Resources

About Us

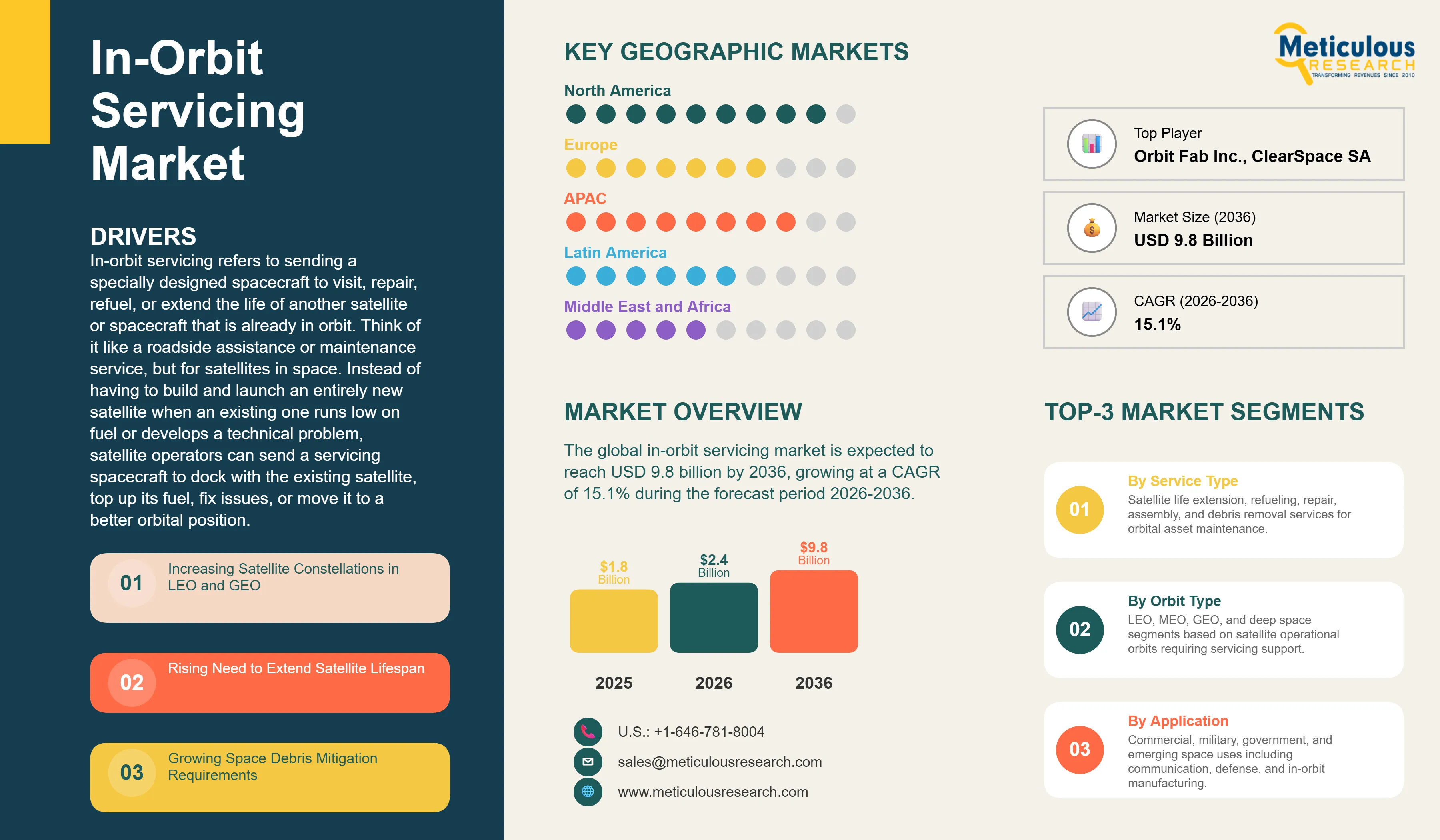

The global in-orbit servicing market was valued at USD 1.8 billion in 2025. This market is expected to reach USD 9.8 billion by 2036 from an estimated USD 2.4 billion in 2026, growing at a CAGR of 15.1% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

In-orbit servicing refers to sending a specially designed spacecraft to visit, repair, refuel, or extend the life of another satellite or spacecraft that is already in orbit. Think of it like a roadside assistance or maintenance service, but for satellites in space. Instead of having to build and launch an entirely new satellite when an existing one runs low on fuel or develops a technical problem, satellite operators can send a servicing spacecraft to dock with the existing satellite, top up its fuel, fix issues, or move it to a better orbital position. This concept makes the entire satellite industry significantly more economical, because satellites represent investments of hundreds of millions to billions of dollars and being able to service rather than replace them extends their commercial lives and improves the return on that investment.

The market is growing because the number of satellites in orbit is growing very rapidly, particularly in low earth orbit where companies like SpaceX, Amazon, and OneWeb are deploying thousands of satellites for broadband internet services. This rapid growth of the satellite population is creating two related business opportunities. First, all these satellites will eventually need servicing, refueling, or repositioning, creating a large and growing addressable market for in-orbit servicing providers. Second, the growing number of satellites is contributing to a serious and worsening space debris problem, with thousands of defunct satellites and fragments of old spacecraft cluttering orbital paths and creating collision risks for active satellites. Cleaning up this debris requires specialized active debris removal missions, which is an entirely new and commercially significant service category that is attracting both government funding and private investment.

Two major opportunities are shaping the market going forward. The development of in-orbit refueling infrastructure, essentially orbital filling stations where servicing vehicles can pick up propellant to deliver to satellites, would transform the economics of satellite operations by making it routine and affordable to extend satellite lifetimes through regular refueling rather than relying on a single fuel load at launch. Orbit Fab and several competitors are working on exactly this concept. In addition, as the commercial space economy expands to include in-orbit manufacturing, space tourism, and eventually lunar operations, the need for space logistics and assembly services in orbit is expected to grow into a major new market category well beyond today's satellite servicing applications.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 9.8 Billion |

|

Market Size in 2026 |

USD 2.4 Billion |

|

Market Size in 2025 |

USD 1.8 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 15.1% |

|

Dominating Service Type |

Satellite Life Extension Services |

|

Fastest Growing Service Type |

Active Debris Removal (ADR) |

|

Dominating Orbit Type |

Geostationary Orbit (GEO) |

|

Fastest Growing Orbit Type |

Low Earth Orbit (LEO) |

|

Dominating Application |

Commercial Applications |

|

Fastest Growing Application |

Military & Defense Applications |

|

Dominating End User |

Satellite Operators |

|

Fastest Growing End User |

Commercial Space Companies |

|

Dominating Vehicle Type |

Servicing Satellites (Servicers) |

|

Fastest Growing Vehicle Type |

Refueling Vehicles |

|

Dominating Operation Type |

Semi-Autonomous Operations |

|

Fastest Growing Operation Type |

Autonomous Operations |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Northrop Grumman's Mission Extension Vehicles Proving the Commercial Model

The most important commercial validation event in the in-orbit servicing market has been Northrop Grumman's successful demonstration of Mission Extension Vehicles, which dock with commercial communication satellites that are running low on fuel and take over their station-keeping and orbit-raising functions, effectively adding years to the operational life of satellites that would otherwise have to be retired. The first MEV mission docked with Intelsat 901 in April 2020, the first commercial docking in geostationary orbit, and extended the satellite's useful service life by five years. A second mission with Intelsat 10-02 followed in 2021. These missions were not just technical demonstrations but commercially contracted services where Intelsat paid Northrop Grumman for a real service that provided real commercial value, establishing a proven business model for in-orbit satellite life extension services that the rest of the industry is now following.

The commercial success of the MEV program has had a significant effect on how satellite operators, insurance companies, and investors think about satellite end-of-life planning. Satellite operators who previously assumed they would deorbit a satellite at the end of its fuel life are now planning for the possibility of extending that satellite's commercial life through servicing, changing the economic model for satellite investment. Insurance and financing companies are beginning to factor in the availability of in-orbit servicing options when underwriting satellite programs and structuring satellite financing. This shift in industry thinking is progressively expanding the addressable market for in-orbit servicing beyond early-adopter demonstration missions toward mainstream commercial adoption across the satellite industry.

Space Debris Removal Becoming an Urgent Commercial and Regulatory Priority

The growing severity of the orbital debris problem is transforming active debris removal from a theoretical future concern into an urgent and commercially real challenge that governments, space agencies, and satellite operators are actively funding solutions to address. The European Space Agency estimates there are over 27,000 pieces of debris large enough to track and millions of smaller fragments in orbit, all traveling at speeds that make even small fragments capable of destroying a satellite on impact. As the number of active satellites increases rapidly, particularly in low earth orbit where most new constellations are being deployed, the probability of collision between debris and active satellites is increasing to levels where insurers, operators, and regulators are treating debris mitigation as a serious operational risk.

