Resources

About Us

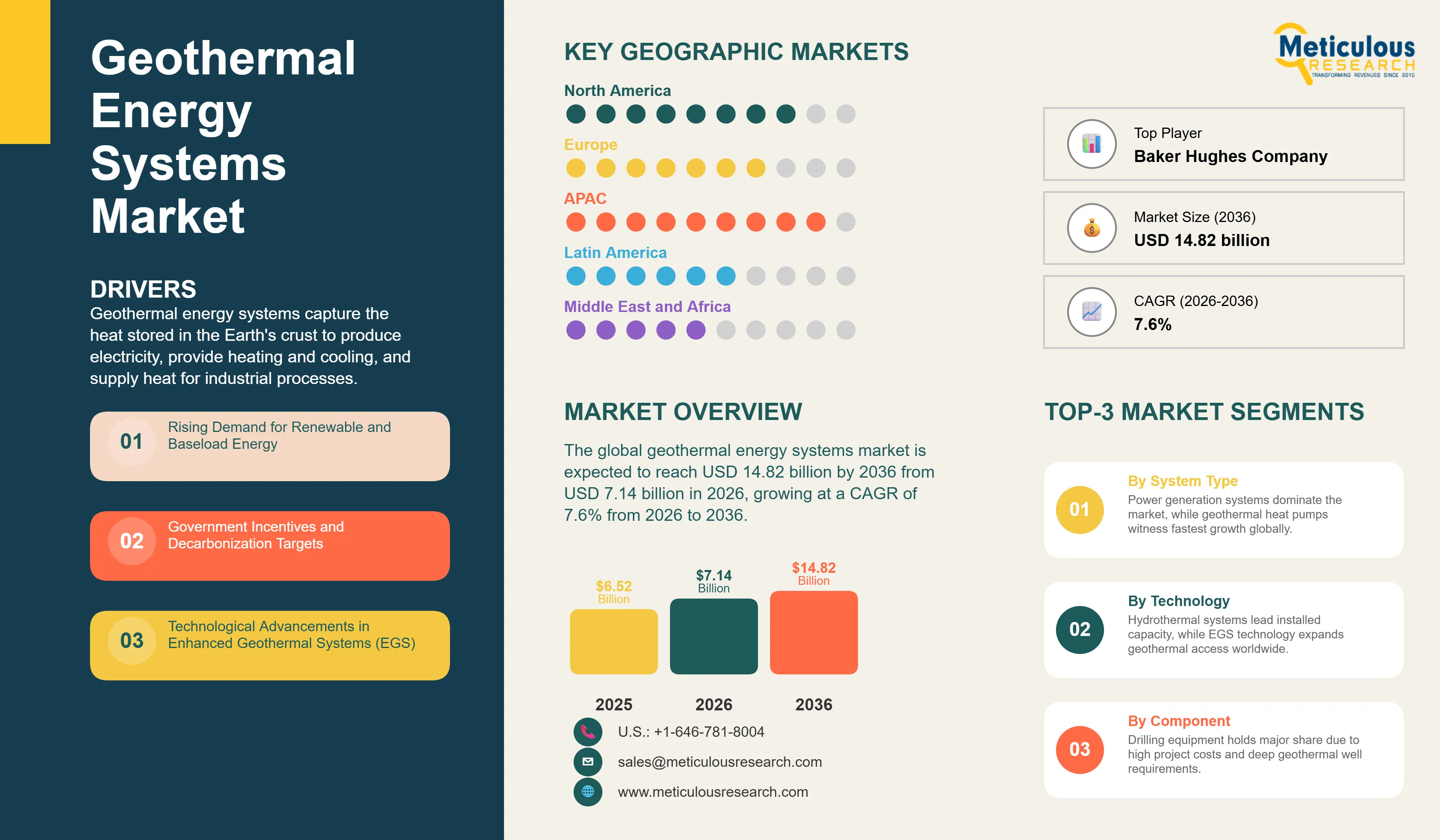

The global geothermal energy systems market was valued at USD 6.52 billion in 2025. This market is expected to reach USD 14.82 billion by 2036 from USD 7.14 billion in 2026, growing at a CAGR of 7.6% from 2026 to 2036.

