliability electricity to critical IT environments. A data center microgrid typically integrates multiple distributed energy resources (DERs), including on-site generators, solar arrays, wind turbines, and battery energy storage systems (BESS), all managed by an intelligent controller. Unlike traditional backup power systems, a microgrid can operate in parallel with the utility grid or in 'island mode' during grid disturbances, ensuring that the data center remains operational without interruption. The market is witnessing rapid expansion as data center operators seek to mitigate the risks of grid instability, rising energy costs, and the need for sustainable, carbon-neutral power solutions.

The growth in data center microgrid adoption is primarily driven by the large scale of new hyperscale facilities and the unprecedented power requirements of artificial intelligence (AI) workloads. According to the International Energy Agency (IEA), global electricity consumption from data centers is projected to grow by approximately 15% per year through 2030, reaching over 1,000 TWh. This growth is placing immense strain on national utility grids, leading to extended wait times for new power connections. In many regions, the utility 'time-to-power' now exceeds 1.5-2 years, forcing data center providers to build their own on-site power generation and microgrid infrastructure to commission facilities on schedule. Bloom Energy reports that total U.S. IT load capacity is expected to roughly double over the next three years, further accelerating the demand for autonomous power solutions.

Sustainability mandates and corporate net-zero goals are also fundamental drivers of the market. Leading technology companies, including Amazon, Google, and Microsoft, have committed to powering their operations with 100% renewable energy. Microgrids enable these operators to integrate intermittent renewable sources like solar and wind with reliable energy storage, effectively balancing the variable supply with the constant demand of server loads. However, the market faces significant restraints, including high initial capital expenditure (CAPEX) and regulatory hurdles. The cost of microgrid controllers, high-capacity batteries, and renewable assets can be 30-50% higher than traditional electrical designs. Additionally, navigating complex interconnection agreements and local regulations regarding 'over-the-fence' power sales remains a challenge for many developers.

Despite these challenges, the emergence of advanced fuel cell technology and the 'Grid-as-a-Service' (GaaS) business model presents substantial growth opportunities. Hydrogen-powered fuel cells offer a zero-emission alternative to diesel generators for long-duration backup, aligning with global decarbonization efforts. The GaaS model allows data center operators to outsource the design, construction, and operation of their microgrids to third-party energy specialists, reducing the financial burden of upfront investment. Geographic expansion in regions with power-constrained grids, such as parts of Asia-Pacific and Europe, further supports the market's robust long-term growth trajectory.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The key driver for the data center microgrid market is the increasing need for energy resilience in the face of utility grid instability. As extreme weather events and aging infrastructure lead to more frequent and prolonged power outages, data center operators can no longer rely solely on the utility grid for primary power. Microgrids provide a layer of 'islandable' protection, allowing facilities to maintain 100% uptime regardless of grid conditions. Pew Research reports that the U.S. is projected to add 217 GW of Distributed Energy Resource (DER) capacity by 2028, highlighting the national shift toward localized power generation for critical infrastructure.

Another significant driver is the gap between data center power demand and utility delivery capacity. The Electric Power Research Institute (EPRI) estimates that data centers could grow to consume up to 9% of total U.S. electricity generation by 2030. In major hubs like Northern Virginia and Dublin, the sheer scale of data center load has outpaced grid upgrades. This has forced operators to become their own power utilities by deploying on-site microgrids that can provide both primary and backup power. The rise of gigawatt-scale campuses, which function as independent energy ecosystems, is a direct result of this driver, necessitating sophisticated microgrid control and distribution systems.

A major restraint is the high initial capital expenditure (CAPEX) required for microgrid implementation. Integrating diverse energy sources like solar PV, wind turbines, and high-capacity BESS requires significant upfront investment in equipment and specialized engineering. For many enterprise data center operators, the payback period for a microgrid can be several years, making it a difficult investment to justify compared to traditional diesel-only backup. Additionally, the lack of standardized microgrid regulations and the complexity of securing interconnection permits from utilities can delay projects and increase soft costs significantly.

The transition toward zero-emission backup power through hydrogen fuel cells presents a massive growth opportunity. As governments tighten regulations on diesel emissions, data center operators are exploring fuel cells as a clean alternative for long-duration power. Companies like Microsoft and Equinix have already begun testing large-scale fuel cell microgrids. Another opportunity lies in the participation of data center microgrids in grid services, such as demand response and frequency regulation. By selling excess on-site power or reducing grid demand during peak periods, data centers can generate new revenue streams, effectively turning their power infrastructure into a profit center.