Several governments including the UK, Japan, the EU, and the US have committed funding to commercial debris removal demonstration programs. Astroscale's ELSA-d mission, which tested magnetic capture technology for debris removal in 2021, and the upcoming ClearSpace-1 mission contracted by ESA to remove a piece of Vega rocket upper stage debris from orbit are the first commercially contracted debris removal missions. These demonstration programs are intended to establish the technical feasibility and regulatory frameworks for debris removal as a service, paving the way for larger-scale debris removal procurement programs by space agencies and eventually by satellite constellation operators who face growing regulatory pressure to manage the orbital environment in which their constellations operate.

New Commercial Entrants Racing to Build the In-Orbit Servicing Infrastructure

A wave of well-funded startups and emerging companies is competing to build the spacecraft, refueling hardware, and service platforms that will constitute the commercial in-orbit servicing industry of the 2030s. Orbit Fab is developing standardized refueling ports and orbital propellant depots, and has already launched demonstration hardware and signed agreements with several satellite manufacturers to include their Rapidly Attachable Fluid Transfer Interface on new satellite designs. Starfish Space is developing a small and affordable proximity operations and docking vehicle called Otter that targets the growing small satellite market that has not traditionally had access to servicing services. D-Orbit operates space tug missions that transport and deploy satellite payloads in orbit, offering a logistics service that bridges traditional launch and satellite operations. Momentus is developing in-space transportation services for satellite repositioning and hosted payload delivery.

The competitive landscape for in-orbit servicing is becoming more dynamic as these newer entrants challenge established aerospace companies in specific service niches, particularly in small satellite servicing and space logistics where the new entrants often have more agile development approaches and lower cost structures. The established prime contractors including Northrop Grumman through SpaceLogistics, Airbus through its space servicing initiatives, and Maxar Technologies through its robotic servicing programs have the advantage of existing customer relationships, deep technical heritage, and government program access. The combination of established and emerging players is creating a more competitive and more commercially innovative market than the in-orbit servicing concept attracted in its early years when only government-funded programs seemed viable.

Rising Need to Extend Satellite Lifespan

A large geostationary communication satellite costs between USD 200 million and USD 500 million to build and an additional USD 80 million to USD 150 million to launch. The commercial life of these satellites is determined primarily by how much fuel they carry for station-keeping, which keeps them in the correct orbital position relative to the Earth and the antenna beams serving customer ground stations. When a satellite runs out of fuel, it drifts out of its operational slot and must be retired, even though all of its electronic systems may still be working perfectly. Being able to refuel or take over the station-keeping function of a satellite that has run out of propellant but is otherwise fully operational is therefore an enormously valuable service that allows the satellite operator to continue generating revenue from a USD 200 million plus asset for years longer than the original fuel load would permit. The commercial logic of this service is so compelling that even early-adopter in-orbit servicing missions priced at several tens of millions of dollars have provided positive economic returns to satellite operators compared with the cost of replacing the served satellite.

Growing Space Debris Mitigation Requirements

The orbital debris problem has reached a point where national space agencies, regulators, and the satellite industry are treating it as a serious business and safety risk rather than a long-term theoretical concern. The Federal Communications Commission in the United States has tightened deorbit requirements for satellites in low earth orbit, reducing the required deorbit timeline from 25 years to 5 years, and is developing rules that will mandate debris mitigation plans for new satellite licenses. The European Space Agency and European national space agencies are funding active debris removal demonstration contracts, and the UK Space Agency has made debris removal a priority area for national space program investment. For satellite constellation operators who are deploying thousands of satellites in low earth orbit, the growing regulatory requirements for debris management and the reputational and liability risks associated with satellite collisions or debris generation are creating direct financial incentives to invest in debris removal and satellite disposal services. These regulatory and liability drivers are converting what was previously a discretionary activity into a commercially mandatory service category.

Development of In-Orbit Refueling Infrastructure

The development of standardized refueling technology and orbital propellant depots that can supply fuel to servicing vehicles and eventually directly to client satellites represents one of the most commercially transformative opportunities in the in-orbit servicing market. Today, each servicing mission must carry all the propellant it needs for both its own operations and any fuel it transfers to client satellites, which limits the number of clients a single servicing vehicle can serve before it needs to return or be retired. An orbital refueling depot that can be resupplied from Earth and provide propellant to multiple servicing vehicles would fundamentally change this model, enabling a much larger scale of servicing operations from a shared infrastructure base. Orbit Fab is the leading commercial developer of this concept, having launched a demonstration propellant depot to the International Space Station's orbit and working to establish its RAFTI interface standard as the industry standard for satellite refueling connections. If standardized refueling ports become a common feature of new satellites, the addressable market for refueling services expands enormously.

Growth in Space Logistics and Assembly

Beyond servicing existing satellites, the broader concept of space logistics, including transporting cargo and satellites between orbits, assembling large space structures from components launched separately, and eventually manufacturing products in orbit for use in space or return to Earth, represents a large and growing commercial opportunity for in-orbit servicing companies. Space tugs that can move satellites from a standard launch orbit to their operational orbit, take over-age satellites to a graveyard orbit, or transport cargo between orbital facilities are needed in growing numbers as space operations become more complex and commercially varied. As NASA's Artemis lunar program and commercial lunar transportation services develop, the need for logistics services between Earth orbit and lunar orbit will create an entirely new market category for in-orbit servicing companies with long-range propulsion capabilities. D-Orbit, Momentus, Rocket Lab, and Starfish Space are all positioning themselves to capture part of this space logistics opportunity, which is expected to grow substantially through the forecast period as the commercial space economy matures.

By Service Type: In 2026, Satellite Life Extension Services to Dominate

Based on service type, the global in-orbit servicing market is segmented into satellite life extension services, refueling services, repair and maintenance services, assembly and manufacturing services, and active debris removal. In 2026, the satellite life extension services segment is expected to account for the largest share of the global in-orbit servicing market. Life extension services, which include Northrop Grumman's commercially proven Mission Extension Vehicle approach of docking with fuel-depleted satellites and taking over their station-keeping and orbit-raising functions, currently represent the most commercially mature and highest-revenue segment of the in-orbit servicing market. The compelling economics of extending the life of high-value geostationary satellites rather than replacing them have driven multiple commercial contracts and established this as a proven revenue-generating service with a clear and growing customer base among satellite fleet operators.

However, the active debris removal segment is projected to register the highest CAGR during the forecast period. The combination of tightening regulatory requirements, growing funding from national space agencies for demonstration programs, and the increasing urgency of the orbital debris problem as satellite numbers grow is expected to drive rapid growth in ADR services from a currently small base. The first commercial ADR demonstration contracts, including ESA's ClearSpace-1 mission, are establishing the technical and commercial foundations for a large-scale debris removal service industry that is expected to develop substantially through the forecast period.

By Orbit Type: In 2026, GEO to Hold the Largest Share

Based on orbit type, the global in-orbit servicing market is segmented into low earth orbit, medium earth orbit, geostationary orbit, and deep space. In 2026, the GEO segment is expected to account for the largest share of the global in-orbit servicing market. Geostationary orbit is home to the world's most valuable commercial communication satellites, which generate the highest revenue per satellite of any orbital class and represent the clearest and most immediate economic case for in-orbit servicing. The proven commercial transactions for GEO satellite life extension through Northrop Grumman's MEV services and the high value per customer satellite make GEO the current revenue leader despite hosting fewer satellites than LEO.

However, the LEO segment is projected to register the highest CAGR during the forecast period. The rapid growth of large satellite constellations in low earth orbit for broadband internet, earth observation, and other services is creating a very large and growing population of LEO satellites that will need inspection, repositioning, and eventually end-of-life disposal services. The active debris removal challenge is also primarily concentrated in low earth orbit, where most debris and most new satellite deployments are located, making LEO the focus of the fastest-growing servicing categories.

By Application: In 2026, Commercial Applications to Hold the Largest Share

Based on application, the global in-orbit servicing market is segmented into commercial applications, military and defense applications, government and civil space applications, and emerging applications. In 2026, the commercial applications segment is expected to account for the largest share of the global in-orbit servicing market, accounting for approximately 47% of total market revenue. Commercial satellite operators, including communication satellite fleet operators and earth observation constellation operators, represent the largest and most commercially active customer base for in-orbit servicing services. The very high value of commercial geostationary communication satellites makes life extension services economically compelling, and commercial operators have been the first customers for commercially contracted in-orbit servicing missions. The broadband mega-constellation operators in LEO, including SpaceX Starlink, Amazon Kuiper, and OneWeb, are expected to become important future customers as their satellite populations grow and satellite replacement and debris management needs increase.

However, the military and defense applications segment is projected to register the highest CAGR during the forecast period. Military satellites are among the most strategically valuable and expensive assets in any national space program, and the ability to service, repair, and extend the life of military satellites rather than replacing them represents a significant cost saving and strategic advantage. The U.S. Space Force's growing interest in satellite servicing and the increasing recognition across allied defense establishments that space asset resilience requires the ability to repair and reconstitute satellites on orbit are expected to drive rapid growth in government-contracted military satellite servicing programs.

By End User: In 2026, Satellite Operators to Hold the Largest Share

Based on end user, the global in-orbit servicing market is segmented into satellite operators, space agencies, defense organizations, and commercial space companies. In 2026, the satellite operators segment is expected to account for the largest share of the global in-orbit servicing market. Commercial satellite fleet operators including Intelsat, SES, Inmarsat, and Eutelsat have been the first paying customers for in-orbit servicing services, recognizing the financial benefit of extending the operational lives of high-value satellites rather than replacing them. The growing number of satellite operators managing large fleets of both GEO and LEO satellites creates a large and expanding potential customer base for in-orbit servicing providers as the technology matures and prices become more competitive.

However, the commercial space companies segment is projected to register the highest CAGR during the forecast period. The rapid expansion of commercial space activities including satellite constellation deployment, commercial space station development, and the growth of the broader commercial space economy is creating growing demand for in-orbit logistics, servicing, and support services from commercial companies that are not traditional satellite operators. New commercial space companies need orbital transportation, satellite deployment optimization, and servicing support in ways that traditional government space programs and established satellite operators did not.

By Vehicle Type: In 2026, Servicing Satellites to Hold the Largest Share

Based on vehicle type, the global in-orbit servicing market is segmented into servicing satellites, space tugs, robotic servicing platforms, and refueling vehicles. In 2026, the servicing satellites segment is expected to account for the largest share of the global in-orbit servicing market. Servicing satellites, which are purpose-built spacecraft designed to rendezvous and dock with client satellites to provide life extension and other services, represent the most commercially advanced vehicle category in the market. Northrop Grumman's Mission Extension Vehicle is the most commercially established example, but several other companies are developing competing servicing satellite concepts targeting different orbital classes and service types.

However, the refueling vehicles segment is projected to register the highest CAGR during the forecast period. The development of dedicated spacecraft designed to carry and transfer propellant to client satellites is a newer but potentially transformative service category that could enable a much larger scale of satellite life extension if standardized refueling interfaces become common on new satellites. The growing investment in refueling vehicle development from Orbit Fab, Starfish Space, and several other companies indicates the strong commercial interest in this category.

By Operation Type: In 2026, Semi-Autonomous Operations to Hold the Largest Share

Based on operation type, the global in-orbit servicing market is segmented into autonomous operations, semi-autonomous operations, and teleoperated systems. In 2026, the semi-autonomous operations segment is expected to account for the largest share of the global in-orbit servicing market. Most current in-orbit servicing missions combine automated proximity operations and docking with ground-based monitoring and human oversight for critical decisions. This semi-autonomous approach reflects where the technology currently is: autonomous rendezvous and docking has been demonstrated and works reliably, but operators and mission designers prefer to maintain human decision-making authority for actions that could have irreversible consequences such as physically docking with a client satellite.

However, the autonomous operations segment is projected to register the highest CAGR during the forecast period. As the volume of servicing missions grows, particularly for debris removal and constellation servicing where large numbers of relatively routine missions need to be completed cost-effectively, full autonomy becomes increasingly important. Ground-controlled operations are expensive and slow relative to the economics that large-scale servicing businesses would require, and fully autonomous servicing will be essential for making in-orbit servicing economically viable at the scale the growing satellite population demands.

In-Orbit Servicing Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global in-orbit servicing market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global in-orbit servicing market. The United States is home to the majority of the world's leading in-orbit servicing companies, including Northrop Grumman through its SpaceLogistics subsidiary which operates the commercially proven Mission Extension Vehicle service, Orbit Fab which is developing the orbital propellant depot infrastructure, Starfish Space, Redwire Corporation, Altius Space Machines, Honeybee Robotics, and Momentus. The U.S. Space Force's growing investment in satellite servicing and space domain awareness, DARPA's in-orbit servicing technology programs, and NASA's interest in servicing capabilities for future space exploration infrastructure collectively represent very large government program budgets that sustain the U.S. in-orbit servicing industry's technical development. The U.S. commercial satellite operator community, which includes some of the world's largest GEO communication satellite fleets, provides the paying customer base for commercial servicing missions. Canada's expertise in space robotics through the Canadarm heritage and its continued participation in space station and orbital infrastructure programs contributes additional North American capability to the market.

However, the Asia-Pacific in-orbit servicing market is expected to grow at the fastest CAGR during the forecast period. Japan has been particularly active in in-orbit servicing development, with JAXA conducting important proximity operations research and the Japanese commercial space sector developing servicing concepts targeting both commercial and government customers. Astroscale, a Japanese company with headquarters in Tokyo and operations in the UK, US, and Israel, is one of the global leaders in debris removal technology and has completed in-orbit demonstration missions. China's large and growing satellite program and its increasing ambitions in space infrastructure create both domestic demand for servicing capabilities and government investment in servicing technology development. India's growing commercial space sector and its ambitious national space exploration program are creating demand for space logistics and servicing capabilities. South Korea and Australia are also investing in space technology programs that include servicing and inspection capabilities.

Europe is a significant and active in-orbit servicing market, with the European Space Agency playing a particularly important role as a customer and program manager for commercial servicing demonstrations. ESA's ClearSpace-1 active debris removal mission, contracted to the Swiss startup ClearSpace SA, is the most prominent European-led commercial in-orbit servicing contract and represents ESA's strategy of purchasing commercial services rather than building government-only programs. Airbus Defence and Space, Thales Alenia Space, and the European space industry supply chain have strong capabilities relevant to in-orbit servicing including robotic systems, rendezvous and docking technology, and satellite interface hardware. Luxembourg and Belgium, despite their small sizes, host important space industry players and commercial space investment funds that contribute to the European in-orbit servicing ecosystem.

The in-orbit servicing market includes a mix of large established aerospace companies with deep space program credentials, mission-proven servicing companies that have already completed commercial in-orbit servicing transactions, and a growing group of well-funded startups developing new approaches to servicing, refueling, and space logistics. Competition is based on demonstrated mission success, the range of services offered, customer relationships, technical capability in autonomous rendezvous and docking, and the commercial and regulatory positioning needed to operate near other parties' satellites.

Northrop Grumman leads the market through SpaceLogistics LLC, which operates the commercially proven Mission Extension Vehicle service and is developing the next-generation Mission Robotic Vehicle offering greater flexibility and a wider range of repair and servicing capabilities. Astroscale is the leading commercial debris removal company, having successfully demonstrated proximity operations and magnetic capture technology for debris removal and secured contracts with JAXA, ESA, and UK Space Agency for demonstration debris removal missions. Orbit Fab is the leading developer of in-orbit propellant infrastructure, having launched hardware to orbit and signed agreements with satellite manufacturers to adopt its RAFTI refueling interface. Airbus SE brings deep aerospace engineering capability to in-orbit servicing through its satellite and space vehicle design expertise. ClearSpace SA in Switzerland is contracted by ESA for the first commercial debris removal mission targeting a specific piece of space junk.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' technology platforms, mission track records, customer relationships, geographic presence, and recent strategic developments. Some of the key players operating in the global in-orbit servicing market include Northrop Grumman Corporation (U.S.), Airbus SE (Netherlands), Astroscale Holdings Inc. (Japan/UK), Maxar Technologies Inc. (U.S.), Thales Alenia Space (France/Italy), Orbit Fab Inc. (U.S.), Redwire Corporation (U.S.), Altius Space Machines (U.S.), Honeybee Robotics/Blue Origin (U.S.), SpaceLogistics LLC (U.S.), ClearSpace SA (Switzerland), D-Orbit S.p.A. (Italy), Rocket Lab USA Inc. (U.S./New Zealand), Starfish Space Inc. (U.S.), and Momentus Inc. (U.S.), among others.

The global in-orbit servicing market is expected to reach USD 9.8 billion by 2036 from an estimated USD 2.4 billion in 2026, at a CAGR of 15.1% during the forecast period 2026-2036.

In 2026, the satellite life extension services segment is expected to hold the largest share of the global in-orbit servicing market, driven by the proven commercial success of Mission Extension Vehicle operations and the compelling economics of extending high-value satellite lifetimes rather than replacing them.