The growth of this market is driven by geothermal energy's unique role among renewable sources. It is a reliable technology that can provide clean electricity and heat around the clock, no matter the weather or time of day. According to IRENA's Renewable Capacity Statistics 2025, total global installed geothermal power capacity reached 15.4 gigawatts by the end of 2024. This reflects an increase from about 13.0 gigawatts at the end of 2020. Currently, geothermal energy meets less than 1% of global energy demand, based on the IEA's 2024 report, the Future of Geothermal Energy. However, new improvements in enhanced geothermal systems and deeper drilling are opening up resources in countries that previously lacked access to conventional geothermal reservoirs. This expansion significantly broadens the global market.

The IEA's report, the Future of Geothermal Energy (2024), found that geothermal energy could meet 15% of the growth in global electricity demand between now and 2050. This is possible if project costs continue to drop, potentially reaching 800 gigawatts of installed capacity worldwide. This would provide an annual output equivalent to the current electricity demand of the United States and India combined. The IEA also estimated that total investment in geothermal could hit USD 1 trillion by 2035 and USD 2.5 trillion by 2050. Employment in the geothermal sector could increase sixfold, reaching 1 million jobs by 2030 if next-generation geothermal develops strongly. These projections rely on the combination of oil and gas drilling technology with geothermal resource development. The IEA noted that up to 80% of the investment needed for a geothermal project involves skills and capacity commonly found in the oil and gas industry.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Geothermal energy systems capture the heat stored in the Earth's crust to produce electricity, provide heating and cooling, and supply heat for industrial processes. These resources range from shallow, near-surface temperatures accessible through ground-source heat pumps at depths of just a few meters to a few hundred meters. They also include intermediate hydrothermal reservoirs at depths of 1 to 3 kilometers, where hot water or steam can be extracted for use in flash steam or binary cycle power plants. Additionally, there are deep, high-temperature resources at depths of 5 to 10 kilometers that next-generation enhanced geothermal systems aim to reach. The IEA's report, The Future of Geothermal Energy (2024), states that the global technical potential for enhanced geothermal system (EGS) electricity generation from resources within 8 kilometers of depth is more than 600 terawatts. This potential is almost 600 times greater than that of conventional hydrothermal geothermal and surpasses all renewable electricity sources except solar PV. The United States has the world's largest EGS technical potential at over 70 terawatts, which is about one-eighth of the global total, followed by China with approximately 50 terawatts.

The commercial geothermal energy market is built around five main system types. Power generation systems change geothermal steam or hot water into electricity using dry steam, flash steam, or binary cycle power plant setups. Installed capacities often range from a few megawatts to over 100 megawatts per plant. Direct use systems apply geothermal heat directly for space heating, greenhouse cultivation, aquaculture, industrial drying, and wellness applications without converting it into electricity. District heating systems distribute geothermal hot water through insulated pipelines to serve groups of buildings in urban or rural areas. Geothermal heat pumps rely on the stable shallow ground temperature as a thermal source for efficient heating and cooling of buildings. Enhanced geothermal systems create or improve permeability in hot, dry rock formations through hydraulic stimulation, allowing heat extraction in areas without natural hydrothermal fluid circulation.

The competitive landscape for geothermal energy includes integrated developers and operators like Ormat Technologies and Calpine Corporation. It also involves large energy companies with geothermal divisions such as Enel Green Power and Chevron. There are major engineering and equipment manufacturers like Mitsubishi Heavy Industries, Toshiba, Siemens Energy, and General Electric. Oilfield services companies, such as Baker Hughes, Halliburton, and SLB, bring their drilling expertise to geothermal projects. Nationally significant geothermal operators include KenGen in Kenya, Star Energy Geothermal in Indonesia, and Pertamina Geothermal Energy. According to the IEA's 2024 geothermal report, geothermal energy currently meets over 90% of heating demand in Iceland and makes up a significant portion of electricity supply in El Salvador, New Zealand, Kenya, and the Philippines. This underscores the commercial success of geothermal in countries with high resource quality and highlights the geographic challenges that next-generation technologies aim to address.

