Resources

About Us

Electric Actuators Market Size, Share & Trends Analysis, by Product Type, Control Type, Voltage, End-use Industry, and Geography — Global Opportunity Analysis & Forecast (2026–2036)

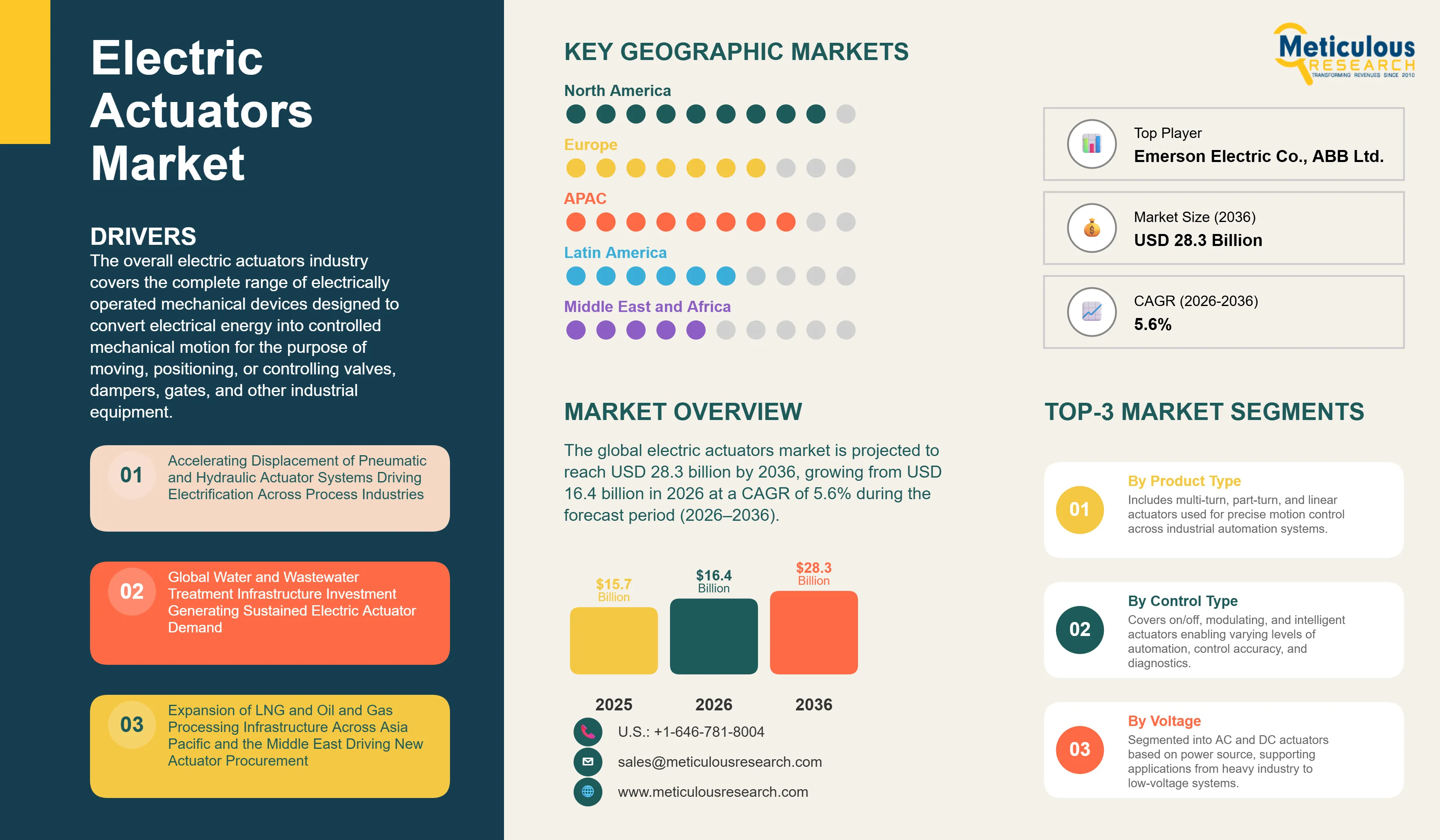

Report ID: MREP - 1041952 Pages: 273 May-2026 Formats*: PDF Category: Energy and Power Delivery: 24 to 72 Hours Download Free Sample ReportThe global electric actuators market was valued at USD 15.7 billion in 2025. The market is projected to reach USD 28.3 billion by 2036, growing from USD 16.4 billion in 2026 at a CAGR of 5.6% during the forecast period (2026–2036).