The active debris removal segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by tightening regulatory requirements for orbital debris management, growing government funding for commercial debris removal demonstrations, and the increasing urgency of the debris problem as satellite numbers in low earth orbit grow rapidly.

In 2026, the commercial applications segment is expected to hold the largest share of the global in-orbit servicing market, accounting for approximately 47% of total market revenue, reflecting commercial satellite operators being the first and most active paying customers for in-orbit servicing services.

The commercial space companies segment is projected to register the highest CAGR during the forecast period, driven by the rapid expansion of commercial space activities creating growing demand for in-orbit logistics, satellite deployment optimization, and servicing support from a broader range of commercial space industry participants.

The market is primarily driven by satellite operators seeking to extend the commercial life of high-value satellites rather than replacing them at enormous cost, and by the growing urgency of the orbital debris problem as the rapid expansion of satellite constellations increases collision risks and prompts regulatory action requiring commercial debris removal services.

Key players are Northrop Grumman Corporation (U.S.), Airbus SE (Netherlands), Astroscale Holdings Inc. (Japan/UK), Maxar Technologies Inc. (U.S.), Thales Alenia Space (France/Italy), Orbit Fab Inc. (U.S.), Redwire Corporation (U.S.), Altius Space Machines (U.S.), Honeybee Robotics/Blue Origin (U.S.), SpaceLogistics LLC (U.S.), ClearSpace SA (Switzerland), D-Orbit S.p.A. (Italy), Rocket Lab USA Inc. (U.S./New Zealand), Starfish Space Inc. (U.S.), and Momentus Inc. (U.S.), among others.

Asia-Pacific is expected to register the highest growth rate in the global in-orbit servicing market during the forecast period 2026-2036, driven by Japan's active in-orbit servicing development programs through Astroscale and JAXA, China's growing satellite program creating domestic servicing demand, and India and South Korea's increasing commercial space ambitions.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Increasing Satellite Constellations in LEO and GEO