Enhanced Geothermal Systems Unlocking Vast Previously Inaccessible Resources

The development of enhanced geothermal systems, using drilling and reservoir stimulation technologies adapted from the oil and gas industry, is the most transformative trend in the geothermal energy market. It has the potential to turn geothermal energy from a location-specific niche into a globally available source of clean baseload energy. Conventional hydrothermal power development is limited to regions with naturally occurring hot water or steam reservoirs near the surface. This restricts commercial deployment to countries along tectonic boundaries or volcanic zones. EGS technology gets around this limitation by drilling deep wells into hot dry rock formations that exist in nearly all geologies at the right depth. It hydraulically stimulates the rock to create permeable fracture networks and circulates water through these networks to extract heat.

According to the IEA's The Future of Geothermal Energy (2024), EGS has the potential to meet global electricity and heat demand many times over. Just 1% of Africa's EGS potential could fulfill the continent's entire projected electricity demand for 2050. The IEA estimates that with policy support and lower technology costs, EGS expenses could drop by 80% by 2035, reaching around USD 50 per megawatt-hour. This would make geothermal one of the cheapest sources of dispatchable low-emissions electricity.

The oil and gas industry's involvement in EGS development is a key factor in this trend. The IEA's 2024 report stated that up to 80% of the investment needed for a geothermal project comes from skills and capacity common in oil and gas. These include subsurface characterization, well drilling and completion, fluid flow management, and large-scale project management. Companies like Baker Hughes, Halliburton, and SLB are actively creating geothermal-specific service offerings. The increased participation of oil and gas majors in geothermal exploration is providing capital, technical expertise, and supply chain infrastructure that the pure-play geothermal industry cannot access on its own.

IEA Projections for Historic Geothermal Capacity Growth by 2030

According to the IEA's Renewables 2025 report, annual geothermal capacity additions are expected to reach a historic high in 2030. This would be three times the 0.4 GW added in 2024, driven by growth in the United States, Indonesia, Japan, Turkey, Kenya, and the Philippines. This projection shows a clear increase from the slow capacity growth of recent years, when geothermal additions lagged behind solar and wind. The IEA's forecast relies on a growing project development pipeline in these key markets, government programs that support geothermal development, and the progress of EGS technology toward commercial use. In the United States, the Department of Energy's Enhanced Geothermal Shot initiative aims to lower EGS costs to USD 45 per megawatt-hour by 2035. The DOE has also funded several EGS demonstration programs, including the FORGE project in Utah, which is providing key data for commercial EGS development. IRENA's April 2026 data confirmed that geothermal capacity added 0.3 GW in 2025, led by the Philippines, Indonesia, Germany, Turkey, and Japan. This shows steady, though modest, growth momentum ahead of the expected increase in 2030.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 14.82 Billion |

|

Market Size in 2026 |

USD 7.14 Billion |

|

Market Size in 2025 |

USD 6.52 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 7.6% |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

System Type, Technology, Component, Deployment Mode, Application, End User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Driver: Geothermal Energy's Baseload Dispatchability Advantage in Variable Renewable Energy Grids

The main driver of the geothermal energy systems market is the technology's unique feature as a baseload, dispatchable renewable energy source. It can deliver a steady power output at high capacity factors, no matter the weather or time of day. According to the IEA's The Future of Geothermal Energy (2024), geothermal plants operate at capacity factors around 80%. This is much higher than solar PV, which operates at about 15-25%, and onshore wind, at 25-40%. As a result, geothermal acts as a dependable resource that helps balance the grid alongside variable solar and wind output.

As the share of variable renewable energy in power grids increases globally to meet decarbonization goals, the importance of dispatchable clean energy sources rises. This trend creates a growing demand for geothermal power. The IEA's Renewables 2025 report predicts that global renewable capacity will double between now and 2030, with solar and wind making up most of the additions. This rise in variable renewables will boost the need for flexible and baseload clean energy options to keep the grid stable. Geothermal's capability to provide baseload clean power in areas with available resources makes it an increasingly valuable asset as energy systems work toward decarbonization.

Opportunity: Industrial Heat Decarbonization Applications

The decarbonization of industrial process heat offers a valuable opportunity for geothermal energy systems in the medium-temperature range of 80 to 200 degrees Celsius. Industries like food and beverage processing, paper and pulp manufacturing, chemical production, and agricultural drying need large amounts of thermal energy at temperatures that medium-enthalpy geothermal resources can provide directly. This approach keeps the thermodynamic value of the geothermal resource intact and avoids efficiency losses associated with generating electricity and using electric heating.

According to the IEA's The Future of Geothermal Energy (2024), using geothermal heat directly for industrial applications is gaining attention. Industrial companies face rising carbon prices and pressure to cut Scope 1 emissions from burning fossil fuels for heat. Countries like Iceland already supply geothermal heat to fish processing, aluminum smelting, and data centers. New Zealand also uses geothermal heat in processing forestry products. These examples show how large-scale geothermal industrial heat supply can work. Other countries with moderate-temperature geothermal resources are looking to follow this model.

Why Do Power Generation Systems Lead the Market?

In 2026, the power generation systems segment is expected to hold the largest share of the geothermal energy systems market. Geothermal power plants are the most expensive installations in the geothermal sector. Utility-scale projects need an investment of USD 3 million to USD 8 million for each installed megawatt in conventional hydrothermal plants, and significantly more for next-generation EGS installations. The global installed geothermal power capacity of 15.4 GW reported by IRENA at the end of 2024 reflects decades of investment in power plant infrastructure across the United States, Indonesia, Philippines, Kenya, Mexico, Italy, Iceland, and New Zealand. Each operational power plant generates ongoing revenue for equipment suppliers and service providers through operations and maintenance contracts, spare parts purchases, and periodic upgrades. The main markets for geothermal power generation systems are in countries with the best hydrothermal resources. IRENA data shows that geothermal energy covers a large share of national electricity demand, including over 90% of heating in Iceland and significant contributions to grid electricity in Kenya and the Philippines.

However, the geothermal heat pumps segment is expected to grow the fastest during the forecast period. Ground-source heat pump systems use the steady temperature of shallow ground or groundwater as a thermal reservoir for heating and cooling buildings. They operate independently of high-temperature geothermal resources, making them available in almost any region. The European Union's heat pump policy framework, including strong support from the REPowerEU plan for heat pump deployment to reduce dependence on natural gas for building heating, is driving rapid growth in ground-source heat pump installations across Germany, France, the Netherlands, and Sweden. The high energy efficiency, recognized by IRENA as providing three to five units of heating energy for each unit of electrical energy used, combined with compatibility with low-carbon electricity from renewable sources, makes geothermal heat pumps one of the most effective technologies for decarbonizing buildings.

Why Do Hydrothermal Systems Lead the Technology Market?

In 2026, the hydrothermal systems segment is expected to have the largest share of the geothermal energy systems market by technology. Conventional hydrothermal systems tap into naturally occurring geothermal reservoirs where hot water or steam is available at exploitable temperatures and flow rates. This represents the established technology base of the global geothermal industry and accounts for nearly all of the 15.4 GW of installed geothermal power capacity reported by IRENA at the end of 2024. The hydrothermal resource base in countries with high-quality geothermal resources supports large power plants that can operate for 30 to 50 years. This generates ongoing revenue from equipment and services at established project sites. Countries like the United States, which has the largest geothermal power fleet in the world, along with Indonesia, the Philippines, Kenya, Italy, and Mexico have the most developed hydrothermal resources. They are the main demand centers for hydrothermal power plant equipment, well drilling services, and plant operations technology.

However, the enhanced geothermal systems segment is expected to grow the fastest during the forecast period. According to the IEA's The Future of Geothermal Energy (2024), EGS technology could turn geothermal energy from a niche resource into a globally available clean energy source. The IEA estimates that EGS has the technical potential to provide nearly 600 TW of capacity from resources within 8 km depth. They also estimated that with the right policy support, EGS costs could drop by 80% by 2035 to around USD 50 per MWh, making it one of the cheapest sources of dispatchable low-emissions electricity. The U.S. Department of Energy's Enhanced Geothermal Shot initiative and the DOE-funded FORGE demonstration site in Utah are producing technical data and reducing drilling costs. This will help commercialize EGS at scale during the forecast period.

Why Does Drilling Equipment Lead the Component Market?

In 2026, the drilling equipment segment is expected to have the largest share of the geothermal energy systems market by component. Drilling makes up the largest cost in a geothermal project, usually accounting for 30% to 50% of the total project capital cost. Therefore, the drilling equipment market captures the biggest share of total geothermal capital spending. According to the IEA's The Future of Geothermal Energy (2024), permitting and administrative processes can delay the commissioning of a new geothermal project by up to a decade. Drilling cost and performance are the main technical and economic challenges affecting project economics. Geothermal wells are drilled to depths of 1 to 5 kilometers for conventional hydrothermal projects and potentially 5 to 10 kilometers for next-generation EGS projects. These projects require specialized high-temperature drilling rigs, drill bits designed to handle tough hard rock at high temperatures, and wellbore casing systems rated for extreme downhole conditions. Baker Hughes, Halliburton, and SLB are the main providers of drilling equipment and services for the geothermal market. They adapt oilfield technology specifically for geothermal use.

On the other hand, the control systems and monitoring software segment is expected to see the fastest growth during the forecast period. The digitalization of geothermal plant operations through better process control systems, real-time monitoring of well and reservoir performance, predictive maintenance analytics, and remote operations management is becoming standard for modern geothermal project development. The IEA's 2024 geothermal report pointed out that digital monitoring and optimization is a key trend that helps geothermal operators improve plant availability, optimize heat extraction from reservoirs over long periods, and lower operations and maintenance costs. As the EGS segment expands and requires more sophisticated subsurface management compared to conventional hydrothermal operations, the need for advanced monitoring and control software in geothermal applications is projected to grow significantly.

How Does Large-scale Utility-scale Lead the Market?

In 2026, the large-scale utility-scale segment is expected to have the largest share of the geothermal energy systems market by deployment mode. Utility-scale geothermal power plants with a capacity of 10 megawatts and above are the most common form of commercial geothermal energy used worldwide. They account for the majority of the 15.4 GW of installed geothermal power capacity reported by IRENA at the end of 2024. Utility-scale projects achieve cost savings in drilling, plant construction, and grid connection. This makes them the most cost-effective option for high-enthalpy hydrothermal resources where fluid temperature and flow rate are adequate for large installations. Major geothermal companies, including Ormat Technologies, Enel Green Power, Calpine, and Pertamina Geothermal Energy, build and operate utility-scale plants typically ranging from 30 to 250 megawatts. The largest geothermal complexes in the United States exceed 700 megawatts in total installed capacity.

However, the small-scale and distributed systems segment is expected to grow the fastest during the forecast period. The rise of ground-source heat pump installations in homes and commercial buildings, the development of small binary cycle power plants for distributed power supply in remote communities, and increasing interest in distributed direct-use geothermal heating systems for industrial and agricultural uses are all contributing to growth in the small-scale segment. The recognized maturity of geothermal heat pump technology for building applications allows for broad deployment of distributed geothermal systems across various locations. This is possible without the high-temperature reservoir requirements that utility-scale power plants have, making small-scale geothermal the most accessible segment of the market.

Why Does Power Generation Lead the Application Market?

In 2026, the power generation segment is expected to hold the largest share of the geothermal energy systems market by application. Geothermal electricity generation is the most valuable commercial use of geothermal energy. It has driven capital investment in geothermal infrastructure worldwide for over a century. The IEA's The Future of Geothermal Energy (2024) confirms that geothermal power generation meets a significant portion of electricity demand in Iceland, El Salvador, New Zealand, Kenya, and the Philippines. These markets show the commercial reliability and long-term performance of geothermal power systems. The IEA's Renewables 2025 report predicts that annual geothermal capacity additions will triple by 2030 compared to the 0.4 GW added in 2024. This reflects a positive growth outlook for the power generation application and the demand for related equipment and services.

However, the industrial applications segment is expected to grow the fastest during the forecast period. The decarbonization of industrial process heat is becoming an important growth area for medium-temperature geothermal resources. This shift is driven by rising carbon pricing in major industrial economies, corporate commitments to net-zero emissions, and the cost-effectiveness of geothermal heat for energy-intensive industries. The IEA's 2024 geothermal report identifies industrial heat decarbonization as a major opportunity for geothermal development. Advances in drilling and enhanced geothermal systems technology are increasing the availability of medium-enthalpy geothermal resources at shallower depths. This is expanding the geographic reach of geothermal heat that is useful for industrial applications.

Why Do Utilities and Power Companies Lead the End User Market?

In 2026, the utilities and power companies segment is expected to hold the largest share of the geothermal energy systems market. Electric utilities and independent power producers are the main developers, owners, and operators of geothermal power plants worldwide. They serve as the primary source for purchasing the high-cost equipment, drilling services, and long-term operations and maintenance contracts that make up most of the geothermal market revenue. National utilities like KenGen in Kenya operate the largest geothermal power fleet in Africa, with about 863 megawatts of installed capacity at the Olkaria geothermal field. Other major operators include state-owned enterprises like Pertamina Geothermal Energy in Indonesia and PNOC Renewables Corporation in the Philippines. Private utilities and IPPs, such as Ormat Technologies, Calpine Corporation, and Contact Energy in New Zealand, develop and manage geothermal power assets through long-term power purchase agreements with grid operators.

However, the commercial sector segment is expected to grow the fastest during the forecast period. Commercial buildings, including offices, hotels, retail centers, and institutions, are becoming an important end-user segment for both geothermal heat pump systems and direct-use geothermal district heating connections. The increasing sustainability commitments of large commercial real estate owners, along with stricter energy efficiency regulations for commercial buildings in Europe and North America, are driving the purchase of ground-source heat pump systems as a key technology for heating and cooling. The high efficiency of geothermal heat pumps, recognized by IRENA, delivers three to five units of heating energy for each unit of electricity used. This provides a strong economic and environmental argument for the adoption of geothermal systems in markets where electricity grids are increasingly powered by low-carbon energy.

How is Asia-Pacific Maintaining Market Leadership?

In 2026, Asia-Pacific is expected to have the largest share of the global geothermal energy systems market. This region includes two of the biggest geothermal power producers by installed capacity, Indonesia and the Philippines. It also features Japan's growing geothermal development program and China's increasing use of geothermal heat. Indonesia has some of the most productive high-enthalpy hydrothermal resources along the Pacific Ring of Fire. Pertamina Geothermal Energy and Star Energy Geothermal operate major power complexes there. The Philippines also enjoys excellent hydrothermal resources, with geothermal energy accounting for about 10% of the country's electricity generation.

According to IRENA's Renewable Capacity Statistics 2025, New Zealand led geothermal capacity additions in 2024, followed by Indonesia, Turkey, and the United States. IRENA's data from April 2026 confirmed that geothermal added 0.3 GW in 2025, with the Philippines and Indonesia each contributing 0.1 GW of new capacity. The IEA's report, The Future of Geothermal Energy (2024), states that ASEAN countries together represent about 15% of global EGS technical potential, with Indonesia and the Philippines at the forefront of the regional assessment. The IEA's Renewables 2025 report identified Indonesia and the Philippines as two of the six countries expected to drive the planned tripling of annual geothermal additions by 2030, along with the United States, Japan, Turkey, and Kenya.

How is North America Contributing to Global Market Growth?

North America is set to have the second largest regional share of the global geothermal energy systems market by 2026. This is largely due to the United States being the biggest geothermal power market in the world, with the highest installed geothermal capacity of any country. The U.S. has the largest technical EGS potential globally, exceeding 70 terawatts, which is about one-eighth of the total worldwide, according to the IEA's 2024 analysis. This underscores the long-term growth potential of the U.S. geothermal market, which far exceeds its current capacity. The U.S. Department of Energy's Enhanced Geothermal Shot initiative aims to reduce EGS costs to USD 45 per MWh by 2035. Additionally, the DOE-funded FORGE site in Utah is producing key technical data for EGS. The IEA's Renewables 2025 report lists the United States as one of six key markets expected to contribute to the projected tripling of annual geothermal capacity additions by 2030. The Inflation Reduction Act’s investment tax credit for geothermal energy and the production tax credit for geothermal power offer financial incentives that are improving project financing for new geothermal development across the United States. Canada also plays a role in regional demand through geothermal direct-use applications and new power development projects in British Columbia and the western provinces.

Some of the key companies operating in the global geothermal energy systems market are Ormat Technologies, Inc., Calpine Corporation, Enel Green Power S.p.A., Chevron Corporation, Mitsubishi Heavy Industries Ltd., Siemens Energy AG, Toshiba Energy Systems & Solutions Corporation, General Electric Company, Baker Hughes Company, Halliburton Company, SLB (Schlumberger), KenGen (Kenya Electricity Generating Company), Contact Energy Ltd., Star Energy Geothermal, and Pertamina Geothermal Energy.

The global geothermal energy systems market is expected to grow from USD 7.14 billion in 2026 to USD 14.82 billion by 2036.

The global geothermal energy systems market is projected to grow at a CAGR of 7.6% from 2026 to 2036.

The power generation systems segment is expected to dominate the overall market in 2026. However, the geothermal heat pumps segment is expected to witness the fastest CAGR, driven by building heating decarbonization policy across Europe and North America and the broad geographic availability of shallow ground-source heat resources independently of high-temperature hydrothermal reservoirs.

The hydrothermal systems segment is expected to dominate the overall market in 2026, accounting for virtually all of the 15.4 GW of global installed geothermal power capacity reported by IRENA at end-2024. However, the enhanced geothermal systems segment is expected to witness the fastest CAGR, supported by the IEA's projection that EGS costs could fall 80% by 2035 and the U.S. DOE's Enhanced Geothermal Shot initiative targeting USD 45 per MWh by 2035.

Asia-Pacific is expected to lead the global market in 2026, driven by Indonesia's and the Philippines' large hydrothermal fleets. Asia-Pacific is also expected to witness the fastest CAGR, with the IEA projecting Indonesia, Japan, and the Philippines among the six key countries driving a tripling of annual geothermal additions by 2030 per its Renewables 2025 report.

According to the IEA's The Future of Geothermal Energy (2024), geothermal could meet 15% of global electricity demand growth to 2050 and reach 800 GW of installed capacity, delivering output equivalent to the current combined electricity demand of the United States and India. Total geothermal investment could reach USD 1 trillion by 2035 and USD 2.5 trillion by 2050, with sector employment potentially growing sixfold to 1 million jobs by 2030.

The major players are Ormat Technologies, Calpine Corporation, Enel Green Power, Chevron, Mitsubishi Heavy Industries, Siemens Energy, Toshiba Energy Systems, General Electric, Baker Hughes, Halliburton, SLB, KenGen, Contact Energy, Star Energy Geothermal, and Pertamina Geothermal Energy.

1. Introduction

1.1 Market Definition (Geothermal Energy Systems & Heat Utilization Technologies)

1.2 Scope (Power Generation, Direct Heating, District Heating, Industrial Applications)

1.3 Market Ecosystem

1.4 Currency and Limitations

1.4.1 Currency

1.4.2 Limitations

1.5 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation

2.2.1 Secondary Research

2.2.2 Primary Research (Energy Companies, EPC Firms, Utilities, Regulators)

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Forecast Modeling

2.4 Data Triangulation

2.5 Assumptions

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Rising Demand for Renewable and Baseload Energy

4.2.1.2 Government Incentives and Decarbonization Targets

4.2.1.3 Technological Advancements in Enhanced Geothermal Systems (EGS)

4.2.1.4 Growing Demand for District Heating

4.2.2 Restraints

4.2.2.1 High Initial Capital Costs

4.2.2.2 Site-specific Resource Availability

4.2.2.3 Exploration Risks

4.2.3 Opportunities

4.2.3.1 Development of EGS and Deep Geothermal Technologies

4.2.3.2 Integration with Hybrid Renewable Systems

4.2.3.3 Expansion in Emerging Markets

4.2.3.4 Industrial Heat Decarbonization

4.2.4 Challenges

4.2.4.1 Drilling Complexity and Costs

4.2.4.2 Environmental Concerns (Seismicity, Water Use)

4.3 Technology Landscape

4.3.1 Hydrothermal Systems

4.3.2 Enhanced Geothermal Systems (EGS)

4.3.3 Binary Cycle Power Plants

4.3.4 Flash Steam Power Plants

4.3.5 Dry Steam Power Plants

4.3.6 Geothermal Heat Pumps

4.4 Geothermal Energy Ecosystem

4.4.1 Project Developers & Operators

4.4.2 EPC Contractors

4.4.3 Equipment Manufacturers

4.4.4 Utilities & Power Producers

4.4.5 Government & Regulatory Bodies

4.5 Value Chain Analysis

4.5.1 Resource Exploration

4.5.2 Drilling & Well Development

4.5.3 Plant Construction

4.5.4 Power Generation / Heat Distribution

4.5.5 Operations & Maintenance

4.6 Regulatory Landscape

4.6.1 Renewable Energy Policies & Incentives

4.6.2 Environmental Regulations

4.6.3 Licensing & Permitting

4.7 Industry Trends

4.7.1 Growth of Enhanced Geothermal Systems

4.7.2 Integration with Energy Storage

4.7.3 Hybrid Renewable Energy Projects

4.7.4 Digital Monitoring & Optimization

4.8 Cost and Pricing Analysis

4.8.1 Capex & Opex Breakdown

4.8.2 Levelized Cost of Energy (LCOE)

4.8.3 Cost by Technology Type

5. Geothermal Energy Systems Market, by System Type

5.1 Introduction

5.2 Power Generation Systems

5.3 Direct Use Systems (Heating & Cooling)

5.4 District Heating Systems

5.5 Geothermal Heat Pumps

6. Geothermal Energy Systems Market, by Technology

6.1 Hydrothermal Systems

6.2 Enhanced Geothermal Systems (EGS)

6.3 Binary Cycle Technology

6.4 Flash Steam Technology

6.5 Dry Steam Technology

7. Geothermal Energy Systems Market, by Component

7.1 Introduction

7.2 Drilling Equipment

7.2.1 Rigs

7.2.2 Drill Bits

7.3 Surface Equipment

7.3.1 Turbines

7.3.2 Generators

7.3.3 Heat Exchangers

7.4 Pumps & Valves

7.5 Control Systems & Monitoring Software

8. Geothermal Energy Systems Market, by Deployment Mode

8.1 Large-scale (Utility-scale)

8.2 Small-scale / Distributed Systems

9. Geothermal Energy Systems Market, by Application

9.1 Introduction

9.2 Power Generation

9.3 Residential Heating & Cooling

9.4 Commercial Heating & Cooling

9.5 Industrial Applications (Process Heat)

9.6 Agriculture (Greenhouses, Aquaculture)

10. Geothermal Energy Systems Market, by End User

10.1 Utilities & Power Companies

10.2 Industrial Sector

10.3 Commercial Sector

10.4 Residential Sector

11. Geothermal Energy Systems Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 Iceland

11.3.3 Italy

11.3.4 France

11.3.5 Netherlands

11.3.6 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 Japan

11.4.3 Indonesia

11.4.4 Philippines

11.4.5 Australia

11.4.6 India

11.4.7 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Mexico

11.5.2 Chile

11.5.3 Rest of Latin America

11.6 Middle East & Africa

11.6.1 Kenya

11.6.2 Turkey

11.6.3 Saudi Arabia

11.6.4 Rest of MEA

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Technology Innovators

12.4.3 Emerging Players

12.5 Market Ranking/Positioning Analysis

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 Ormat Technologies, Inc.

13.2 Calpine Corporation

13.3 Enel Green Power S.p.A.

13.4 Chevron Corporation

13.5 Mitsubishi Heavy Industries, Ltd.

13.6 Siemens Energy AG

13.7 Toshiba Energy Systems & Solutions Corporation

13.8 General Electric Company

13.9 Baker Hughes Company

13.10 Halliburton Company

13.11 SLB (Schlumberger)

13.12 KenGen (Kenya Electricity Generating Company)

13.13 Contact Energy Ltd.

13.14 Star Energy Geothermal

13.15 Pertamina Geothermal Energy

14. Appendix

14.1 Customization Options

14.2 Related Reports

Published Date: Jul-2024

Published Date: Jun-2023

Subscribe to get the latest industry updates