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The overall electric actuators industry covers the complete range of electrically operated mechanical devices designed to convert electrical energy into controlled mechanical motion for the purpose of moving, positioning, or controlling valves, dampers, gates, and other industrial equipment. The market includes multi-turn electric actuators, part-turn electric actuators, and linear electric actuators deployed across a wide range of end-use industries including oil and gas, power generation, water and wastewater treatment, chemical and petrochemical processing, automotive and electric vehicle manufacturing, aerospace and defense, food and beverage processing, and HVAC and building automation. The International Energy Agency (IEA) reports that electric motor systems currently account for about 53% of global electricity consumption, rising toward ~70% in industrial applications; this embeds a strong policy push to improve efficiency of motor‑driven equipment, including actuators.

These devices play an important role in process control and industrial automation by delivering accurate, repeatable, and remotely managed mechanical positioning. This precision is essential for maintaining pipeline safety, improving production efficiency, meeting regulatory standards, and optimizing overall processes. Electric actuators are offered in a broad spectrum of control configurations from basic on/off operation to proportional modulation and advanced digital systems with built-in diagnostics and support for fieldbus communication protocols such as HART, Foundation Fieldbus, Profibus, Modbus, EtherNet/IP, and PROFINET. They are manufactured in standard designs for general industrial use, as well as in specialized versions that are explosion-proof, weather-resistant, or submersible, making them suitable for hazardous areas, outdoor environments, and subsea applications.

The growth of the electric actuators market is primarily driven by the growing displacement of pneumatic and hydraulic actuator systems across process industries, as industrial operators increasingly prioritize the energy efficiency, installation simplicity, precise positioning performance, and remote monitoring capabilities that electric actuation platforms offer compared to compressed air and hydraulic fluid-based alternatives. The total energy inefficiency of compressed air generation and distribution, where compressor drive losses typically result in only 10 to 15 percent useful work delivery at the actuation point, is now under intense scrutiny as industrial operators pursue decarbonization commitments and seek to reduce operational energy expenditure under increasingly stringent energy efficiency mandates in North America, Europe, and Asia Pacific.

The increasing adoption of IIoT platforms in process plants has significantly strengthened the investment case for electric actuators, as modern intelligent electric actuator units from manufacturers including Rotork plc, AUMA Riester GmbH & Co. KG, and Flowserve Corporation now offer embedded diagnostic sensors, remote configuration interfaces, and predictive maintenance data streams that integrate directly with plant distributed control systems and asset management platforms. This connectivity allows plant operators to move away from time-based maintenance schedules toward condition-based maintenance programs that reduce unplanned downtime and optimize operational costs across large installed actuator fleets.

Global investment in water and wastewater treatment infrastructure is providing a broad and structurally expanding demand base for electric actuators, particularly in the context of water scarcity concerns, urbanization-driven municipal water system expansion, and the regulatory tightening of discharge quality standards across both developed and developing economies. The International Water Association estimates that global capital investment in water infrastructure needs to reach approximately USD 1 trillion annually through 2030 to meet safe water and sanitation goals, directly driving demand for electric actuators used in water intake, treatment, distribution, and wastewater collection and processing operations. In parallel, the global expansion of LNG infrastructure, including export and import terminal construction, regasification plant development, and long-distance gas pipeline projects across North America, the Middle East, and Asia Pacific, is generating sustained demand for explosion-proof and SIL-rated multi-turn and part-turn electric actuators in high-consequence process control applications.

In addition to these sector-specific drivers, the broader shift toward industrial automation is significantly expanding the market for precision linear electric actuators. The rapid expansion of electric vehicle battery manufacturing, advanced production facilities, and automated logistics and warehousing systems worldwide is extending their use beyond traditional process control into an increasingly diverse set of industrial applications.

Despite strong growth fundamentals, the market faces challenges related to the comparatively higher upfront procurement cost of electric actuator systems relative to pneumatic alternatives, particularly in applications with existing compressed air infrastructure where the incremental cost of switching to electric actuation must be justified against established operational practice. Technical challenges including heat management in high-cycle-rate applications, battery backup system requirements for fail-safe operation in power loss scenarios, and the complexity of commissioning intelligent actuator systems with multiple fieldbus protocol options continue to influence procurement decisions and total cost of ownership calculations for industrial buyers.

Stricter functional safety requirements under IEC 61508 and IEC 61511, along with the growing adoption of Safety Integrity Level (SIL) certifications in oil, gas, and chemical processing, are creating strong growth prospects for electric actuator manufacturers that offer SIL-rated products and proven functional safety expertise. At the same time, the rapid global expansion of renewable energy—particularly utility-scale solar and wind projects, where actuators are used for solar tracking and turbine pitch and yaw control—is establishing a new and steadily growing demand segment. Additionally, the increasing implementation of Industry 4.0 and digital twin technologies in process plants is driving investment in intelligent electric actuators capable of delivering real-time position and diagnostic data to support advanced digital operations.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 28.3 Billion |

|

Market Size in 2026 |

USD 16.4 Billion |

|

Market Size in 2025 |

USD 15.7 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 5.6% |

|

Dominating Product Type |

Multi-turn Electric Actuators |

|

Fastest Growing Product Type |

Linear Electric Actuators |

|

Dominating Control Type |

On/Off Electric Actuators |

|

Fastest Growing Control Type |

Intelligent Electric Actuators |

|

Dominating Voltage |

AC Electric Actuators |

|

Fastest Growing Voltage |

DC Electric Actuators |

|

Dominating End-use Industry |

Oil and Gas |

|

Fastest Growing End-use Industry |

Water and Wastewater Treatment |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Accelerating Displacement of Pneumatic and Hydraulic Actuator Systems Across Process Industries Driven by Electrification and Energy Efficiency Mandates

The sustained and accelerating shift away from pneumatic and hydraulic actuator systems toward electric alternatives across process industries represents the most significant structural demand driver in the global electric actuators market. Pneumatic actuators have historically dominated valve control applications in oil and gas, chemical processing, and power generation facilities, benefiting from their simplicity, speed, and compatibility with existing compressed air infrastructure. However, the total energy inefficiency of compressed air generation and distribution is now under intense scrutiny as industrial operators pursue decarbonization commitments and seek to reduce operational energy expenditure against increasingly stringent regulatory benchmarks. IEA‑4E and DOE‑sponsored studies confirm that compressed‑air systems typically have very low effective utilization efficiency, with only about 10–15% of compressor‑input energy converted into useful mechanical work at the actuator, whereas modern electric motor systems achieve 85–90% efficiency at the drive point. Policy documents such as the OECD‑IEA “Energy Technology Transitions for Industry” and IEA “Energy Efficiency 2025” explicitly promote the replacement of inefficient pneumatic auxiliary systems with high‑efficiency electric drives, including electric actuators, to reduce industrial energy intensity and assist decarbonization.

The European Union's revised Industrial Emissions Directive, the ongoing development of energy efficiency requirements under the EU Ecodesign Regulation framework, and the U.S. Department of Energy's Industrial Decarbonization Roadmap, which outlines sector-specific efficiency improvement targets across energy-intensive manufacturing sectors, are collectively compelling industrial operators to audit and reduce auxiliary energy consumption, including compressed air system losses. Electric actuators, which convert electrical energy to mechanical motion at efficiencies typically exceeding 85 percent, present a compelling operational cost reduction case in these environments, particularly as electricity prices in many industrial markets have stabilized relative to the variable operating cost of maintaining compressed air systems at required pressure and purity levels.

Beyond energy efficiency, the adoption of electric actuation is being reinforced by the superior positioning precision, programmability, and remote controllability of modern electric actuator platforms relative to pneumatic systems. In applications such as control valve modulation for flow, pressure, and temperature regulation in chemical and pharmaceutical processes, electric actuators with integrated positioners and closed-loop feedback control provide positioning repeatability and diagnostic capabilities that pneumatic systems cannot match without significant additional instrumentation investment. This performance advantage is increasingly compelling to plant operators investing in digital process control platforms, where the data richness of intelligent electric actuators directly supports model-based process optimization and advanced process control initiatives.

Integration of IIoT Connectivity and Predictive Diagnostics Reshaping Electric Actuator Performance Management and Service Models

The integration of industrial IoT sensors, embedded diagnostics, and cloud-connected monitoring capabilities into electric actuator platforms is fundamentally transforming both the operational model of actuator ownership and the competitive positioning of leading manufacturers in the global market. Traditionally, electric actuators functioned largely as standalone electromechanical devices, with maintenance carried out at fixed intervals based on operating hours or calendar schedules regardless of actual device condition. This approach led to unnecessary preventive maintenance expenditures in well-functioning units while failing to anticipate impending failures in devices experiencing abnormal operating conditions. The IEA‑4E Electric Motor Systems Annex and IEA “Energy Efficiency 2025” highlight that sensor‑embedded, digitally connected actuators support predictive‑maintenance and condition‑based schemes, which can reduce maintenance costs and unplanned downtime by 15–30% in industrial applications. NAMUR NE 107 and IEC‑4E guideline documents treat self‑monitoring and diagnostics in field devices (including actuators) as a minimum expectation for modern process plants, reinforcing the investment case for intelligent electric actuators.

Modern intelligent electric actuator platforms, such as Rotork's IQ3 range with its data logging and Bluetooth diagnostic interface, AUMA's AUMATIC actuator control units with integrated Modbus, Profibus, and HART communication, and Flowserve Corporation's Limitorque MX series with embedded performance monitoring, now provide continuous real-time data on motor temperature, torque demand, vibration, position, and operational cycle counts. This data, when streamed to plant distributed control systems or dedicated asset management platforms such as Emerson's AMS Device Manager or ABB's Ability Asset Management suite, enables maintenance teams to identify actuator degradation patterns, bearing wear, gear backlash, and seal deterioration well in advance of functional failure, enabling planned maintenance interventions that avoid unplanned production stoppages.

The business case for connected electric actuator platforms is particularly compelling in high-consequence process control environments such as oil and gas pipelines, refinery process units, and power plant auxiliary systems, where actuator failure can trigger plant shutdowns, safety system activations, or environmental releases that carry significant financial and regulatory consequences. Manufacturers that deliver integrated intelligent actuator solutions combining the hardware platform, embedded software diagnostics, and connectivity to plant digital infrastructure are gaining measurable competitive advantage over traditional equipment suppliers, and are additionally building durable aftermarket service revenue streams through extended service agreements, remote monitoring subscriptions, and digital performance analytics packages that increase customer retention and improve revenue visibility.

Functional Safety Certification and Digital Fieldbus Protocol Adoption Driving Actuator Platform Differentiation in Critical Process Applications

The growing mandated adoption of functional safety standards, specifically IEC 61508 for the safety of electrical and electronic programmable systems and IEC 61511 for process industry safety instrumented systems, is creating a structurally important tier of demand in the global electric actuators market for Safety Integrity Level certified actuator products with documented design and validation processes. In oil and gas, chemical processing, and power generation facilities, electric actuators used in safety instrumented system applications are required to meet SIL 1, SIL 2, or SIL 3 certification levels depending on the consequence severity of the associated hazardous event, driving demand for actuator platforms that combine certified hardware reliability with fault detection and diagnostic coverage capabilities that can be verified against IEC standard requirements.

Rotork's IQ3 and Skilmatic electro-hydraulic actuation range, AUMA's SA and SAR multi-turn actuators with SIL-certified documentation, and IMI plc's actuator product lines for critical service applications represent product families offering SIL-rated performance documentation in compliance with IEC 61508 and IEC 61511. The commercial importance of SIL certification is increasing as plant operators and engineering procurement and construction contractors increasingly specify safety-rated actuation in new facility designs and major plant upgrade projects, creating a clear and growing procurement differentiator that excludes lower-specification products from consideration in safety system applications.