4.2.1.2 Rising Need to Extend Satellite Lifespan

4.2.1.3 Growing Space Debris Mitigation Requirements

4.2.1.4 Cost Optimization vs Satellite Replacement

4.2.2 Restraints

4.2.2.1 High Mission Complexity and Risk

4.2.2.2 Limited Standardization Across Satellite Interfaces

4.2.2.3 High Capital Investment Requirements

4.2.3 Opportunities

4.2.3.1 Development of In-Orbit Refueling Infrastructure

4.2.3.2 Growth in Space Logistics and Assembly

4.2.3.3 Expansion of Commercial Space Economy

4.2.3.4 Increasing Defense and Strategic Space Investments

4.2.4 Challenges

4.2.4.1 Autonomous Operations and Robotics Limitations

4.2.4.2 Regulatory and Liability Frameworks

4.3 Technology Landscape

4.3.1 Robotic Servicing Systems

4.3.2 Autonomous Rendezvous & Docking (AR&D)

4.3.3 Space Robotics and Manipulators

4.3.4 AI-Based Mission Planning and Control

4.3.5 Refueling Interfaces and Fluid Transfer Systems

4.5 Value Chain Analysis

4.5.1 Component Suppliers (Robotics, Sensors, Propulsion)

4.5.2 Spacecraft Manufacturers

4.5.3 Service Providers

4.5.4 Satellite Operators

4.5.5 Space Agencies and Defense Organizations

4.6 Regulatory and Standards Landscape

4.6.1 Space Traffic Management Policies

4.6.2 Debris Mitigation Regulations

4.6.3 Licensing and Liability Frameworks

4.7 Porter’s Five Forces Analysis

4.8 Investment and Industry Trends

4.8.1 Growth in Commercial Servicing Startups

4.8.2 Government and Space Agency Programs

4.8.3 Strategic Partnerships and Joint Missions

4.9 Cost and Pricing Analysis

4.9.1 Mission Cost Breakdown

4.9.2 Refueling vs Replacement Economics

4.9.3 Cost by Service Type

5. In-Orbit Servicing Market, by Service Type

5.1 Introduction

5.2 Satellite Life Extension Services

5.2.1 Orbit Raising and Station-Keeping

5.2.2 Mission Extension Vehicles (MEVs)

5.3 Refueling Services

5.4 Repair and Maintenance Services

5.5 Assembly and Manufacturing Services

5.6 Active Debris Removal (ADR)

6. In-Orbit Servicing Market, by Orbit Type

6.1 Introduction

6.2 Low Earth Orbit (LEO)

6.3 Medium Earth Orbit (MEO)

6.4 Geostationary Orbit (GEO)

6.5 Deep Space

7. In-Orbit Servicing Market, by Application

7.1 Introduction

7.2 Commercial Applications

7.2.1 Communication Satellites (GEO Fleet Management)

7.2.2 Earth Observation Constellations

7.2.3 Broadband Mega-Constellations (LEO)

7.2.4 Satellite Fleet Optimization and Lifecycle Management

7.3 Military & Defense Applications

7.3.1 Strategic Satellite Maintenance

7.3.2 ISR (Intelligence, Surveillance, Reconnaissance) Support

7.3.3 Anti-Satellite Threat Mitigation

7.3.4 Resilient Space Architecture Support

7.4 Government & Civil Space Applications

7.4.1 Scientific Missions and Space Exploration

7.4.2 Space Station Support and Logistics

7.4.3 Climate Monitoring Satellites

7.4.4 National Space Programs

7.5 Emerging Applications

7.5.1 In-Orbit Manufacturing

7.5.2 Space Infrastructure Assembly

7.5.3 Space Tourism Support Systems

7.5.4 Lunar and Deep Space Servicing

8. In-Orbit Servicing Market, by End User

8.1 Introduction

8.2 Satellite Operators

8.3 Space Agencies

8.4 Defense Organizations

8.5 Commercial Space Companies

9. In-Orbit Servicing Market, by Vehicle Type

9.1 Introduction

9.2 Servicing Satellites (Servicers)

9.3 Space Tugs

9.4 Robotic Servicing Platforms

9.5 Refueling Vehicles

10. In-Orbit Servicing Market, by Operation Type

10.1 Introduction

10.2 Autonomous Operations

10.3 Semi-Autonomous Operations

10.4 Teleoperated Systems

11. In-Orbit Servicing Market, by Mission Type

11.1 Introduction

11.2 Inspection Missions

11.3 Docking and Relocation Missions

11.4 Refueling Missions

11.5 Repair Missions

11.6 Debris Removal Missions

12. In-Orbit Servicing Market, by Geography

12.1 Introduction

12.2 North America

12.2.1 U.S.

12.2.2 Canada

12.3 Europe

12.3.1 Germany

12.3.2 U.K.

12.3.3 France

12.3.4 Italy

12.3.5 Spain

12.3.6 Netherlands

12.3.7 Luxembourg

12.3.8 Belgium

12.3.9 Rest of Europe

12.4 Asia-Pacific

12.4.1 China

12.4.2 India

12.4.3 Japan

12.4.4 South Korea

12.4.5 Australia

12.4.6 Singapore

12.4.7 Indonesia

12.4.8 Thailand

12.4.9 Vietnam

12.4.10 Rest of Asia-Pacific

12.5 Latin America

12.5.1 Brazil

12.5.2 Mexico

12.5.3 Argentina

12.5.4 Chile

12.5.5 Colombia

12.5.6 Rest of Latin America

12.6 Middle East & Africa

12.6.1 UAE

12.6.2 Saudi Arabia

12.6.3 Israel

12.6.4 South Africa

12.6.5 Turkey

12.6.6 Rest of Middle East & Africa

13. Competitive Landscape

13.1 Overview

13.2 Key Growth Strategies

13.3 Competitive Benchmarking

13.4 Competitive Dashboard

13.4.1 Industry Leaders

13.4.2 Market Differentiators

13.4.3 Vanguards

13.4.4 Emerging Companies

13.5 Market Ranking/Positioning Analysis of Key Players, 2025

14. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

14.1 Northrop Grumman Corporation

14.2 Airbus SE

14.3 Astroscale Holdings Inc.

14.4 Maxar Technologies Inc.

14.5 Thales Alenia Space

14.6 Orbit Fab, Inc.

14.7 Redwire Corporation

14.8 Altius Space Machines

14.9 Honeybee Robotics (Blue Origin)

14.10 SpaceLogistics LLC

14.11 ClearSpace SA

14.12 D-Orbit S.p.A.

14.13 Rocket Lab USA, Inc.

14.14 Starfish Space Inc.

14.15 Momentus Inc.

15. Appendix

15.1 Additional Customization

15.2 Related Reports

Published Date: Aug-2025

Published Date: Feb-2026

Published Date: Apr-2026

Published Date: Apr-2026

Subscribe to get the latest industry updates