The technical integration of intermittent renewable energy with the constant, high-availability load of a data center is a critical challenge. Ensuring that the microgrid can seamlessly balance variable solar or wind output with server demand requires highly sophisticated control software and fast-responding energy storage. Furthermore, the increasing connectivity of microgrid components introduces cybersecurity vulnerabilities. Protecting distributed energy assets from grid-level cyber threats is a paramount concern, requiring robust security frameworks and continuous monitoring to prevent unauthorized access to the facility's power management system.

The 'Grid-as-a-Service' model is gaining traction as a way for data center operators to deploy microgrids without significant upfront investment. Under this model, third-party energy companies or manufacturers design, build, own, and operate the microgrid infrastructure, selling the power and resilience back to the data center operator through a long-term agreement. This allows data center providers to focus on their core IT business while benefiting from the reliability and sustainability of an on-site microgrid.

The use of artificial intelligence and machine learning in microgrid controllers is a growing trend. AI-driven controllers can analyze weather patterns, utility pricing, and facility load profiles in real-time to optimize energy dispatch. This ensures that the microgrid always uses the most cost-effective and sustainable energy source available. Predictive analytics also allow for the early detection of equipment anomalies, enabling proactive maintenance and further enhancing the overall reliability of the data center's power system.

Based on power source, the market is segmented into Natural Gas & Diesel Generators, Renewable Energy (Solar, Wind), Battery Energy Storage Systems (BESS), and Fuel Cells. In 2026, the Natural Gas & Diesel Generators (Hybrid) segment is expected to hold the largest share of the market. Despite the shift toward renewables, high-capacity generators remain the only proven technology capable of providing the 48-72 hours of continuous backup power required by Tier III and IV data centers. The transition toward natural gas and renewable-diesel blends is helping to reduce the carbon footprint of this segment while maintaining its reliability.

However, the Renewable Energy and BESS segments are projected to register the highest CAGR during the forecast period. This growth is driven by the falling cost of solar PV and lithium-ion batteries, combined with the aggressive sustainability targets of major cloud providers. BESS units are increasingly being used not just for backup, but also for peak shaving and grid stabilization, significantly improving the economic viability of the microgrid.

North America is expected to dominate the global data center microgrid market in 2026, primarily due to the high concentration of hyperscale facilities and the presence of major technology companies. The U.S. Congress reports that data center annual energy use reached ~176 TWh in 2023, representing ~4.4% of total U.S. electricity. This massive energy demand, combined with an aging utility grid, has made microgrids a necessity for many North American operators. The key companies operating in the North American market are Schneider Electric SE, ABB Ltd., Siemens Energy AG, Eaton Corporation plc, and Bloom Energy Corporation.

Asia-Pacific is projected to witness the fastest growth during the forecast period. This is driven by rapid digital transformation, increasing internet penetration, and significant investments in data center infrastructure in countries like China and India. In many parts of the region, utility grid reliability remains a challenge, making on-site microgrids an essential component of data center design. The key companies operating in the Asia-Pacific market are Mitsubishi Electric Corporation, Fuji Electric Co., Ltd., LS ELECTRIC Co., Ltd., CHINT Group, and Toshiba Energy Systems & Solutions Corporation.

The market is projected to reach USD 17.7 billion by 2036, growing at a CAGR of 14.2% from 2026 to 2036.

The Natural Gas & Diesel Generators (Hybrid) segment is expected to hold the largest share in 2026 due to its reliability.

The increasing need for energy resilience and the gap between data center power demand and utility grid capacity are the primary drivers.

Asia-Pacific is projected to witness the highest CAGR due to rapid digitalization and grid reliability challenges in the region.

It allows operators to deploy microgrids without significant upfront investment by outsourcing the infrastructure to third parties.

AI-driven controllers optimize energy dispatch, analyze weather patterns, and enable predictive maintenance for better reliability.

BESS provides immediate backup, enables renewable integration, and allows for participation in grid services like demand response.

Challenges include complex interconnection agreements and regulations regarding 'over-the-fence' power sales.

It offers a zero-emission alternative for long-duration backup, helping data centers meet aggressive sustainability goals.

Leading companies include Schneider Electric SE, ABB Ltd., Siemens Energy AG, Eaton Corporation plc, and Bloom Energy.

Published Date: Jun-2026

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Feb-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates