Resources

About Us

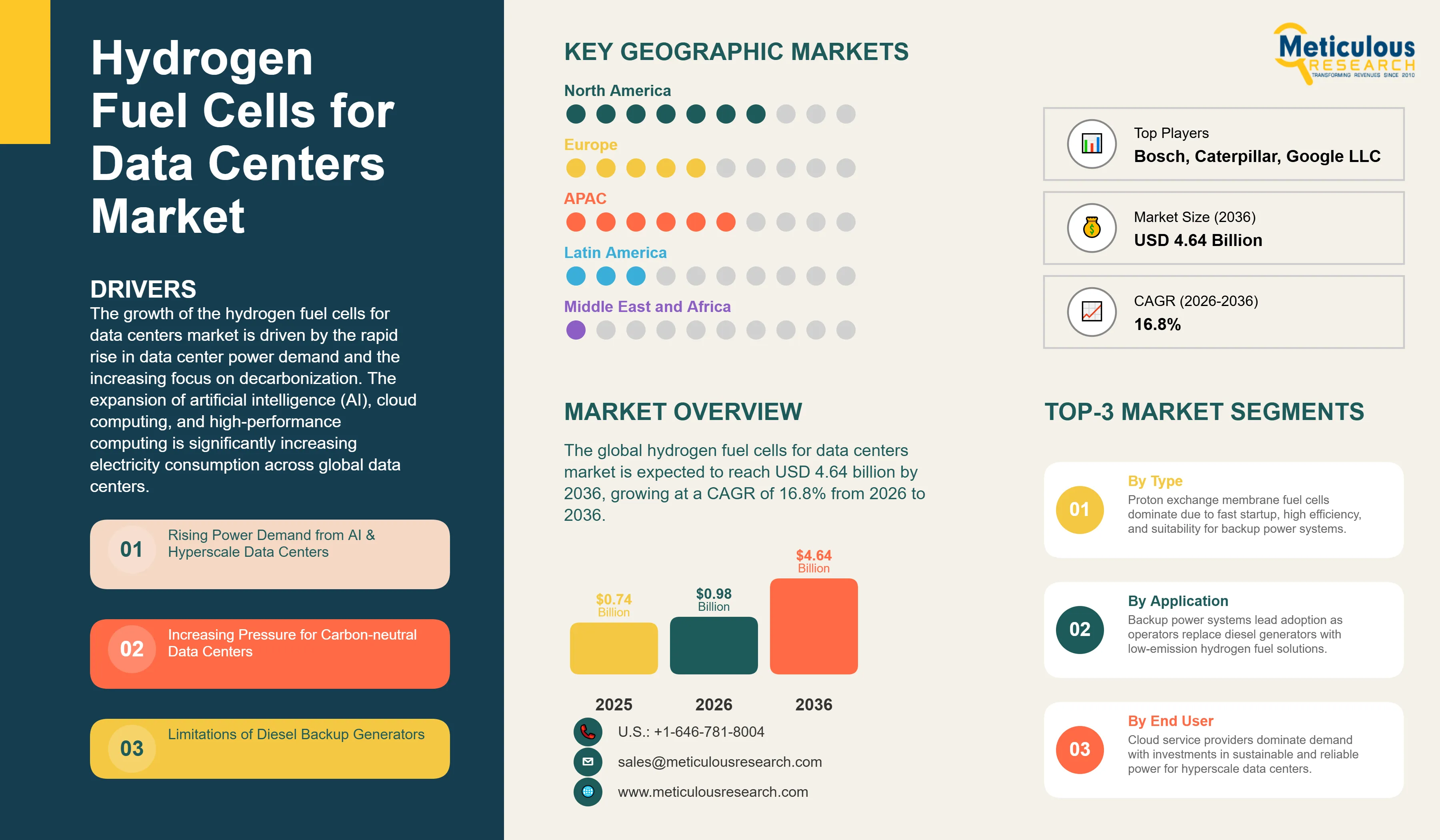

The global hydrogen fuel cells for data centers market was valued at USD 0.74 billion in 2025. This market is expected to reach USD 4.64 billion by 2036 from USD 0.98 billion in 2026, growing at a CAGR of 16.8% from 2026 to 2036.