In parallel, the progressive migration of process plants from legacy 4 to 20 mA analog signal wiring toward HART, Foundation Fieldbus, Profibus PA and DP, and increasingly toward Industrial Ethernet protocols including EtherNet/IP and PROFINET, is creating sustained demand for actuator control units that support these protocols and can participate in plant-wide digital communication networks. NAMUR Recommendation NE 107, which defines self-monitoring and diagnostics requirements for intelligent field devices including actuators, is widely adopted across European process industries and is gaining traction in North America and Asia Pacific as a standard for specifying minimum diagnostic functionality in intelligent actuator procurement. The incoming EU Machinery Regulation (EU) 2023/1230, which will replace the current Machinery Directive 2006/42/EC and enter into application in January 2027, is additionally prompting actuator manufacturers supplying European markets to review and update product conformity documentation and risk assessment processes across their full product ranges.

By Product Type: In 2026, the Multi-turn Electric Actuators Segment to Dominate the Global Electric Actuators Market

Based on product type, the electric actuators industry is segmented into multi-turn electric actuators, part-turn electric actuators, and linear electric actuators. In 2026, the multi-turn electric actuators segment is expected to account for the largest share of this market. The leading position of this segment is attributed to its established and dominant role as the primary electrically operated drive technology for gate valves, globe valves, and rising stem ball valves used extensively in oil and gas pipelines, process chemical plants, power station auxiliary systems, and water distribution networks, where multi-rotation output torques ranging from a few hundred Newton-metres to several hundred thousand Newton-metres are required to operate large-bore valves against full line pressure. The long operational service life of multi-turn electric actuator installations, combined with the large and continuously expanding installed base of rising stem valves across global process infrastructure, sustains strong replacement and upgrade procurement demand alongside new installation activity. Key manufacturers including Rotork plc with its IQ3 intelligent multi-turn range, AUMA Riester GmbH & Co. KG with its SA and SAR series, and Flowserve Corporation with its Limitorque L120 series exemplify the sustained product development investment sustaining the competitiveness of this segment.

However, the linear electric actuators segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the accelerating adoption of electric linear actuation across industrial automation and robotics applications, the rapid buildout of electric vehicle manufacturing capacity globally that requires precision linear actuators across battery module assembly, body shop automation, and end-of-line testing equipment, the growing deployment of linear electric actuators in solar photovoltaic tracker systems and wind turbine pitch control applications, and the increasing preference for clean, maintenance-friendly linear electric drive solutions in food processing and pharmaceutical manufacturing environments where pneumatic or hydraulic actuation raises contamination and hygiene compliance concerns. The IEA‑4E Electric Motor Systems policy brief notes that industrial automation and robotics are key growth areas for electric‑motor‑driven systems, including linear actuators integrated into workcells, conveyors, and assembly lines. National EV‑incentive programs indicate robotic automation and electric‑drive‑based production lines, which directly increase demand for precision linear electric actuators in battery‑cell stacking, body‑in‑white automation, and end‑of‑line testing.

By Control Type: In 2026, the On/Off Electric Actuators Segment to Hold the Largest Share

Based on control type, the electric actuators industry is segmented into on/off electric actuators, modulating electric actuators, and intelligent electric actuators. In 2026, the on/off electric actuators segment is expected to account for the largest share of this market. The growth of this segment is driven by its broad deployment across isolation valve applications throughout oil and gas, water distribution, and power generation infrastructure, where the actuator function is limited to fully opening or fully closing a valve in response to a binary control signal, and where the simplicity, reliability, and lower unit cost of on/off actuator configurations make them the predominant technology selection for the large majority of valve actuation points in any given process facility. The enormous global installed base of on/off actuated isolation valves across existing pipeline, refinery, and utility infrastructure sustains strong replacement procurement demand for this segment across all major geographies. The U.S. DOE’s Industrial Control Systems (ICS) security and modernization initiative reports that over 150 electric utilities, serving about 90 million U.S. customers, have adopted or committed to advanced monitoring and protection technologies for operational‑technology (OT) networks, including valve and actuator control systems. This modernization drive in the power, oil and gas, and water sectors increases the replacement of older pneumatic/hydraulic actuators with certified on/off electric actuators for isolation and emergency‑shutdown duties.

However, the intelligent electric actuators segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the rapidly expanding adoption of IIoT-enabled actuator platforms that provide real-time operational data, remote configurability, and predictive maintenance capabilities across process plant operations, the tightening of functional safety requirements that mandate diagnostic coverage levels achievable only with intelligent, self-monitoring actuator hardware, and the compelling total cost of ownership advantages that intelligent actuator platforms deliver relative to conventional units through extended service intervals, early fault detection, and integration with plant digital infrastructure supporting broader Industry 4.0 transformation programs.

By Voltage: In 2026, the AC Electric Actuators Segment to Hold the Largest Share

Based on voltage, the electric actuators industry is segmented into AC electric actuators and DC electric actuators. In 2026, the AC electric actuators segment is expected to account for the largest share of this market. The dominant position of this segment reflects the prevalence of standard single-phase and three-phase AC power distribution infrastructure across industrial facilities globally, which makes AC-powered actuators the default technology selection for fixed installations in process plants, power generation facilities, and water treatment works where reliable grid power is available and where the high torque output characteristics of AC induction motor drives are well-suited to the demanding duty cycles of industrial valve and damper actuation. The broad compatibility of AC actuators with established plant electrical infrastructure reduces both installation cost and engineering complexity, sustaining their dominance across the large majority of new and replacement procurement in industrial process control applications.

However, the DC electric actuators segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the expanding deployment of battery-powered and low-voltage DC actuation solutions in electric vehicle manufacturing automation, remote pipeline and infrastructure monitoring stations where grid power is unavailable, renewable energy systems including solar tracker and wind turbine applications that operate on DC power architectures, and the growing adoption of 24 V and 48 V DC-powered building automation and HVAC control systems that require compact, energy-efficient actuator solutions compatible with low-voltage DC building management system architectures.

By End-use Industry: In 2026, the Oil and Gas Segment to Hold the Largest Share

Based on end-use industry, the electric actuators industry is segmented into oil and gas, power generation, water and wastewater treatment, chemical and petrochemical processing, automotive, aerospace and defense, food and beverage processing, HVAC and building automation, and other end-use industries. In 2026, the oil and gas segment is expected to account for the largest share of this market, reflecting the status of this sector as the largest global procurer of industrial electric actuators, driven by the enormous valve count in upstream production facilities, midstream pipeline and compression systems, and downstream refinery and gas processing operations, each of which relies on electrically actuated valve control for flow regulation, isolation, emergency shutdown, and pressure management functions. The ongoing global expansion of LNG export and import terminal capacity, large-diameter gas transmission pipeline projects, and upstream production facility automation programs across North America, the Middle East, and Asia Pacific is continuously adding new actuation demand alongside replacement procurement for aging actuator systems in the existing global oil and gas infrastructure base. The IEA’s statistical publications show that global LNG export capacity has increased by 300 billion cubic meters (bcm) per year of new capacity expected to be added by 2030, with major new projects in the U.S., Qatar, Australia, and the Middle East, all of which add hundreds of control and safety valves driven by electric actuators.

However, the water and wastewater treatment segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the massive global capital investment cycle in water supply, treatment, and distribution infrastructure, fueled by population growth, urbanization, water scarcity, and the tightening of regulatory standards for drinking water quality and wastewater discharge across both developed and emerging economies. Municipal water utilities are deploying electric actuators across intake structures, treatment plant process equipment, distribution network pressure management stations, and sewage pumping and treatment facilities, where electrically actuated valve and gate control provides the remote operability and monitoring capability needed to meet modern water utility automation and resilience requirements. The growing deployment of desalination capacity across water-stressed regions including the Middle East, North Africa, and parts of Asia is additionally creating significant new demand for corrosion-resistant and marine-grade electric actuator solutions in seawater intake, pre-treatment, and brine disposal applications.