The growth of the hydrogen fuel cells for data centers market is driven by the rapid rise in data center power demand and the increasing focus on decarbonization. The expansion of artificial intelligence (AI), cloud computing, and high-performance computing is significantly increasing electricity consumption across global data centers. According to the International Energy Agency (IEA), global data center electricity demand grew by 17% in 2025, while AI-focused data centers recorded nearly 50% growth. The IEA also projects global data center electricity consumption to increase from 485 terawatt-hours in 2025 to around 950 terawatt-hours by 2030.

At the same time, data center operators are under growing pressure to reduce carbon emissions and secure reliable clean power sources. This is accelerating investments in alternative energy solutions, including hydrogen and small modular nuclear reactors.

Hydrogen fuel cells are well positioned to address both reliability and sustainability requirements. Fuel cells generate electricity through an electrochemical reaction without combustion, resulting in low emissions, low noise, and high efficiency. Unlike conventional battery-based UPS systems, hydrogen fuel cells can provide continuous power for extended periods as long as hydrogen supply is available, making them suitable for both backup and primary power applications.

In addition, the growing availability of green hydrogen is strengthening market adoption. Fuel cells powered by green hydrogen can achieve near-zero lifecycle emissions, supporting the carbon neutrality goals of major data center operators such as Microsoft, Google, Amazon, and Meta.

Hydrogen fuel cell systems for data centers are stationary power generation units that use the electrochemical reaction between hydrogen fuel and atmospheric oxygen to generate direct current electricity, with water as the only direct byproduct. This process happens without combustion. Unlike diesel generators and natural gas turbines, fuel cells do not produce nitrogen oxides, particulate matter, or carbon dioxide at the point of use. For data center applications, fuel cell systems are set up to fulfill one of three main power roles: backup power systems, which stay on standby and automatically respond to grid power failures; prime or continuous power systems, which serve as the main power source for data center operations alongside or instead of grid power; and combined heat and power setups that capture the thermal energy from fuel cell operations to aid in data center cooling or heating, improving overall energy efficiency.

The four main fuel cell technologies relevant to data centers have different operational features. Proton exchange membrane fuel cells use a solid polymer electrolyte membrane and operate at relatively low temperatures of 60 to 80 degrees Celsius. This allows for quick startup from cold or standby states, making them ideal for backup power applications that need rapid load pickup. Solid oxide fuel cells use a solid ceramic electrolyte and operate at high temperatures of 700 to 1,000 degrees Celsius. They achieve electrical efficiencies of 60% or higher and enable combined heat and power operation, but they require long warmup periods that limit their use in pure backup power roles. Molten carbonate fuel cells use a molten carbonate salt electrolyte at around 650 degrees Celsius and can achieve electrical efficiencies of 47% or higher in power-only operation, reaching over 80% in combined heat and power mode. Phosphoric acid fuel cells use liquid phosphoric acid electrolyte and operate at temperatures of about 150 to 200 degrees Celsius. They are the most commercially developed stationary fuel cell technology, with decades of deployment in buildings and industrial facilities.

The competitive landscape includes fuel cell manufacturers, hydrogen system integrators, data center infrastructure companies, and major technology operators who are pushing the market with demonstration projects and early commercial deployments. Bloom Energy is the most active fuel cell company in data center applications, with its SOFC-based Energy Servers used at data centers operated by Google, Apple, Equinix, and other major operators. Ballard Power Systems provides PEM fuel cell technology for backup power applications. Plug Power and FuelCell Energy serve both the data center and broader stationary power markets. A significant demonstration in January 2024 by Caterpillar, Microsoft, and Ballard Power Systems showcased a 1.5 MW hydrogen fuel cell backup power system at Microsoft’s data center in Cheyenne, Wyoming. This milestone validated the technology, showing that large-format hydrogen fuel cell systems can meet data center uptime requirements of 99.999% in tough environmental conditions, including high altitude and freezing temperatures.

Caterpillar-Microsoft-Ballard Commercial Validation Establishing the Technology Pathway

The successful demonstration of a large-format hydrogen fuel cell backup power system at a Microsoft hyperscale data center in January 2024 marks a major milestone in this market. It establishes a proven design and validates the technology for future deployments. According to a Caterpillar press release from January 19, 2024, Caterpillar shared the results of its work with Microsoft and Ballard Power Systems. They showed that large-format hydrogen fuel cells can provide reliable and sustainable backup power for data centers.

The demonstration offered valuable insights into the ability of fuel cell systems to power multi-megawatt data centers. It ensured an uninterrupted power supply to meet 99.999% uptime requirements. The event took place at Microsoft’s data center in Cheyenne, Wyoming. It confirmed the hydrogen fuel cell power system's performance at 6,086 feet above sea level and in freezing temperatures. A Caterpillar Microgrid Controller operated two Cat Power Grid Stabilization battery energy storage systems alongside a 1.5 MW hydrogen fuel cell, simulating a 48-hour backup power event. This demonstration shows that hydrogen fuel cell systems can meet the highest availability and environmental resilience needs of hyperscale data centers. It also helps reduce the concerns about technology risks that have slowed wider adoption.

Growing Green Hydrogen Supply Pipeline Supporting Long-term Fuel Cell Decarbonization Case

The growth of the global low-emissions hydrogen production pipeline is steadily making the case for decarbonizing hydrogen fuel cell data center systems. It creates a path from the current grey hydrogen fuel supply to green hydrogen, allowing for near-zero lifecycle emissions. The IEA's Global Hydrogen Review 2024, published in October 2024, reports that global installed water electrolyser capacity reached 1.4 GW by the end of 2023. This capacity could hit 5 GW by the end of 2024, with China accounting for nearly 70% of that capacity and 60% of global electrolyser manufacturing capacity. The total electrolyser capacity that has reached a final investment decision stood at 20 GW globally, as stated in the IEA GHR 2024. Notably, 6.5 GW reached FID in the past 12 months alone. The IEA's Global Hydrogen Review 2025 confirmed that the global installed capacity of water electrolysis reached 2 GW in 2024, with more than 1 GW of additional capacity added through July 2025. Low-emissions hydrogen production grew by 10% in 2024 and is on track to reach 1 million tonnes in 2025, according to the IEA GHR 2025. While the IEA notes that the pace of low-emissions hydrogen growth has slowed compared to earlier expectations due to high costs and regulatory uncertainty, the trend of increasing green hydrogen supply is clear. This gives data center operators a reliable path to sourcing clean hydrogen for fuel cell operations in the forecast period.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 4.64 Billion |

|

Market Size in 2026 |

USD 0.98 Billion |

|

Market Size in 2025 |

USD 0.74 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 16.8% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Fuel Cell Type, Power Capacity, Deployment Model, Data Center Type, Application, End User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America |

Driver: AI-driven Data Center Power Demand Growth and Decarbonization Pressure

The main factor driving the market for hydrogen fuel cells in data centers is the increasing power demand from AI workloads, along with the growing pressure on data center operators to reduce carbon emissions from their power sources. According to the IEA's report, Key Questions on Energy and AI, released in April 2026, electricity demand for data centers jumped by 17% in 2025, while AI-focused data centers grew by 50% in that same year. The IEA predicts that data center electricity use will nearly double, going from 485 TWh in 2025 to 950 TWh by 2030, with an annual growth rate of about 15%. This growth is more than four times faster than in other sectors.

The IEA's April 2025 Energy and AI report indicates that major technology companies increased their capital spending to over USD 400 billion in 2025. This includes a commitment from Meta, Amazon, Alphabet, and Microsoft to spend USD 320 billion in 2025 alone. This investment marks the largest sustained cycle of data center investment ever. It is focused on AI-optimized data centers, which consume as much electricity as power-hungry factories. This demand creates a significant need for clean power alternatives, such as hydrogen fuel cells, to replace diesel backup generators and grid electricity.

Public commitments by data center operators to achieve carbon neutrality further drive clean power investments. Microsoft aims to be carbon negative by 2030, and Google plans to operate on 24/7 carbon-free energy by 2030. These commitments underscore the importance of clean power in their corporate strategies, directly influencing decisions to invest in hydrogen fuel cells.

Opportunity: Replacement of Diesel Generators with Hydrogen Systems

The switch from diesel backup generators to hydrogen fuel cell systems at existing and new data centers is the most clear and accessible near-term opportunity for this market. Diesel generators are the standard technology for emergency backup power in data centers. They provide cost-effective, reliable, and well-understood power at all sizes, from small facilities to large campus installations. However, diesel generators emit significant NOx, particulate matter, and CO2 during operation and testing. They face stricter air quality regulations in major markets. They also require regular load bank testing to ensure they are ready, which uses fuel without producing useful work. Additionally, they create complications with fuel storage and logistics, especially for large campuses that need multiple megawatts of backup capacity. The DOE's Hydrogen Fuel Cell Technologies Office has pointed out that data center backup power is an important early market for fuel cell technology. They have funded several demonstration projects at telecommunications facilities and data centers through the American Recovery and Reinvestment Act and later research programs. The IEA’s data from April 2026 shows a growing number of data center-SMR offtake agreements, reaching 45 GW worldwide as operators look for clean, reliable power options. This highlights the scale of investment driven by the need to decarbonize conventional fossil fuel power systems in data centers, with hydrogen fuel cells as a leading option.

Why Do PEM Fuel Cells Lead the Market?

In 2026, the proton exchange membrane fuel cells segment is expected to capture the largest share of the hydrogen fuel cells market for data centers. PEMFC technology is ideal for backup power. It currently represents the main deployment use case for fuel cells in data centers. This is because PEMFC systems start up quickly from cold or standby states and can rapidly respond to sudden load demands, similar to diesel generators when grid power fails. PEMFC systems operate at low temperatures of 60 to 80 degrees Celsius and use a solid polymer electrolyte. This simplicity makes them easier to operate and maintain compared to high-temperature fuel cell types. Ballard Power Systems, Plug Power, and Cummins are the main suppliers of PEMFC systems for backup power in data centers. The 1.5 MW hydrogen fuel cell system used in the Caterpillar-Microsoft-Ballard demonstration at the Microsoft Cheyenne data center used Ballard's PEMFC technology. This confirmed the application of PEMFC at a megawatt scale in data centers. The fast load response and ability to start up from cold are crucial for backup power systems that may need to take on the full data center critical load within seconds of a grid power failure. PEMFC meets these requirements more effectively than high-temperature fuel cells, which need longer warm-up times.

However, the solid oxide fuel cells segment is expected to grow the fastest during the forecast period. Bloom Energy's commercially deployed SOFC Energy Server platform is the most successful stationary fuel cell product for prime power in data centers. It has installations at Google, Apple, Equinix, and other major data center operators, providing continuous baseload power with efficiencies over 60%. SOFC systems can run on both natural gas and hydrogen. This allows for deployment before green hydrogen infrastructure is ready and enables a transition from natural gas to hydrogen as supply becomes available. The DOE's Hydrogen Fuel Cell Technologies Office has supported SOFC technology development for stationary uses for several years, recognizing its efficiency benefits for continuous power applications.

How Does the 1 MW to 5 MW Segment Lead the Market?

In 2026, the 1 MW to 5 MW segment is expected to dominate the hydrogen fuel cells market for data centers. This capacity range matches the power needs of individual data center buildings and halls in hyperscale and colocation segments. Backup power systems in these areas are usually designed to meet the critical load of one building or a specific group of loads. The 1.5 MW hydrogen fuel cell system from the Caterpillar-Microsoft-Ballard demonstration falls within this range. It serves as the reference design for future commercial deployments in the hyperscale segment. Fuel cell systems between 1 MW and 5 MW can be constructed using modular components. This modularity allows the system to be adjusted according to the specific building load while ensuring redundancy through multiple units.

However, the segment above 5 MW is expected to grow the fastest during the forecast period. As hyperscale data center projects increase in power density due to AI workloads, and as data center operators become more confident in hydrogen fuel cell technology from initial backup power deployments, the use of fuel cells for primary power at whole-campus scales of 5 MW and higher is anticipated to expand. Bloom Energy has installed multi-megawatt solid oxide fuel cell (SOFC) systems at data center locations. The IEA confirmed that the pipeline of data center agreements for clean, reliable power sources reached 45 GW by April 2026, highlighting the ambition for clean energy alternatives at major hyperscale facilities.

Why Do Backup Power Systems Lead the Market?

In 2026, the backup power systems segment is expected to hold the largest share of the hydrogen fuel cells for data centers market based on deployment model. Replacing diesel generators with backup power systems is the least risky way for data centers to adopt hydrogen fuel cells. This option allows for a direct substitution of an existing infrastructure component with clear specifications. The replacement system must offer the same or better power availability. It should respond to grid failure within the same or shorter timeframe as the current diesel generators. It also needs to support the critical load for at least the minimum backup duration specified in the facility's availability design and comply with local environmental and safety regulations. The DOE's Hydrogen Fuel Cell Technologies Office has identified backup power as an important early market for fuel cells. They pointed out the cost benefits over diesel in regions with fuel cell incentives, along with operational advantages like reduced maintenance and the elimination of emissions from diesel load bank testing. The demonstration by Caterpillar, Microsoft, and Ballard confirmed this application at a commercial scale by simulating a 48-hour backup power event at a megawatt-scale hyperscale data center.

However, the prime power systems segment is expected to grow the fastest during the forecast period. Using fuel cells as continuous primary power sources for data centers is on the rise. This trend is supported by Bloom Energy's SOFC installations at major tech companies. Data center operators aim to lessen their reliance on the electrical grid and avoid high transmission costs and carbon emissions associated with grid electricity in many markets. They also want to meet their commitments for 24/7 carbon-free energy through on-site zero-emission power generation. The IEA's report confirms that as of April 2026, data center operators had entered into 45 GW of conditional offtake agreements with SMR developers. This underscores the strong interest in reliable clean power sources for primary power, with hydrogen fuel cells being an available option in the near term.

Why Do Hyperscale Data Centers Lead the Market?

In 2026, hyperscale data centers are expected to make up the largest share of the hydrogen fuel cells market for data centers based on data center type. Companies like Microsoft, Google, Amazon, and Meta have the capital, technical know-how, and commitment to sustainability that position them as the main early users and partners for hydrogen fuel cell power systems in data centers. The IEA's Energy and AI report states that the capital spending of five major tech companies exceeded USD 400 billion in 2025 and is projected to rise by another 75% in 2026. This growth will create significant purchasing power for clean energy projects, including hydrogen fuel cells.

Microsoft's collaboration with Caterpillar and Ballard for the Cheyenne demonstration, Google's use of Bloom Energy SOFC systems at its data centers, and Equinix's fuel cell installations across its colocation sites show that the largest data center operators are actively testing and implementing hydrogen fuel cell technology. The scale of hyperscale data center construction also makes the higher initial costs of fuel cell systems viable compared to diesel. This is because spreading costs over a large installed power capacity decreases the per-megawatt premium compared to traditional options.

On the other hand, the edge data centers segment is expected to grow the fastest during this period. Edge data centers are often in remote or restricted areas where grid power is less reliable, diesel fuel logistics are complicated and expensive, and regulations on generator emissions are becoming stricter. These centers provide a strong opportunity to deploy hydrogen fuel cells, which can deliver clean, reliable backup or primary power without needing diesel storage, exhaust emissions, or the noise and vibration of traditional engines. The rise of edge computing for AI tasks, 5G functions, and applications that need low latency is increasing the number of edge data center installations in various regions, many of which face challenges with diesel-based power and are ideal for hydrogen fuel cell solutions.

Why Does Backup Power Lead the Application Market?

In 2026, the backup power and emergency power systems segment is expected to have the largest share of the hydrogen fuel cells for data centers market by application. Backup power is the most proven and easily available use for hydrogen fuel cells in data centers. It offers clear advantages over diesel generators, has specific technical requirements, and is backed by evidence from DOE-funded demos and commercial deployments by leading operators. The DOE's Hydrogen Fuel Cell Technologies Office has shown the benefits of fuel cells over diesel for backup power, including zero emissions during operation and testing, lower noise levels, longer runtime limited only by fuel supply instead of battery capacity, and reduced maintenance since there are no combustion engine parts. The January 2024 demonstration by Caterpillar, Microsoft, and Ballard confirmed that these benefits are possible in large-scale data centers under tough conditions.

On the other hand, the continuous primary power generation segment is set to grow the fastest during the forecast period. Using fuel cells as primary power sources for data centers taps into the biggest potential revenue opportunity in the market. Primary power systems run constantly and use hydrogen fuel all the time, not just during grid failures. Bloom Energy's SOFC installations at major tech firms prove that this application works on a large scale. Additionally, the rising interest from operators in clean, reliable on-site power as a replacement for grid electricity—given its carbon footprint and transmission costs—is increasing the appeal of fuel cells for primary power.

Why Do Cloud Service Providers Lead the End User Market?

In 2026, the cloud service providers segment is expected to hold the largest share of the hydrogen fuel cells market for data centers based on end users. Microsoft, Google, Amazon Web Services, and Meta are the leading developers of hydrogen fuel cell power programs for data centers. They are also the main channels for purchasing commercial fuel cell systems at a data center scale. These companies have made firm public promises to reduce carbon emissions in their data center operations. For example, Microsoft aims to be carbon negative by 2030 and plans to eliminate all the carbon it has ever emitted by 2050. Google intends to run all its data centers on 24/7 carbon-free energy by 2030. According to the IEA, these companies have committed to spending USD 320 billion on data center capital projects in 2025. This funding will help cover the higher initial cost of hydrogen fuel cell systems compared to diesel alternatives, especially when this investment supports their sustainability goals. The demonstration project by Microsoft, Caterpillar, and Ballard, as well as Google’s deployments with Bloom Energy, show the direct involvement of leading cloud providers with hydrogen fuel cell technology.

On the other hand, the government and defense data centers segment is expected to see significant growth during the forecast period. Government and military data centers have specific needs for reliable power continuity, aligning well with the benefits of hydrogen fuel cells. These benefits include long operation times without relying on grid power, no diesel fuel supply issues during emergency situations, lower emissions allowing for placement in regulated areas, and quiet operation that reduces noise at sensitive sites. The DOE’s Fuel Cell Technologies Office has supported fuel cell backup power demonstrations at military bases, such as Robins Air Force Base, through its ARRA program. This confirms that the government sector is increasingly interested in using fuel cell backup power for crucial facilities, including data centers.

How is North America Maintaining Market Leadership?

In 2026, North America is expected to have the largest share of the global hydrogen fuel cells market for data centers. The United States leads this market. It has the biggest concentration of hyperscale data center capacity. The active government research and demonstration program run by the DOE Hydrogen Fuel Cell Technologies Office also plays a key role. Furthermore, the significant commercial validation of the technology comes from the January 2024 demonstration by Caterpillar, Microsoft, and Ballard at the Microsoft data center in Cheyenne, Wyoming.

The DOE's Hydrogen Fuel Cell Technologies Office has put money into data center fuel cell applications through various programs. It held the Hydrogen and Fuel Cells for Data Center Applications Project Meeting in March 2019 as part of the H2@Scale initiative and has supported subsequent demonstration projects. The Bipartisan Infrastructure Law set aside USD 9.5 billion for clean hydrogen programs. This money will help create regional hydrogen hubs, which will boost domestic clean hydrogen production and distribution. This will benefit data center fuel cell operators by making hydrogen supply more accessible and reliable. The U.S. Inflation Reduction Act's Section 45V tax credit for clean hydrogen production offers up to USD 3 per kilogram for production at the lowest carbon intensity tier. This is encouraging the growth of green hydrogen production and will help lower fuel costs for data center fuel cell operators during the forecast period. Canada is also contributing to regional demand with increased data center investments and its National Hydrogen Strategy, which supports the rollout of fuel cell technology.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific is expected to see the highest growth rate in the hydrogen fuel cells for data centers market during the forecast period. This growth stems from Japan's strong hydrogen economy strategy, South Korea's government-led hydrogen plan, China's leading role in electrolyser manufacturing, and the region's rapidly growing data center construction pipeline.

According to the IEA's Global Hydrogen Review 2024, China makes up 60% of global electrolyser manufacturing capacity. China also leads in committed electrolyser projects, potentially representing nearly 70% of the electrolyser capacity installed in 2024. The IEA's Global Hydrogen Review 2025 confirmed that global water electrolysis capacity hit 2 GW in 2024, with most additions coming from China. China's strong position in electrolyser manufacturing is expected to lower electrolysis costs, similar to the trend seen with Chinese solar PV and battery manufacturing. This will gradually bring down the cost of green hydrogen as a fuel for data center fuel cell systems.

Japan's hydrogen strategy aims for a tenfold increase in hydrogen supply to 3 million tonnes per year by 2030. It has identified stationary fuel cells as a key application for commercial and government facilities. South Korea's Hydrogen Economy Roadmap aims for 15 GW of stationary fuel cell deployment by 2040. Singapore's expanding data center sector and interest in hydrogen imports from the Asia-Pacific region place it as an early adopter market for fuel cell data center power in Southeast Asia.

Some of the key companies operating in the global hydrogen fuel cells for data centers market are Bloom Energy Corporation, Ballard Power Systems Inc., Plug Power Inc., FuelCell Energy Inc., Cummins Inc., Doosan Fuel Cell Co. Ltd., Bosch Group, Siemens Energy AG, Caterpillar Inc., Microsoft Corporation, Equinix Inc., Google LLC, Vertiv Holdings Co., Schneider Electric SE, and Eaton Corporation plc.

The global hydrogen fuel cells for data centers market is expected to grow from USD 0.98 billion in 2026 to USD 4.64 billion by 2036.

The global hydrogen fuel cells for data centers market is projected to grow at a CAGR of 16.8% from 2026 to 2036.

The PEMFC segment is expected to dominate the overall market in 2026.

The backup power systems segment is expected to dominate the overall market in 2026.

North America is expected to lead the global market in 2026, anchored by U.S. hyperscale data center concentration, DOE Hydrogen Fuel Cell Technologies Office programs, and the January 2024 Caterpillar-Microsoft-Ballard commercial demonstration. Asia-Pacific is expected to witness the fastest CAGR, driven by China's 60% global electrolyser manufacturing share per the IEA, Japan's hydrogen strategy, and South Korea's fuel cell deployment targets.

The major players are Bloom Energy, Ballard Power Systems, Plug Power, FuelCell Energy, Cummins, Doosan Fuel Cell, Bosch Group, Siemens Energy, Caterpillar, Microsoft, Equinix, Google, Vertiv, Schneider Electric, and Eaton Corporation.

1. Introduction

1.1. Market Definition (Hydrogen Fuel Cell Power Systems for Data Centers)

1.2. Scope (Primary Power, Backup Power, Microgrids, Off-grid Data Centers)

1.3. Market Ecosystem

1.4. Currency and Limitations

1.4.1. Currency

1.4.2. Limitations

1.5. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research (Data Center Operators, Fuel Cell Manufacturers, Utilities, EPC Firms)

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Forecast Modeling

2.4. Data Triangulation

2.5. Assumptions

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Rising Power Demand from AI & Hyperscale Data Centers