Based on geography, the overall electric actuators market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of this market. This is driven by the concentration of oil and gas production, processing, and pipeline infrastructure across the United States, Canada, and Mexico, the presence of a large installed base of aging pneumatic and electric actuator systems across chemical plants, refineries, and power generation facilities that are actively undergoing technology refresh programs, and the deep local supply base provided by leading manufacturers including Emerson Electric Co., Flowserve Corporation, Curtiss-Wright Corporation, Moog Inc., and Tolomatic, Inc. The stringent safety management requirements enforced under OSHA's Process Safety Management standard, the EPA's Risk Management Program, and the Pipeline and Hazardous Materials Safety Administration's regulations for pipeline integrity management collectively compel sustained investment in reliable, certified electric actuator platforms across North American process industries. The United States in particular benefits from strong ongoing capital spending in LNG export terminal construction, refinery modernization, and water infrastructure upgrade programs that drive consistent new installation activity for electric actuators across multiple end-use sectors. The U.S. DOE’s ICS and OT‑modernization initiative reports that over 150 U.S. utilities have adopted advanced monitoring and protection technologies for operational‑technology networks, which supports the deployment of certified electric actuators in pipeline and power‑plant safety systems. The IEA’s gas‑infrastructure tables show that U.S. LNG export capacity has more than doubled over the last decade, adding thousands of process‑control valves and supporting rapid electric‑actuator procurement in terminals and upstream/ midstream infrastructure.

However, the Asia Pacific electric actuators market is expected to grow at the fastest rate from 2026 to 2036. This is driven by the massive ongoing expansion of refinery, petrochemical, LNG, and industrial process manufacturing capacity across China, India, South Korea, Japan, and Southeast Asia, the accelerating buildout of municipal water treatment and distribution infrastructure in rapidly urbanizing economies, and the scaling of electric vehicle battery production and automotive manufacturing operations across the region that are generating substantial new demand for precision linear and rotary electric actuators. China's continuing investment in natural gas pipeline infrastructure under its national energy security program, combined with the enforcement of enhanced safety management standards for hazardous chemical facilities under the Work Safety Law amendments, is compelling large-scale adoption of intelligent and SIL-rated electric actuator platforms across Chinese process industries. India's Jal Jeevan Mission, targeting household piped water connections across rural India, and the ongoing Smart Cities Mission infrastructure program together represent a significant and time-bounded procurement opportunity for electric actuators in municipal water and wastewater treatment applications across the country.

Europe is a large and technically sophisticated market for electric actuators, supported by a robust regulatory framework encompassing the ATEX Directive 2014/34/EU for hazardous area equipment, IEC 61508 and IEC 61511 functional safety standards, the EU Industrial Emissions Directive, and the incoming EU Machinery Regulation (EU) 2023/1230, which will replace the current Machinery Directive and introduce updated safety and electromechanical equipment requirements from January 2027. European manufacturers including Rotork plc, AUMA Riester GmbH & Co. KG, IMI plc, and Festo SE & Co. KG maintain strong competitive positions in their home region and globally, supported by deep application engineering expertise and long-established relationships with major European oil and gas, chemical, and water utility operators.

The global electric actuators market is moderately consolidated at the platform level, with competition primarily driven by torque output capability, actuation speed, control precision, functional safety certification, digital connectivity features, and the strength of global distribution and aftermarket service networks. Key differentiators include the availability of explosion-proof and SIL-rated configurations certified under ATEX, IECEx, and NEC standards, the range of supported digital communication protocols, the depth of application engineering expertise across end-use industry sectors, and the geographic breadth of installation, commissioning, and maintenance service capabilities.