4.2.1.2. Increasing Pressure for Carbon-neutral Data Centers

4.2.1.3. Limitations of Diesel Backup Generators

4.2.1.4. Government Support for Hydrogen Economy Development

4.2.2. Restraints

4.2.2.1. High Capital Costs of Fuel Cell Systems

4.2.2.2. Limited Hydrogen Infrastructure Availability

4.2.2.3. Fuel Storage & Transportation Challenges

4.2.3. Opportunities

4.2.3.1. Growth in Green Hydrogen Production

4.2.3.2. Integration with Renewable Energy & Microgrids

4.2.3.3. Expansion of Edge Data Centers

4.2.3.4. Development of On-site Hydrogen Generation

4.2.4. Challenges

4.2.4.1. Fuel Supply Reliability

4.2.4.2. Efficiency Optimization for Large-scale Deployments

4.3. Technology Landscape

4.3.1. Proton Exchange Membrane Fuel Cells (PEMFC)

4.3.2. Solid Oxide Fuel Cells (SOFC)

4.3.3. Molten Carbonate Fuel Cells (MCFC)

4.3.4. Phosphoric Acid Fuel Cells (PAFC)

4.3.5. Hydrogen Storage Technologies

4.3.6. Fuel Cell + Battery Hybrid Systems

4.4. Hydrogen Fuel Cells for Data Centers Ecosystem

4.4.1. Fuel Cell Manufacturers

4.4.2. Hydrogen Suppliers & Producers

4.4.3. Data Center Operators

4.4.4. EPC Contractors & Integrators

4.4.5. Utilities & Renewable Energy Providers

4.5. Value Chain Analysis

4.5.1. Hydrogen Production & Supply

4.5.2. Fuel Cell Manufacturing

4.5.3. System Integration

4.5.4. Deployment & Installation

4.5.5. Operations & Maintenance

4.6. Regulatory Landscape

4.6.1. Hydrogen Safety Standards

4.6.2. Emission Regulations for Data Centers

4.6.3. Renewable Energy & Hydrogen Incentives

4.6.4. Grid Interconnection Policies

4.7. Industry Trends

4.7.1. Replacement of Diesel Generators with Hydrogen Systems

4.7.2. Rise of AI-driven High-density Data Centers

4.7.3. Integration with Renewable-powered Microgrids

4.7.4. Growth of Zero-emission Data Centers

4.8. Cost and Pricing Analysis

4.8.1. Capex Analysis (Fuel Cells vs Diesel Backup)

4.8.2. Hydrogen Fuel Cost Analysis

4.8.3. Total Cost of Ownership (TCO)

5. Hydrogen Fuel Cells for Data Centers Market, by Fuel Cell Type

5.1. Introduction

5.2. Proton Exchange Membrane Fuel Cells (PEMFC) (Largest Segment)

5.3. Solid Oxide Fuel Cells (SOFC) (Fastest-growing)

5.4. Molten Carbonate Fuel Cells (MCFC)

5.5. Phosphoric Acid Fuel Cells (PAFC)

5.6. Other Fuel Cell Types

6. Hydrogen Fuel Cells for Data Centers Market, by Power Capacity

6.1. Below 500 kW

6.2. 500 kW to 1 MW

6.3. 1 MW to 5 MW

6.4. Above 5 MW

7. Hydrogen Fuel Cells for Data Centers Market, by Deployment Model

7.1. Backup Power Systems (Largest Segment)

7.2. Prime Power Systems

7.3. Combined Heat & Power (CHP) Systems

7.4. Microgrid-based Deployments

8. Hydrogen Fuel Cells for Data Centers Market, by Data Center Type

8.1. Hyperscale Data Centers

8.2. Colocation Data Centers

8.3. Enterprise Data Centers

8.4. Edge Data Centers

9. Hydrogen Fuel Cells for Data Centers Market, by Application

9.1. Introduction

9.2. Backup Power & Emergency Power Systems

9.3. Continuous Primary Power Generation

9.4. Peak Load Management

9.5. Renewable Energy Integration & Energy Storage

9.6. Off-grid / Remote Data Centers

10. Hydrogen Fuel Cells for Data Centers Market, by End User

10.1. Cloud Service Providers (CSPs)

10.2. Colocation Providers

10.3. Enterprises

10.4. Telecommunications Companies

10.5. Government & Defense Data Centers

11. Hydrogen Fuel Cells for Data Centers Market, by Geography

11.1. Introduction

11.2. North America

11.2.1. U.S.

11.2.2. Canada

11.3. Europe

11.3.1. Germany

11.3.2. U.K.

11.3.3. Netherlands

11.3.4. Ireland

11.3.5. Nordic Countries

11.3.6. France

11.3.7. Rest of Europe

11.4. Asia-Pacific

11.4.1. China

11.4.2. Japan

11.4.3. South Korea

11.4.4. Singapore

11.4.5. India

11.4.6. Australia

11.4.7. Rest of Asia-Pacific

11.5. Middle East & Africa

11.5.1. UAE

11.5.2. Saudi Arabia

11.5.3. South Africa

11.5.4. Rest of MEA

11.6. Latin America

11.6.1. Brazil

11.6.2. Mexico

11.6.3. Rest of Latin America

12. Competitive Landscape

12.1. Overview

12.2. Key Growth Strategies

12.3. Competitive Benchmarking

12.4. Competitive Dashboard

12.4.1. Industry Leaders

12.4.2. Technology Innovators

12.4.3. Emerging Players

12.5. Market Ranking/Positioning Analysis

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1. Bloom Energy Corporation

13.2. Ballard Power Systems Inc.

13.3. Plug Power Inc.

13.4. FuelCell Energy, Inc.

13.5. Cummins Inc.

13.6. Doosan Fuel Cell Co., Ltd.

13.7. Bosch Group

13.8. Siemens Energy AG

13.9. Caterpillar Inc.

13.10. Microsoft Corporation

13.11. Equinix, Inc.

13.12. Google LLC

13.13. Vertiv Holdings Co.

13.14. Schneider Electric SE

13.15. Eaton Corporation plc

14. Appendix

14.1. Customization Options

14.2. Related Reports

Published Date: Apr-2026

Published Date: Apr-2026

Published Date: Jun-2026

Subscribe to get the latest industry updates