Large diversified industrial automation and flow control companies such as Emerson Electric Co. and ABB Ltd. compete through comprehensive electric actuator portfolios integrated within broader valve and process control automation offerings, providing customers with single-source procurement, commissioning, and lifecycle support across valve, actuator, positioner, and control system components. Dedicated actuator specialists including Rotork plc and AUMA Riester GmbH & Co. KG compete through deep actuator engineering expertise, the broadest available torque and size range coverage, and the strongest intelligent actuator platform capabilities, with Rotork having further strengthened its market position through the acquisition of complementary actuator and flow control businesses across multiple geographies. Flowserve Corporation competes through its Limitorque actuation brand alongside its broader valve portfolio, offering integrated valve and actuator procurement that simplifies engineering procurement and construction contractor sourcing. Regionally focused motion control specialists including Tolomatic, Inc. and Curtiss-Wright Corporation maintain competitive positions in North American industrial automation and precision actuation markets, while Nidec Corporation has expanded its global presence across precision motion and actuator markets through a sustained strategy of targeted acquisitions across Asia Pacific, Europe, and North America.

The report provides a comprehensive competitive analysis based on an assessment of key players' product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.

Some of the key players operating in the global electric actuators market include Rotork plc (U.K.), Emerson Electric Co. (U.S.), AUMA Riester GmbH & Co. KG (Germany), Flowserve Corporation (U.S.), ABB Ltd. (Switzerland), Siemens AG (Germany), Nidec Corporation (Japan), Parker Hannifin Corporation (U.S.), Moog Inc. (U.S.), Curtiss-Wright Corporation (U.S.), IMI plc (U.K.), Festo SE & Co. KG (Germany), SMC Corporation (Japan), Tolomatic, Inc. (U.S.), and Honeywell International Inc. (U.S.), among others.

The global electric actuators market is expected to reach USD 28.3 billion by 2036 from an estimated USD 16.4 billion in 2026, at a CAGR of 5.7% during the forecast period 2026–2036.

In 2026, the multi-turn electric actuators segment is expected to hold the largest share of this market, driven by its established dominance in rising stem valve control across oil and gas, power generation, chemical processing, and water treatment infrastructure where multi-rotation torque output is required.

The linear electric actuators segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by accelerating adoption across industrial automation, electric vehicle manufacturing, renewable energy, and food and beverage and pharmaceutical processing applications.

In 2026, the on/off electric actuators segment is expected to hold the largest share of this market, reflecting the broad deployment of binary isolation valve control applications across oil and gas, water, and power generation infrastructure globally.

In 2026, the AC electric actuators segment is expected to hold the largest share of this market, driven by the prevalence of AC power distribution infrastructure across industrial facilities globally and the high torque output characteristics of AC motor drives for industrial valve and damper actuation.

In 2026, the oil and gas segment is expected to hold the largest share of this market, reflecting the status of this sector as the largest global procurer of industrial electric actuators across upstream, midstream, and downstream operations.

The growth of this market is primarily driven by the accelerating displacement of pneumatic and hydraulic actuator systems by electric alternatives, growing global investment in water and wastewater treatment infrastructure, the rapid expansion of LNG and oil and gas processing capacity across Asia Pacific and the Middle East, the integration of IIoT connectivity and predictive diagnostics in intelligent actuator platforms, the tightening of functional safety standards under IEC 61508 and IEC 61511, and the growing adoption of electric actuators in renewable energy and electric vehicle manufacturing applications.

Key players in the global electric actuators market include Rotork plc (U.K.), Emerson Electric Co. (U.S.), AUMA Riester GmbH & Co. KG (Germany), Flowserve Corporation (U.S.), ABB Ltd. (Switzerland), Siemens AG (Germany), Nidec Corporation (Japan), Parker Hannifin Corporation (U.S.), Moog Inc. (U.S.), Curtiss-Wright Corporation (U.S.), IMI plc (U.K.), Festo SE & Co. KG (Germany), SMC Corporation (Japan), Tolomatic, Inc. (U.S.), and Honeywell International Inc. (U.S.).

Asia Pacific is expected to register the highest growth rate in the global electric actuators market during the forecast period 2026–2036, driven by accelerating expansion of oil and gas processing, water treatment, and industrial manufacturing capacity, the scaling of electric vehicle production facilities, and the enforcement of enhanced safety and environmental regulations across the region's large industrial sector.

Published Date: May-2026

Published Date: May-2026

Published Date: May-2026

Published Date: May-2026

Published Date: May-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates